KatarzynaBialasiewicz/iStock through Getty Pictures

Funding thesis

Over the previous 8 years, Tempur Sealy’s (NYSE:TPX) income grew at 7 % CAGR due primarily to the USD 0.5 billion acquisition in 2021. With out the acquisition, income development would solely be at in regards to the long-term GDP development price. I even have considerations about its means to attain productiveness and capital effectivity enhancements with out the acquisition.

Nonetheless, the corporate is essentially sound with the previous 8 years’ common returns larger than the price of funds. However the excessive Debt-Capital ratio, it has a powerful monitor file in producing money circulation from operations with a superb money conversion ratio.

The one concern is that there’s solely a margin of security in the event you assume that TPX will undertake one other main acquisition inside the subsequent 5 years. There isn’t any margin of security if there isn’t any such acquisition plan.

Enterprise background

TPX is a number one designer, producer, distributor, and retailer of bedding merchandise to shoppers in over 100 nations. The corporate has an omnichannel distribution technique. Its merchandise are offered by way of third-party retailers, its greater than 700 company-owned shops, and its e-commerce platforms.

Though the corporate has a worldwide manufacturing footprint with roughly 12,000 workers world wide, North America accounted for about 79% of its 2022 gross sales. The corporate has 2 enterprise segments – North America and Worldwide.

- The North America phase consists of producing and distribution subsidiaries, joint ventures, and licensees positioned within the U.S., Canada, and Mexico.

- The Worldwide phase consists of producing and distribution subsidiaries, joint ventures, and licensees positioned in Europe, Asia-Pacific, and Latin America (aside from Mexico).

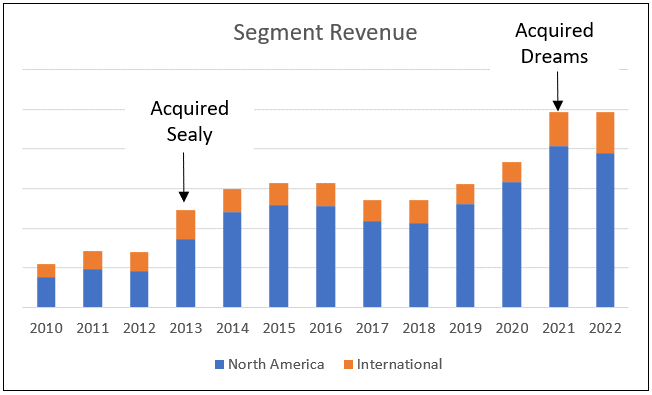

North America was the largest income contributor over the previous 2 many years. From 2010 to 2022, this phase’s income grew at 14.4 % CAGR. The Worldwide phase was no pushover both when it got here to income development with a 9.9 % CAGR.

These resulted within the firm reaching a income development of 13.3 % CAGR from 2010 to 2022. Taking a look at this development price, you will be forgiven for pondering that it is a high-growth firm.

However this excessive development was as a consequence of 2 main acquisitions:

- Desires Topco Ltd, UK (Desires) in 2021 for about USD 0.5 billion.

- Sealy in 2013 for about USD 1.0 billion.

Taking a look at Chart 1, you possibly can see that these acquisitions resulted in income spikes within the respective acquisition years.

Chart 1: Section Income (Creator)

Thrust of my evaluation

Final month, I printed an evaluation of Sleep Quantity Company (SNBR), a competitor to TPX. I wished to see how TPX can be truthful if I adopted the identical basic evaluation and valuation method as that for SNBR. This could then assist me to resolve on whether or not to spend money on TPX or SNBR if I had to decide on just one bedding firm.

This isn’t the primary time that I coated TPX as I had 3 earlier articles:

The important thing findings from the sooner articles had been:

- TPX grew as a consequence of a mix of main acquisitions, development within the Housing Begins, and anti-dumping motion.

- There’s a sturdy correlation between the North America phase’s income and the US Housing Begins. Housing Begins are cyclical, making TPX a cyclical firm.

- Though extremely geared, TPX is essentially sound.

- The bedding business just isn’t a high-growth one. The US bedding business is projected to develop beneath 4 % over the following 5 to 10 years. Numerous market analysis corporations have projected the worldwide bedding market to develop between 4.2 % to 7.4 % over the following few years.

Within the earlier analyses, I had considered TPX as a cyclical firm and valued it as such. On such a foundation, I concluded that it was overpriced.

To my shock, the market value had elevated from USD 26 per share (Jan 2021) to USD 51 per share (2 Jan 2024). Both the market could be very irrational or my cyclical foundation in valuing TPX was incorrect. So, beware when studying my present valuation.

Given my earlier articles, I’d not cowl what I had carried out earlier. As an alternative, I’ll assess how properly the corporate has achieved its enterprise technique as set out in its 2022 Kind 10k:

“…to drive earnings growth with high return on invested capital and strong free cash flow…We also intend to generate earnings growth through… productivity initiatives…We have a balanced approach to capital allocation…”

To allow an apple-to-apple comparability with SNBR, I’ll cowl the 2016 to 2023 interval in my evaluation of TPX. I’ll use the Sep 2023 LTM outcomes because the 2023 efficiency.

Working efficiency

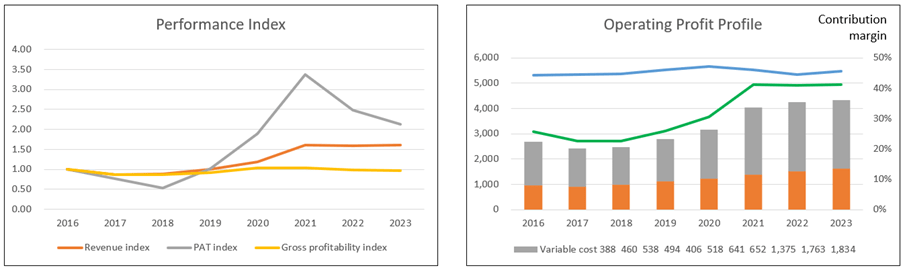

I checked out two teams of metrics to get a way of how the corporate had carried out over the previous 8 years.

- Efficiency Indices for income, PAT, and gross profitability (gross income / whole belongings). Discuss with the left a part of Chart 2.

- Working income are damaged down into income, mounted prices, and variable prices. Discuss with the correct chart in Chart 2.

I had earlier talked about that TPX’s income development was excessive as a consequence of its acquisitions. That is illustrated by the 2016 to 2023 efficiency:

- From 2016 to 2020 when there was no main acquisition, income grew at 4.5 % CAGR.

- From 2020 to 2023 when the Desires acquisition occurred, income grew at 10.4 % CAGR.

General, from 2016 to 2023, income grew at 7.0 % CAGR. However PAT grew at a a lot quicker price at 11.5 % CAGR. This was as a consequence of increased income in addition to the expansion in gross revenue margins. For instance, the typical gross revenue margin for 2020/21 was 44.2 % in comparison with the typical of 41.7 % for 2016/17.

The larger concern was the declining gross profitability since 2016. In accordance with Professor Novy-Marx, this metric has the identical energy as PBV in predicting cross-section returns of shares. The declining development signifies growing capital inefficiencies. That is counter to the corporate’s productiveness targets.

For those who have a look at the working revenue profile of Chart 2, the hole between the income and the entire prices (Mounted value + Variable value) represents the working revenue.

- The working income for the previous 3 years (publish the Desires acquisition) had declined after peaking in 2021.

- The contribution margin has been “stable” since 2016. Technically, there was solely a 0.4 % CAGR from 2016 to 2023.

Chart 2: Working Developments (Creator)

a) Word to Efficiency Index chart. I’ve transformed the varied metrics into indices to plot the varied metrics on one chart. The respective index was created by dividing the annual values by the 2016 values.

b) Word to Working Revenue chart. I broke down the working income into mounted prices and variable prices.

- Mounted value = SGA and Depreciation & Amortization.

- Variable value = Value of Gross sales – Depreciation & Amortization.

- Contribution = Income – Variable Value.

- Contribution margin = Contribution/Income.

Returns

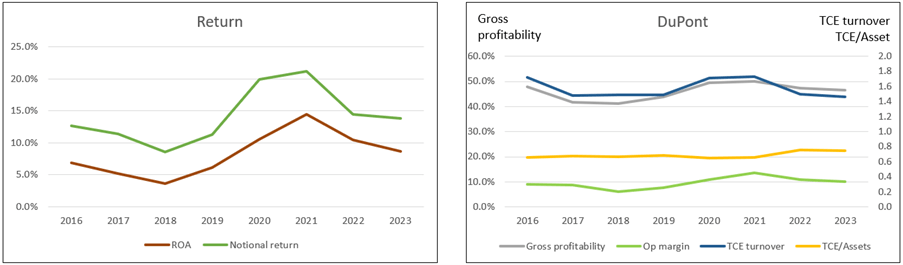

The corporate had an aggressive share buyback program that lowered its fairness. In returns, it’s thus extra applicable to take a look at the Return on Belongings (ROA) somewhat than ROE.

On the identical time, to supply an apple-to-apple comparability with SNBR, I additionally seemed on the Notional return on capital employed. Right here I assumed that there was no share buyback. Moderately all of the monies spent on the buyback had been distributed as dividends. In different phrases, the fairness was assumed to be a relentless on the 2015 degree. I outlined the Notional return as = NOPAT / (Notional fairness + Debt)

The left a part of Chart 3 compares the returns for these 2 metrics. You’ll be able to see that each metrics had been unstable – first declining from 2016 to then uptrend to peak in 2021 earlier than declining. The 2021 peak coincided with the acquisition of Desires.

The returns for each metrics in 2023 had been a bit increased than these in 2016. On this sense, you possibly can argue that the corporate achieved its return targets.

A DuPont evaluation of the working returns (outlined at NOPAT / Complete Capital Employed) confirmed that the enhancing returns had been as a consequence of higher working margins and leverage that was partly offset by decrease capital turnover.

With the decrease capital turnover Collectively and declining gross profitability, I’d conclude that the corporate didn’t obtain its productiveness targets.

Wanting on the previous 4 years’ returns and the DuPont Evaluation, you could wonder if the enhancing returns and productiveness are as a consequence of acquisitions. As soon as the acquisition had been built-in, it appeared that the corporate was not in a position to extract “organic” productiveness or effectivity enhancements.

Chart 3: Returns and DuPont Evaluation (Creator)

a) Word to Return chart. The Notional return assumed that there was no change within the 2015 Fairness. In different phrases, all the cash spent on share buyback was assumed to be paid out as dividends.

b) Word to DuPont Evaluation chart. The DuPont relies on Working Return = NOPAT / Complete Capital Employed. Complete Capital Employed = Fairness + Debt – Money.

Monetary place

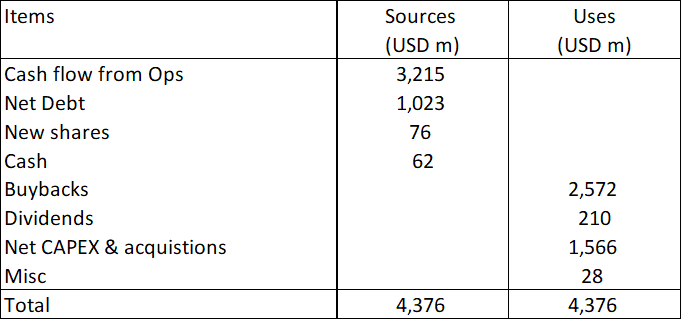

I’d price TPX’s monetary place as common primarily based on the next:

- It has a 91 % Debt Capital ratio as of the tip of Sep 2023. As per the Damodaran Jan 2023 dataset, the Debt Capital ratio for the furnishings/residence furnishing sector was 36 %. It was solely 13% for the family merchandise sector.

- As of the tip of Sep 2023, it had USD 92 million in money. This was solely about 2 % of its whole belongings.

- It didn’t have a superb capital allocation plan as proven in Desk 1. The money circulation from operations was not enough to fund share buybacks, dividends, and CAPEX. It needed to elevate extra Debt for its CAPEX and acquisitions.

Desk 1: Supply and Makes use of of Funds 2016 to 2023 (Creator)

However it had some constructive factors:

- Over the previous 8 years, it generated constructive money circulation from operations yearly. In whole, it generated USD 3.2 billion money circulation from operations in comparison with the entire PAT of USD 2.4 billion. This is a superb money conversion ratio.

- I had earlier talked about the Notional return on capital. Over the previous 8 years, this averaged 14.2 % in comparison with the present value of capital of 8.5 %. This indicated that it was in a position to create shareholders’ worth.

Free money circulation

The Free Money Circulation to the Agency (FCFF) is outlined as:

FCFF = EBIT(1-t) X (1 – Reinvestment price)

The place:

EBIT(1 – t) = After-tax Working revenue or NOPAT

Reinvestment = Web CAPEX + Acquisitions – Depreciation & Amortization + Web Adjustments in Working Capital

Reinvestment price = Reinvestment / EBIT(1 – t)

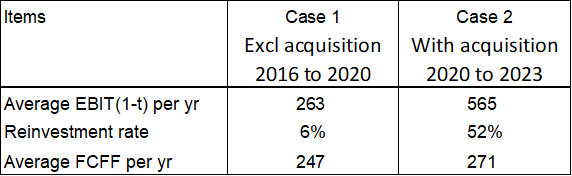

The Reinvestment price would differ if we excluded Acquisitions. To see the influence of this, I thought of 2 instances:

- Case 1 – taking the typical 2016 to 2020 values. There have been no important acquisition throughout the interval.

- Case 2 – taking the typical 2020 to 2023 values. This coated the Desires acquisition.

Desk 2 reveals the influence on the FCFF for each instances.

Desk 2: Comparative FCFF (Creator)

There are 2 takeaways right here:

- The corporate was in a position to generate important common FCFF yearly in each instances. That is consistent with its technique of driving “…earnings growth with high return on invested capital and strong free cash flow.”

- Whereas there have been increased NOPAT with acquisitions, there have been additionally increased Reinvestment charges. Nonetheless, there was a rise within the FCFF in comparison with the case with out the acquisition.

Word that the typical annual FCFF in Case 2 is a conservative estimate. I had assumed that the influence of the acquisition was unfold over 4 years. Traditionally the interval between the most important acquisitions was a lot bigger. For instance, there has not been any main acquisition for the reason that 2021 acquisition of Desires. The opposite main acquisition earlier than Desires was the Sealy acquisition in 2013.

Valuation

I had initially deliberate to worth TPX primarily based on what I did for SNBR. Given SNBR’s earnings profile, I valued it primarily based on its Earnings Energy Worth in addition to assuming a 3% regular development price.

TPX’s earnings profile over the identical interval was very completely different from that of SNBR. As such it made extra sense to worth TPX primarily based on the next Situations:

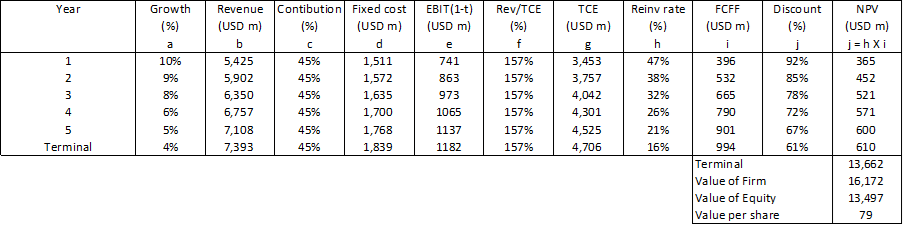

- State of affairs 1. That is primarily based on a single-stage mannequin with a 4 % perpetual development price. I assumed that the long run income relies on the previous 3 years’ common income.

- State of affairs 2. That is primarily based on a 2-stage mannequin. I assumed that there can be one other main acquisition subsequent yr that will improve the previous 3 years’ common income by 10%. Thereafter income development would decline to a 4 % terminal worth in yr 6.

In my SNBR valuation, I assumed that the long-term or terminal development price was half of the WACC. The 4% development price for TPX was primarily based on the identical logic. For each Situations, I assumed the next key parameters to account for the cyclical results:

- The contribution margin was primarily based on the 2016 to 2023 common values.

- Capital turnover (Income / TCE) was primarily based on the 2016 to 2023 common ratios

The outcomes of the valuations are proven in Desk 3.

Desk 3: Abstract of valuation. (Creator)

Notes to Desk 3:

a) The income proven refers to these for the bottom yr.

b) The income proven refers to these for Yr 1.

At USD 43 per share, there’s not sufficient margin of security primarily based on State of affairs 1. However at USD 79 per share, there’s greater than a 30% margin of security beneath State of affairs 2.

The margin of security is determined by your perspective of development. The market appears to be pricing TPX as if it might proceed to develop through one other main acquisition within the not-too-distant future.

Single-stage valuation mannequin

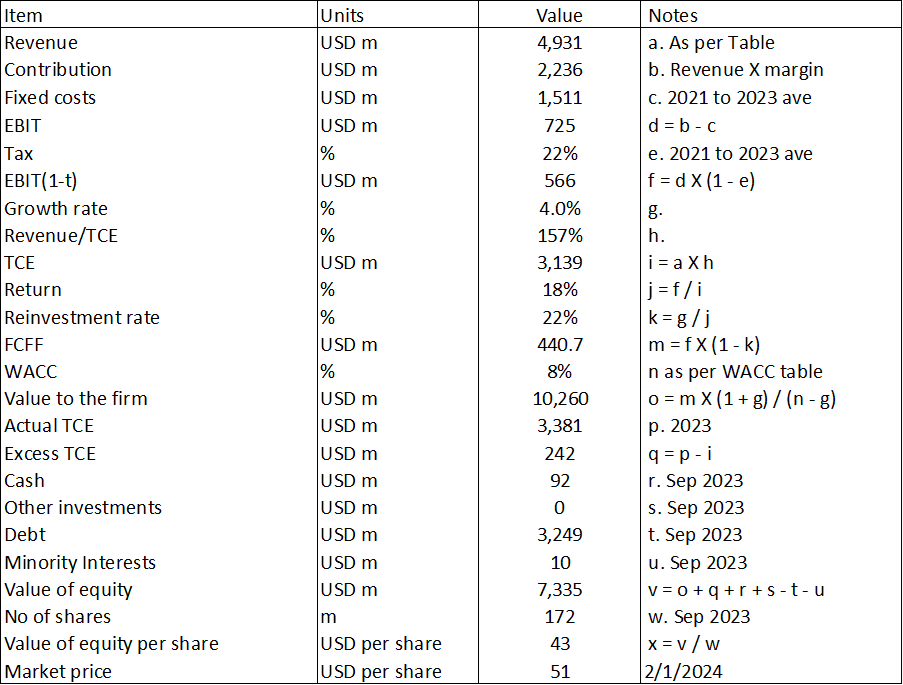

The only-stage mannequin is similar as that used for SNBR. Discuss with that article for an outline of the mannequin. A pattern calculation for TPX is proven in Desk 4.

Desk 4. Pattern calculation for single-stage mannequin (Creator)

Two-stage valuation mannequin

Desk 5 illustrates the mannequin. The important thing variables listed here are the expansion price which impacts the income and EBIT. The opposite parameters for the bottom yr had been the identical as these within the single-stage mannequin.

Desk 5. Two-stage mannequin (Creator)

Notes to Desk 5:

a) Straight-line discount.

b) Pegged to development price

c) Assumed no enchancment.

d) Assumed development at a terminal price.

e) Income X Contribution margin and after accounting for Mounted value.

f) Assumed no enchancment.

g) Income X (Income/TCE) ratio

h) Based mostly on the expansion equation.

i) EBIT(1-t) X (1 – Reinvestment price).

j) Assumed fixed D/E ratio.

Dangers and limitations

There are 3 points to contemplate in my valuation:

- Excessive WACC.

- Acquisition prospects.

- Cyclical values.

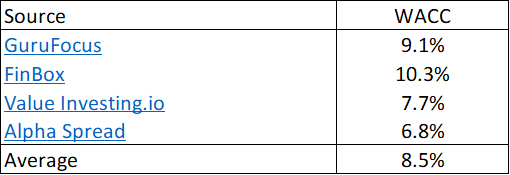

The WACC used was primarily based on the primary web page outcomes of a Google seek for the time period “TPX WACC” as proven in Desk 6.

Desk 6: Estimating the WACC (Numerous)

We at the moment have a excessive FED rate of interest leading to a high-risk free price. When the anticipated FED price reduce happens, we’ll see a fall within the risk-free price. This may result in a decrease WACC. As such, the present valuation is conservative.

The opposite valuation concern pertains to the way you see the acquisition prospects for TPX.

- For those who consider that it already has a sizeable market share and there’s unlikely to be one other main acquisition, you’d undertake the valuation mannequin of State of affairs 1.

- For those who consider that there’ll nonetheless be alternatives for different main acquisitions, you’d undertake the valuation mannequin of State of affairs 2.

Given its historical past, State of affairs 2 appears believable. The problem just isn’t understanding when it will occur. In my valuation, I’ve assumed that it’s going to happen subsequent yr. If the acquisition takes place a lot additional out in time, the worth could also be decrease than that proven in Desk 3 as a result of time worth of cash.

I’ve earlier talked about that TPX is a cyclical firm. In valuing TPX, we ought to be trying on the efficiency of the important thing metrics over the cycle. Assuming a 2005 to 2023 peak-to-peak cycle, I then estimated the typical contribution margin and Income / TCE for this era. Based mostly on these, I discovered that there’s a 14 % margin of security utilizing a single-stage mannequin. The worth proven in Desk 3 is conservative.

Conclusion

I’d price TPX as essentially sound primarily based on the next:

- With out the acquisitions, its income development price matched these of the long-term GDP development price and the business. Acquisitions boosted its income development.

- Even with acquisitions, it generated sturdy Free Money Flows.

- Whereas it achieved solely marginal development within the ROA and Notional return over the previous 8 years, they had been larger than its present value of funds. This meant that TPX created shareholders’ worth.

- Whereas it has a excessive Debt Capital ratio, it was in a position to generate constructive money circulation from operations yearly. It additionally had a superb money circulation from operations to PAT conversion ratio.

- It requires little extra capital to develop the enterprise. Whereas I’ve some considerations about its capital allocation plan, this has extra to do with how administration has allotted capital. The enterprise is a money cow.

Nevertheless, I’ve considerations about its means to attain productiveness or working effectivity positive factors. The true problem with TPX is the valuation. There’s solely a margin of security in the event you consider that it’s going to proceed with its acquisition technique to develop. I’m a conservative investor so I’d somewhat not guess on this.

Comparability with SNBR

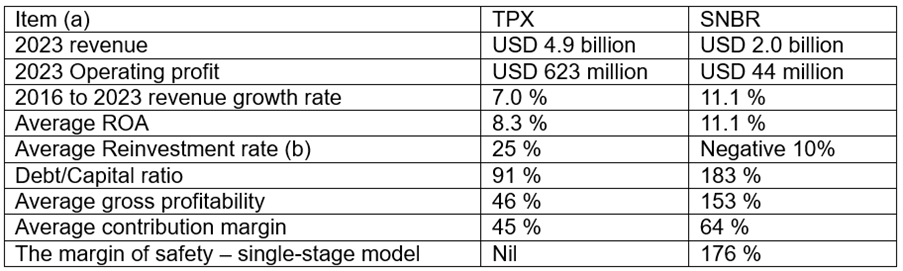

One of many targets of this evaluation was to see whether or not TPX was a greater funding alternative than SNBR. On this context, I in contrast these 2 corporations primarily based on the important thing parameters that drive the intrinsic worth – return, Reinvestment price, development and monetary threat. Discuss with Desk 7.

- Leaving apart the scale and Debt Capital metrics, you possibly can see that SNBR did higher than TPX for the opposite metrics.

- Each corporations had aggressive share buyback applications. In each instances, the quantity spent on the buyback and dividends exceeded the money circulation from operations.

- Over the previous 8 years, acquisitions helped to spice up TPX development whereas SNBR development was extra natural.

- SNBR has a margin of security primarily based on the single-stage mannequin.

Desk 7. TPX vs SNBR (Creator)

Notes to Desk 7:

a) Except said in any other case, the typical refers back to the 2016 to 2023 interval.

b) Excluding acquisitions.

TPX and SNBR have their respective enterprise set-up (methods, group construction, company tradition, and so on). What you see from Desk 7 are the outcomes of their respective enterprise set-up. Alongside this line, it I had to decide on just one bedding firm to spend money on, it might be SNBR.