George Pachantouris/Second through Getty Photos

Generally, it may be troublesome to put an organization. Some are simply clearly enticing, whereas others are clearly unattractive. However from time to time, there are companies that sit someplace within the center. One firm that I may level to the place this was the case, at the least for me, is The First of Lengthy Island Company (NASDAQ:FLIC). On the one hand, shares are extremely low cost relative to ebook worth. However alternatively, there are different methods by which the enterprise is unremarkable. It additionally has a excessive uninsured deposit publicity and up to date monetary efficiency has been something however nice. When confronted with a blended alternative like this, the most effective factor I can do is to be cautious and err on the conservative facet. And on this occasion, that leads me to price the enterprise a ‘maintain’.

A financial institution I am going to cross on

In keeping with the administration crew at First of Lengthy Island, the establishment dates again to its founding in 1927. Since its humble beginnings, it has grown right into a multifaceted enterprise with 41 department areas largely centered across the Nassau and Suffolk Counties of Lengthy Island, and in addition all through the 5 boroughs of New York Metropolis. Identical to most any regional financial institution, the enterprise provides clients a wide selection of providers. Examples of the merchandise provided embrace deposit accounts, loans for small and medium sized companies, house fairness traces of credit score, residential mortgage loans, building and land growth loans, shopper loans, and extra. The financial institution additionally has different providers that it provides akin to funding administration providers, belief providers, property and custody providers, and extra.

Creator – SEC EDGAR Knowledge

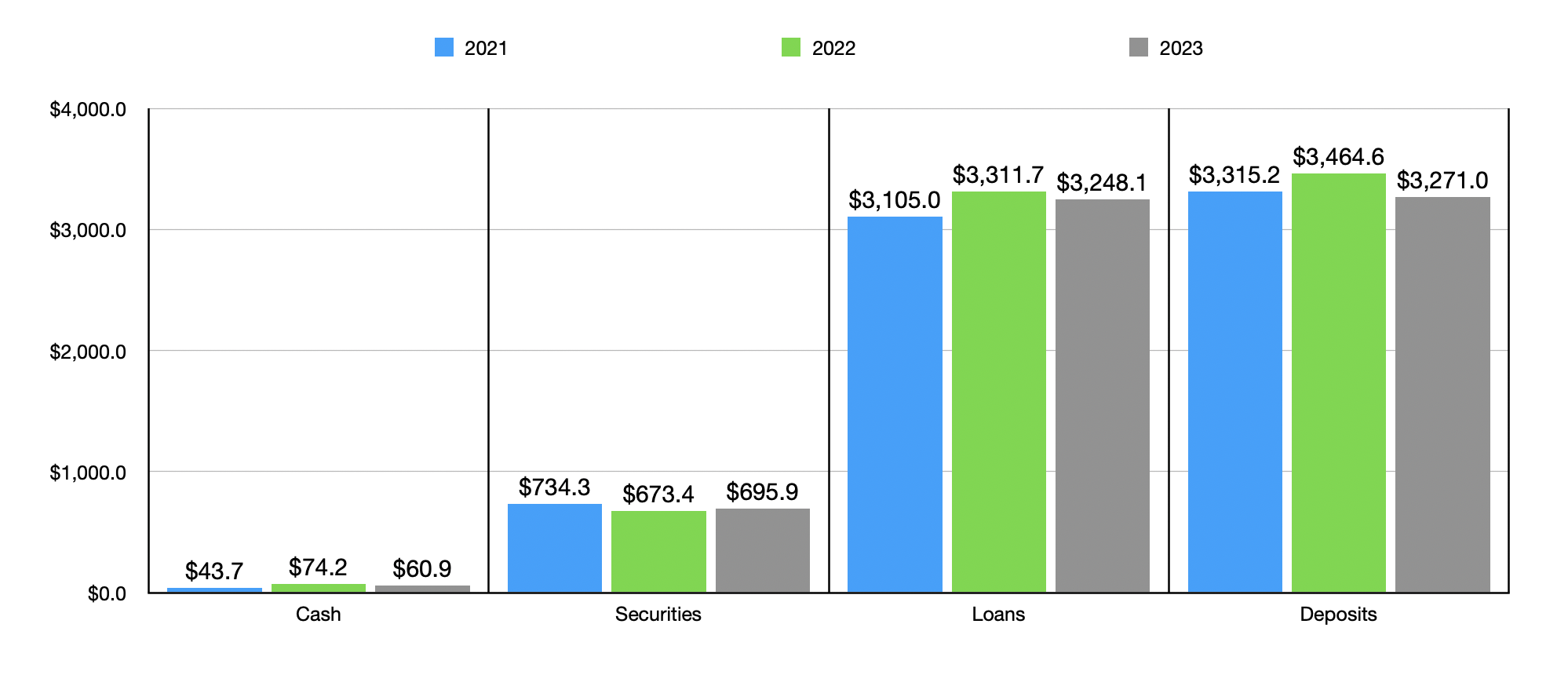

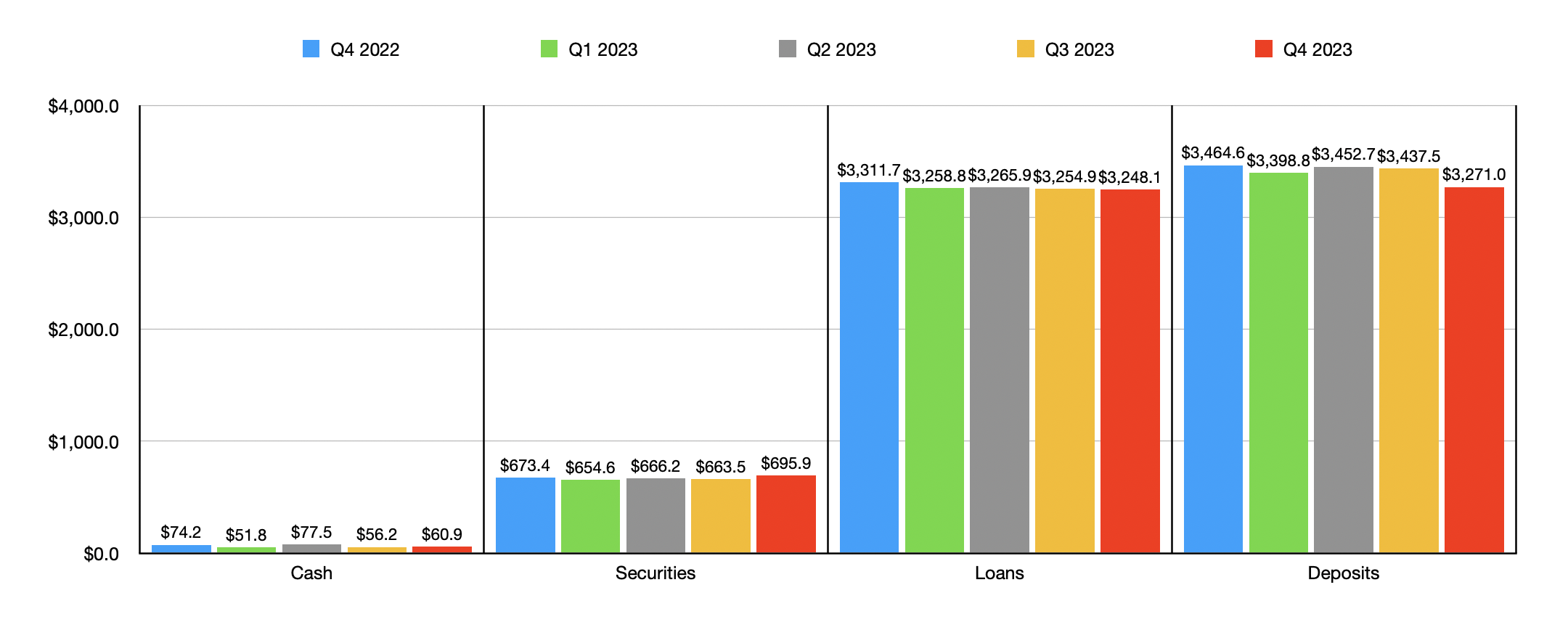

Current monetary efficiency achieved by the financial institution has been blended and, in some respects, disappointing. Take into account, for example, the worth of deposits on its books. Deposits grew from $3.32 billion in 2021 to $3.46 billion in 2022. After seeing a small decline in deposits within the first quarter of 2023, there was a rebound within the second quarter. However that was brief lived. By the top of 2023, deposits had declined to $3.27 billion. The excellent news is that uninsured deposit publicity had fallen from 58% on the finish of 2022 to 38% at the moment. However that is nonetheless above the 30% threshold that I set as a most for what I usually choose on this area.

Creator – SEC EDGAR Knowledge

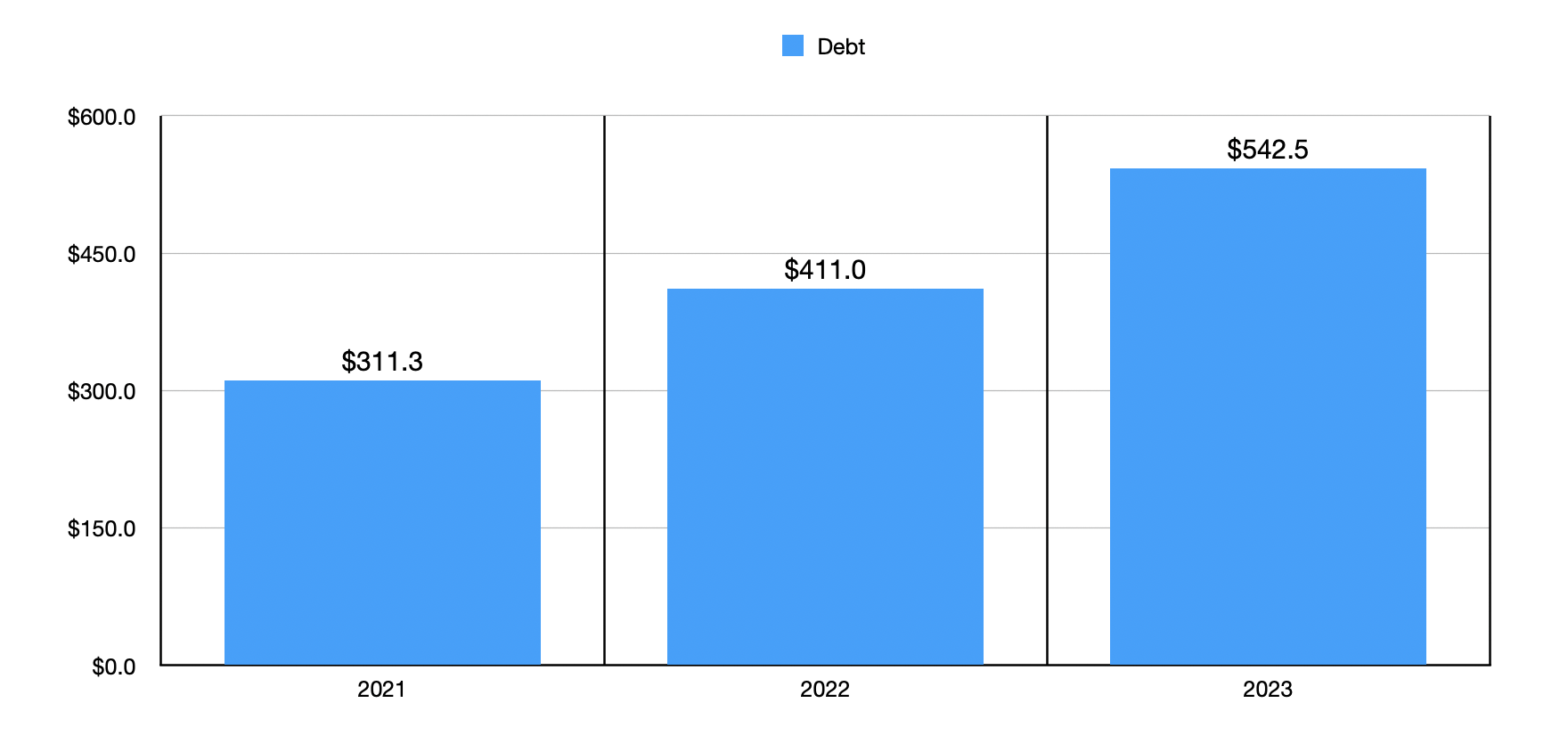

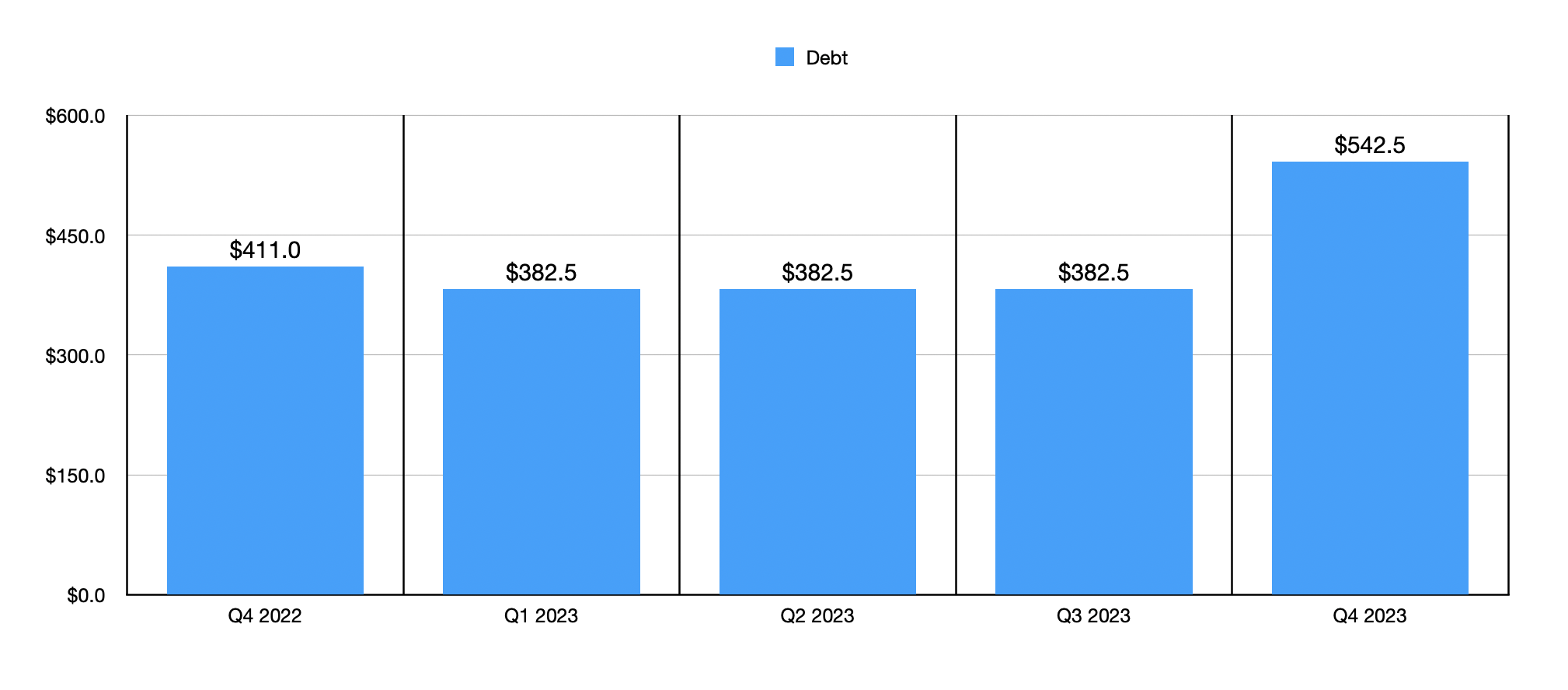

On the mortgage facet, the image has adopted the same trajectory. After rising from $3.11 billion in 2021 to $3.31 billion in 2022, loans dropped to $3.25 billion in 2023. There have been different methods by which the establishment has proven blended outcomes. The worth of securities on its books, for example, did rise from $673.4 million in 2022 to $695.9 million in 2023. That is a optimistic. However that is nonetheless down from the $734.3 million that the financial institution had in 2021. The worth of money has remained in a reasonably slender vary, significantly over the previous few quarters. However debt has really elevated. Again in 2021, it got here in at $311.3 million. By the top of 2023, it had grown to $542.5 million. And the overwhelming majority of that improve from 2021 occurred from the third quarter of final yr to the ultimate quarter.

Creator – SEC EDGAR Knowledge Creator – SEC EDGAR Knowledge

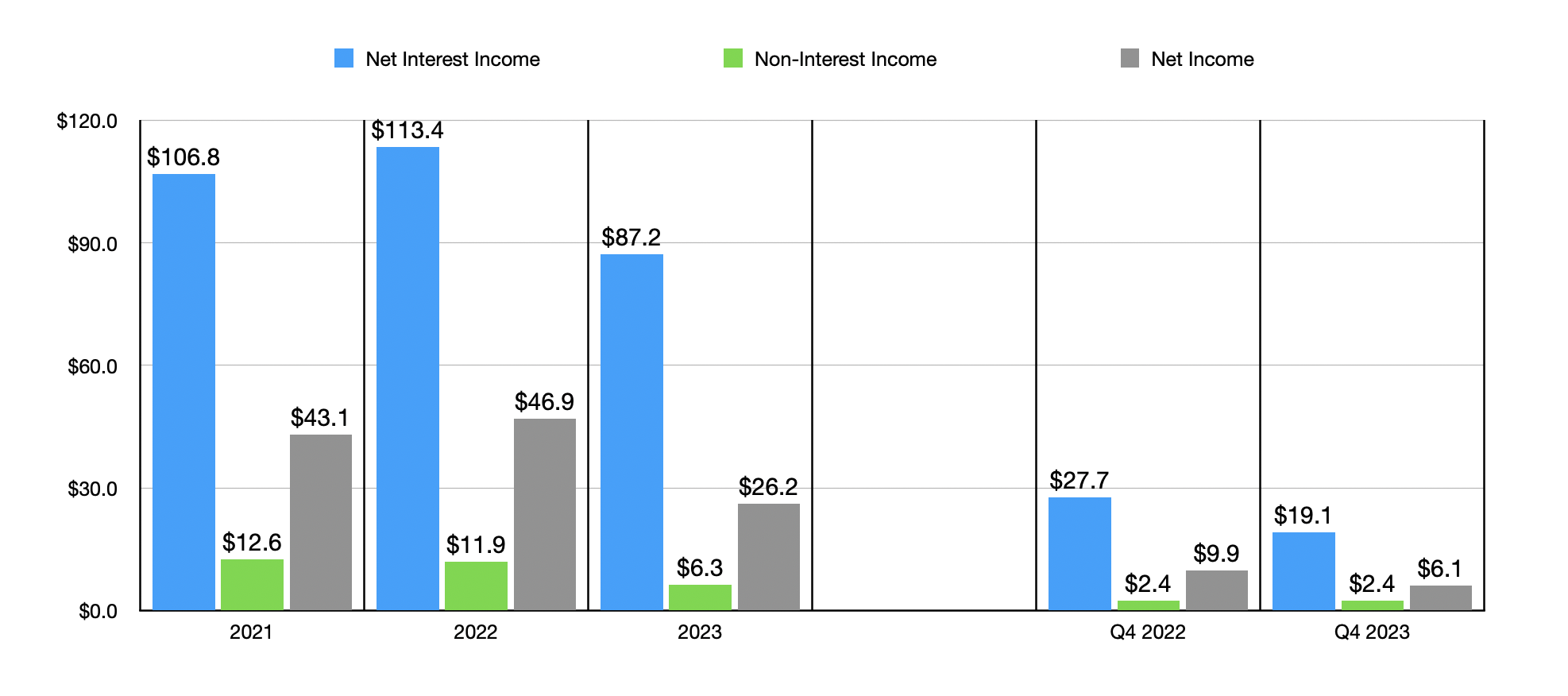

This ache on the stability sheet has confirmed instrumental in impacting the revenue assertion for the financial institution. After seeing web curiosity revenue rise from $106.8 million in 2021 to $113.4 million in 2022, it plunged to $87.2 million final yr. That drop was pushed partly by a decline within the worth of loans and better curiosity funds wanted to be paid out to depositors with a view to maintain their funds throughout the financial institution. The rise in debt additionally has confirmed to be an issue right here, particularly when you think about the function that increased rates of interest cannot play on the image. Because the chart beneath illustrates, different profitability metrics for the financial institution haven’t fared significantly nicely. Non-interest revenue declined by practically half from $11.9 million in 2022 to $6.3 million in 2023. And web income plunged from $46.9 million to $26.2 million.

Creator – SEC EDGAR Knowledge

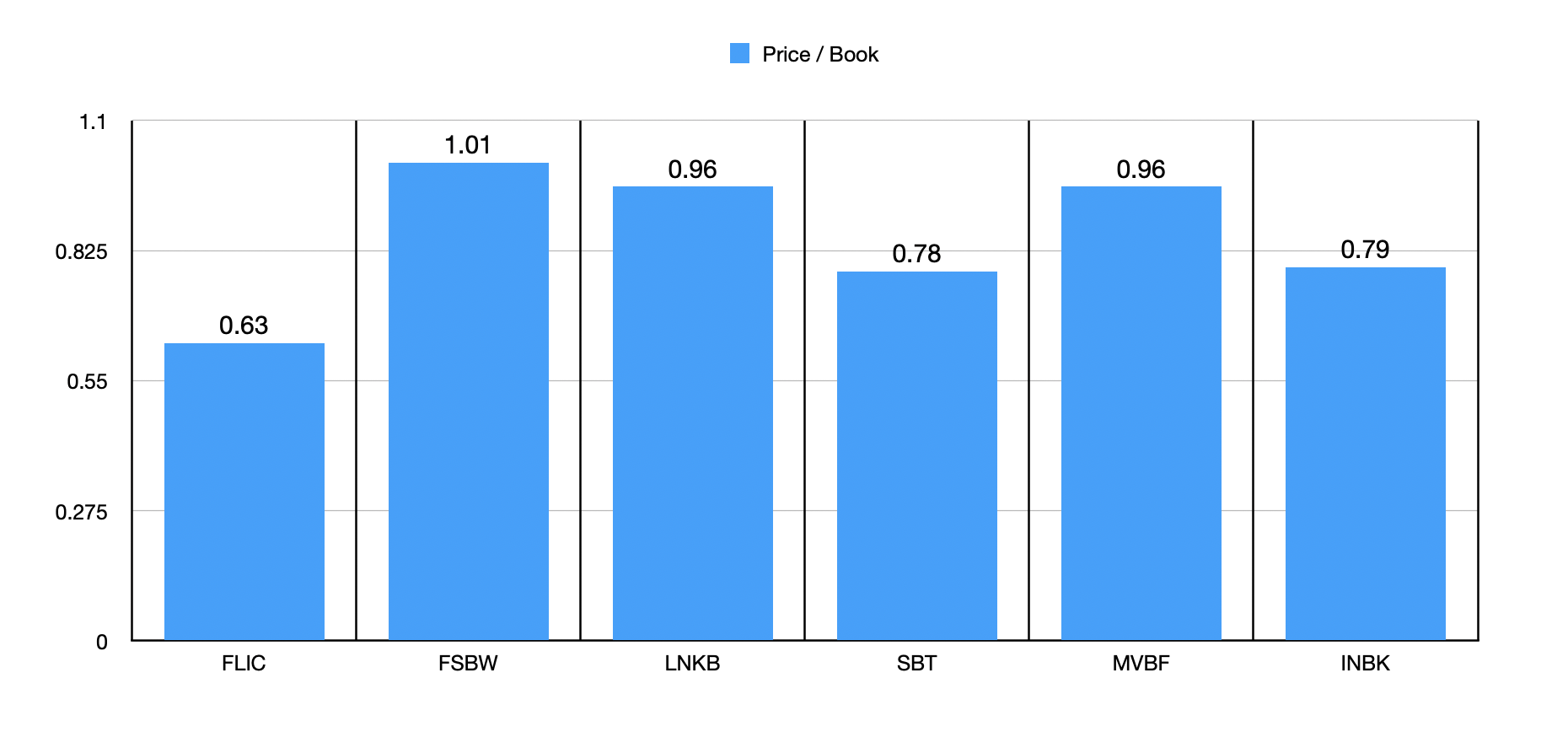

Nearly with out exception, the information that we have now coated up up to now has been disappointing. However the upside to that is that the worth to ebook a number of of the financial institution is kind of low. Sadly, the ebook worth per share has jumped all over, with no clear pattern over the previous a number of quarters. That’s seemingly factoring into the general worth to ebook a number of of 0.63, as can be the opposite weak spots for the establishment. In actual fact, as a part of my evaluation, I in contrast First of Lengthy Island to 5 related companies. As you may see within the chart beneath, it has the bottom worth to ebook a number of right now. Conserving all else the identical, this is usually a web optimistic as a result of it may point out vital upside potential. However once we begin wanting on the image in different methods, issues begin to look lower than superb.

Creator – SEC EDGAR Knowledge

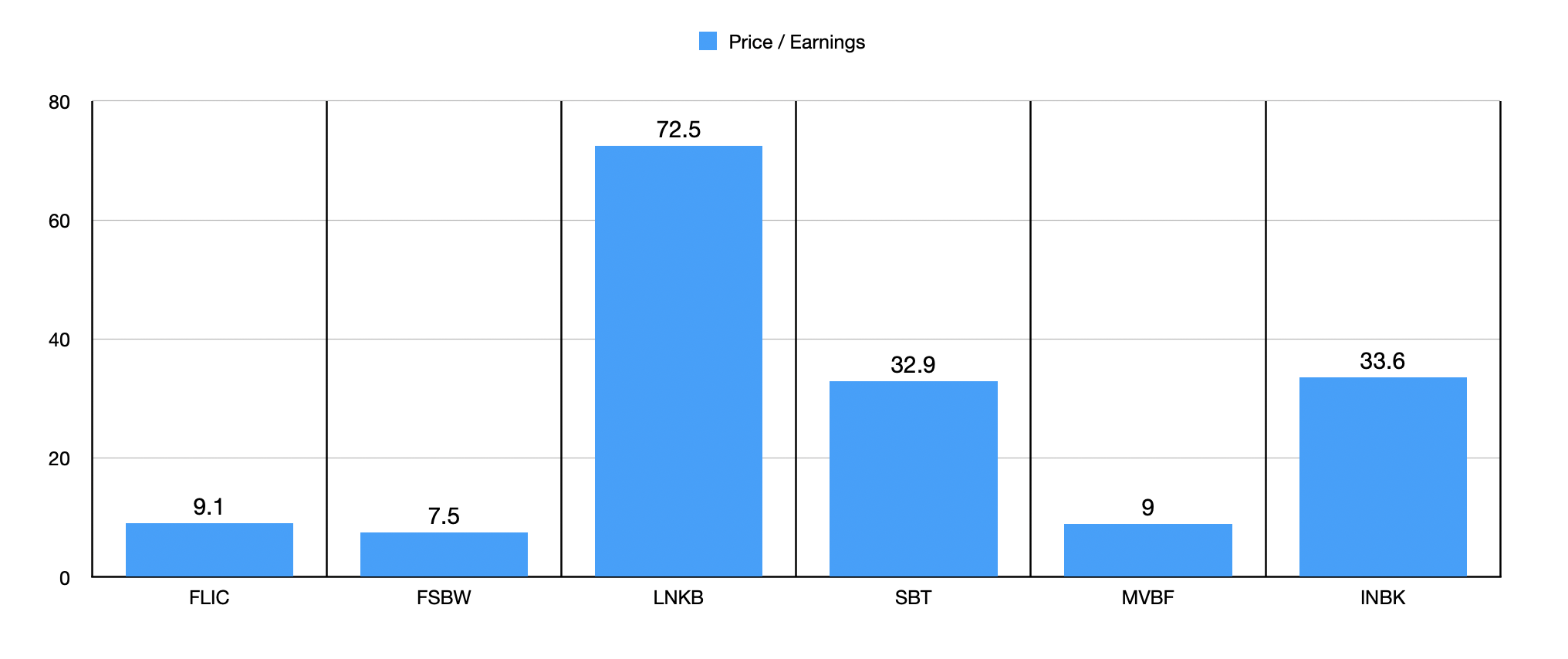

Within the subsequent chart, you may see the worth to earnings a number of, not just for First of Lengthy Island, but additionally for these identical 5 corporations as earlier than. With a studying of 9.1, the establishment is principally on the excessive finish of what I usually choose. There are some banks that also commerce at ranges of between 6 and 9 and that is the place I really feel most snug. Because the aforementioned chart illustrates, solely two of the 5 corporations that I in contrast it to have worth to earnings multiples decrease than what it does. In order that locations it across the center of the pack.

Creator – SEC EDGAR Knowledge

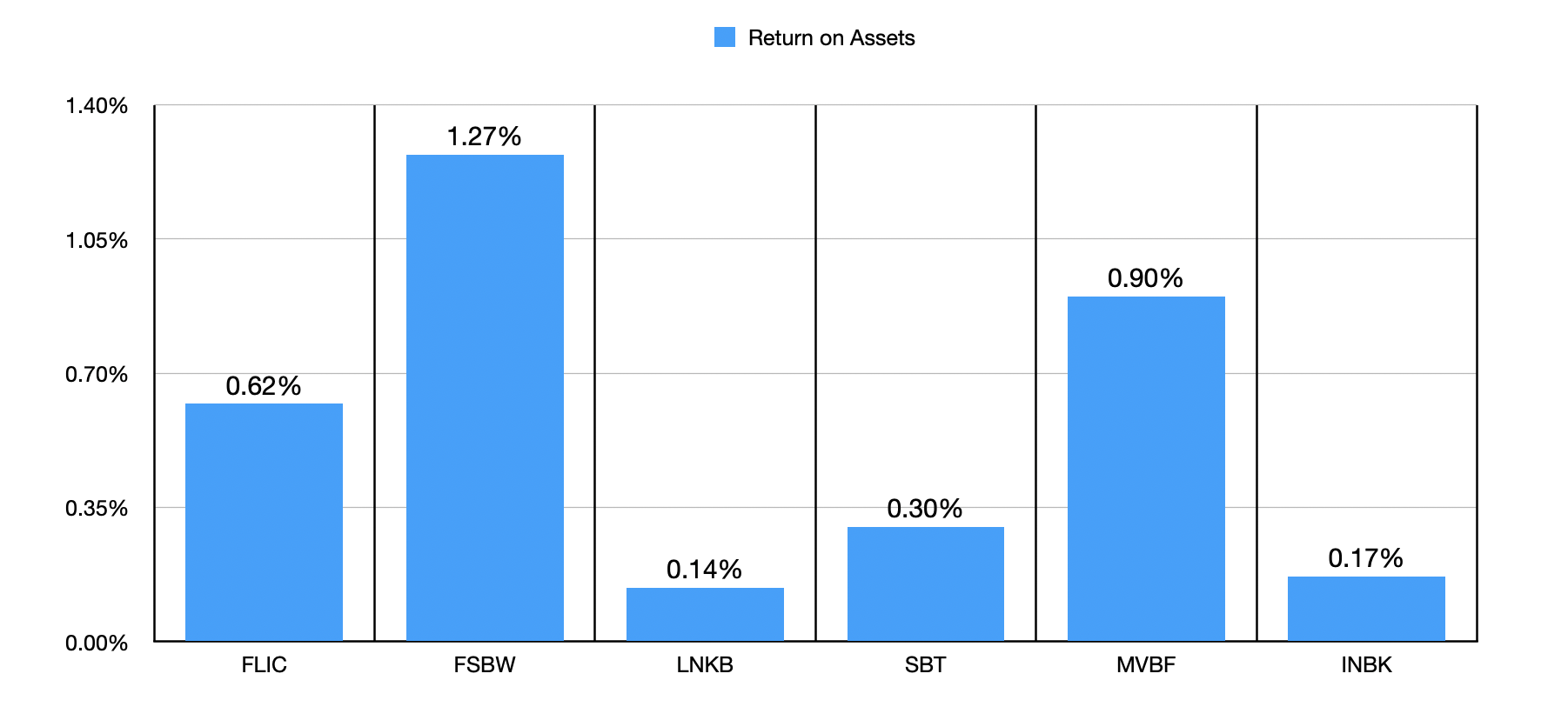

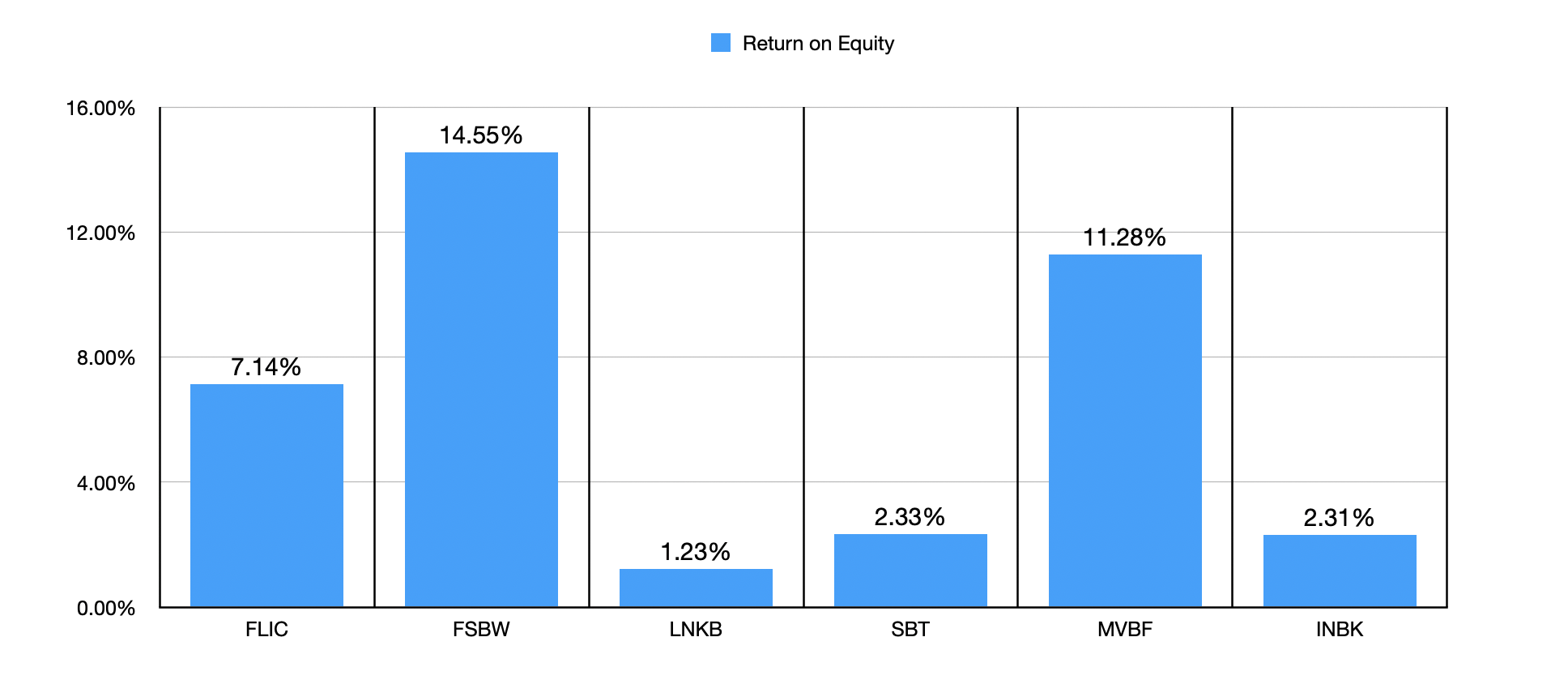

In fact, generally establishments should commerce the place they do. And one factor that we will take a look at to see whether or not or not that is the case can be its return relative to different measures. Return on property, for example, are significantly low for the financial institution at solely 0.62%. As the primary chart beneath illustrates, this isn’t the bottom of the group by any means. However I’ve seen a number of establishments with readings of 1% or increased. There’s additionally the subject of return on fairness. And as soon as once more, First of Lengthy Island appears to be across the center of the pack on this entrance.

Creator – SEC EDGAR Knowledge Creator – SEC EDGAR Knowledge

Takeaway

Operationally talking, First of Lengthy Island is pretty unremarkable. What I do like concerning the financial institution is that shares are very low cost relative to ebook worth. And relative to the opposite companies that I in contrast it to, sure metrics place it in the course of the pack or thereabouts. However while you begin different elements, it turns into fairly clear that the image is problematic. Regardless of how low cost the inventory is, the massive variety of points like declining deposits, excessive uninsured deposit publicity, declining mortgage values, and a drop in income and income, leads me to consider {that a} ‘maintain’ score solely is sensible at this time limit.