jetcityimage/iStock Editorial by way of Getty Photos

The Tesla (NASDAQ:TSLA) inventory has been off to a weak begin this yr, dropping near a 3rd of its worth whereas the broader S&P 500 index rose near 11% over the identical interval. Rising weak spot within the EV demand atmosphere regardless of aggressive worth cuts on the expense of Tesla’s margins stays a key space of concern for buyers.

Particularly, markets had earlier anticipated full yr 2024 deliveries to vary between 2 million to 2.1 million items, with demand anticipated to choose up within the again half of the yr. But the mix of weak demand in China throughout the first two months of the yr, alongside manufacturing disruptions in Berlin as a result of Red Sea crisis are including complexity to Tesla’s outlook. That is in keeping with the 1Q24 delivery bust reported this morning.

Wanting forward, we see restricted structural tailwinds to Tesla’s core auto enterprise. As auto gross sales progress is predicted to stay gradual, alongside restricted margin enlargement in Tesla’s favour of volumes over pricing, we remain confident that buyers’ focus will more and more tilt in direction of FSD progress. That is in keeping with CEO Elon Musk’s latest announcement of a one-month free FSD trial on all U.S. deliveries shifting ahead. Along with boosting uptake for the high-margin software program subscription, the most recent perk is more likely to be a constructive on Q2 volumes.

Nevertheless, intensifying regulatory hurdles imply restricted progress to full recognition of related revenues into P&L over the near-term, providing restricted respite to Tesla’s bottom-line. Taken collectively, we consider the inventory will stay range-bound at present ranges (~$170-range). A structural restoration would require materials FSD monetization progress to unlock pent-up worth attributable to the expertise, which is central to the Tesla inventory outlook.

Tesla 1Q24 Supply Replace

Tesla delivered 386,810 automobiles in 1Q24, representing y/y decline of -9% and sequential decline of -20%. Particularly, Mannequin 3/Y volumes, which proceed to dominate the gross sales combine, declined by -10% y/y throughout 1Q24. In the meantime, Tesla has stopped individually disclosing Mannequin S/X volumes, and have as a substitute reported a lump-sum of 17,027 deliveries for “other models” that seemingly embrace the premium passenger line-up alongside Cybertruck and Semis. The outcomes are largely in keeping with the mix of shopper weak spot – particularly in China – and restricted pricing incentives on the premium line-up throughout 1Q24.

Mannequin 3/Y’s disappointing 1Q deliveries aligns with beforehand anticipated headwinds pertaining to revised guidelines for tax credit score eligibility underneath the Inflation Discount Act. Recall that the Treasury Division had tightened battery sourcing necessities on EVs eligible for the complete $7,500 tax credit score underneath the IRA. The change, which took impact January 1, eliminates Tesla’s best-selling rear-wheel drive and long-range Mannequin 3 variants from the eligibility list. This had seemingly pulled ahead a few of Mannequin 3 demand in 4Q23. Even Tesla’s determination to unveil the refreshed Mannequin 3 line-up to the U.S. market in 1Q24 – 1 / 4 later than in China and Europe – did little to arrest a sequential decline in associated gross sales volumes.

Intensifying competitors in China additionally stays a heightened headwind for Tesla. Particularly, latest information from China’s Passenger Automotive Affiliation (“CPCA”) exhibits Tesla had solely shipped barely over 60,000 automobiles from its Shanghai facility in February. This represents a -16% m/m decline in volumes, with about 132,000 vehicles shipped from Giga Shanghai in the complete first two months of the yr mixed. And solely about half of this quantity was absorbed by the native Chinese language EV market, regardless of Tesla’s embrace for deep worth cuts.

Information from tesla.cn

These are a few of the lowest volumes from Tesla’s Shanghai facility since December 2022. Tesla’s newest outcomes additionally diverge from rivalling Chinese language upstarts – together with Li Auto (LI), NIO (NIO), XPeng (XPEV), and key native rival BYD (OTCPK:BYDDF / OTCPK:BYDDY). Many completed 1Q24 with resilient deliveries regardless of the seasonal drop-off in February volumes as a result of Lunar New 12 months vacation, along with macroeconomic and aggressive headwinds. And though BYD’s supply of 300,114 BEVs within the first quarter falls beneath Tesla’s volumes over the identical interval, the Chinese language automaker seemingly continues to carry the crown within the native market. Particularly, Tesla had shipped 131,812 vehicles from Giga Shanghai within the two months by way of February 2024, with solely 53% or 69,860 items offered within the Chinese language market in accordance with information from the CPCA. This compares to BYD gross sales of greater than 160,000 BEVs throughout the identical interval, with the bulk shipped to the Chinese language market, highlighting Tesla’s struggles in increasing market share. This continues to spotlight the toll of intensifying competitors and shopper weak spot dealing with Tesla in its core Chinese language market.

The EV Slowdown is Right here to Keep

Wanting forward, we count on Tesla’s core auto enterprise to take a again seat as progress and demand are anticipated to face an prolonged slowdown. Particularly, Chinese language EV gross sales progress is predicted to gradual to 25% y/y in 2024, down from 36% noticed in 2023 and 96% in 2022. In the meantime, within the U.S., EV gross sales are anticipated to develop by about 30% y/y in 2024, decelerating from 50% enlargement noticed in 2023. Nevertheless, demand is more likely to favour the growing herd of non-Tesla choices. Particularly, 1Q24 U.S. EV gross sales grew 15% y/y. But stripping Tesla gross sales from the metric, U.S. 1Q24 EV gross sales grew a whopping 33%, matching momentum noticed within the prior yr interval.

Consequently, we count on ongoing worth adversities for Tesla, which might, inadvertently, drive renewed headwinds to its auto gross margins. This could seemingly additional complicate Tesla’s path to restoring 20%+ auto gross margins. The prolonged worth headwinds are more likely to persist, as Tesla stays dedicated to driving quantity progress essential for optimizing its aspired market share management in autonomous mobility. That is more likely to overshadow declining battery prices and early optimism on the longer-term ramp-up of its next-generation automobile platform, which guarantees up to 50% value reductions.

Gauging the Worth of FSD

FSD progress has grow to be extra vital than ever for Tesla’s valuation outlook. Admittedly, a lot of the inventory’s outsized premium has lengthy trusted Tesla’s high-margin FSD and robotaxi prospects. But with normalizing quantity progress, Tesla faces an growing pivot in buyers’ deal with the way it plans to optimize monetization of its autonomous mobility applied sciences.

This pent-up worth has grown in tandem with Tesla’s sturdy auto market share beneficial properties lately. The larger Tesla’s automobile gross sales volumes, the larger its FSD adoption prospects, therefore administration’s precedence for supply progress over near-term auto gross sales margins. As mentioned in a previous coverage on the inventory, Tesla’s EV market management is essential to making sure optimization of the anticipated lifetime worth per buyer, particularly in excessive margin subscriptions essential to bolstering its steadiness sheet.

Moreover, a degree typically ignored is the lifetime worth of Tesla automobile gross sales. Along with full self-driving (“FSD”) subscription gross sales that haven’t any definitive timeline on realization into income as a consequence of mounting regulatory hurdles for Degree 4/5 autonomous mobility, Tesla automobile gross sales are additionally supply to adjoining income streams resembling in-vehicle infotainment subscription gross sales and Supercharging community gross sales. As automobile gross sales volumes proceed to develop – albeit at decrease profitability within the near-term – adjoining income streams would profit from extra demand at incrementally decrease marginal prices over the lifetime of the automobile.

Supply: “Tesla Overcomes Demand Risks”

Admittedly, FSD-related revenues can’t be completely acknowledged into Tesla’s P&L but as a consequence of regulatory constraints. Nevertheless, sturdy adoption is in itself sufficient to buoy buyers’ optimism of ensuing valuation tailwinds for Tesla. That is in keeping with Musk’s latest announcement to supply a one-month free trial on Tesla’s FSD subscription on all U.S. deliveries. This might be accompanied by a complementary walkthrough and demo previous to the completion of the automobile’s handover to its new proprietor. We consider the initiative could possibly be a constructive to Q2 volumes by incentivizing potential automobile patrons available in the market to decide on Tesla. In the meantime, the perk might additionally drive larger uptake of the $199/month subscription (or $12,000 outright), and reinforce Tesla’s lifetime income prospects from its main share of EVs in operation.

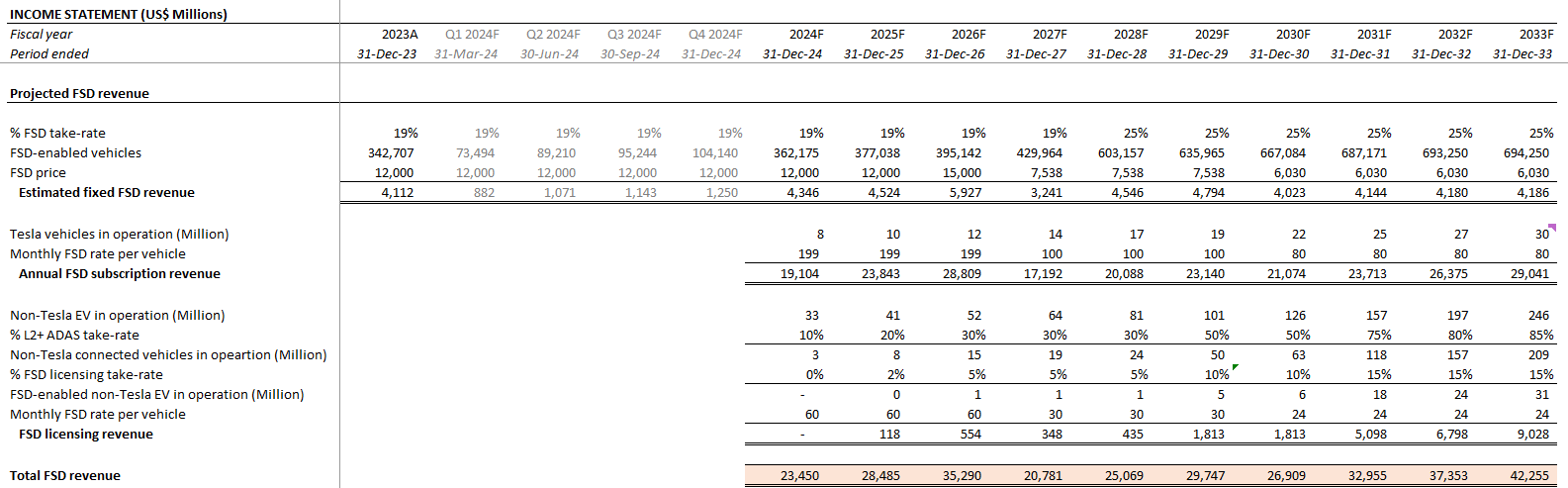

Particularly, we consider Tesla has three avenues to producing income from its FSD expertise: 1) outright FSD buy from Tesla house owners, 2) month-to-month FSD subscriptions from Tesla house owners, and three) FSD licensing to third-party OEMs. This differs from our earlier forecast, which estimates FSD-related revenues from anticipated uptake on longer-term Tesla automobile gross sales.

1) Outright FSD buy

Tesla at present sells a “perpetual license” for its FSD software program to house owners at $12,000. That is down from a earlier charge that goes as excessive as $15,000 only a yr in the past. The most recent business information estimates near 285,000 new FSD prospects in Tesla’s North American market in 2022, which represents uptake of about 22% on gross sales of 1.3 million automobiles that yr. Our estimate assumes 25% FSD perpetual license uptake on future annual Tesla automobile gross sales. The idea considers that almost all of potential customers would go for the month-to-month subscription various as a substitute as a consequence of private causes resembling the common supposed size of car possession. Observe that the present $12,000 outright price ticket implies breakeven at five-year automobile possession based mostly on the $199/month subscription charge, and isn’t transferrable between Tesla automobiles. Our forecast for long-term income generated FSD perpetual license gross sales additionally assumes a discount within the worth, because the product beneficial properties regulatory approval and adoption ramps at scale.

Creator

2) FSD month-to-month subscription

Tesla additionally gives FSD subscription at a charge of $199 per automobile per 30 days. We consider this would be the hottest alternative for potential FSD customers within the longer-term, given flexibility and financial causes. As talked about earlier, the FSD perpetual license choice is non-transferrable and implies automobile utilization of greater than 5 years to breakeven. This compares to the common American’s choice to personal a automobile for five years or less. Equally, we count on the month-to-month subscription charge to come back down over time as effectively to foster mass market adoption and, inadvertently, higher economies of scale for Tesla’s FSD margins.

Creator

3) Third-party OEM FSD licensing

Along with FSD adoption for Tesla automobiles, the corporate can be eyeing licensing alternatives for the expertise. Nevertheless, adoption is more likely to stay gradual, particularly given intensifying regulatory scrutiny over Tesla’s FSD product, and broader business skepticism in regards to the trajectory of autonomous mobility developments.

I actually suppose plenty of automobile corporations needs to be asking for FSD licenses. And we have had some tentative conversations, however I believe they do not consider it is actual fairly but. I believe that may grow to be apparent most likely this yr. And I do need to emphasize that if I had been CEO of one other automobile firm, I might undoubtedly be calling Tesla and asking to license Tesla full self-driving expertise. It is undoubtedly the sensible transfer.

Conservatively, we count on FSD licensing to third-party OEM to be already within the works, with potential for nominal uptake starting subsequent yr, which is according to administration’s commentary. Our forecast for related gross sales is predicated on an estimated 10-year CAGR of twenty-two% on non-Tesla EVs in operations over the longer-term, with the extra consideration of L2+ ADAS uptake and subsequent FSD uptake. We count on third-party FSD licensing uptake to be comparatively decrease as a proportion in comparison with potential Tesla automobile house owners.

That is in line Tesla’s competitors in opposition to ongoing in-house developments throughout each legacy automakers and EV upstarts alike, alongside different proprietary choices offered by companies like Mobileye (MBLY) and Luminar Applied sciences (LAZR). As an illustration, Volkswagen Group (OTCPK:VWAGY / OTCPK:VLKAF / OTCPK:VWAPY) has adopted Mobileye’s SuperVision product to empower the autonomous driving options throughout its model portfolio, together with Porsche. In the meantime, others like Mercedes-Benz (OTCPK:MBGAF/ OTCPK:MBGYY) have partnered with chipmakers like Nvidia (NVDA) for the in-house growth of its personal proprietary self-driving methods. As an illustration, the German automaker’s “Drive Pilot” self-driving system has additionally lately grew to become the primary to obtain Degree 3 ADAS regulatory approval from California. Particularly, Degree 3 ADAS certification validates Drive Pilot’s capacity in monitoring exterior driving situations, regardless of nonetheless requiring human intervention always. In the meantime, Tesla’s FSD is barely authorised for Level 2 ADAS, that means a human driver nonetheless must be actively monitoring exterior driving situations always, whereas holding fingers on the steering wheel.

Creator

Taken collectively, we count on pent-up FSD income progress at a 10-year CAGR of seven%. Although nominal in comparison with present core auto gross sales, the low marginal prices of FSD-related income underpins substantial money flows essential to the inventory’s valuation outlook.

Creator

Value Issues

With expectations for an growing pivot in buyers’ focus to FSD progress, as core auto gross sales gradual, we count on problem for a structural restoration within the Tesla inventory over the near-term. The Tesla inventory is more likely to keep range-bound within the $160-level within the near-term, with potential draw back to $162 based mostly on our evaluation.

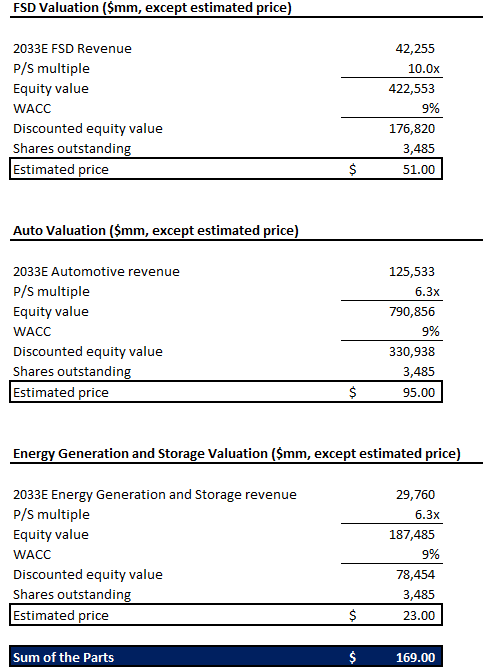

Our worth goal is derived from a sum-of-the-parts valuation that considers the elemental outlook of Tesla’s core auto, vitality era and storage, and rising FSD companies. Admittedly, Tesla additionally touts substantial prospects attributable to its robotaxi ambitions, regardless of multi-year delays from its original go-to-market timeline. Nevertheless, contemplating the unsure regulatory trajectory over autonomous mobility applied sciences, related prospects can’t be fairly quantified in the meanwhile, in our opinion.

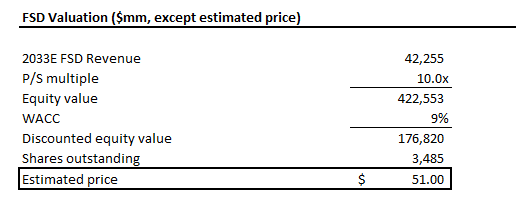

1) FSD valuation

We estimate an intrinsic worth of $176.8 billion for Tesla’s FSD enterprise. The estimate applies a 10x a number of to our earlier mentioned long-term FSD income projections. The valuation a number of utilized is according to the common noticed throughout high-growth (30%+) software program sector friends with the same revenue margin trajectory. A 9% WACC according to Tesla’s capital construction and danger profile can be utilized to low cost the estimated 2033 worth again to 2024.

Creator

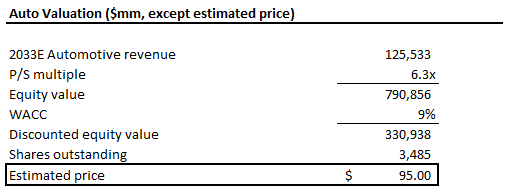

2) Auto valuation

We estimate an intrinsic worth of $330.9 billion for Tesla’s core auto enterprise. The estimate applies a 6.3x a number of on our long-term auto income forecast for Tesla, adjusted for the most recent supply outcomes. The valuation a number of utilized is according to the common noticed throughout Tesla’s megacap friends that exhibit the same progress profile. We consider it is a higher valuation benchmark in comparison with our earlier use of tendencies noticed throughout the mid-cycle U.S. OEM common, contemplating Tesla’s technology-driven, higher-margin enterprise mannequin which is deserving of an incremental premium. A 9% WACC can be utilized to low cost the estimated 2033 worth again to 2024.

Creator

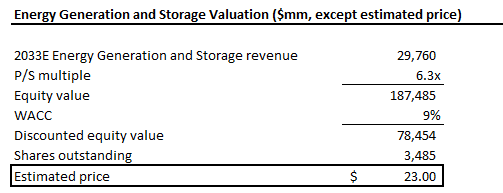

3) Power era and storage valuation

We estimate an intrinsic worth of $78.5 billion for Tesla’s vitality era and storage enterprise. The estimate additionally applies a 6.3x a number of on our long-term vitality era and storage income forecast for Tesla. The valuation a number of utilized is according to the common noticed throughout Tesla’s megacap friends that exhibit the same progress profile. We consider the usage of its megacap friends as a substitute of legacy vitality era and storage business as comparable friends is a extra satisfactory metric for Tesla’s enterprise, given its proprietary applied sciences within the discipline and better progress outlook. A 9% WACC can be utilized to low cost the estimated 2033 worth again to 2024.

Creator

Taken collectively, the enterprise ought to have a sum-of-the-parts valuation of about $586.2 billion, or $169 apiece based mostly on diluted shares excellent of three,485 million items reported in 4Q23. That is according to the inventory’s pre-market buying and selling worth on April 2 upon launch of 1Q24 supply outcomes.

Creator

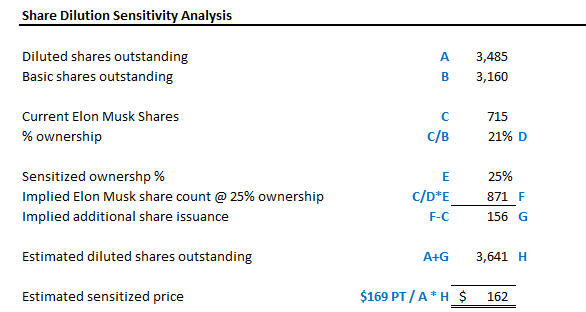

Nevertheless, our draw back worth for Tesla of $162 apiece is derived based mostly on anticipation of additional dilution dangers sooner or later. That is according to Musk’s earlier push for 25% possession in Tesla with a purpose to proceed with AI developments on the firm, which is essential to its outlook.

Contemplating Musk’s lately reported possession of about 21% along with his 715 million shares in Tesla, it implies additional dilution of about 156 million items of Tesla shares to deliver his possession as much as 25%. This could lead to an estimated diluted share depend of about 3,641 million items. At an estimated intrinsic worth of $586.2 billion for Tesla, our projection is equal to $162 apiece. Though it stays unsure on whether or not the Board would approve such requests, the chance shouldn’t be ignored given Musk’s affect over the model. This sentiment might probably function incremental downward strain weighing on Tesla’s worth efficiency.

Creator

Conclusion

The most recent supply bust for Tesla is a warning for not solely the corporate however the broader EV business. Though buyers’ confidence in Tesla’s market management and FSD prospects seemingly stays, the inventory continues to face draw back dangers forward given weak spot to its ahead basic story. That is additionally in keeping with the inventory’s persistent valuation premium at 59x ahead earnings in comparison with its auto and megacap friends’ common. This accordingly highlights elevated execution dangers forward for Tesla and growing urgency for the corporate to ship on different features of its present valuation premium.