jejim

The Semiconductor Expertise Scarcity

The semiconductor trade is predicted to grow to be a trillion-dollar trade by 2030. In accordance with McKinsey analysis, the trade might develop 6%-8% a 12 months as much as 2030. The expansion of the trade is pushed by megatrends that embody IoT good units, the expansion of AI, and growing demand for robotics and autonomous autos.

Nevertheless, this development additionally creates a big problem for the trade: the scarcity of expert expertise. According to Deloitte, the trade will want greater than 1 million further staff by 2030, including greater than 100,000 per 12 months. However discovering and retaining certified candidates isn’t simple, as there will not be sufficient graduates and trade competes with different sectors for expertise. To place this in perspective, there are lower than 100,000 graduate college students in electrical engineering and pc science in the US yearly.

That is the place Synopsys (NASDAQ:SNPS) is available in to assist the trade overcome this problem. On this article, we’ll discover how Synopsys is boosting engineering productiveness and dashing up chip design for semiconductor firms, and the way it’s increasing the EDA market alternative past the present projections. We will even analyze Synopsys development trajectory and valuation based mostly on its elevated market potential.

Synopsys Outgrowing the EDA Market

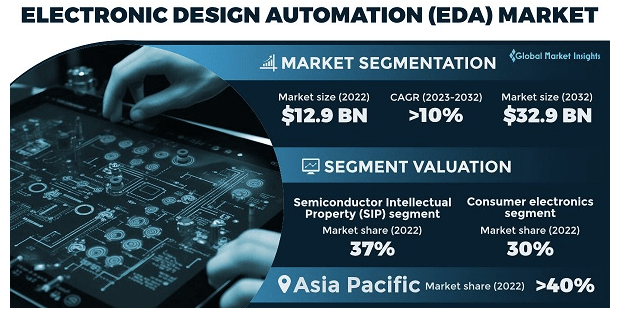

In accordance with a report by Global Market Insights, The Digital Design Automation (EDA) market measurement is predicted to develop from $13 billion in 2022 to USD $33 billion by 2032, at a CAGR of 10% through the forecasted interval.

EDA Market Dimension (World Market Insights)

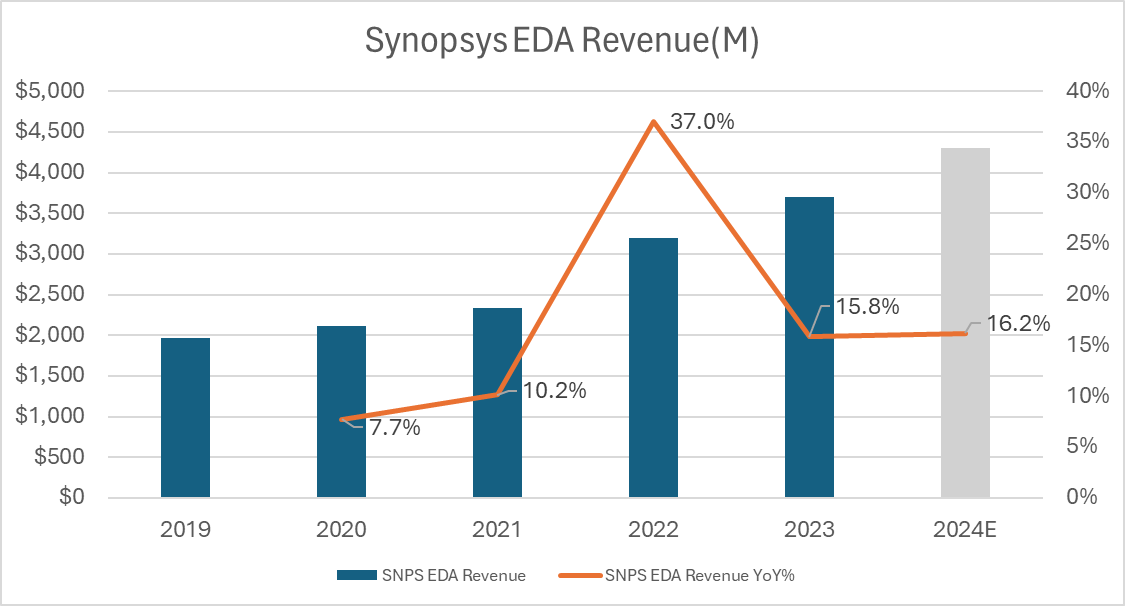

The EDA market is a specialised phase of the broader semiconductor market, with few rivals. Synopsys is the EDA trade chief with a 32% market share, adopted by Cadence, which has 30% market share. The attention-grabbing level right here is that Synopsys EDA has began to outgrow the EDA market since 2022 as you may see beneath.

Synopsys EDA Income (Writer)

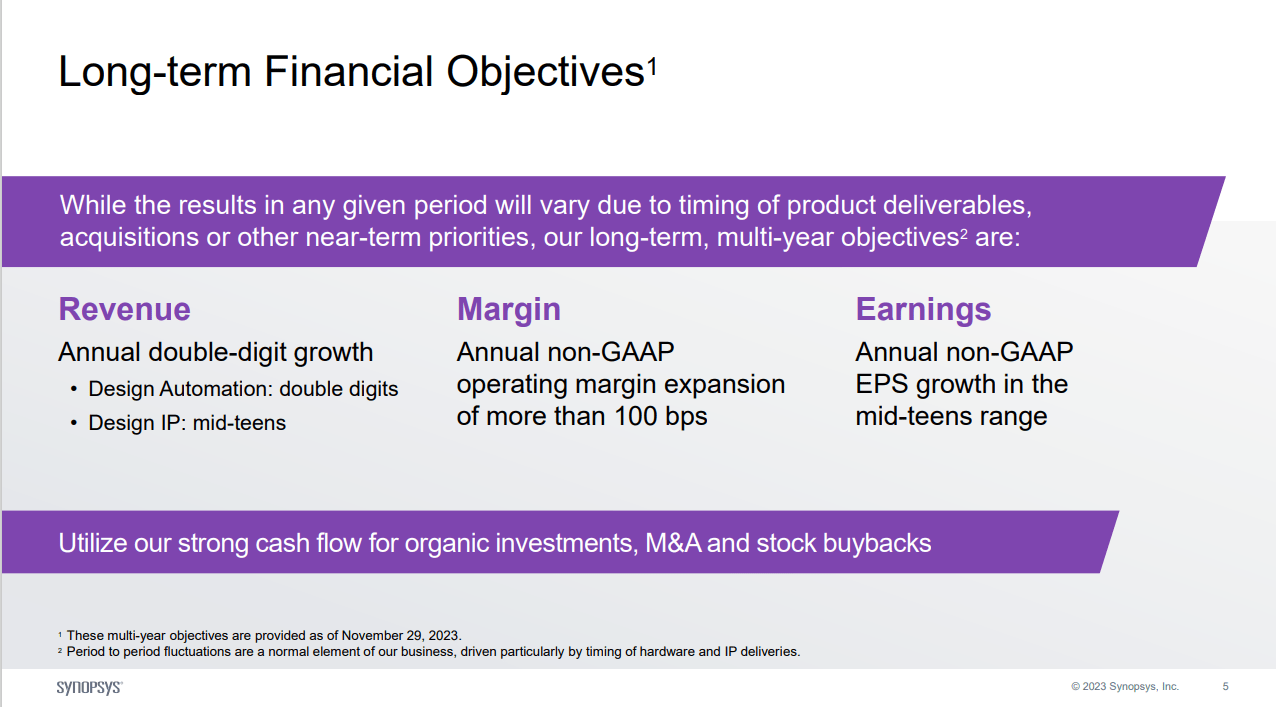

Synopsys can be guiding that their EDA phase will develop double digits on the long run (see beneath). Our view is that the present EDA market development projections of 10% don’t replicate the potential of Synopsys to increase the EDA market.

SNPS Lengthy Time period Targets (Synopsys This fall Earnings Presentation)

Synopsys.ai: A Recreation-Changer for the EDA Trade

Because the semiconductor trade faces a worldwide expertise scarcity and an increase in chip design complexity and price, Synopsys has launched Synopsys.ai, the AI-powered EDA suite for chipmakers. What we’re listening to from public sources is that Synopsys.AI product has gained plenty of recognition and is in nice demand. Clients are witnessing impressive results, resembling 3x enchancment in design productiveness, 10x enhancement in verification course of, and energy reductions as much as 15%. Its newest device Synopsys.ai Copilot has been adopted by a number of the world’s main chip firms, resembling AMD and Intel, who’ve reported vital enhancements of their chip design outcomes.

By automating and optimizing many points of chip design, we expect that Synopsys.ai is altering the sport for the EDA trade. We additionally suppose that this product has enabled a brand new incremental TAM for Synopsys which is way larger than what’s being estimated in the present day. Synopsys.ai is creating a brand new paradigm for the EDA market and positioning Synopsys because the chief in AI-driven chip design.

Our assumption is that Synopsys.ai product will drive elevated demand for EDA instruments by enabling new AI-powered capabilities and use circumstances. We estimate that it might increase the EDA market measurement as much as $43 billion by 2032, from the present projection of $33 billion. This might suggest a CAGR of 13% for the EDA market, in comparison with the present estimate of 10%. This might additionally suggest the next development price for Synopsys, because the EDA market chief.

Synopsys Financials and Income Trajectory

On November 29, 2023, Synopsys introduced strong Q4 results, which exceeded analysts’ forecasts. The corporate reported income of $1.59 billion, a 25% enhance from the identical interval final 12 months and non-GAAP EPS of $3.17, up 66% year-over-year. Firm additionally reported $8.6 billion non-cancellable backlog, which means power of its enterprise. Synopsys guided Q1 FY 2024 income above consensus: to be between $1.63 to $1.66 billion and non-GAAP EPS to be between $3.40 to $3.45.

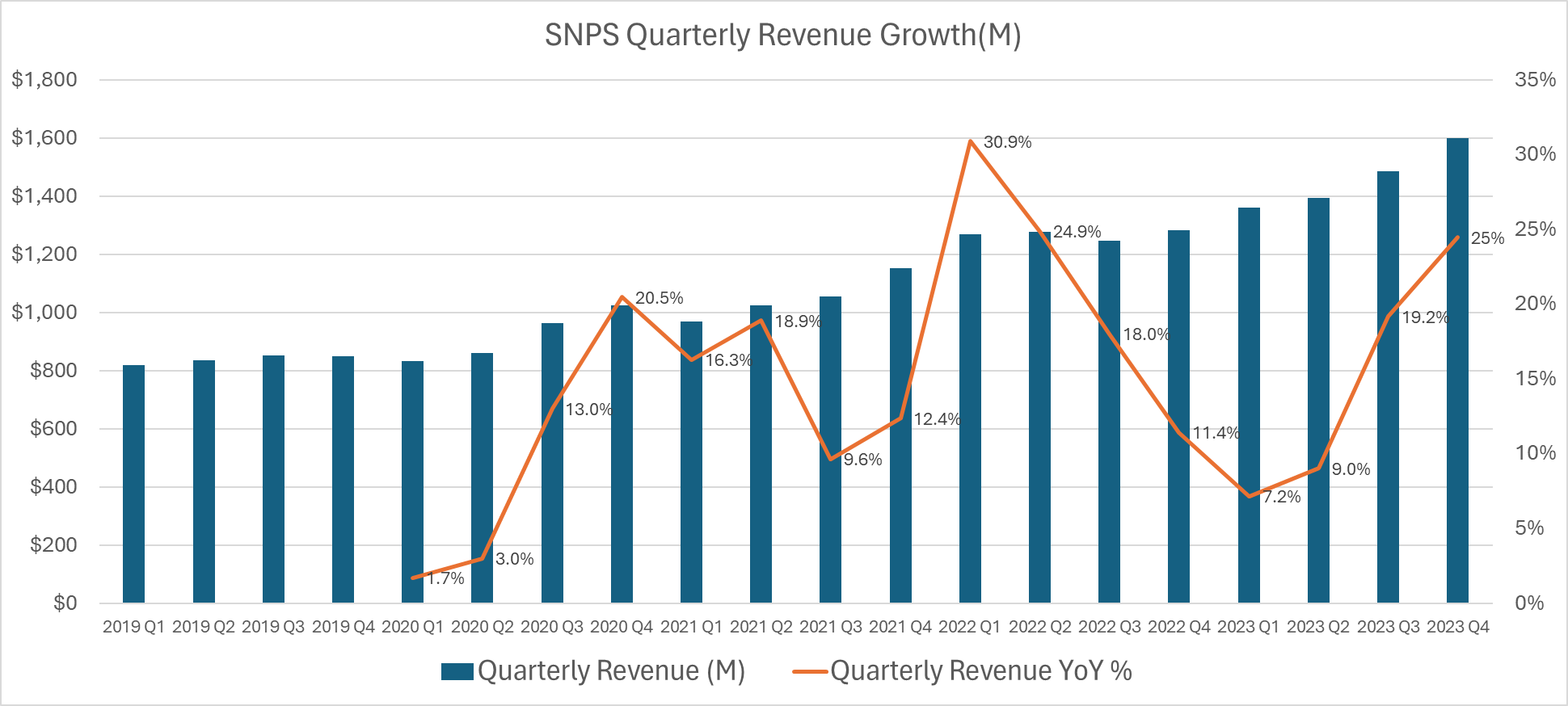

Synopsys has 3 enterprise segments that are EDA, Design IP and Software program Integrity. Synopsys.ai, is a part of the EDA phase which generated income of $3.7 billion (16% YoY) and accounted for 63% of Synopsys’ whole FY 2023 income (EDA is the most important phase of Synopsys). If we take a look at the Synopsys income efficiency beneath, we will see a development surge from FY2022 This fall onwards. We attribute this surge to the launch of Synopsys.ai, and we anticipate that this development pattern will proceed for the foreseeable future.

SNPS Quarterly Income (Writer)

Synopsys Valuation

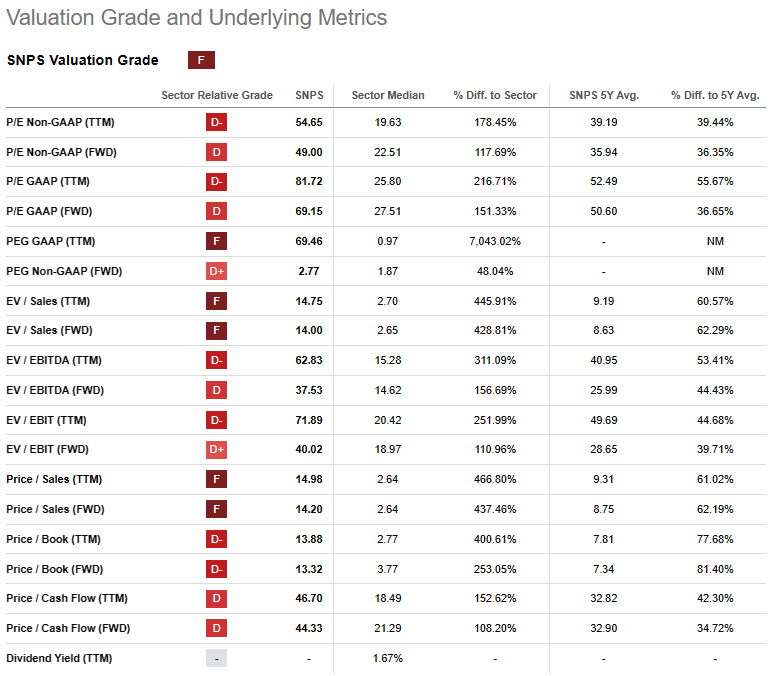

Synopsis is an costly inventory. Its market cap is $82.6 billion, and its gross sales and earnings multiples are fairly excessive in comparison with its friends and trade averages. It has a P/E ratio of 81, and a P/S ratio of 15. Our view is that Synopsys’s excessive valuation displays its robust development prospects, market management, and innovation potential, particularly with its latest launch of Synopsys.ai.

SNPS Valuation Metrics (Searching for Alpha)

Synopsys has a excessive valuation, however we consider that its income development momentum will proceed within the coming years.

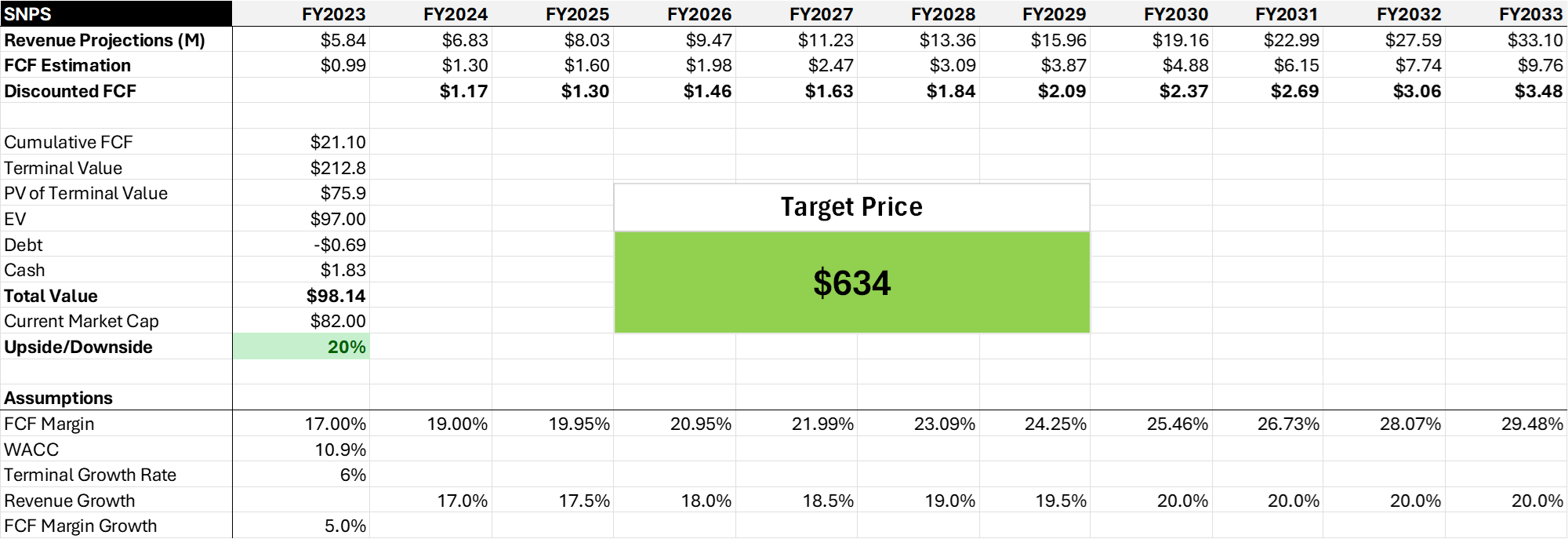

We carried out a DCF evaluation to estimate the honest worth of Synopsys in case of such income acceleration. We use a ten.9% WACC to low cost the long run money flows. We assume $6.83 billion as FY2024 income and 19% because the FY2024 FCF margin. We mission a gradual income development enhance as much as 20% by FY 2030. This offers us 19% CAGR which is greater than the EDA market development as we consider that Synopsys will develop above the market price and in addition acquire market share. Furthermore, we apply a 6% terminal development price after the 10-year interval.

Our mannequin additionally assumes a 5% annual enhance in FCF margin, according to the present working margin trajectory.

Be aware: Firm income steering for FY 2024 is $6.6 billion midpoint (13% YoY), which we expect could be very conservative contemplating the expansion momentum and the $8.6 billion backlog they’ve. We’re forecasting 17% development for FY2024 in our mannequin.

SNPS DCF Mannequin (Synopsys)

In accordance with our DCF calculations, the honest worth of Synopsys enterprise is $98 billion. This valuation implies a 20% upside potential for the inventory, suggesting a goal worth of $634.

Dangers

We see the next dangers for Synopsys valuation:

- Volatility within the international economic system and the semiconductor trade: Synopsys operates in a cyclical and risky trade that’s affected by varied macroeconomic and geopolitical elements, resembling financial recessions, commerce disputes, provide chain disruptions, and regulatory modifications. These elements could negatively have an effect on the corporate’s enterprise.

- IP violation claims and litigations: Synopsys operates in a extremely aggressive and progressive trade that entails advanced and evolving IP rights. The corporate could face claims or lawsuits from its opponents, or third events alleging that its services or products violate their patents, logos, or different IP rights. Any such declare or litigation might lead to vital authorized charges or damages.

Conclusion

A dominant place within the EDA market, a broad portfolio IP, a robust give attention to AI-powered chip design, and an increasing TAM positions Synopsys as an EDA chief within the good all the pieces period.

Taking a look at Synopsys’ monetary efficiency additionally reveals a constant development pattern. Our DCF valuation estimates that Synopsys has an intrinsic worth of $634. Regardless of the latest surge in its inventory worth, we consider that it has extra upside based mostly on our valuation metrics.

We price Synopsys as a Purchase.