da-kuk

Funding overview

I give a purchase score for Tenable (NASDAQ:TENB) as I see the expansion momentum persevering with into FY24. On a longer-term foundation, there’s a sturdy secular tailwind (demand for cybersecurity) that ought to proceed to broaden the overall addressable marketplace for TENB. Extra importantly, the enterprise has an enormous runway for margin growth forward, which ought to proceed to help a premium valuation.

Enterprise description

TENB is a leading player within the Vulnerability Administration [VM] end-market. In at this time’s digitalized world, they provide an answer that’s mission-critical: a unified view of the group’s assault floor. This view helps prospects handle and measure cybersecurity threat. Cybersecurity threat exists all over the place, not solely within the conventional recognized areas like community’s companies. Cloud computing, IoT units, and OT methods like Industrial Management Programs are just some examples of the place they are often discovered at this time. By way of using a unified platform that converts vulnerability knowledge into simply shareable enterprise metrics, TENB permits its prospects to leverage cybersecurity knowledge for executive-level strategic decision-making and offers safety groups the means to prioritize problem-solving.

4Q23 earnings outcomes

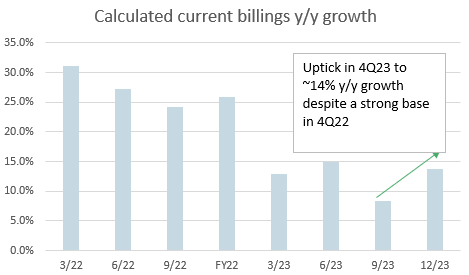

TENB reported 4Q23 results ~2 weeks ago, and for the advantage of those who missed the outcomes: TENB reported calculated present billings [CCB] of $271.6 million, representing a progress of 14% y/y. Income got here in at $213.3 million, which exceeded the excessive finish of administration’s steering vary ($204 million to $208 million) in addition to consensus expectations for $206.4 million. TENB continued to point out enhancements in profitability, the place its non-GAAP gross margin expanded by 210bps y/y to 80.6%, sustaining above the 80% threshold. Non-GAAP EBIT additionally exceeded the excessive finish of administration’s steering, coming in at $36.1 million, primarily as a result of sturdy top-line efficiency.

Count on progress momentum to proceed

My expectation for the TENB progress outlook is constructive for each the near-term and the long-term. For the close to time period, I consider the 4Q23 outcomes confirmed enough proof of ongoing momentum. After failing to fulfill consensus expectations in 3Q23, TENB confirmed that 3Q was only a blip and they’re again on observe in assembly expectations (to reiterate: TENB beat expectations in CCB, income, and EBIT margin in 4Q23).

Could Investing Concepts

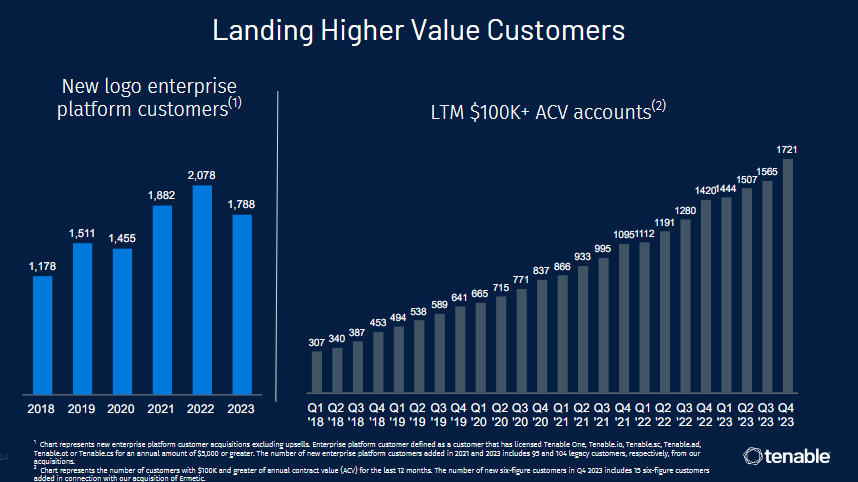

Main progress indicators like CCB and present bookings progress recommend demand momentum rolling into FY24 as nicely, the place CCB grew 14% and present bookings (income + q/q change in remaining efficiency obligation [RPO]) grew 19%, with the latter indicating the success in enhancing execution throughout 4Q23. Positively, the sturdy 4Q23 progress didn’t include a deterioration in unit economics, because the TENB dollar-based web growth price [DBNER] remained steady at 111% for the third consecutive quarter. Except for quantitative metrics, the qualitative feedback supplied by administration additionally level to a constructive progress outlook. Their first encouraging remark was that CCB’s progress was pushed partly by the stabilization of their mid-market enterprise this quarter. Gaining traction within the mid-market is vital as a result of it’s certainly one of TENB’s methods to increase its progress runway by its “land and expand” technique, which has confirmed to achieve success primarily based on the variety of prospects with greater than $100k in annual contract worth [ACV].

TENB

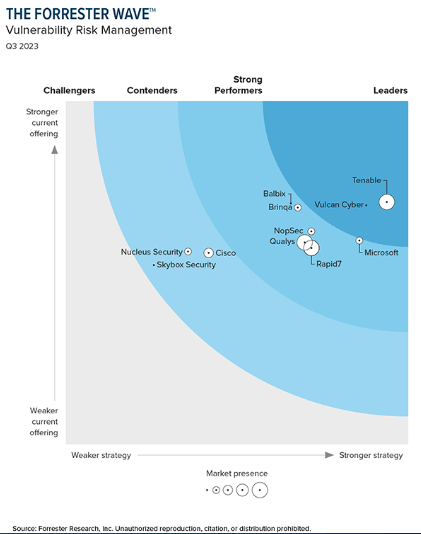

Secondly, it was encouraging to know that TENB is profitable share in new markets, suggesting that TENB product’s worth proposition and price resonate with buyer calls for. This additionally helps the truth that TENB is the main participant within the trade, outperforming the likes of massive gamers like Microsoft (MSFT), Vulcan Cyber, Rapid7 (RPD), Qualys (QLYS), and many others. I might anticipate market share positive factors to proceed as TENB leverages its latest acquisition of Ermetic to seize cloud safety share because it positive factors publicity to the fast-growing OT safety market.

Forrester Analysis

Between our know-how management and our important buyer base and distribution, we’re profitable and taking share on this important market. We’ll proceed to be dedicated to offering market-leading discrete merchandise to prospects.

Proceed to really feel like we’re profitable greater than our fair proportion in opposition to each of these within the completely different market segments. Outdoors of VM, we’re clearly seeing Wiz and Paolo Alto much more on the cloud aspect as we deliver our new cloud safety capabilities to market. Company 4Q23 earnings

Lastly, the efficiency of Tenable One is one issue that lends credence to a constructive progress outlook. Tenable One reached a 100% progress price in FY23, in line with administration feedback. It now makes up over 20% of latest enterprise and round mid-teens of complete gross sales in 4Q23. I consider there’s a lovely alternative for upselling given the success in different use instances like Cloud, OT, and Id, which collectively account for roughly half of TENB’s gross sales.

TENB

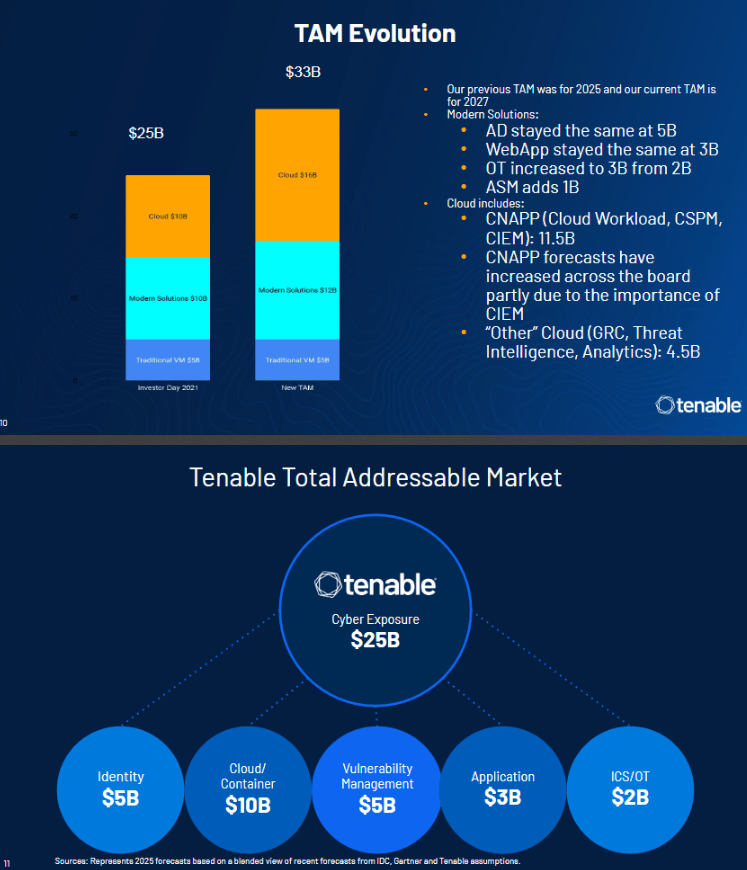

As for the long-term progress outlook, I consider any TAM estimates at this time are going to considerably underestimate the magnitude of progress. My perception is that the world goes to get extra linked digitally at an exponential price, and with that assumption, there can be extra endpoints which can be uncovered to cybersecurity threats. Take TENB estimates, for example; in simply 2 years, the TAM has expanded by $8 billion, from $25 billion to $33 billion. This means that the trade grew ~30% over 2 years, or about mid-to-high-teens share CAGR a 12 months. As such, wanting forward, I consider there can be loads of progress alternatives for TENB.

Enterprise going to get extra worthwhile

Over the previous few quarters, TENB has proven important incremental margin efficiency, the place the adj. EBIT margin expanded from 7.8% in 1Q22 to 16.9% in 4Q23. Based mostly on my calculation (change in adj EBIT/change in income), in FY23, incremental adj EBIT margin trended at greater than 50% for the final 3 quarters of the 12 months, indicating large margin growth potential forward. If we have a look at the closest peer, Qualys (QLYS), the enterprise has an adj. EBIT margin of ~42% as of 4Q23, which is greater than double what TENB is producing at this time. The important thing variance between the 2 is that TENB is spending extra on gross sales and advertising [S&M] and analysis and improvement [R&D] vs. QLYS. For reference, in FY23, TENB spent 42% of S&M and 15% in R&D, whereas QLYS spent 14% of S&M and 4% in R&D. Suppose TENB have been to cease investing in progress and begin farming for income and money. I see a straightforward path for TENB to achieve comparable ranges of profitability as QLYS. That mentioned, given the chance set out there, I believe it’s higher for TENB to spend money on progress whereas increasing margins steadily. On this facet, I consider administration FY24 steering has set the expectation proper in that TENB goes to proceed increasing margins; they guided for adj. EBIT margins north of 17% in FY24, which is above the consensus estimate of 16.5% for FY24. This speaks to administration’s willingness to optimize the associated fee construction and enhance effectivity.

Valuation

Could Investing Concepts

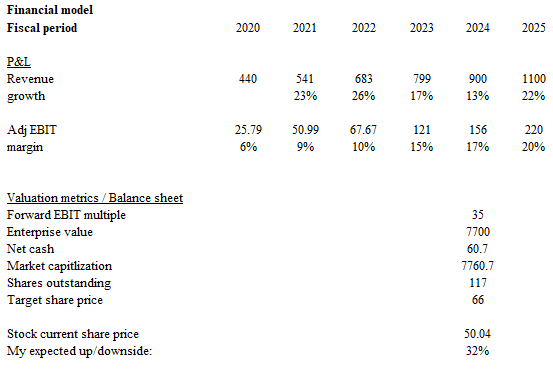

Based mostly on my analysis and evaluation, my anticipated goal value for TENB is $66.

- Income ought to on the naked minimal be capable of develop as per steering for FY24 by 13% given the momentum that TENB is seeing at this time (be aware that I consider administration’s information could be overly conservative right here), adopted by an acceleration to 22% to attain administration’s >$1.1 billion income information for FY25.

- Adj EBIT ought to proceed to broaden given the excessive incremental margin that the enterprise has. Utilizing administration steering, I anticipate TENB to attain $156 million in adj EBIT for FY24 (17% margin), adopted by additional the same margin growth development to twenty%.

- The inventory ought to commerce at a 35x ahead EBIT a number of, a premium to friends, as it’s anticipated to develop a lot quicker than friends (QLYS is predicted to develop low-teens for the subsequent 2 years) and is increasing its margin (QLYS margin seems to have peaked already).

Danger

TENB has been buying property to enhance its product choices not too long ago, buying 5 over the previous three years. This technique is helpful in lowering time to market; nonetheless, if not nicely built-in, it might end in a decline in product high quality, which can influence R&D effectivity as TENB must spend extra time reconfiguring its product sooner or later. As well as, ought to TENB select to pursue extra margin-dilutive M&A to bolster platform capabilities, profitability upside could grow to be tougher to understand.

Conclusion

My suggestion for TENB is a purchase score as I consider the enterprise will proceed to see progress momentum with margin growth. Within the near-term, TENB efficiency within the mid-market phase, profitable upselling, and the sturdy efficiency of Tenable One help progress. As for the long-term progress outlook, I additionally assume it’s promising, contemplating the evolving digital panorama and steady growth of the cybersecurity market. On profitability, TENB’s sturdy incremental margin efficiency and the speed of growth to this point point out a path in direction of higher margins.