niphon

The ECB expected to cut

The European Central Bank is widely expected to cut interest rates on Thursday, in what seems like a policy rate normalization.

Essentially, it appears that the ECB has achieved a soft-landing – the EU GDP is moderately positive, inflation is just above the 2% target, the unemployment rate is stable, and the European stock market indices are in the bull market.

On the other side of the Atlantic, the Fed is not expected to start cutting interest rates this summer, with possible cuts coming in November or December, although some believe that the Fed will not able to cut in 2024 at all. Specifically, inflation in the US seems to be sticky just below the 4% level, and that’s too high for the Fed to start normalizing interest rates. At the same time, the unemployment rate in the US is increasing, while the GDP growth is slowing. The US is facing a stagflationary environment.

Despite the stagflationary environment in the US, the US stock market is also in the bull market, with the S&P 500 near the all-time highs. The key factor behind the US stock bull market has been the expectations of soft-landing and the Fed’s policy rate normalization – exactly what’s about to unfold in the EU.

The question is whether the European soft-landing is preceding the US soft-landing, and the ECB cuts are signaling that the Fed cuts are coming. If yes, this could justify the bull market in the US stock market, and the European stock market.

In other words, the ECB cut could be signaling that the global central banks are soft-landing the post-pandemic economy, and that would be a positive for global stocks.

The argument in this article is that the global soft-landing is unlikely. Specifically, the US is likely to enter a recession, and that’s a hard-landing scenario. Thus, the European soft-landing is likely only a temporary state before the hard-landing as well.

The European soft-landing

Here are some key data-points with respect to the EU soft-landing.

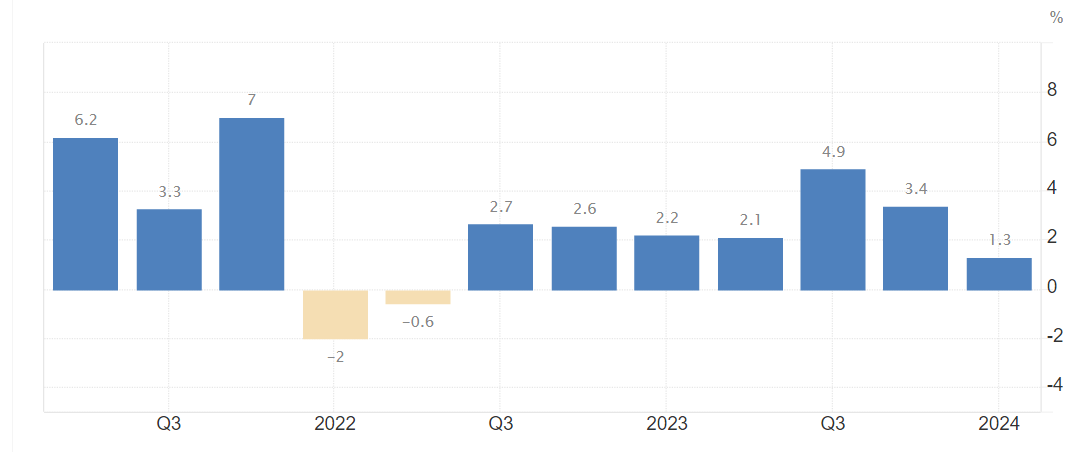

The EU economy is exiting a mild technical recession – the EU GDP had negative growth in Q3 and Q4 of 2023 at -0.2%. However, the EU economy rebounded in Q1 2024, growing at 1.3%, and that’s positive.

EU GDP (Trading Economics)

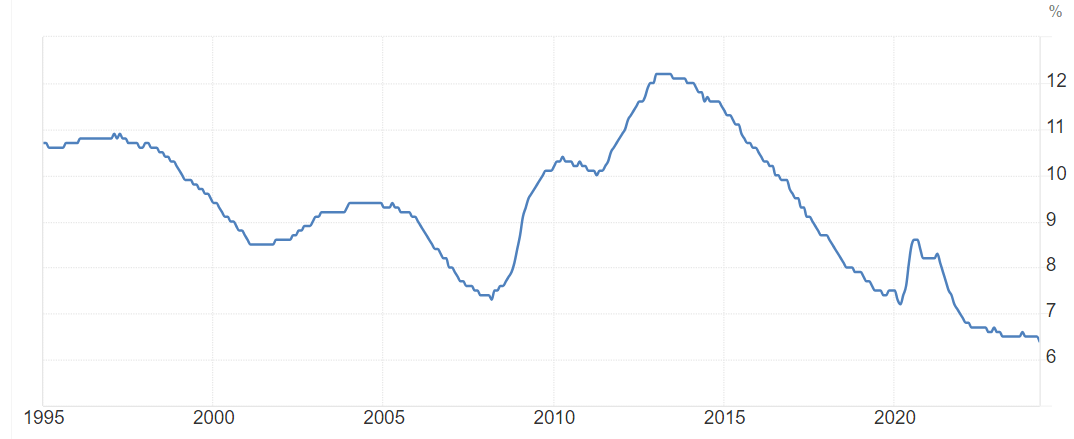

The late 2023 EU recession was only a technical recession because the EU unemployment rate remained at 6.4% – there was no spike in the unemployment rate, which is what happens in “real” recessions. This is also positive – it verifies the soft-landing.

EU unemployment rate (Trading Economics)

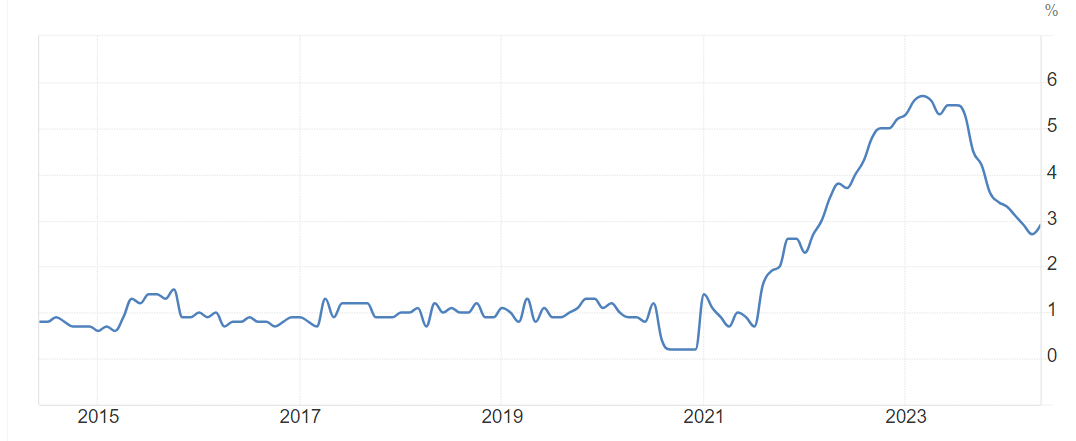

The EU headline inflation fell back from the pandemic highs of above 10% to just above the 2% level and remained fairly stable. This is positive, as the EU has suffered from low inflation and deflation pre-pandemic.

EU inflation (Trading Economics)

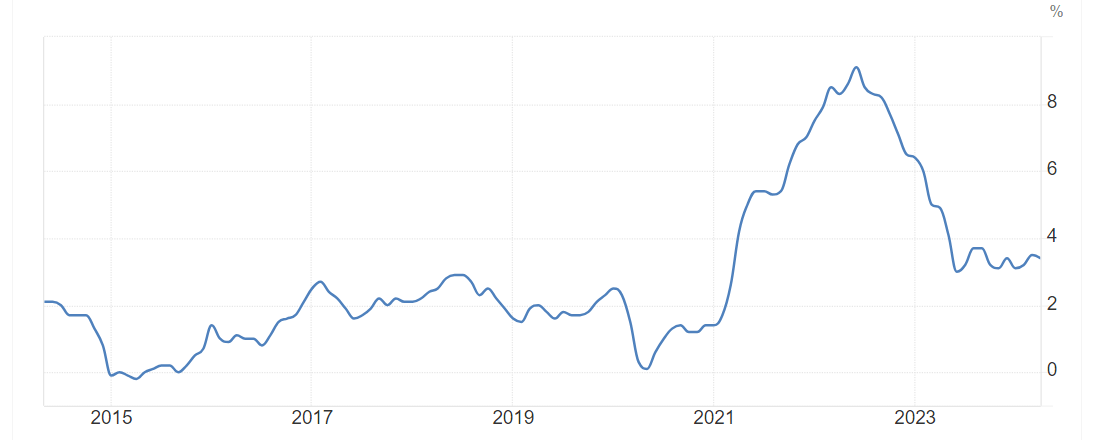

However, the EU core CPI inflation is still elevated, at just below the 3% level, and this is potentially too high to start normalizing interest rates. The EU inflation is more sensitive to energy and food prices, so the fall in the headline inflation is a reflection of falling oil prices. However, the core CPI remains elevated.

EU core CPI (Trading Economics)

The unfolding US stagflation

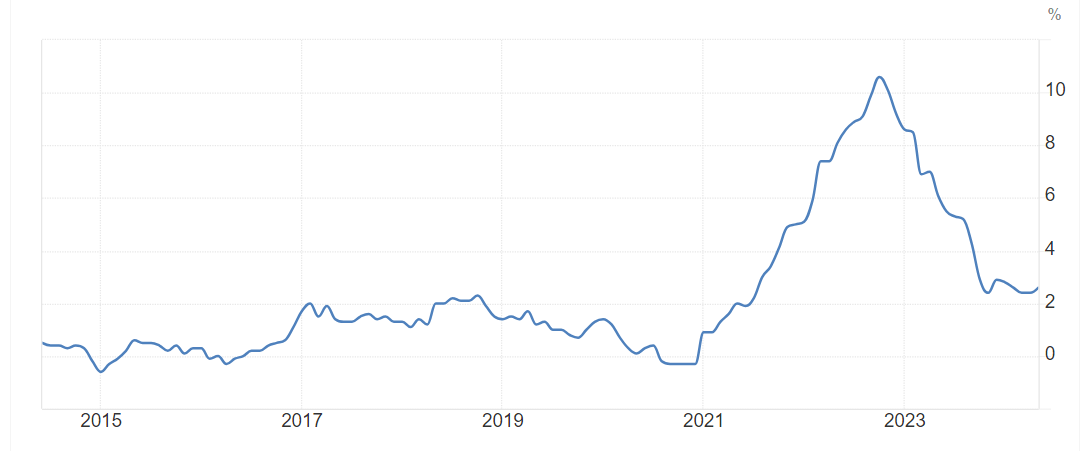

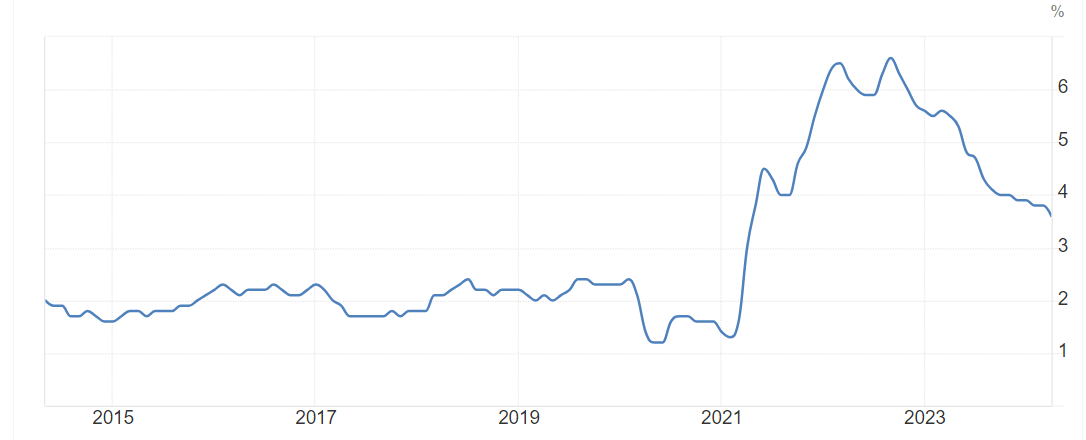

Meantime, in the US, the headline CPI inflation has been sticky at just below the 4% level for many months now. This is almost double the Fed’s 2% target and shows that the disinflationary process in the US has stalled near the 4% level – much higher than in the EU’s inflation level.

US CPI (Trading Economics)

The US core CPI has also stalled just below the 4% level, and the recent disinflationary process has been very slow. The US still has an inflation problem – inflation is still too high for the Fed to start policy normalization.

US core CPI (Trading Economics)

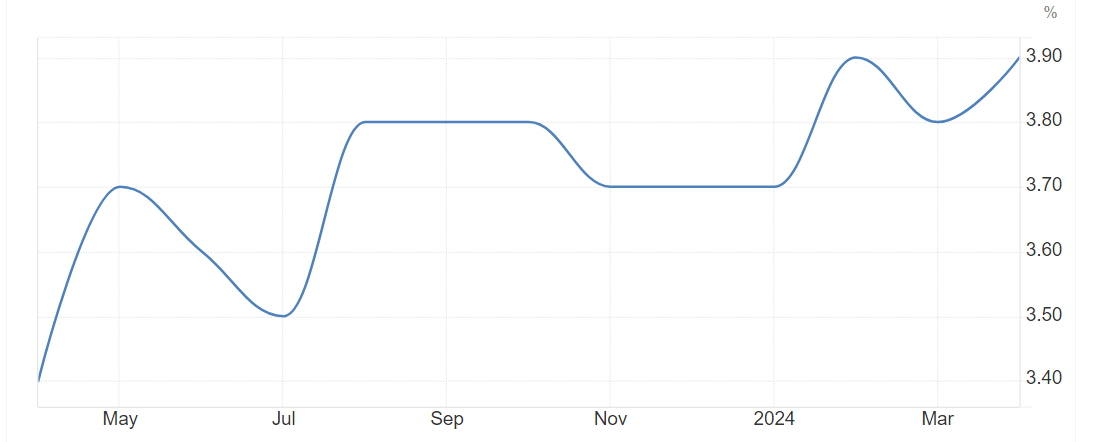

At the same time, the unemployment rate in the US has been rising over the last 12 months from 3.4% to 3.9%, unlike the unemployment rate in the EU, which is higher at 6.4%, but remained steady. Thus, the US is more likely to enter a “real” recession if the trend of rising unemployment rate continues and breaches the 4% level.

US unemployment rate (Trading Economics)

The US economy has significantly slowed in Q1 2024 to 1.3% annual growth rate. While the EU economy was in a recession, the US economy was booming in Q3 and Q4 2023. Now, the US economy is slowing. Based on the recent consumer spending report, the US real consumption decreased by 0.1% in April 2024. Thus, the US GDP is likely to continue to slow in Q2 2024, possibly slipping into negative territory by Q3 2024.

US GDP (Trading Economics)

Is the ECB cut premature?

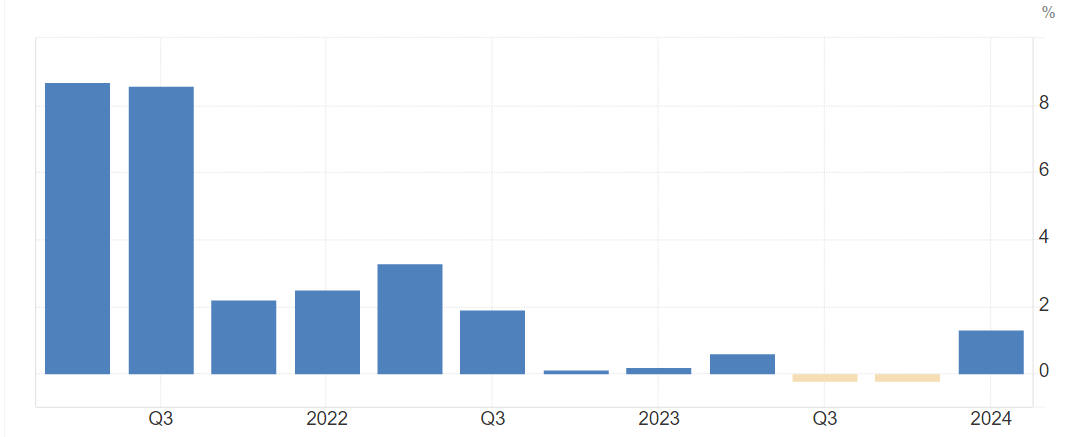

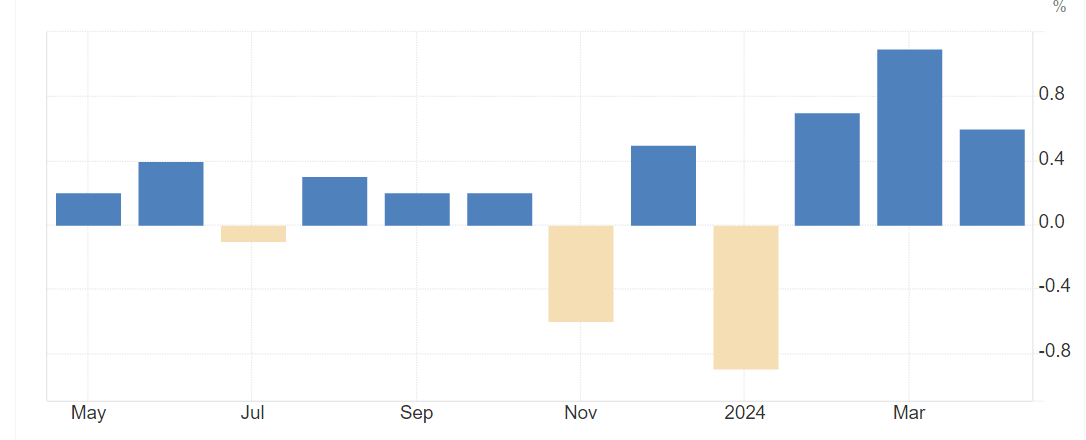

On the surface, the EU is in a soft-landing. However, the recent data shows otherwise. The monthly core CPI reveals that inflation is also accelerating in the EU. Specifically, the disinflationary process in the EU continued due to the base effects, as monthly inflation fell sharply in 2024, with several months of deflation, most notably in November 2023 when monthly inflation fell by 0.9%.

However, the EU monthly core inflation has been very high in Q1 2024, and the inflationary bump from the US is also evident in the EU. Thus, the ECB is potentially prematurely thinking about cutting interest rates. As a result, the ECB might not even cut interest rates next week, as the market expects.

Furthermore, could the ECB really be thinking about cutting interest rates with the escalating geopolitical situation in the Middle East and Ukraine, and crude oil (USO) vulnerable to a sharp spike?

The global economy is facing a stagflationary environment due to the unfolding process of deglobalization, with protectionism, real wars, and cold wars. Thus, global inflation will be prone to shocks, as commodity prices spike and supply chains get disrupted. This is really what the recent spike in price of gold (GLD) signals.

EU MoM core CPI (Trading Economics)

Implications

The S&P 500 (SP500) and the Stoxx 600 (STOXX) are both trading based on sentiment, hoping that the ECB and the Fed will be able to engineer a soft-landing.

The ECB cut next week, if it happens, could be a short-term boost to global stocks as the market gets excited with hopes of a global soft landing – before these hopes get dashed by the hard-landing data on both sides of the Atlantic.

The S&P 500 and the Stoxx 600 are facing a recessionary bear market. The S&P 500 is especially vulnerable to a deep correction due to its excessive PE multiple valuation at 22, and concentrated exposure to the “AI-hyped” megacaps.