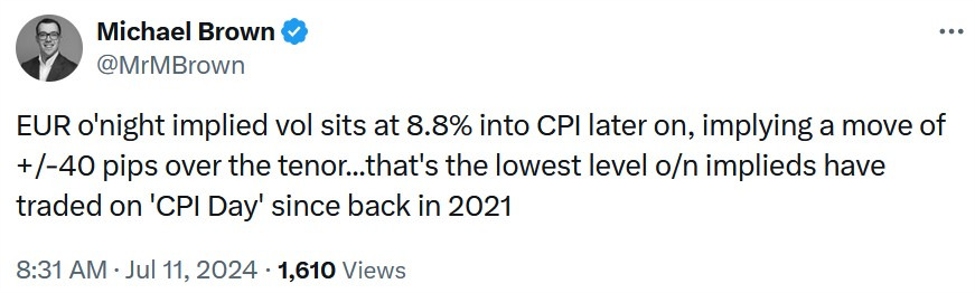

Michael Brown, Senior Research Strategist at Pepperstone, shared on X an interesting finding today. “The EUR overnight implied volatility sits at 8.8% into CPI later on, implying a move of +/-40 pips over the tenor. That’s the lowest level o/n implieds have traded on ‘CPI Day’ since back in 2021”.

Michael Brown’s post on X

This is just another evidence showing us that the importance of inflation data is starting to fade and the market’s focus has shifted towards growth and the labour market. There are two main reasons for such development:

Central Bank Focus

The first one is that the Fed has been mentioning countless times that they are very focused on the labour market and that an unexpected deterioration will call for a rate cut. In fact, the only path for interest rates at the moment is downwards. If inflation stays high, the Fed will just keep rates steady, but if it continues to ease, the Fed will cut.

Effective Fed Funds Rate

Business Cycle

The second reason is tied to the business cycle. In different parts of the cycle, we can see the market focusing on different things. For example, coming out of a recession, nobody cares about inflation because there’s very little pressure on it given that the economy is recovering and there’s lots of unutilised resources in the economy.

On the other hand, when we are well into an expansion, inflation starts to become the main focus as the market expects the central bank to tighten policy to slow down the economy and bring it back in balance. If the central bank keeps conditions tight for too long or it overtightens, then the economy could slip into a recession.

Business Cycle (illustration by Invesco)

Right now, we are in a “slowing but growing” phase and the Fed will need to time lots of things correctly to achieve the soft landing. If it fails to do it, the next thing we will be talking about is a hard landing.