MicroStockHub

Virtually as if a swap was pressed, the NASDAQ Composite (COMP.IND) – which encapsulates nearly all Nasdaq-listed shares – collapsed 1.63% on the primary day of buying and selling from the highs of 2023. This was the 4th-worst begin to a brand new 12 months since 1972 and solely the fifth time {that a} 12 months began with a one-day drop of greater than 1.5%. Within the first week of the 12 months, the index fell one other 1.64%.

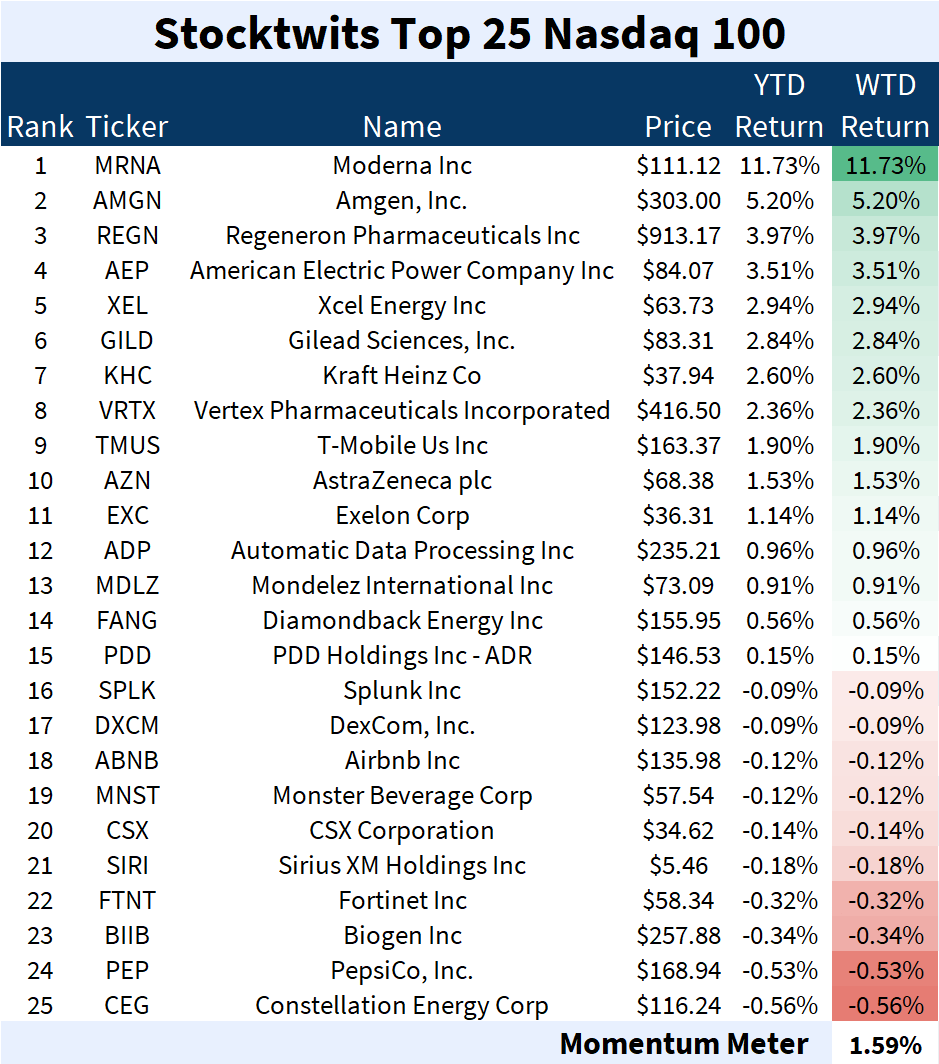

Throughout the “tech-heavy” NASDAQ 100-Index (NDX), prescription drugs dominated the roost by way of momentum; tech was just about nowhere to be seen within the Prime 25 checklist – an enormous shift in developments seen in Q3 and This autumn of 2023.

Supply: StockTwits

In holistic phrases, the index is not rising: the one-day drop for the Nasdaq-100 within the new 12 months was 1.68%. As of the primary week of the 12 months, the index shed one other 1.44%.

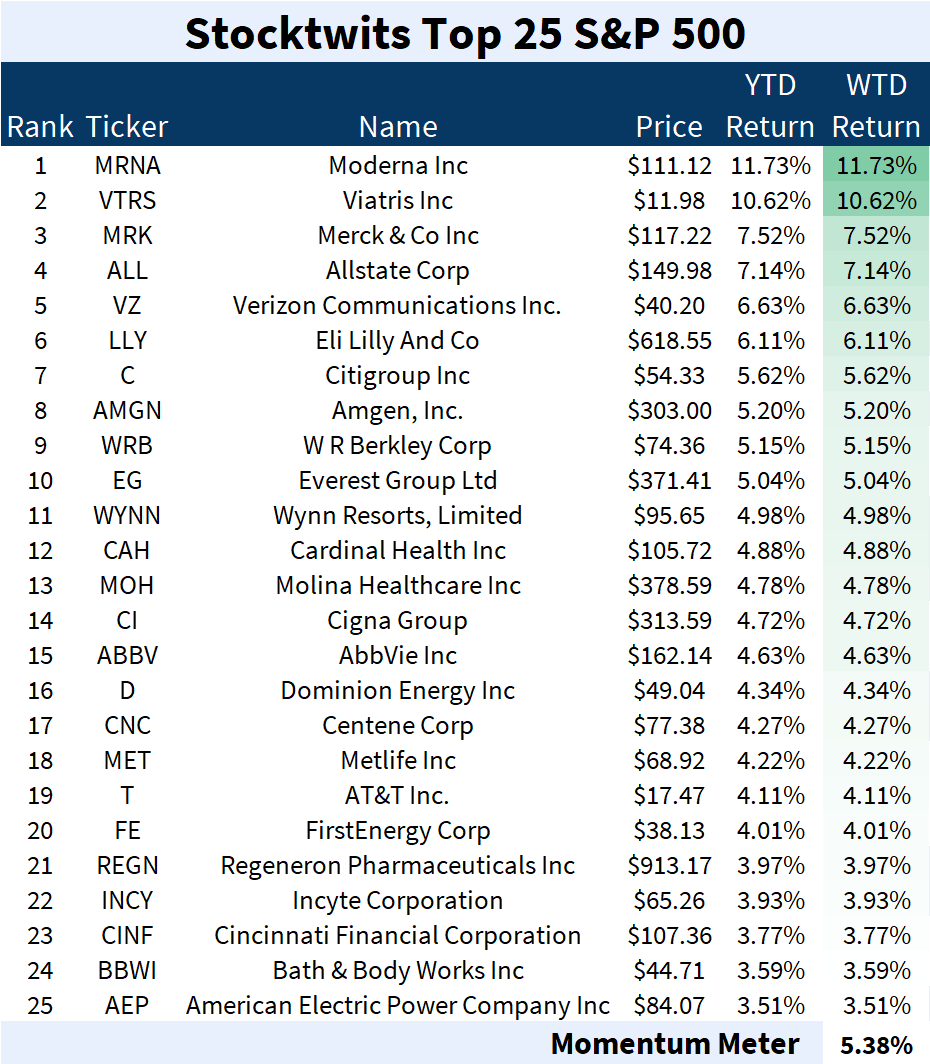

The “broad market” S&P 500 (SPX in index type and SPY in ETF type) was comparatively muted: its one-day drop within the new 12 months was 0.57% and it dropped one other 0.96% within the first week of the 12 months. Prescribed drugs and monetary companies dominated the roost within the Prime 25 checklist.

Supply: StockTwits

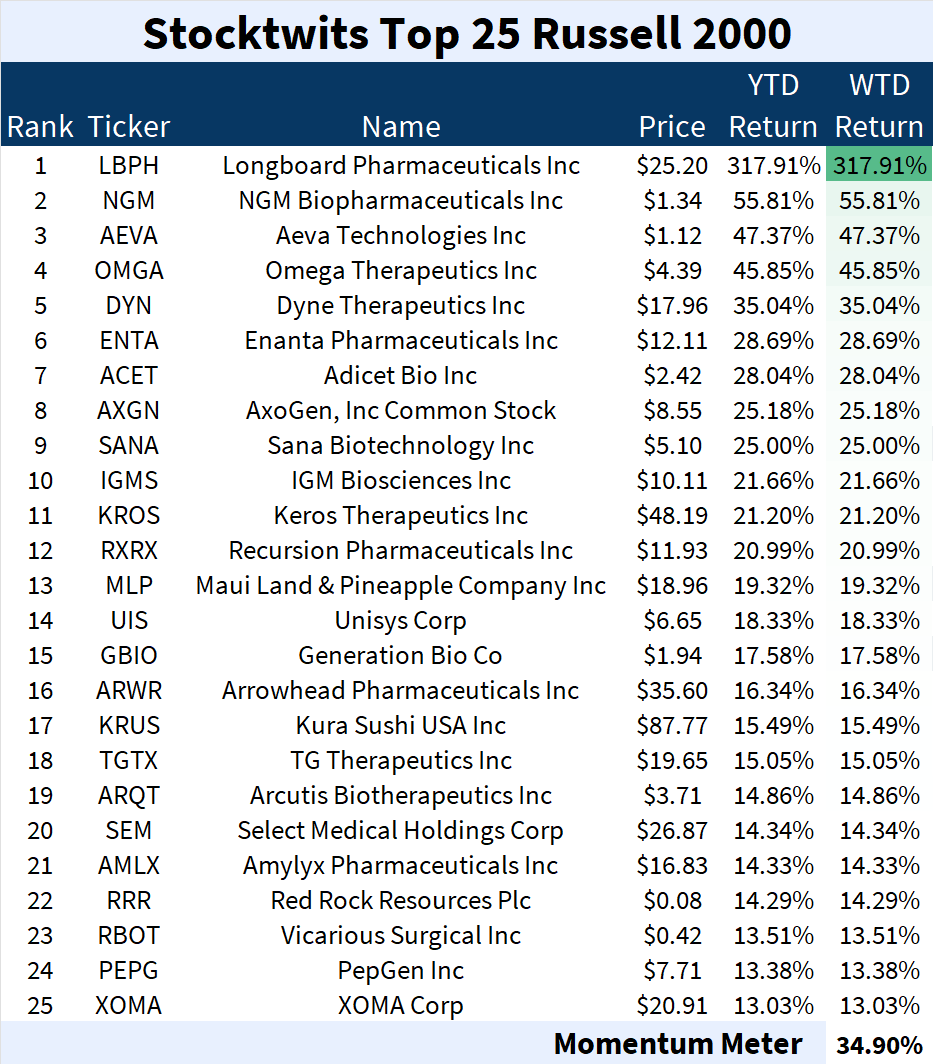

The largest drop over the week, nonetheless, was witnessed within the small-cap Russell 2000 (RUT; represented by the ETF IWM) which pulled again by 3.1%. Its one-day drop within the new 12 months was 0.7%. The highest gainers on this index had been nearly solely pharmaceutical corporations.

Supply: StockTwits

Whether or not these early developments portend basic market directionality within the 12 months to return is likely to be aided (or hindered) by the general institutional outlook for the 12 months, which runs the gamut from blasé to optimistic.

Institutional Views

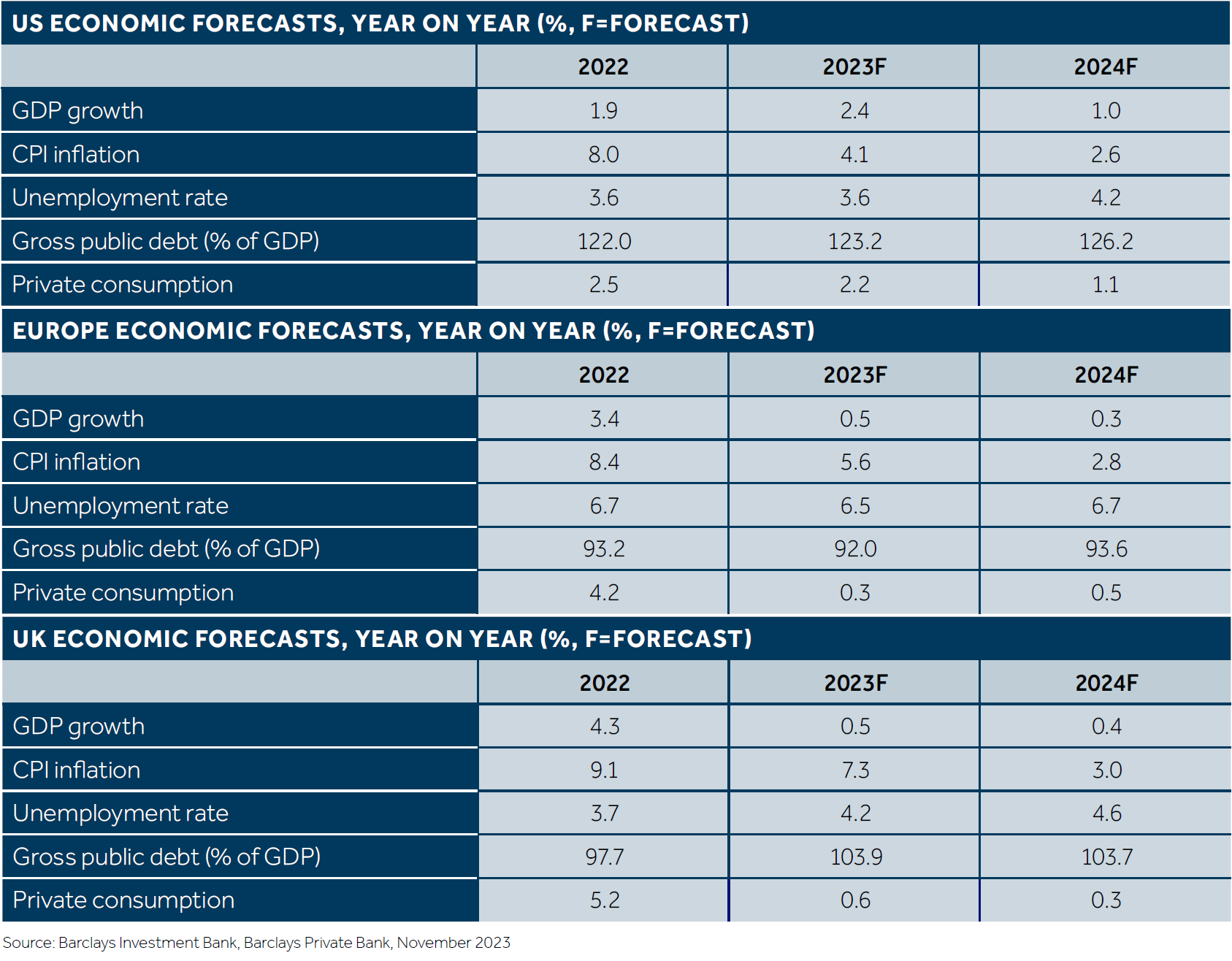

In its outlook for 2024, British funding financial institution Barclays opined that 2024 might be a very muddled 12 months for the Western Hemisphere.

Supply: Barclays Capital

Whereas the Hemisphere is anticipated to see decrease year-on-year Shopper Value Index (CPI) inflation, the USA will see a 17% improve within the unemployment fee together with a 50% lower in personal consumption. No area – be it the U.S., the U.Ok., or the Continent – will expertise GDP progress.

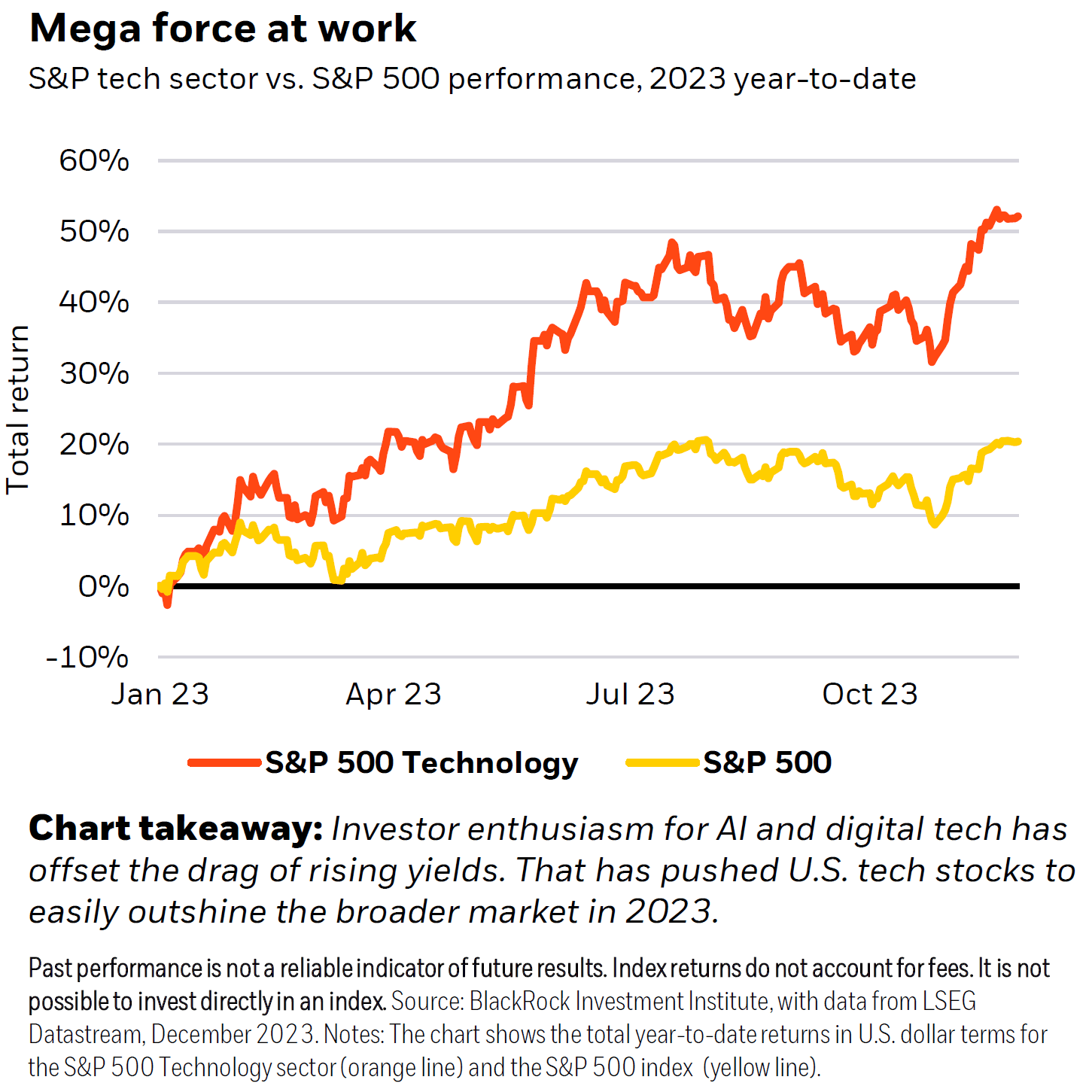

The drop in consumption is a very ominous indicator for the know-how sector: with out important buy-ins, ahead valuations and investor convictions get shaky. Because the Blackrock Funding Institute indicated, “tech” loved a conviction premium all through 2023 and ended the 12 months with an almost 155% outperformance towards the “broad market”.

Supply: BlackRock Funding Institute

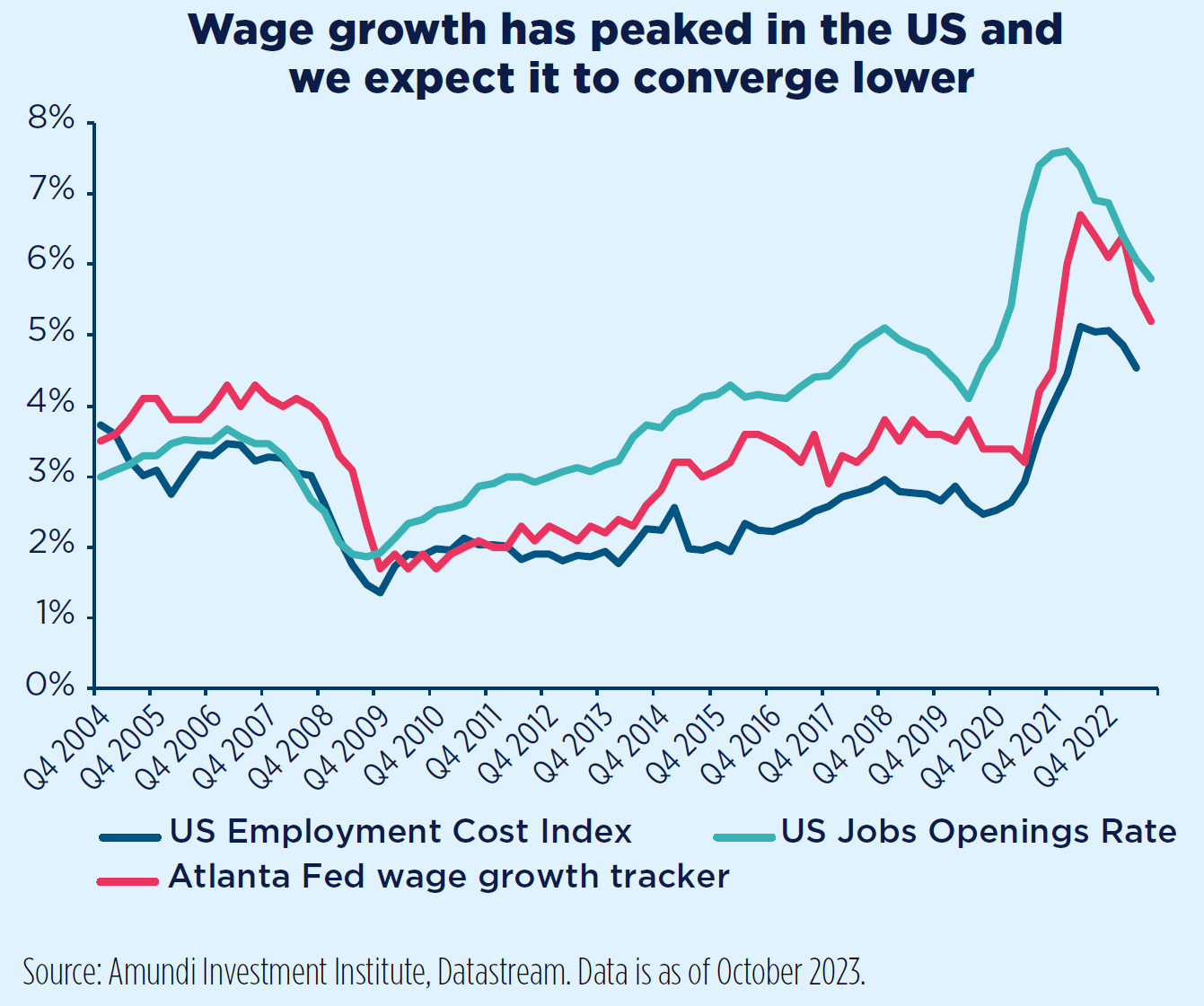

France’s Amundi – Europe’s largest asset supervisor in Europe and one of many world’s 10 largest funding managers – estimates that wage progress within the U.S. has peaked and can slide decrease within the 12 months forward.

Supply: Amundi Funding Institute

On condition that CPI inflation is anticipated to drop, that drop in wage progress may need a sure rationale. Then why the drop in private consumption? It is a extra complicated and multi-factored concern that isn’t actually helped by the truth that the typical U.S. shopper/resident has been saddled with rising prices far in extra of wage progress for nicely over a decade now. The “weight of macro consequences” is a slow-moving iceberg seldom addressable with easy measures.

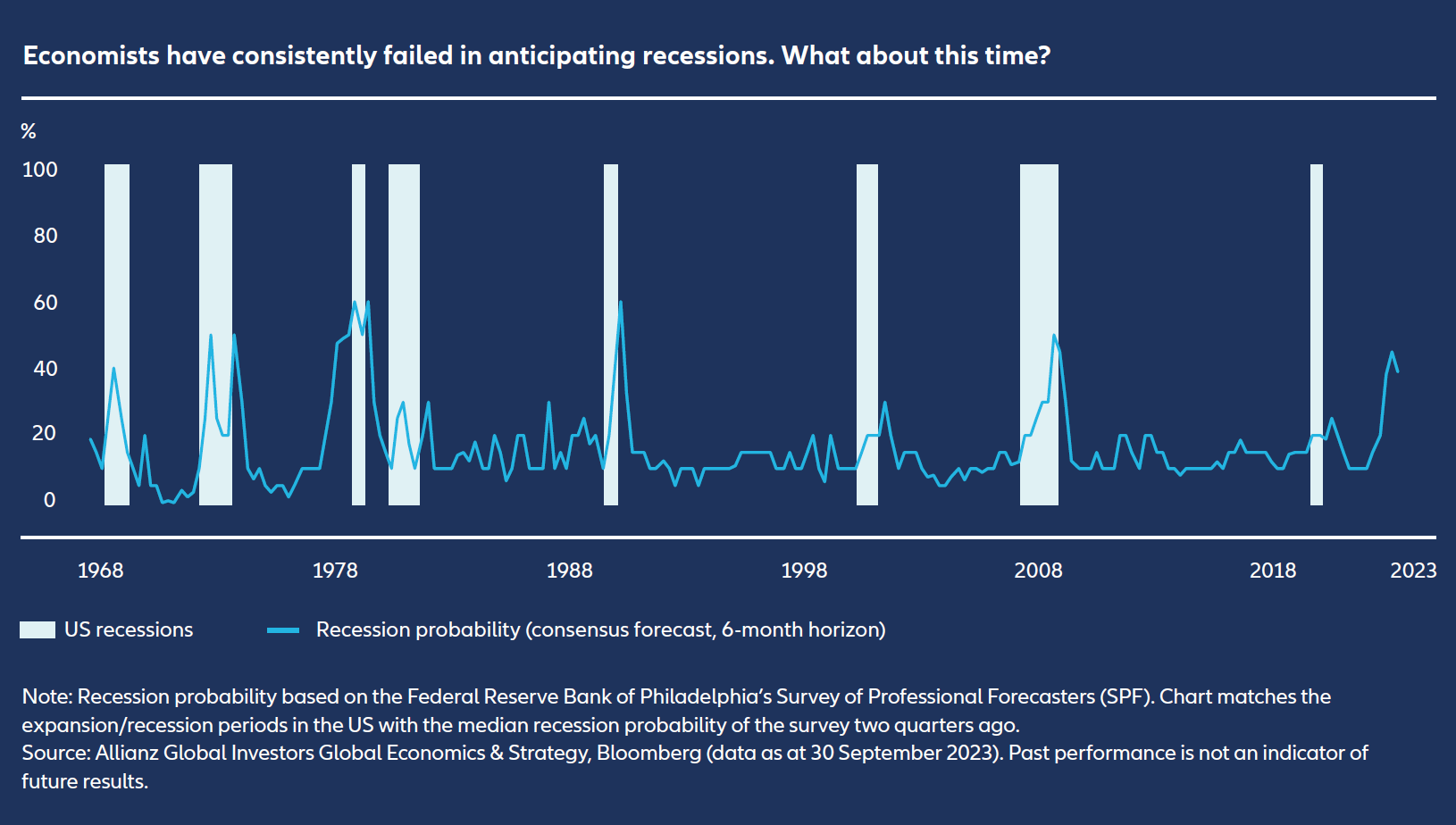

Because the U.S. prepares for arguably one of the vital contentious elections in fashionable historical past, economists and forecasters have been significantly cautious of creating prognostications, particularly aftermarket cool-offs and sector rotations did not materialize as anticipated in 2023. Some have substituted the time period “recession” with musings on whether or not a “landing” might be “hard” or “soft”. Presently, the consensus is inching in the direction of a “soft landing”. Nonetheless, Germany’s Allianz International Traders – a subsidiary of the world’s largest insurance coverage firm – famous in its outlook that forecasters’ consensus opinions have been incorrect on nearly each recession for the reason that eighties:

Supply: Allianz International Traders

One function that stands out is that just about each recessionary occasion was nearly instantly preceded by a low chance consensus of mentioned recession occurring.

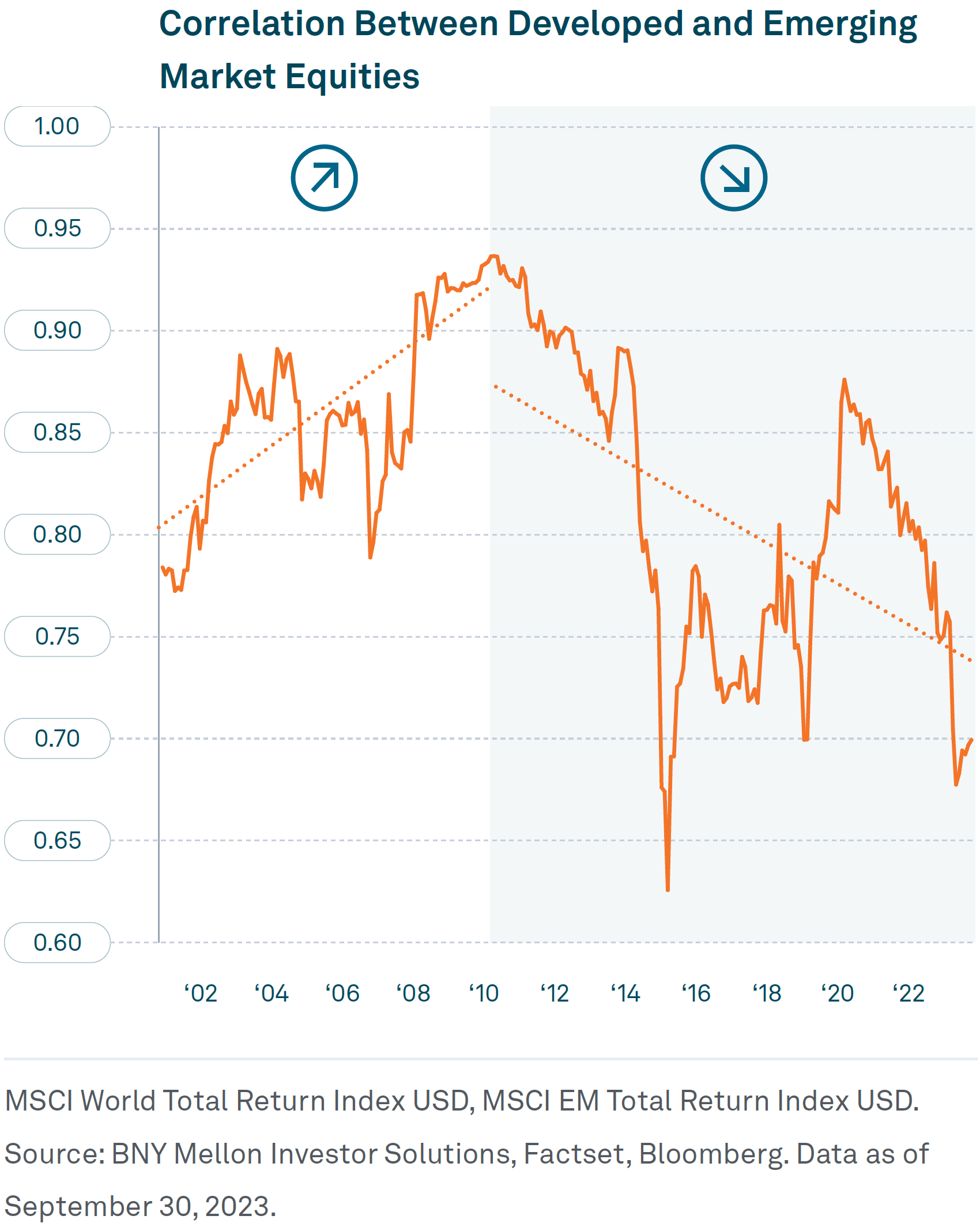

One other assumed truism is that an “American” recession tends to spell doom for the worldwide market and economic system as nicely. In its outlook for 2024 titled “10-Year Capital Assumptions”, BNY Mellon outlines that this will likely not occur: for the reason that final nice recessionary occasion – the International Monetary Disaster [GFC]- Rising Markets [EM] have been more and more uncoupled from Developed Markets [DM].

Supply: BNY Mellon

This highlights an often-stated but frequently-derided pattern broadly known as “deglobalization”. In impact, the notion of a single “global driver” is more and more much less viable.

Fashions Breaking

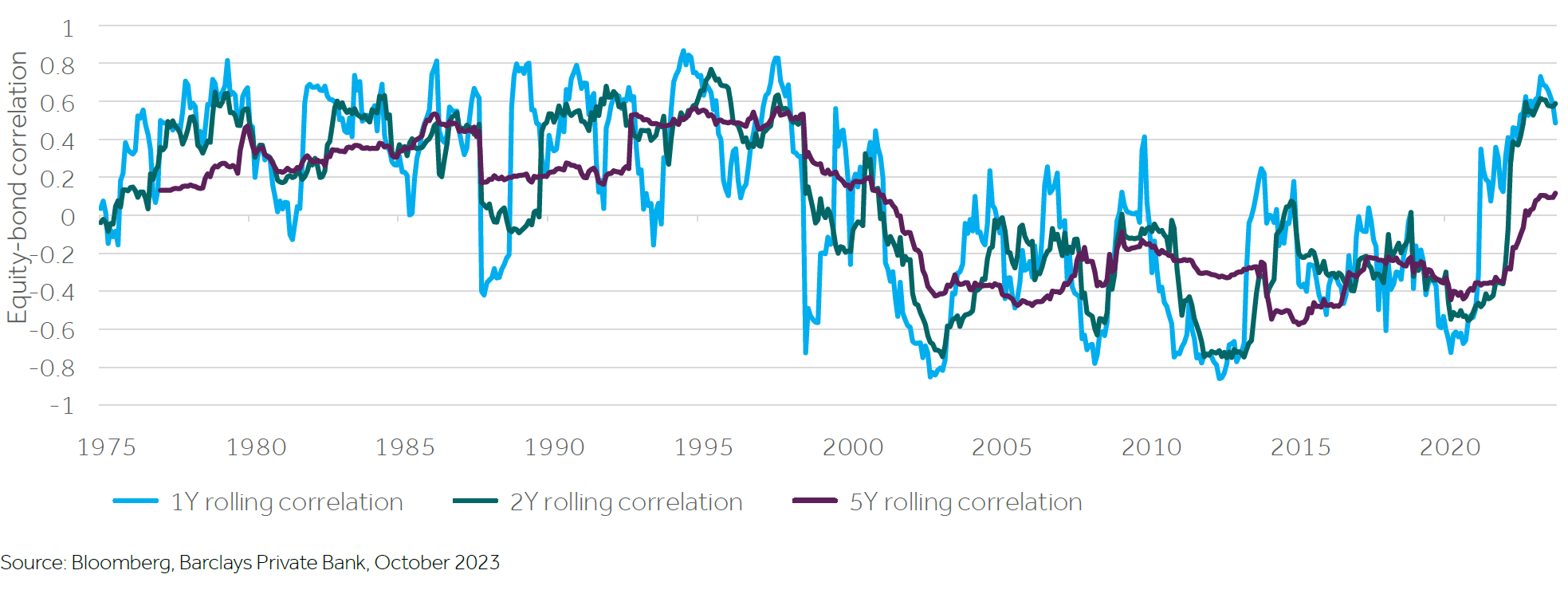

“Deglobalization” is merely one in every of many indicators that classical fashions are being challenged. One “classic” is the bond-equities relationship which most buyers broadly perceive as a “flight to safety” paradigm from equities to bonds when the previous seems shaky and vice versa when the outlook has stabilized. Barclays asserted that bond-equity correlations, a key measure for asset allocation methods, have shot as much as ranges final seen twenty years in the past (i.e. circa the dot-com bubble).

Supply: Barclays Capital

At present ranges of correlation, the financial institution states that bonds don’t act because the shock absorbers to equities as they’ve carried out up to now.

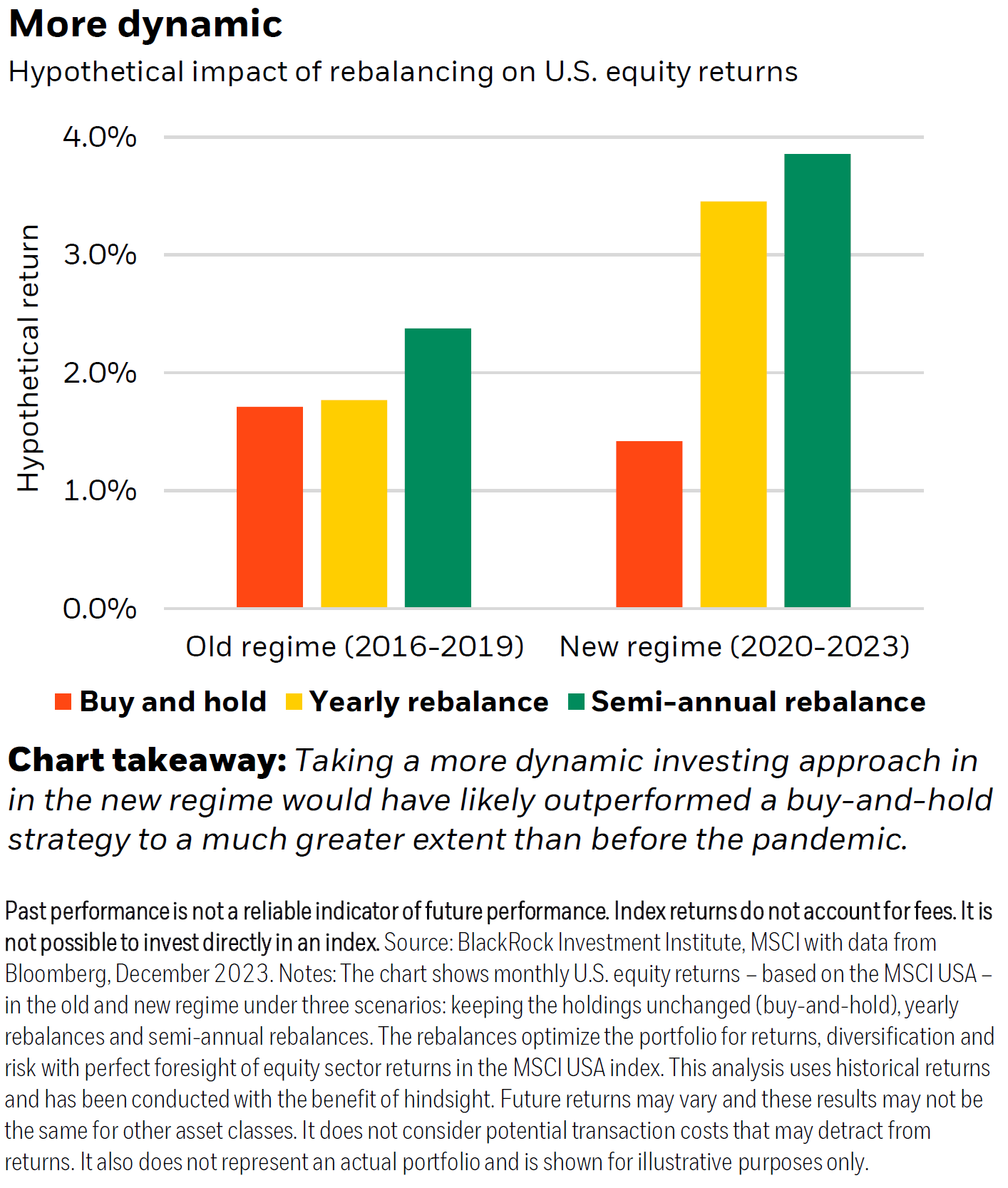

One other “classic” being challenged is an investor favorite: the “buy and hold”. As per research by the BlackRock Funding Institute, buyers who get “granular” with their portfolio allocations have tended to thrive over these with “static” portfolios.

Supply: BlackRock Funding Institute

With a large arsenal of instruments and methods to assist outperform static portfolios, BlackRock asserts that funding experience is probably going to provide portfolios an edge by enabling simpler core allocations, implementing “alpha” concepts and hedging danger.

The Backside Line

Within the 2024 market outlook article published last month, it was opined that AI, for higher or for worse, is right here to remain and can proceed to have a powerful affect in investor conviction a minimum of within the near- to mid-term. Whereas it is actually nicely inside purpose to carry forth that America’s tech shares being closely overvalued relative to the remainder of the market is a headwind, AI-related developments will proceed to be thought to be tailwinds for the constituents of the sector. An identical tilt in favour is anticipated to be writ giant within the personal market as nicely.

With deeply-held notions being challenged (and even probably altered endlessly), it seemingly would pay – extra so now than ever – if buyers had been to eschew the hype round favourites, study intently concepts thought-about to be “fundamental” and discover new methods obtainable.

Given shifting developments and long-held paradigms, a “caveat emptor” can be so as.