Liudmila Chernetska/iStock through Getty Pictures

Funding Rundown

The inventory efficiency for Tennant Firm (NYSE:TNC) has been on a powerful transfer over the past 12 months outperforming the broader markets, being up 33%. TNC is included within the industrial sector and extra particularly the commercial equipment & provides parts business. The product portfolio stays nicely diversified for the enterprise and margins are on the highest ranges in the previous couple of years even because the rates of interest have quickly risen within the US. I believe this underscores among the demand that TNC nonetheless experiences and its sturdy market place has helped it hedge towards what for others has been a really turbulent 12 months.

The corporate is valued fairly low proper now and I believe that has to do with the expansion outlook for the enterprise. I do not see something that might put TNC in a spot the place it may well ship sturdy double-digit development YoY, it is simply not that form of firm. I’d view TNC extra as a resilient dividend payer that might make up a smaller portion of a portfolio and supply some stability when markets are risky. Due to this, the marginally low valuation makes numerous sense in my view, and I would wish a good decrease one to make a purchase case right here. I’d say it is pretty valued based mostly on what I’d assume is round 4 – 5% CAGR for the revenues. These projections lead me to price the corporate a maintain for now, with the opportunity of an improve ought to the worth attain an space the place I believe there may be an ample quantity of worth available.

Firm Segments

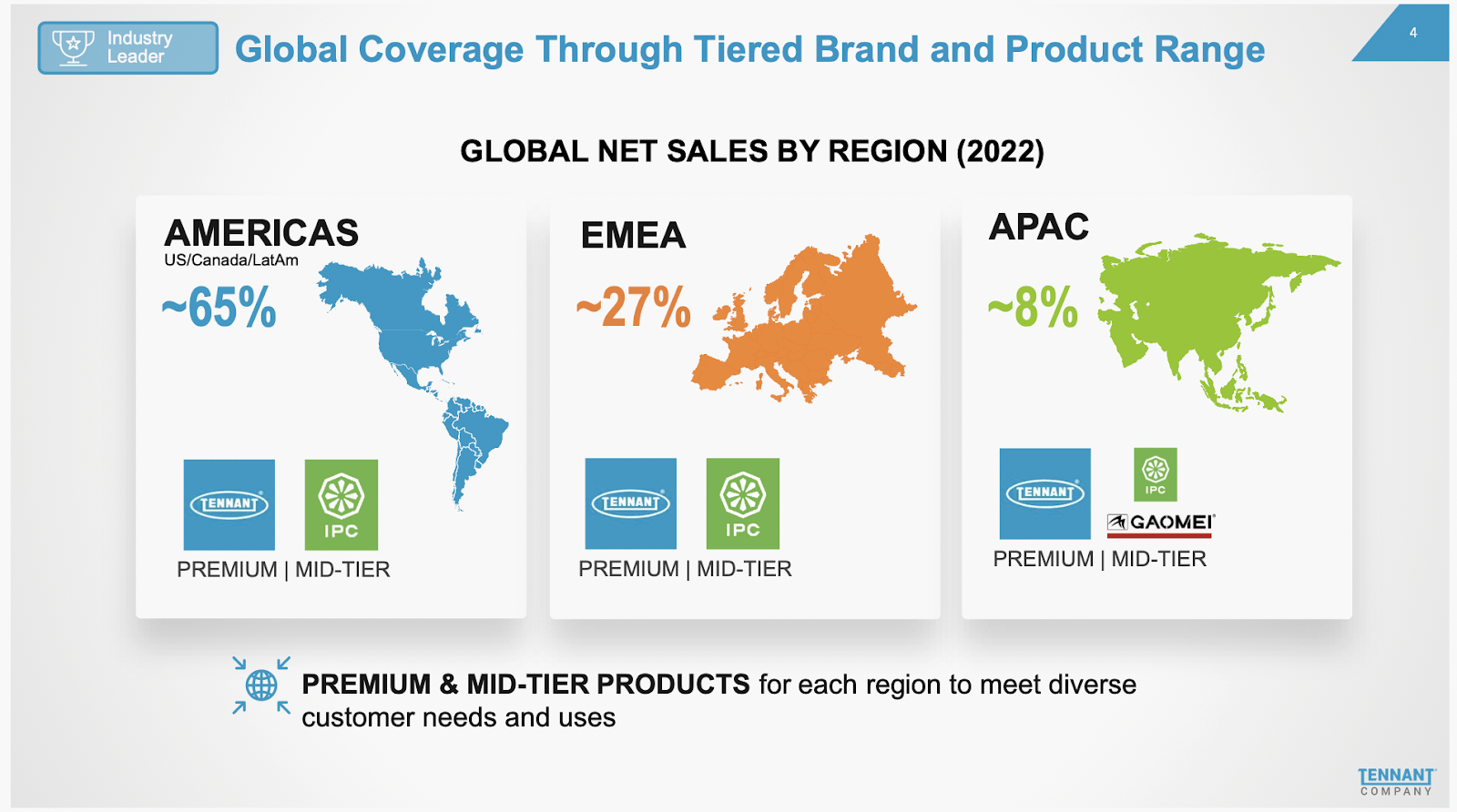

TNC operates within the ground cleansing tools market, with a worldwide presence spanning the Americas, Europe, the Center East, Africa, and the Asia Pacific. The corporate’s various product vary consists of ground upkeep and cleansing tools, progressive detergent-free and sustainable cleansing applied sciences, and a wide range of aftermarket elements and consumables.

Firm Gross sales (Investor Presentation)

TNC provides complete tools upkeep and restore companies, together with asset administration options. To additional assist its clientele, the corporate gives a spread of enterprise options, together with versatile financing, rental, and leasing choices, in addition to superior machine-to-machine asset administration options. When it comes to how this diversified method has netted the corporate over time the compounded 5.09% development price for the highest line I believe could be very sturdy. The corporate had set out some girth targets with a 5-year plan, which they’ve managed to attain a 12 months early. A few of these targets included a 3% annual income development price EBITDA proportion of 15%. I believe that these achievements have been an element within the inventory value performing so nicely over the previous 12 months.

Earnings Highlights

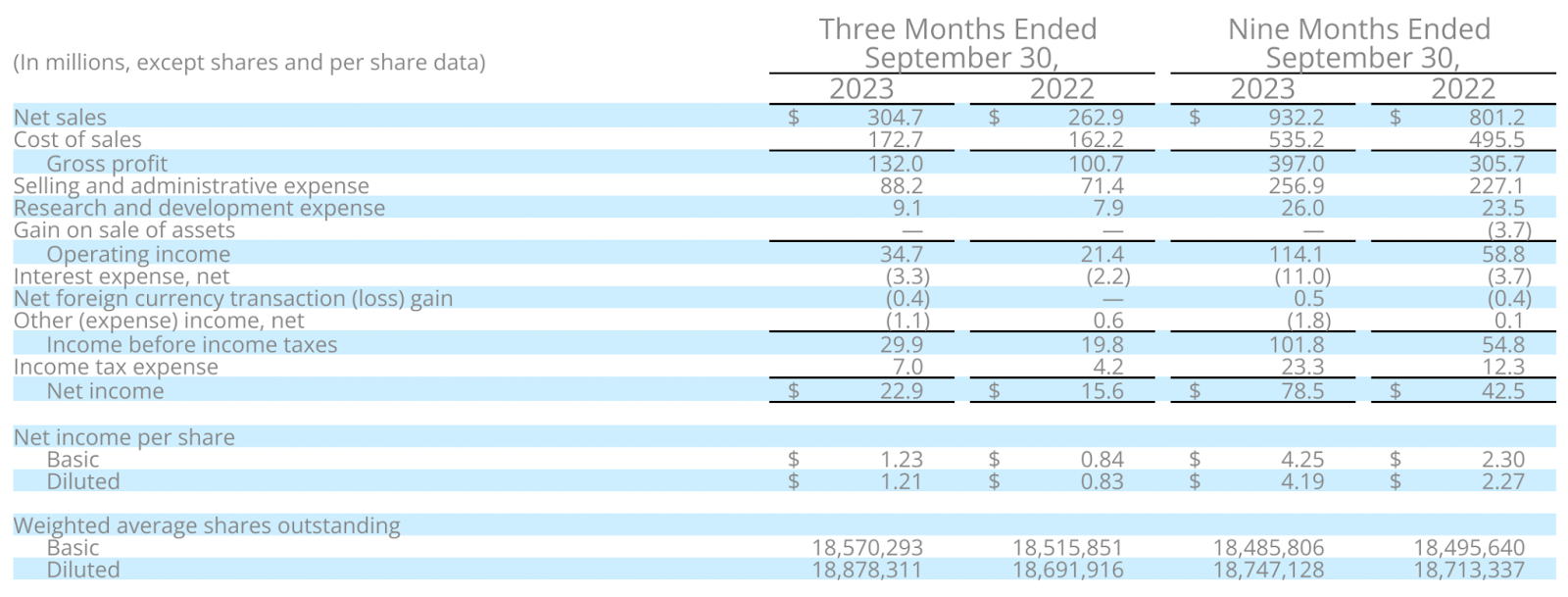

Revenue Assertion (Earnings Report)

Probably the most recent report by TNC was launched on October 31 2023 and we appear to be slightly over a month out from the next report which would offer the full-year outcomes of 2023 by TNC. So far as the earnings assertion goes, it is seen that TNC managed to develop fairly nicely YoY. The revenues reached over $300 million which is only a slight decline from the file ranges seen within the earlier quarter of $321 million. I do assume the revenues will stabilize considerably and extra development as a substitute come from acquisitions. The final major acquisition by the corporate was some years in the past although, after they bought the stake Ambienta had in IPC Group valued at $353 million in complete. This pushed up the debt ranges by nearly 10 fold nevertheless it has since declined by over $100 million.

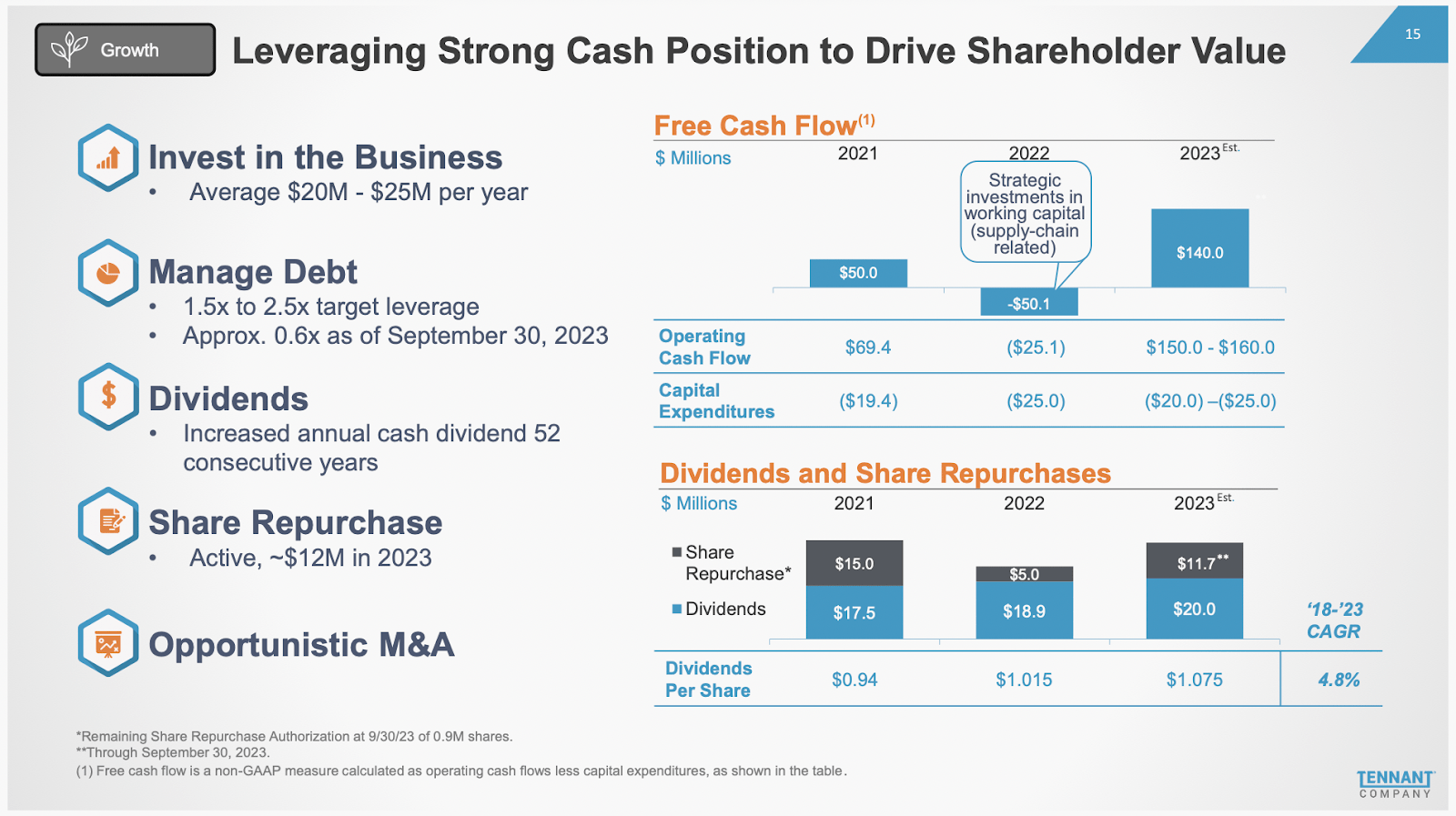

Money Place (Investor Presentation)

The corporate makes it fairly clear that it intends to have a decrease stage of leverage to correctly handle market climates and challenges. The goal debt leverage is 1.5 to 2.4 which proper now could be at 0.6. Which means that the corporate is in a fantastic place to make additional acquisitions and nonetheless keep inside this leverage vary. So far as catalysts that I’m in search of, this will surely be certainly one of them. The expansion of the enterprise organically shouldn’t be that top I believe. The worldwide cleansing merchandise for the family for instance are estimated to develop round 6.5% within the subsequent 7 years in complete. That isn’t a really excessive development market in my view, however I do assume TNC might do a superb job in reflecting that CAGR of their prime line in the identical timeframe, given the market place they’ve acquired up to now.

2023 Steerage (Investor Presentation)

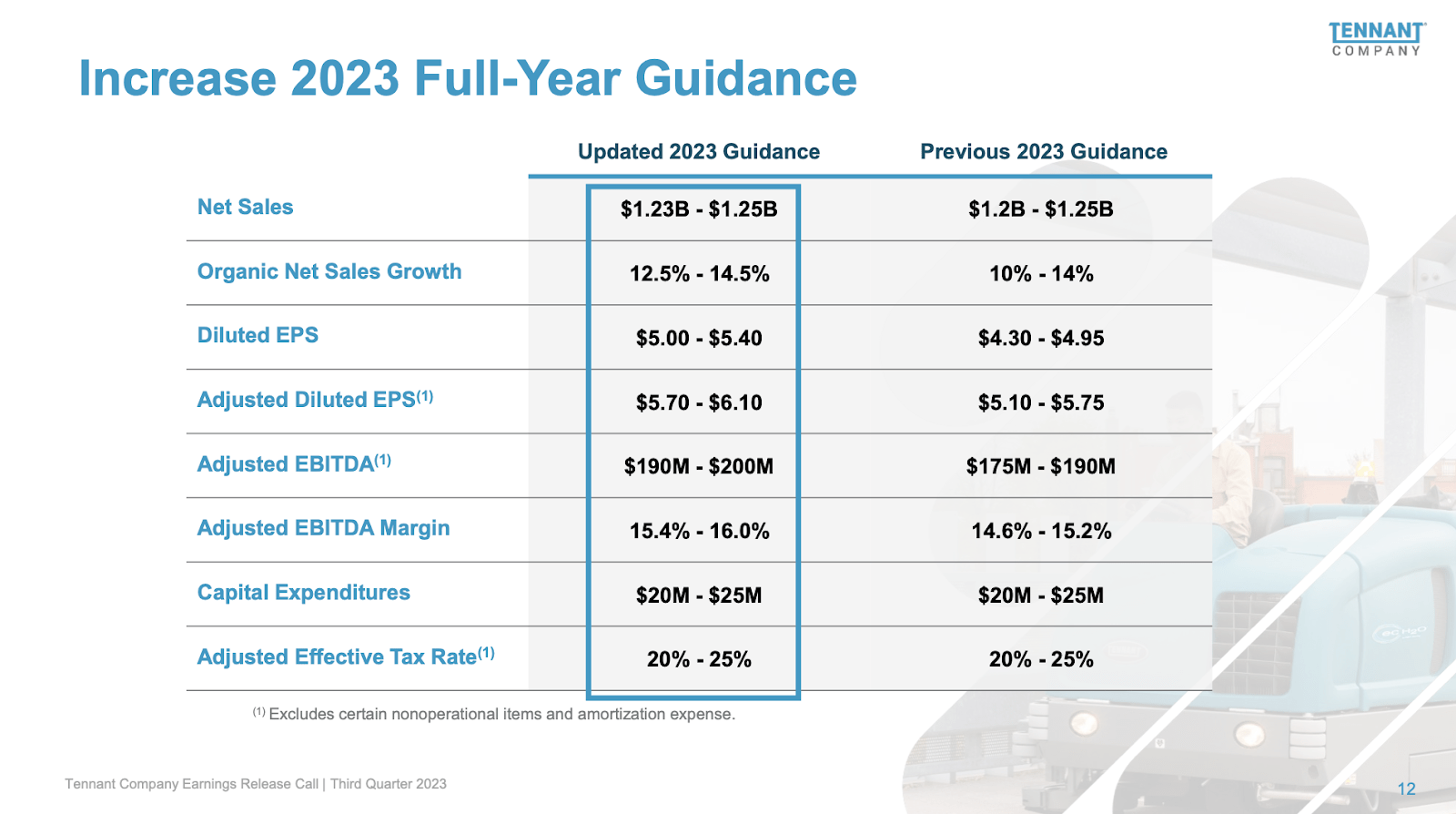

The steerage for 2023 is for gross sales to achieve between $1.23 – $1.25 billion, which is a really tight vary but in addition underscores the comparatively regular and dependable demand that TNC has. This might result in a 12.5% – 14.5% YoY gross sales development. If the margins stay sturdy it could end in $5.4 for the EPS and put TNC at an FWD a number of of 16.6. I’ve made it clear that I do not assume the present valuation is that interesting to purchase at, I would favor one thing within the vary of 13 -14 as a substitute, due to the poor development outlook that also exists with TNC. It is not working in a market with numerous disruption and catalysts that gasoline development, which I’ve to emphasize once more is not one thing damaging essentially. I believe that TNC will produce EPS development of round 5 – 6% over the following 7 years, which might be smaller than the cleansing merchandise market. That stage of development shouldn’t be definitely worth the present a number of and with m most popular one places the corporate at a 12-month value goal of $77 as a substitute. This implies a drop of 16% is critical earlier than I get in, however given the fast rise within the inventory value over the past 12 months, this is not so unlikely if the markets see a broader sell-off.

Dangers

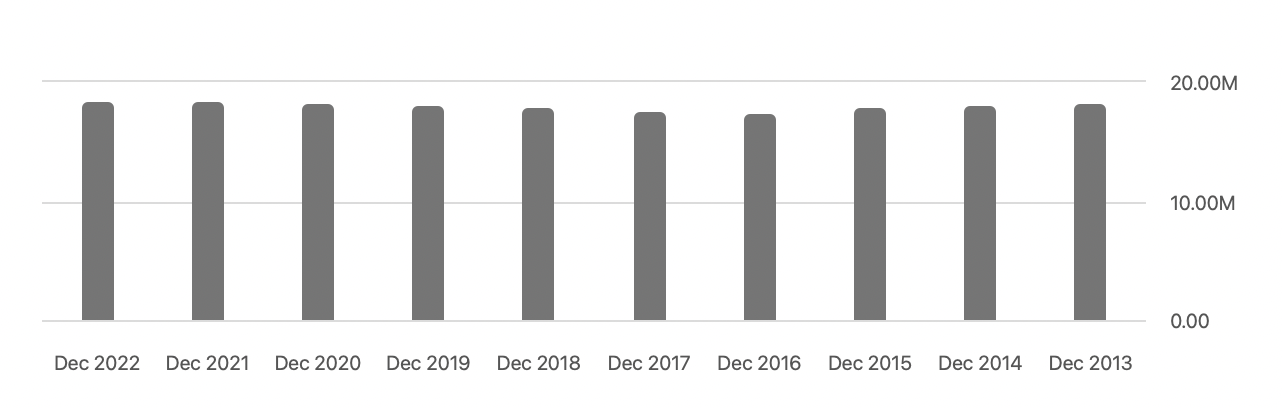

One of many notable dangers related to TNC is the potential for share dilution, a pattern noticed within the firm’s current historical past. Whereas the present stage of dilution is not alarmingly excessive, it stays an vital level of consideration. Ought to the corporate keep excessive charges of dilution, coupled with a possible decline in demand, there could be a necessity for additional share dilution to handle and repay maturing money owed.

Share Dilution (Looking for Alpha)

One other threat that’s placed on the corporate is elevated materials prices. The corporate manufactures a wide range of merchandise and if the revenues cannot climb sooner than the price of revenues there will likely be stress on the margins of the enterprise. Within the final 12 months, the enhancements have gone in the correct course with revenues rising practically 12% and the price of revenues rising roughly 5% YoY as a substitute. Certainly one of my worries is that the continued conflicts within the Crimson Sea are going to disrupt the shipments that TNC has. It is a world firm with 10% of gross sales in Asia. Deliveries to that area all undergo the Crimson Sea. We have now already seen the shipping rates improve fairly quickly previously months due to this escalation, however ought to they keep persistent I’m apprehensive concerning the backside line for TNC. It might consequence within the share value dropping and leaving us with a shopping for alternative, which in the end could be a optimistic maybe.

Ultimate Phrases

I’ve not coated TNC earlier than however doing so now has led me to an organization that I believe can produce fairly regular outcomes over the long run. It operates in a really secure market the place cleansing merchandise and tools are all the time going to be in demand. The corporate has seen margins rise fairly quickly over the previous few years which could have given approach to the inventory value rising simply as quick, however in my thoughts, there is not sufficient incentive right here with the inventory to make for a simply but. My 12-month goal is $77, however I’d nonetheless argue holding onto shares is sensible given the dividend and stability of the enterprise. Quick-term fluctuations within the inventory value might open up a shopping for alternative, however for the second the inventory will likely be a maintain.