champc

With the month of February coming to an finish this week, a majority of 2024 continues to be earlier than us. Because the 12 months started, many strategists predicted as much as six Fed Fund price cuts by the Federal Reserve. The primary reduce was anticipated to happen in March, however financial knowledge and Federal Reserve commentary has pushed the anticipated first price reduce to June. What’s influencing the delay in price cuts is the very fact the economic system is doing higher than many had anticipated, and inflation is somewhat stickier than anticipated.

The Fed’s twin mandate is that of sustaining steady costs and maximizing employment. The steady costs mandate had a setback a number of weeks in the past when inflation was reported larger than anticipated at 3.1%. The Fed’s most popular inflation measure is the Private Consumption Expenditures Value Index (PCE) and will likely be reported Wednesday. The Fed’s goal for Core PCE is 2.0%.

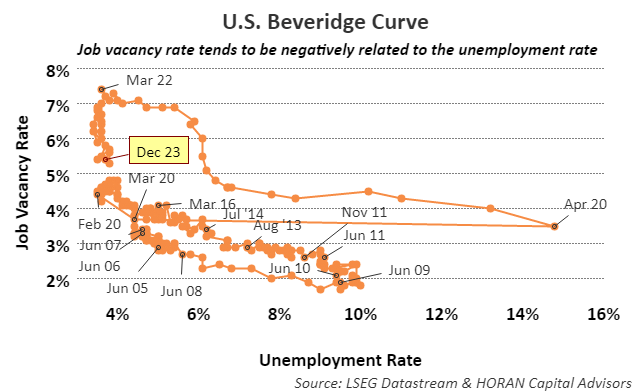

With respect to employment, the unemployment price stays at a low degree of three.7% despite the fast improve in short-term charges that the Fed pursued from 2022 to mid-year 2023. One would anticipate the tighter financial coverage to sluggish financial progress and certain lead to the next unemployment price, which has not occurred. One graphical manner to have a look at that is to guage the unemployment price versus the extent of job openings. A standard measure to do that is named the Beveridge Curve, named after the British economist William Henry Beveridge. When there’s a mismatch between accessible jobs and the unemployment degree, the curve shifts outward and as much as the best. Following the pandemic, this was what unfolded as many service jobs had been misplaced, and better expert know-how jobs grew as companies had been closed. Nevertheless, if one seems to be from April 2020 to March 2022, employment recovered. Then from March 2022 when the Fed started growing rates of interest, the Fed had the good thing about a excessive degree of job vacancies and job vacancies declined whereas the unemployment degree remained regular. So, as a substitute of firms decreasing employment, vacancies declined partly attributable to the next employment degree, however partly attributable to a discount in job openings.

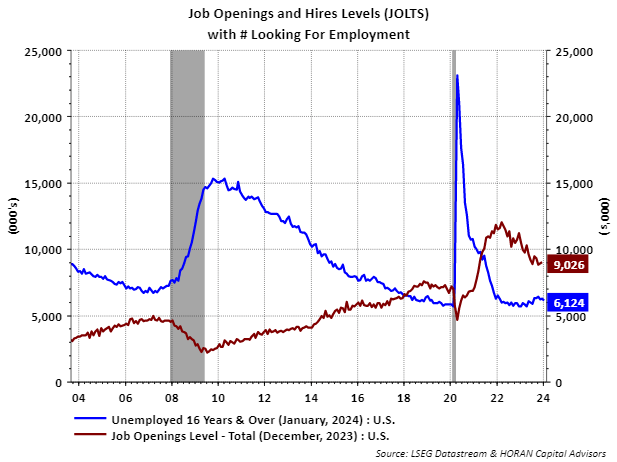

One other technique to see that is to have a look at the job openings versus the variety of people unemployed. Because the under chart exhibits, the variety of open positions has declined since early 2023, whereas the variety of people unemployed stays close to the extent reached pre-pandemic.

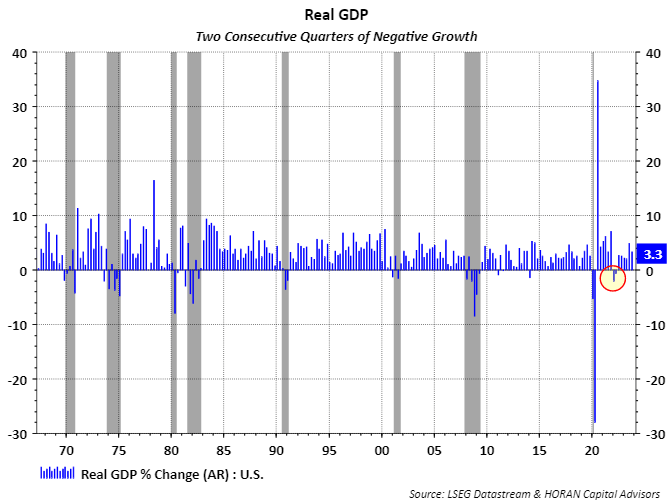

At HORAN, we wrote in a number of of our quarterly investor letters in late 2022 and early 2023 that the U.S. economic system did expertise a recession in early 2022 when actual GDP was destructive for 2 consecutive quarters. NBER establishes the beginning and finish of recession intervals, and so they have a extra nuanced recession definition. Nonetheless, two consecutive quarters of destructive GDP is usually understood to suggest a recession. Because the under chart exhibits, going again to the late Sixties, anytime two consecutive quarters of destructive GDP progress was skilled, a recession was famous by NBER (gray shading.)

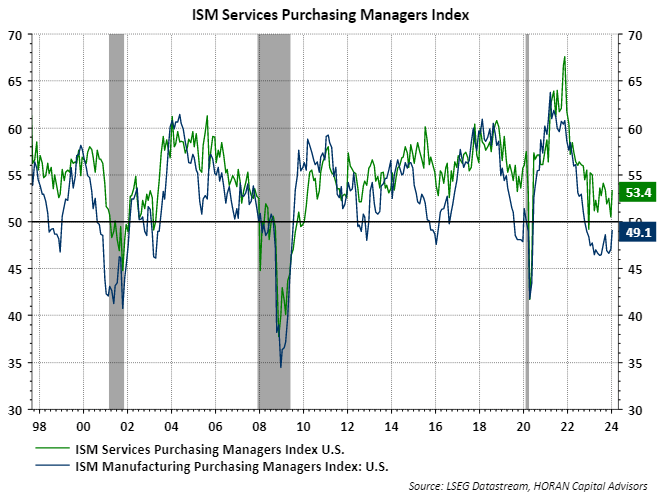

The Institute for Provide Administration (ISM) conducts month-to-month surveys for the manufacturing and repair sectors of the economic system. The companies industries characterize greater than 70% of GDP, and a studying above 50% signifies a service sector that’s increasing. Because the under chart exhibits, the ISM Providers Buying Managers’ Index (PMI) got here in at 53.4% in December. The ISM Manufacturing PMI was reported at 49.1%, a contractionary degree. Nevertheless, ISM notes, “a Manufacturing PMI® above 42.5%, over a period of time, generally indicates an expansion of the overall economy.”

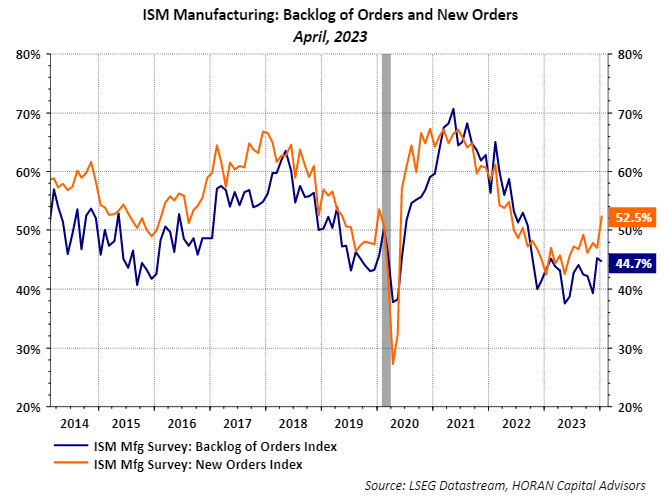

Lastly, the place backlogs had been important following the pandemic, the blue line on the under chart exhibits a lot of the backlog has been decreased to a extra regular degree as provide chain points have resolved. Additionally, new orders have been trending larger for many of 2023.

So, with all of the discuss a recession, each onerous and gentle knowledge suggests an financial setting that’s rising at a tempo that’s not too quick. The unemployment price stays at a low 3.7%, jobless claims reported final week equaled 201,000 which was decrease than the estimate of 218,000. From an earnings perspective, fourth-quarter earnings season is nearly full. A complete of 448 firms within the S&P 500 Index have reported earnings up to now. The year-over-year earnings progress price is predicted to equal 10% for This fall 2023. On the finish of 2023, the This fall earnings progress estimate was solely 5.2% and all of 2024 earnings progress is predicted to equal close to a double-digit price at 9.5%. Actually, there are potential headwinds that may be cited: an inverted yield curve, a steeply destructive Main Financial Indicators Index and extra, however extra of the information appears supportive of a gentle touchdown, if not already landed.

Editor’s Notice: The abstract bullets for this text had been chosen by Searching for Alpha editors.