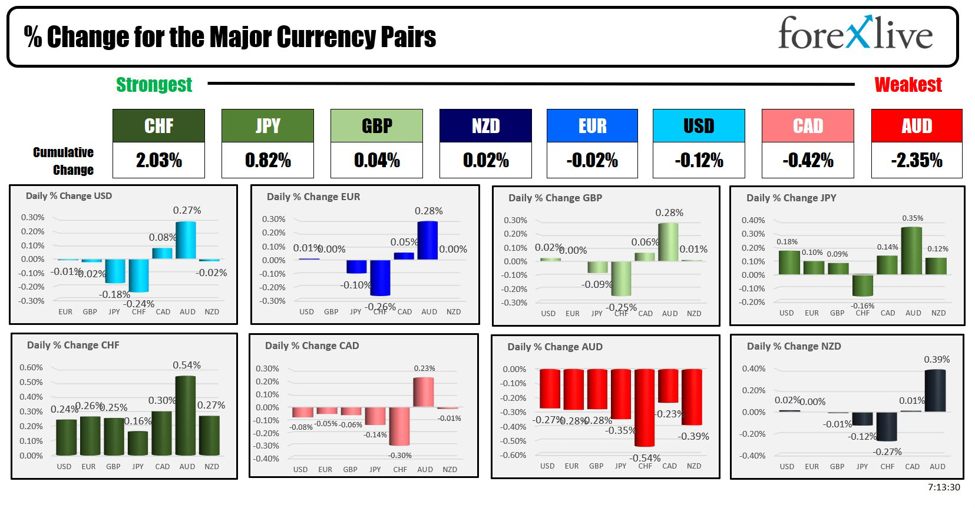

The CHF is the strongest and the AUD is the weakest as the NA session begins.

Today at 8:30 AM ET, Canada will release its July jobs report. The expectation are for:

- Employment Change (Jul): Estimate 22.5k, Prior -1.4k

- Unemployment Rate (Jul): Estimate 6.5%, Prior 6.4%

- Full-Time Employment Change (Jul): Prior -3.4k

- Part-Time Employment Change (Jul): Prior 1.9k

- Participation Rate (Jul): Prior 65.3%

- Average Hourly Wages (Permanent, Jul): Prior 5.60%

Adam posts this morning that the data will be releases at a time where the consumer is cutting back spending despite the 2 successive cuts in rates by the BOC.

“Canadian consumers are pulling back this summer after years of pandemic revenge spending,” RBC writes, nothing that sales have fallen in six of the past seven months.

In other central bank news,

- Boston Fed President Susan Collins indicated that it may soon be appropriate to ease monetary policy, contingent on data aligning with current expectations. She emphasized that the timing and pace of any rate cuts will be data-dependent, suggesting a cautious approach to policy adjustments.

- Kansas City Fed President Jeffrey Schmid also spoke and stated that if inflation continues to come in low, it would be appropriate to lower interest rates, although he emphasized that the Fed is not yet at its 2% inflation target. Schmid noted that the current Fed policy stance isn’t overly restrictive and stressed the importance of staying focused on the Fed’s dual mandate. He acknowledged a noticeable cooling in the labor market, which he views as necessary for easing inflation, but cautioned that the path of Fed policy will be determined by ongoing data and the overall strength of the economy.

- Federal Reserve Bank of Chicago President Austan Goolsbee emphasized the need for the Federal Open Market Committee (FOMC) to see more employment data before making policy decisions. He noted that while the economy is returning to more normal conditions, the Fed’s policy remains tight. Goolsbee highlighted that the Fed monitors markets but does not let them dictate policy. He raised concerns about whether the job market will stabilize or deteriorate further, stressing the importance of looking beyond just payroll data and single-month figures. Goolsbee acknowledged that any Fed action will likely displease some parties, but the Fed’s role is to clearly outline the criteria for adjusting rates, independent of political considerations.

The Fed passed on a rate change last week with the next meeting on September 18. The story remains they are watching the data.

Latar this month the Jackson Hole Conference will take place (August 22 -24). The door will be there for the Fed Chair to pave the way (explicitly) for a change, but he may choose to keep the storyline the same. Next week US CPI and PPI data will be released along with retail sales but he will not have the current PCE data as it won’t be released until later in the month. .

In an aside, in a speech at Mara Lago, GOP candidate Trump, said that if elected president he should have say on US interest-rate policy saying:

“I feel the president should have at least (a) say in there. Yeah, I feel that strongly. I think that in my case, I made a lot of money, I was very successful, and I think I have a better instinct than, in many cases, people that would be on the Federal Reserve or the chairman.”

HMMMMM

A snapshot of the other markets as the North American session begins shows:

- Crude oil is trading up $0.47 or 0.62% at $76.66. At this time yesterday, the price was at $75.31

- Gold is trading near unchanged at $2426.42. At this time yesterday, the price was trading at $2408.50

- Silver is trading down five cents or -0.20% to $27.48. At this time yesterday, the price is trading at $26.96

- Bitcoin is trading at $60,693. At this time yesterday, the price was trading at $57,533

- Ethereum is trading at $2638.40. At this time yesterday, the price was trading at $2449.90

In the premarket, the snapshot of the major indices are now lower

- Dow Industrial Average futures are implying a decline of -20.49 points. Yesterday, the Dow Industrial Average rose 683.04 points or 1.76% at 39446.50

- S&P futures are implying a decline of -8.56 points. Yesterday the S&P index rose 119.79 points or 2.30% at 5319.30

- Nasdaq futures showing decline of -51.57 points. Yesterday the index rose 464.22 points or 2.87% at 16660.02

Coming into the day, the NASDAQ and S&P are on pace for the fourth straight weekly decline despite the strong gains yesterday. Monday with declines of 3.0% in the S&P and 3.4% in the Nasdaq were a lot to make up. The Dow is working on its second consecutive weekly decline. The numbers for the week are showing:

- Dow Industrial Average average, -0.73%..

- S&P index, -0.51%

- NASDAQ index, -0.69%

Yesterday, the small-cap Russell 2000 rose 49.31 points or 2.42% at 2084.42

European stock indices are trading higher:

- German DAX, +0.17%

- France CAC, + 0.36%

- UK FTSE 100, +0.42%

- Spain’s Ibex, +0.67%

- Italy’s FTSE MIB, +0.18% (delayed 10 minutes).

Shares in the Asian Pacific markets closed mixed:

- Japan’s Nikkei 225, +0.56%. For the week the Nikkei fell -2.46%.

- China’s Shanghai Composite Index, -0.27%. For the week the index fell -1.48%..

- Hong Kong’s Hang Seng index, +1.17%. For the week the index rose 0.5%

- Australia S&P/ASX index, -0.23%. For the week the index fell -2.1%

Looking at the US debt market, yields are moving lower:

- 2-year yield 4.021%, -2.2 basis points. At this time yesterday, the yield was at 3.959%

- 5-year yield 3.784%, -4.9 basis points. At this time yesterday, the yield was at 3.746%

- 10-year yield 3.943%, -5.3 existence. At this time Friday, the yield was at 3.925%

- 30-year yield 4.232%, -5.4 basis points. At this time Friday, the yield was at 4.233%

Looking at the treasury yield curve, the spreads are showing

- The 2-10 year spread is at -7.6 basis points. At this time yesterday, the spread was at -3.2 basis points.

- The 2-30 year spread is at +21.3 basis points. At this time yesterday, the spread was +22.5 basis points.

In the European debt market, the benchmark 10-year yields are lower: