TERADAT SANTIVIVUT

By Raffaele Savi and Jeff Shen, PhD

As we glance forward, our systematic evaluation continues to help the case for an eventual “soft landing” financial situation, the place inflation falls to central financial institution targets with out inflicting a recession.

However the macroeconomic and market backdrop isn’t with out uncertainty, and there are a number of unknowns going through fairness buyers within the months forward. What are the implications of policymakers approaching the slicing cycle with warning? Is all of the constructive macro information priced in after the latest rally, or is there extra room for equities to run? And are there any alternatives or dangers that markets is probably not absolutely pricing? On this outlook, we take a data-driven method to answering these questions and talk about how they’re influencing our portfolio positioning within the months forward.

Tender touchdown nonetheless on observe… however will the Fed fall behind the curve?

In latest months, declines in official inflationary knowledge, largely pushed by items costs have more and more aligned with our view {that a} mushy touchdown is enjoying out. Now, the query is whether or not financial coverage will sustain with how the macro backdrop has been evolving.

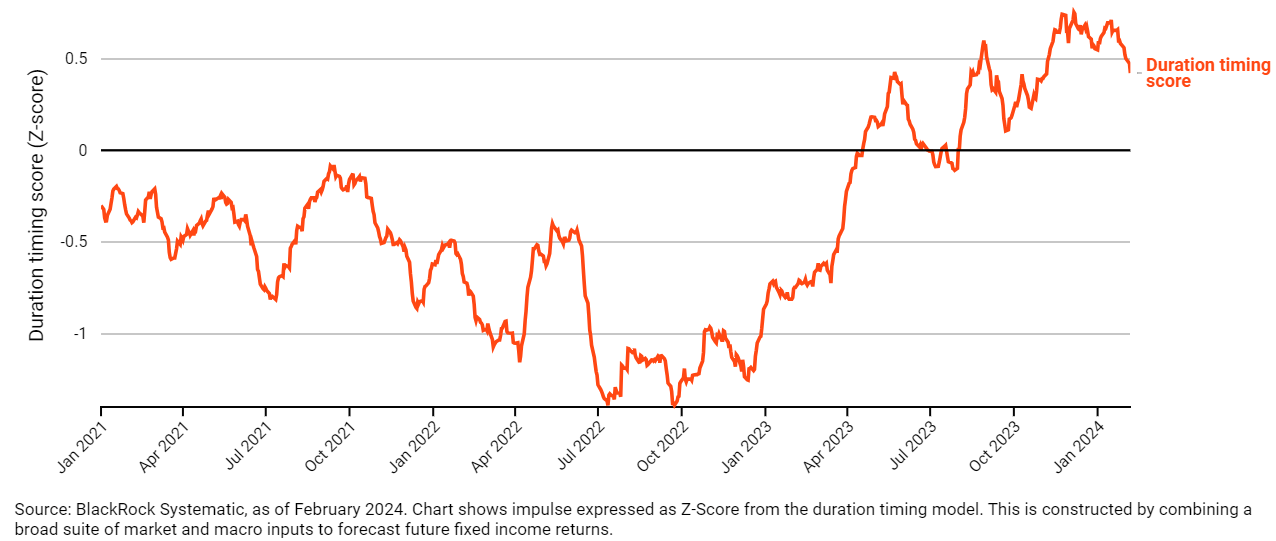

Determine 1 exhibits our systematic period timing mannequin, which makes use of a mix of real-time financial, coverage, and market indicators to forecast the route of rates of interest. The mannequin turned constructive on bonds (charges falling) as inflation quickly declined, and coverage sentiment turned more and more dovish during the last six months. Whereas the mannequin stays lengthy period, largely pushed by inflation dynamics, latest pushback from Chair Powell on the timing of the primary price lower has decreased the extent of conviction in that view. And since markets proceed to cost in vital expectations for price cuts later this yr, the Fed’s cautiousness towards a backdrop of continued financial resilience raises the likelihood that financial coverage will lag each the tempo of disinflation and market expectations for price cuts. Because of this, the potential for a rising disconnect between inflation and coverage dynamics is changing into more and more necessary in our mannequin.

Determine 1: Length timing mannequin factors to downward stress on yields, however coverage sentiment is pushing again on that view

Length timing mannequin (constructive: yields down, detrimental: yields up)

Extra room for equities to cost in disinflation

For fairness buyers, the tempo of disinflation and energy of the latest fairness market rally raises the query of whether or not all of the potential “good news” on the financial system is already mirrored in market pricing.

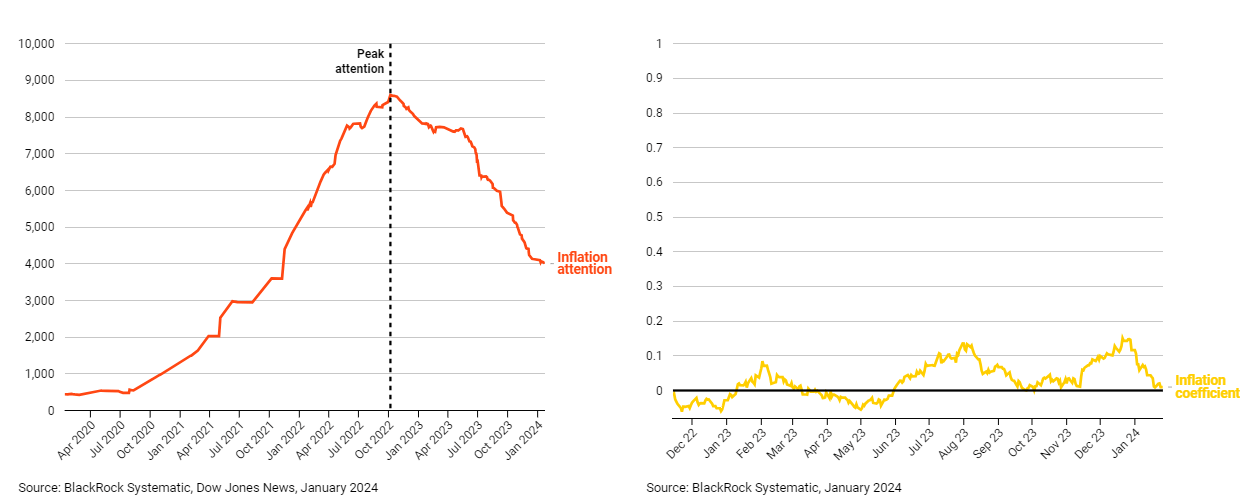

To reply this, we study the energy of the cross-sectional market rotation noticed since consideration to greater inflation versus decrease inflation peaked in This autumn 2022 and examine these strikes with what can be required to return pricing absolutely to the final level at which inflation dynamics appeared regular. We used this identical conceptual framework throughout the COVID-19 reopening part to find out whether or not the market had rotated sufficient following the value actions noticed throughout the earlier lockdown interval. Determine 2 exhibits the energy of the rotation within the interval since consideration to greater inflation peaked, as measured by the coefficient (a coefficient of 1 would suggest {that a} rotation has absolutely taken place). We discover that near not one of the cross-sectional worth motion that came about throughout the abnormally excessive inflation interval has since reversed – even with peak worth pressures far behind us and substantial progress on inflation normalization.

This implies that markets could also be behind in pricing the magnitude of latest declines in inflation and presents a possibility to generate alpha within the cross-section of markets as pricing dynamics reverse.

Determine 2: The decline from peak inflation consideration hasn’t coincided with a reversal of cross-sectional worth motion

Left chart: Information articles discussing “high” versus “low” inflation, Proper chart: Inflation rotation coefficient (1 = full rotation)

Assessing international fairness alternatives and dangers

Past the constructive macroeconomic backdrop that has remained a key focus of markets, there’s a vary of different alternatives and dangers influencing our international fairness views and positioning. On this part, we’ll cowl two of those matters – our method to navigating the Pink Sea disaster and the evolving outlook for China.

1. Mapping the impression of Pink Sea dangers

Provide chain disruptions and transport curtailment pushed by the Pink Sea disaster have the potential to affect cross-sectional pricing dynamics and will pose an upside danger to inflation ought to they proceed to escalate.

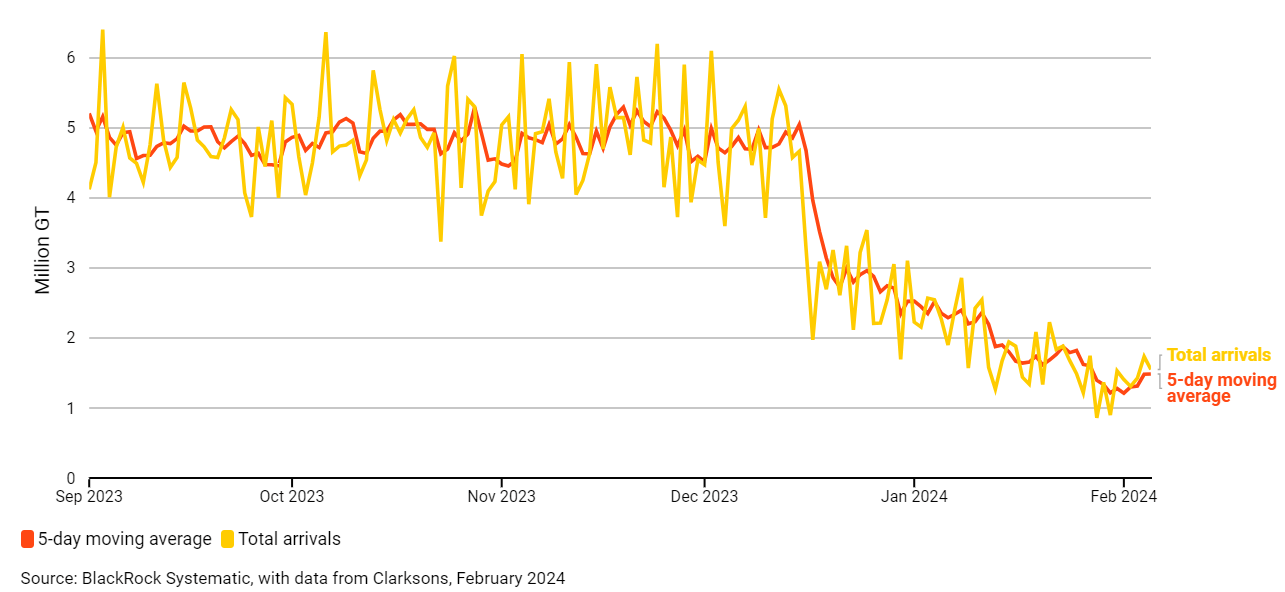

Determine 3 exhibits how greater frequency transport knowledge helps us intently monitor the evolving disaster and what it might imply for the worldwide financial system and markets in real-time. At a excessive stage, the five-day shifting common of vessel arrivals to the Gulf of Aden is now 68% beneath 2023 common ranges when it comes to gross tonnage. Wanting on the particulars, we see disruptions which have been first concentrated in containerships (largely transporting items) and automotive carriers, now more and more affecting ships carrying oil, meals, and gasoline. This has coincided with a major escalation of assaults in latest weeks.

Determine 3: Delivery knowledge supplies real-time perception into evolving Pink Sea dangers

Vessel arrivals to Gulf of Aden in gross tonnage

We complement our suite of in-house knowledge sources with perception from an elite panel of material consultants often called “superforecasters” who’ve a confirmed observe document of forecasting geopolitical occasions with a excessive diploma of accuracy. These professional views have validated our evaluation that Pink Sea dangers are accelerating and never absolutely mirrored in market pricing.

In mapping these dangers to firm exposures, giant language fashions permit us to leverage the large quantity of textual content that tends to encompass market-relevant themes – together with information articles, convention name transcripts, and dealer stories – to create bespoke fairness baskets. Used alongside the above insights, this textual content evaluation helps to uncover even essentially the most refined firm connections that inform our lengthy and brief safety positioning. Our evaluation means that sure retail, automotive, manufacturing, and airline corporations are most susceptible to ongoing challenges, whereas sure freight and logistics and power corporations might expertise tailwinds.

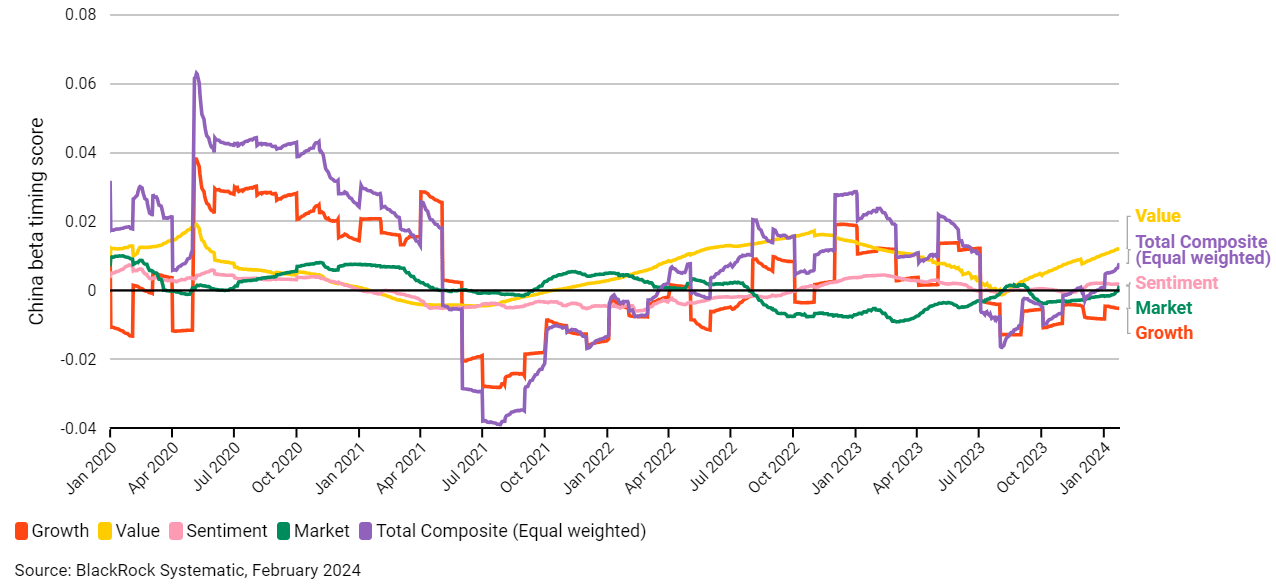

2. Reassessing the China alternative

Alongside the nation dimension, Chinese language equities struggled in 2023 as sentiment continued to deteriorate. Nonetheless, indicators of Chinese language policymakers aiming to shift that narrative have been surfacing in latest weeks with extra pro-growth/pro-market actions and a change within the tone of coverage bulletins. Our systematic timing mannequin for China has just lately turned constructive, pushed largely by valuation and sentiment insights (Determine 4). Given how detrimental sentiment and positioning have been, a continuation of those tendencies may doubtlessly current alternatives for buyers who’re contemplating including China publicity.

Determine 4: Systematic fashions have turned constructive on China relative to latest historical past

China beta timing rating

Placing all of it collectively

Our conviction within the mushy touchdown final result and the chance to take advantage of associated fairness pricing dynamics stays intact. By way of broad portfolio positioning, our largely pro-risk stance is mirrored in a good outlook for cyclical worth throughout shopper discretionary and industrial sectors. On the identical time, period timing insights referenced above stay supportive of rate-sensitive progress exposures inside the info know-how sector – albeit to a lesser diploma than on the finish of 2023.

Whereas the tempo of disinflation ought to permit expectations for price cuts in 2024 to play out, the timing and magnitude of cuts stays much less sure. Moreover, we’re intently monitoring market-relevant dangers, together with macroeconomic and geopolitical uncertainty. Our systematic method to navigating these dynamics helps us stay nimble in harnessing rising alpha alternatives and managing dangers.

This post initially appeared on the iShares Market Insights.