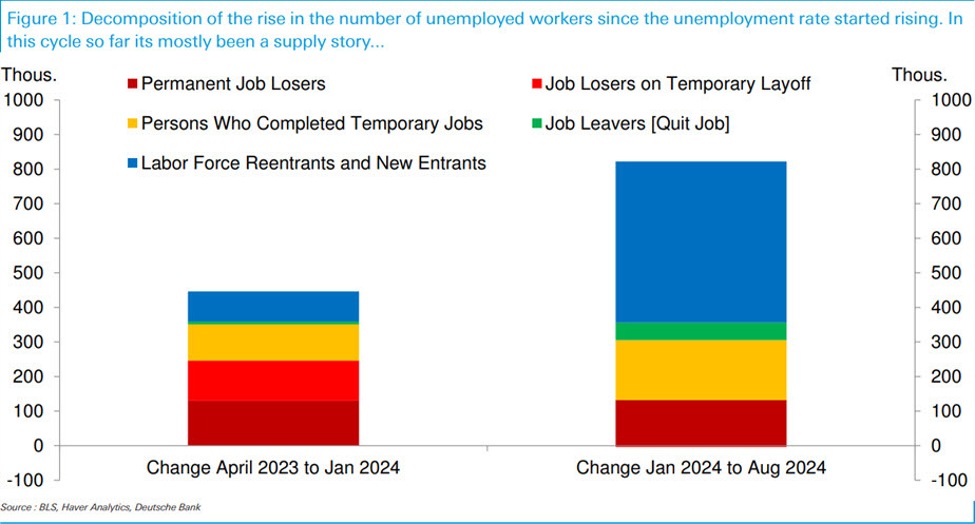

Jim Reid at Deutschebank makes a great point in a note today. He illustrates that US unemployment has risen to 4.2% from 3.4% almost entirely due to people entering or re-entering the labor force.

Then goes on to warn that it can quickly change to something problematic. A look at the past 13 recessions shows that when you do get a first negative print on non-farm payrolls, it

tends to happen out of nowhere and tends to be the start of a trend.

Reid writes this:

The risk for the Fed is if and when job

losses actually arrive in the payrolls report, you tend to get little warning

(as we showed in Friday’s CoTD). With hiring now relatively soft it wouldn’t

take much for the Fed to be behind the curve and a string of 50bp cuts to

follow. With markets now pricing in over 250bps of cuts by January 2026 there

has to be a reasonably high market expectation in the fixed income space of

this policy error occurring.

That’s a great way of framing it and helps to explain why bonds have held a really strong bid despite some decent economic data.

US 2s daily