JHVEPhoto

The recovery in the automated testing market

Last May, I had written about Teradyne (NASDAQ:TER), predicting that the cyclical trough in the semiconductor Automated Test Equipment (ATE) market should be taken advantage of. Last July, I wrote about Advantest (OTCPK:ATEYY) reiterating a buy, advising that even they had a tough quarter, they would recover in the second half of 2023.

I was early by a few quarters in both cases, and both stocks bottomed out only in October 2023: Teradyne at $83 and Advantest at $27. Teradyne reported better than expected results on April 24th, 2024, and also guided higher, signaling that the worst should be over, after a long and debilitating trough of about 10 quarters.

Where will Teradyne go from here? I believe it is the beginning of an up cycle, and Teradyne too will reap the benefits of the AI growth that has already benefited memory stalwart, Micron (MU), foundry leader Taiwan Semiconductor (TSM) and semiconductor equipment leader Lam Research (LRCX).

The stock is at $143 today and has the potential to grow over 50% to $220 in the next four years on solid revenue and earnings CAGR’S of 13% and 28% respectively.

The arms race for semiconductors, which are indispensable in data centers, generational and transformative AI, gaming, computers, defense, auto and IoT, should provide the duopoly of Teradyne and Advantest sustainable revenue for at least the next decade.

Teradyne Trough (Teradyne, Seeking Alpha, Fountainhead)

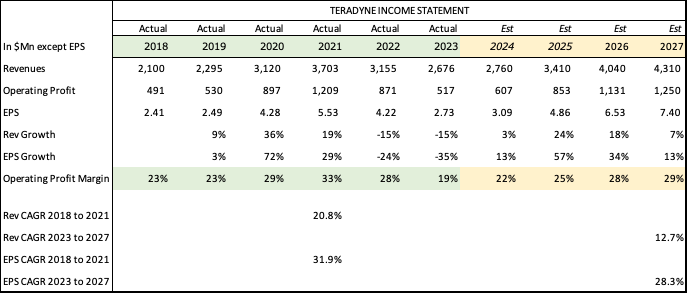

Teradyne had its cyclical through, which lasted a long and painful ten quarters from a peak of $950Mn in Oct 2021, before bottoming out to $599Mn in March 2024. I’m conservatively positing an estimated growth of 61% in the next 4 years to $4.31Bn, much lower than the 76% achieved in the previous cycle on the back of these main catalysts.

- Taiwan Semiconductor’s production in the 3nm node, which finally got off the ground in 2H of 2023.

- Artificial Intelligence demand for generative GPU’s, especially huge demand from memory, which was a big grower for Teradyne in Q1-2024

- The cyclical revival in semiconductor demand.0

- A solid improvement in its robotic division, with further gains from the Nvidia collaboration.

Growth Catalysts

Let’s take a closer look at these catalysts.

More complex and newer chips:

The 3nm surge from TSM has finally gathered fruition after having only one customer, Apple, (AAPL) last year. TSM should achieve 80% capacity utilization of 3nm production in 2024 on the backs of orders from Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) and Mediatek.

One of the key characteristics of the downturn from 2021 to 2023, which saw revenues drop a whopping 15% each year, was the delay in TSM moving to 3nm production. Automated Test Equipment makers require new and improved, more complex semiconductors to be brought to market for testing to increase revenue. User companies such as Apple can expand the useful life of previous equipment if there is no increased complexity or innovation, or if there is low utilization if their own revenues slow down. Thankfully, TSM has confirmed that the 3nm process is in full swing and is likely to create demand for new testing equipment for the next two years, after which we should see demand for the 2nm process nodes.

Artificial Intelligence and huge demand for memory:

From Greg Smith, CEO, on the March 2024 earnings call:

Memory and SoC delivered above our plan and showed strong performance in the quarter driven primarily by AI applications. The impact of AI on our business was seen in networking as well as in Edge AI applications like ADAS. Over 40% of our memory shipments in the first quarter were driven by AI applications.

Greg Smith and CFO, Sanjay Mehta added color stating that HBM was even stronger with increased demand for Q2 and the full year as well. Memory testing was the star in Q1, with a 61% growth rate. To be sure, surging GPU sales and the required high bandwidth memory chips that need to make it all work is finding its way to Teradyne’s revenues as well. They also increased the TAM for Teradyne for memory from $1.2Bn to $1.3Bn on stronger HBM demand, which should grow about 5x the previous year.

Micron, which is one of the larger beneficiaries of HBM demand, is expected to grow revenues by a CAGR of 26% from $25Bn to $40Bn in the next two years, indicating strong demand for memory testing.

The cyclical revival in semiconductor demand

The global semiconductor market should recover with 16% growth in 2024 and 12.5% in 2025, after dropping 8% in 2023. With 16% growth, the entire market should grow to $611Bn worldwide in 2024 and further to $688Bn in 2025. The biggest catalyst – memory with 77% growth to 163Bn or 27% of the entire market and growing further in 2025 by 26% to $204Bn or 30% of the market.

The Global Semiconductor Market (World Semiconductor Trade Statistics)

Besides the overall growth in semiconductors for the next two years, it’s also important to note that TSM continues to get a larger percentage of sales from advanced nodes, and is working on moving speedily to the 2nm process node. It expects to see widespread adoption at an even greater scale, which means more complexity and therefore the need for more testing.

Improvement in robotics with the Nvidia collaboration

In Q-1, Robotics contributed $88 Mn or 15% of total revenues, down 2% YoY. However, Teradyne expects 10-20% growth for the year, which after a down quarter means solid growth in the second half. During the Q1-earnings call, CEO, Greg Smith elaborated further.

We were very pleased to see the team deliver on plan and are expecting sequential growth in the second quarter. We are executing the plan which we expect to deliver 10% to 20% growth in 2024. This plan includes three elements: first is SAM expansion through new offerings. Second is growing our OEM solution provider in large account channels. Third is building increased recurring revenue through service and software offerings.

We executed on new SAM expanding initiatives with the announcement of UR’s collaboration with NVIDIA and the new MiR1200 pallet jack. We grew our UR OEM business 58% year-on-year, and we received the single largest order in the history of MiR from a strategic customer.

The partnership with Nvidia will help Teradyne – They get to use Nvidia’s robotic stack with all the artificial intelligence features using 3D vision for pallet movements and factory / supply chain workspace management, which should give it a competitive edge.

Plus, this almost allows them to create new and better solutions; Teradyne will leverage those tools to great effect and as you see from CEO, Greg Smith’s response below to a question about AI being used for robotics, this should allow them to expand the market. Also using Nvidia’s Omniverse for simulations could be an added benefit for both partners.

Yes. So, for sure, the great thing about AI; there are two primary benefits to AI. One is that it’s far easier to design a solution that is able to deal with variation, whether it is part variation or location variation or other uncertainties that exist in normal manufacturing environments. The solutions end up being far more resilient, so that means that more people would be willing to adopt them.

As I always say, people don’t want to put fragile things into production and AI will help make things more robust. The simplicity of developing things is definitely a huge benefit of AI. So, the demonstration that we did at GTC was a pretty sophisticated visual inspection application. And because we were leveraging a really powerful AI stack from NVIDIA, we were able to put that together in less than two weeks. It was a very fast turnaround to be able to build that solution. And we expect that both customers and customers and especially solution providers are going to be able to leverage that and create solutions to categories of problems that will help drive growth.

The Duopoly

I wrote in detail about the advantages of being in a duopoly in my earlier articles on Advantest and Teradyne, and I’ll summarize the main points below.

Advantest and Teradyne control a substantial share of the ATE (Automated Testing Equipment) market.

The main characteristics of the ATE industry are:

Significant barriers to entry – Advantest and Teradyne have more a century of experience between them and a stranglehold in the ATE business, making it very difficult and costly for new entrants to come in.

A specialized business with a long learning curve: This is a very specialized business that needs strong decades of long relationships with customers, such as Integrated Device Manufacturers (IDM’s) like Intel (INTC) and foundries like Taiwan Semiconductor Manufacturing and Samsung (OTCPK:SSNLF) among others.

High Switching Costs: Switching costs are high for machines that cater to diverse set of semis such as datacenter AI GPU’s, SOC’s and phones, or high volume requirements for memory or storage chips, or different solutions for a gamut of industries from IOT to Auto. Besides, the cost of re-training staff even from Advantest to Teradyne is expensive and customers rarely change between the two.

Great Pricing Power resulting in excellent margins of 27-29% on a regular basis and over 31% in exceptional years. Pricing and revenues depend on complexity of the chips and as Nvidia, AMD and others rush to build their transformative AI chips, this will only increase revenues for Teradyne and Advantest.

Key weaknesses and challenges – what could go wrong?

Delays in new semiconductor production

One of the key characteristics of the downturn from 2021 to 2023, which saw revenues drop a whopping 15% each year, was the delay in TSM moving to 3nm production. The Automated Test Equipment (ATE) industry requires new, improved, and more complex semiconductors to be brought to market for customers to order and replace older machines. User companies such as TSM/Apple can expand the useful life of previous equipment if there is no increased complexity or innovation. Thankfully, TSM has confirmed that the 3nm process is in full swing and is likely to create demand for ATE for the next two years, after which we could see demand for the 2nm process semis. Similarly, delayed production of the 2nm process could also lead to lower revenue for Teradyne and as abundant caution I’ve reduced my 2026 forecast expecting the 2nm process delay the way 3nm was and have only forecasted 7% growth.

Over optimism from Teradyne management

Teradyne management has consistently provided growth forecasts as below, and in my experience while the forecasts are directionally reasonable, they don’t necessarily provide enough margin of safety for cyclical disruptions. For example, while Teradyne forecasts an EPS of $6.5 at mid-point below for 2026, a previous model in 2022, had them forecasting an EPS of $8.75 in 2026.

Teradyne Earnings Model (Teradyne)

AI spending could be front loaded

While everyone and every segment of the semiconductor seems to be gung ho about AI and accelerators, as seen from the capital spend, with Microsoft, Alphabet and Meta alone spending $14, $12 and $6Bn respectively, there is scant evidence of meaningful AI revenue. Microsoft calculated that just 7% of the 31% increase in Azure revenue was from AI. Another report from the Wall Street Journal on AI cited only $3Bn in AI revenue. I suspect there could be a lull before businesses churn out useful applications for end users to successfully monetize that spend.

Valuation may be high

While I have taken a P/E of 30 as a reasonable multiple for Teradyne, clearly Teradyne’s multiples, like all cyclicals, have oscillated a lot between peak and through. We could see Teradyne stay range bound for the rest of 2024, and / or slide heavily to 20x earnings if growth is delayed. From the 10-year chart below, Teradyne after the heady all-time high price of $170 in Nov 2021, dropped like a brick and was stuck between $70 and $100 for around 20 months. It is at a peak P/E of 50 now, with a very wide range, dipping to 12, given the drop in earnings in the trough years 2021 to 2023.

Robust up cycle

Teradyne Financial Forecast (Seeking Alpha, Teradyne, Fountainhead)

Growing revenues: As I showed in the previous table, revenue should have bottomed out in Q1-2024, and even though I don’t estimate Teradyne to grow more than 3% in 2024, growth in 2025 and 2026 should be very robust at 24% and 18% each. If you compare it to the previous up cycle from 2018 to 2021, when Teradyne grew revenue at a CAGR of 20.8%, the CAGR of 12.7% is a fairly conservative estimate. The previous up cycle, though, grew significantly on the back of the iPhone, and also saw significant growth from the pandemic, neither of which will not be followed in this cycle. However, as I outlined in the growth catalysts section, there are enough reasons to grow revenues at a CAGR of 12.7% in the next 4 years.

Operating leverage: Earnings have always grown faster than revenues for Teradyne, the duopoly nature between Advantest and Teradyne ensures that they have strong operating margins and pricing power. I expect earnings to grow at a CAGR of 28% in the next up cycle from 2024-2027, which is similar to the trajectory shown in the previous up cycle with 21% revenue growth and 32% earnings growth. In 2021 Teradyne had an exceptionally strong operating margin of 33%, and I’m confident that they will easily achieve 28% at the bare minimum in 2026 and 2027.

My target price for Teradyne is 30x 2027 forward EPS of $7.4 = $222 or a total return of 54% or 15% annualized over 3 years.

This stacks up well with close competitor Advantest, which is at a similar high P/E of 55, as it grows out of its trough. If these estimates pan out, Teradyne’s P/E drops to 19 in 2026.

Teradyne and Advantest (Seeking Alpha, Teradyne, Advantest, Fountainhead)

I own Teradyne and last added around $140, with most of my purchases in the $100 to $110 range, and plan to hold it for at least another 2-3 years. The strengths of the duopoly, the robust growth in memory testing, strong requirements from AI and a much better overall semiconductor up cycle make it a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.