Anna Moneymaker

Introduction

In my previous article published on August 7th, 2023, I used to be bullish on T-Cellular (NASDAQ:TMUS). On the time, I seen the corporate’s sooner development to be the most important issue behind the purchase score. T-Cellular was rising at a considerably sooner velocity than business friends, AT&T (T) and Verizon (VZ). On the time, I argued {that a} sooner buyer acquisition tempo was probably the results of higher service and worth proposition relative to its rivals. In the present day, regardless of a few 19.44% rise in inventory for the reason that publication of my earlier article, I proceed to face by my earlier thesis—T-Cellular’s sooner buyer acquisition development isn’t but challenged, which has the potential to create a continued optimistic flywheel impact. As well as, the corporate may gain advantage from a optimistic macroeconomic tailwind that has been forming in latest months because the federal funds fee probably declines and an curiosity expense burden lightens. Due to this fact, I proceed to consider that T-Cellular is a purchase.

Argument

T-Cellular’s buyer acquisition fee continues to dwarf its rivals. As talked about in my earlier article, T-Cellular reported a web postpaid cellphone provides of 1,298 thousand whereas AT&T and Verizon added 750 thousand and detrimental 399 thousand, respectively, by the tip of 2023Q2, which showcased T-Cellular’s dominance over its rivals. Thankfully for the corporate, this development has continued all through 2024, persevering with to cement T-Cellular because the business chief when it comes to buyer acquisition. For the total yr 2023, T-Cellular’s whole postpaid web buyer addition was 5,700 thousand or 5.7 million whereas AT&T reported 1,700 thousand or 1.7 million and Verizon reported 132 thousand buyer losses for the yr. As such, it’s clear that T-Cellular is main its rivals in buyer acquisitions reflecting the higher attraction to prospects.

I consider this to be vital. Not solely does this knowledge painting that T-Cellular’s development will persist via sooner enlargement, however I consider it additionally implies that the customers consider T-Cellular’s companies provide a greater worth proposition. Shoppers are logical. Why would customers flock to T-Cellular over different rivals in a mature business? Due to this fact, because of this, I consider the present trajectory of T-Cellular’s sooner buyer acquisition fee might proceed for the foreseeable future. All through 2023, there have been no indicators of T-Cellular’s buyer acquisition fee slowing.

Quicker buyer acquisition probably helps a extra premium valuation as it is going to be mentioned later within the article. However, past a valuation perspective, I additionally consider that T-Cellular, from a elementary stage, might see a flywheel impact via this rising buyer base.

The Telecommunications business has a low churn fee. Within the case of T-Cellular, the corporate reported a 2023 churn fee of 0.87%, which in response to the administration workforce is the “lowest in the company history.” From the floor, we already see the advantage of buyer development. The lifetime worth of the group of latest prospects might be vital as they don’t simply go away T-Cellular for its rivals. Past this reasoning, T-Cellular may also upsell or cross-sell amongst a bigger buyer base bettering the corporate’s backside line, which is already the case for the corporate.

Due to this fact, T-Cellular’s continued stronger buyer acquisition fee relative to its business friends is a big tailwind for the corporate because it presents the corporate a larger loyal buyer base with a chance to cross-sell and upsell.

Administration Workforce’s View

T-Cellular’s administration workforce’s view and technique additional assist my argument. In the course of the Media, Internet & Telecom Conference hosted on March 11 by Deutsche Financial institution (DB), T-Cellular’s administration workforce has mentioned that the corporate’s “strategy has been a land-and-expand strategy” in growing ARPU or common income per person to in the end broaden margins and income. To attain this measure, the corporate mentioned that it’s going to proceed attracting new prospects with a powerful worth proposition whereas additionally providing premium and better margin plans for cross-selling alternatives. That is consistent with my view of a optimistic flywheel impact taking form because of a sooner buyer acquisition fee. Thus, I consider the path the corporate is taking to be correct, which might probably proceed to permit the corporate to attain a sooner buyer acquisition development fee for the foreseeable future.

Macroeconomic Tailwind on Steadiness Sheet

T-Cellular is predicted to see a macroeconomic tailwind within the coming few quarters. The Federal Reserve, through the December 2023 FOMC meeting, has mentioned that the group is anticipating to chop the federal funds fee by 3 times in 2024. Then, in the entire following FOMC so far, together with the FOMC meeting in March, the group has continued to counsel that there shall be three fee cuts in 2024 adopted by one other three fee cuts in 2025. As that is the bottom case, I consider it’s cheap to imagine a big federal funds fee minimize within the coming few quarters, which can lighten the curiosity expense burden for T-Cellular as market rates of interest decline.

T-Cellular at the moment has $71.399 billion in long-term debt leading to a web curiosity expense of $864 million for the quarter, which leads to about 4.84% annualized curiosity expense for the quarter, and within the 10-Ok, the corporate’s administration workforce mentioned that the corporate incurred a “higher interest expense, primarily due to higher average debt outstanding and a higher average effective interest rate” at the same time as many of the firm’s excellent debt is in fixed-interest fee. Thus, a significant decline within the federal funds fee from the present 5.25-5.50% to about 4.5-4.75% in 2024 and about 3.75-4.0% in 2024 might act in favor of T-Cellular by reducing the curiosity expense on the corporate’s debt burden.

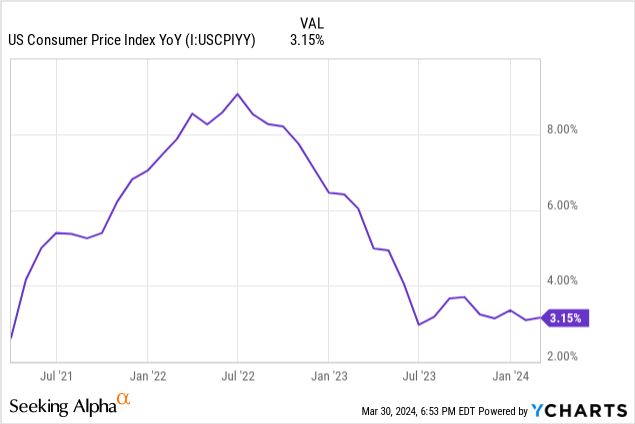

I consider the idea of the reducing rate of interest implied by the Federal Reserve is cheap provided that the CPI data has been trending down towards the two% goal fee for the previous a number of quarters. Because the chart beneath reveals, for the reason that peak of the inflation fee in mid-2022, the inflation has declined to three.15%. One might surprise if inflation is coming down to focus on prompting the Federal Reserve to chop charges because the CPI knowledge reveals that it has not been capable of fall beneath the three% stage. Whereas it is a legitimate level of concern, I don’t suppose that it’s going to trigger a reverse within the Federal Reserve’s tone in the direction of the federal funds fee minimize as a result of the bulk of the present inflation is pushed by housing. The CPI reveals that the worth of fabric items excluding meals and power fell 0.3% year-over-year whereas companies much less power noticed a 5.2% development year-over-year pushed by the shelter price enhance of 5.7%. As such, it’s evident that the present stage of inflation is pushed primarily by the rise in shelter prices, and since the financial coverage of excessive curiosity didn’t settle down the housing market prior to now few years. I don’t suppose that the Federal Reserve will wait till the housing costs cool as that is the results of the bodily supply shortage of housing in the US. Due to this fact, I consider it’s cheap to imagine that the Federal Reserve will decrease the federal funds fee within the coming few quarters via 2025 making a optimistic tailwind for T-Cellular by lowering the curiosity burden on its debt.

[Chart created by author using YCharts]

Financials

Lastly, T-Cellular’s monetary efficiency has been seeing sturdy enchancment in latest quarters as nicely. Wanting on the 2023Q4 earnings report, it might be seen that T-Cellular’s backside line has seen a stark enchancment from the prior yr. The corporate’s web earnings elevated to $2.014 billion from $1.477 representing a few 36.36% year-over-year development. The sturdy enchancment within the web earnings was a results of growing margins pushed by operational efficiencies and better ARPA, common income per account. The Adjusted EBITDA noticed a few 5.8% enhance year-over-year from $6.828 billion to $7.224 billion whereas the free money stream margin noticed a rise from 14.1% to 26.8%. These metrics, a results of the land and broaden technique, have been positively affected by the rise in ARPA from $137.92 in 2022Q4 to $140.23 in 2023Q4 seeing an about 1.7% enhance year-over-year. Total, T-Cellular’s bottom-line has been seeing a stark enchancment prior to now yr with a continued sturdy expectation. The corporate is anticipating the adjusted free money stream to see about 22% year-over-year in 2024 persevering with the sturdy momentum that was seen in 2023. Due to this fact, T-Cellular’s monetary efficiency is wholesome with an expectation for these tendencies and trajectory to proceed for the foreseeable future.

Danger: Valuation

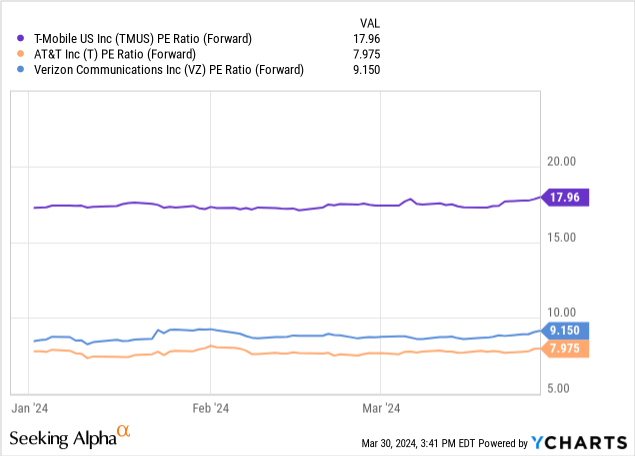

The largest threat to my bullish thesis comes from T-Cellular’s premium valuation. T-Cellular’s ahead price-to-earnings a number of, because the chart beneath reveals, is 17.96, which is about double that of AT&T and Verizon at 7.975 and 9.150, respectively. Additional, T-Cellular boasts this premium valuation a number of even whereas the corporate isn’t paying engaging dividends like AT&T and Verizon. As such, I consider it’s cheap for some traders to level out that T-Cellular’s valuation is dear posing a big threat to the shareholders. Nonetheless, I wish to argue in any other case as I consider that the corporate’s premium valuation is justified.

[Chart created by author using YCharts]

First, as talked about within the earlier portion of the article, T-Cellular boasts a considerably stronger buyer acquisition fee. The corporate is proving that T-Cellular’s attraction to prospects is best relative to its rivals by showcasing higher development for the previous a number of years.

Second, T-Cellular is anticipating to see a a lot stronger bottom-line and top-line development for the foreseeable future in comparison with its rivals. For the fiscal year 2024, T-Cellular is anticipating a bottom-line development of 20.52% adopted by 25.35% development in 2025. Nonetheless, AT&T and Verizon expect a bottom-line development of -8.43% and -2.64% within the fiscal yr 2024 adopted by 3.69% and a pair of.43% within the fiscal yr 2025, respectively. Additional, whereas AT&T and Verizon expect round 1% top-line development for each 2024 and 2025, T-Cellular’s top-line development expectation is round 3%.

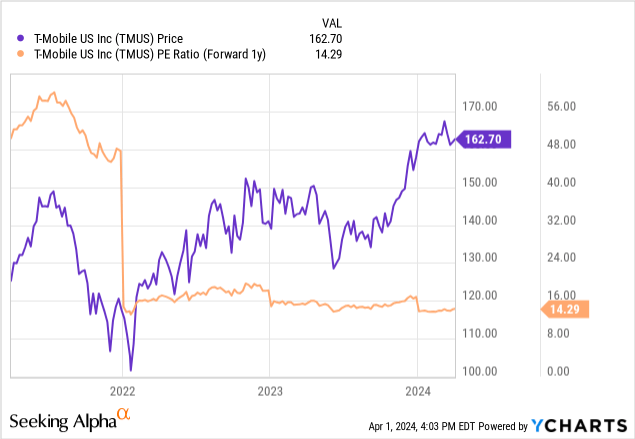

Thus, T-Cellular, in my view, ought to obtain a valuation premium relative to its business friends; nevertheless, to what extent ought to this premium valuation be justified? Because the chart beneath reveals, whereas T-Cellular’s inventory worth noticed a big enhance over the previous few years, the corporate’s ahead price-to-earnings a number of has been contracting as the corporate has reached profitability and stability. Excluding the dramatic adjustment within the ahead valuation multiples earlier than 2023 the corporate’s ahead valuation a number of has been buying and selling close to the 15-19 vary. Due to this fact, provided that the present ahead valuation a number of of 17.96 is inside the historic vary, I consider the present valuation is inside an inexpensive vary.

[Chart created by author using YCharts]

Total, I consider the mix of a sooner buyer acquisition fee together with stronger high and bottom-line development is an element supporting T-Cellular premium valuation. Whereas the corporate doesn’t pay its traders dividends, the corporate presents a considerably sooner bottom-line development fee. Nonetheless, traders ought to proceed to observe T-Cellular’s buyer acquisition charges and bottom-line development charges because the deterioration in these metrics might break the argument justifying the corporate’s premium valuation.

Abstract

I consider T-Cellular is engaging regardless of the corporate’s inventory worth seeing a few 19.44% appreciation for the reason that publication of my earlier article. T-Cellular continues to steer the business in buyer acquisition charges whereas the macroeconomic tailwind is probably impending from the federal funds fee minimize lightening the curiosity expense burden. Additional, though T-Cellular boasts a premium valuation in comparison with its business friends, I consider this to be justified as the corporate is predicted to develop sooner in all metrics together with top-line, bottom-line, and buyer acquisition fee. Due to this fact, I’m sustaining a purchase score on T-Cellular.