mikkelwilliam

Co-Authored with Whole Return Investor

Revisiting Julia 2023

The idea of an All-Climate Portfolio – a portfolio that may carry out satisfactorily in any market circumstances, with none want for getting or promoting – will not be a brand new one. The “60/40” portfolio – 60% shares, 40% bonds – is an concept that’s been round since at least the center of the final century. In line with the 60/40 principle, the costs of shares and bonds are inclined to differ inversely, with one going up when the opposite goes down, so a portfolio balanced between the 2 ought to keep a extra even keel over time than pure inventory or bond portfolios. Very broadly, the historic information bears out the 60/40 view. (For statistical particulars, please see our unique article, The Search for an All-Weather Portfolio.)

After all, if conserving a fair keel is the goal, the plain and rapid query is, does the 60/40 portfolio do the absolute best job of it? Placing 60% of 1’s capital in a broad inventory market fund, 40% in a broad bond market fund, and anticipating optimum efficiency, appears nearly too simple (though Vanguard’s extremely revered Vanguard Balanced Index Fund Inst (VBIAX), which implements the 60/40 technique by merely following two broad-market indices, continues to be a good competitor). And certainly, as will be seen on the web sites PortfolioCharts.com, LazyPortfolioETF.com, and OptimizedPortfolio.com, dozens of proposals have been made for higher AWPs than the 60/40. In our previous article, we arrange a uniform framework for evaluating these AWPs, evaluated a number of the most well-known of them, and provided a statistically superior various of our personal, “Julia.”

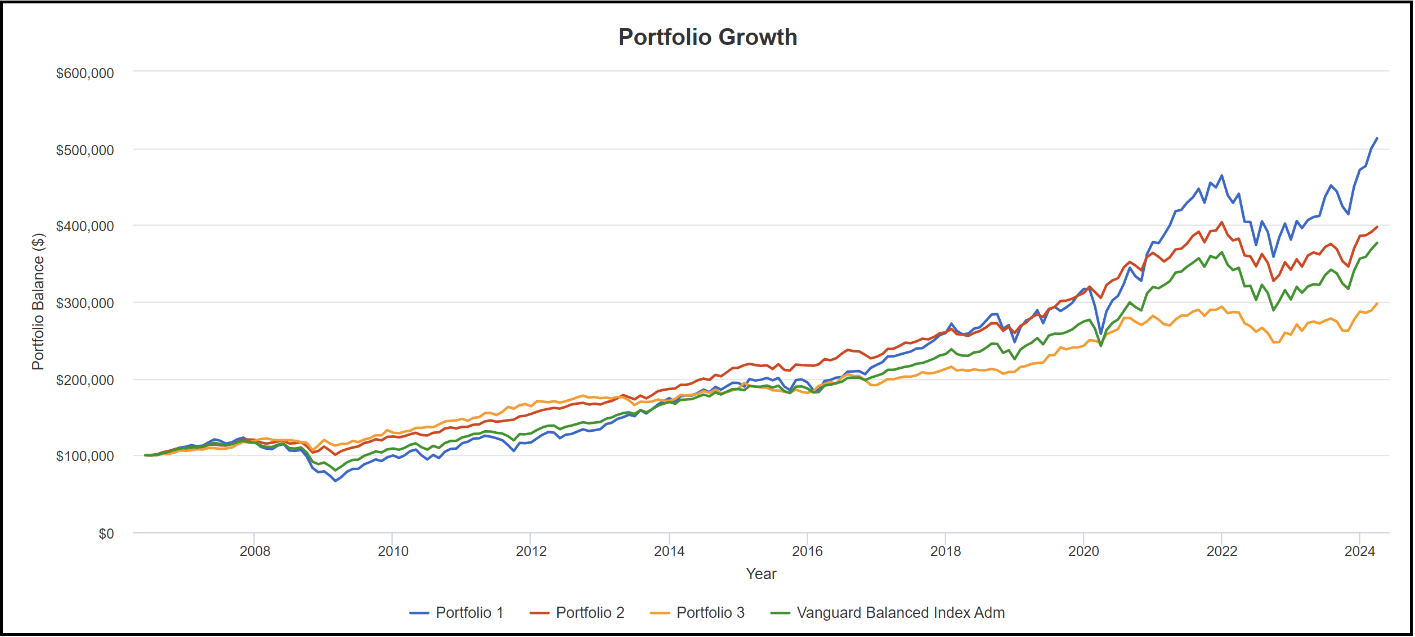

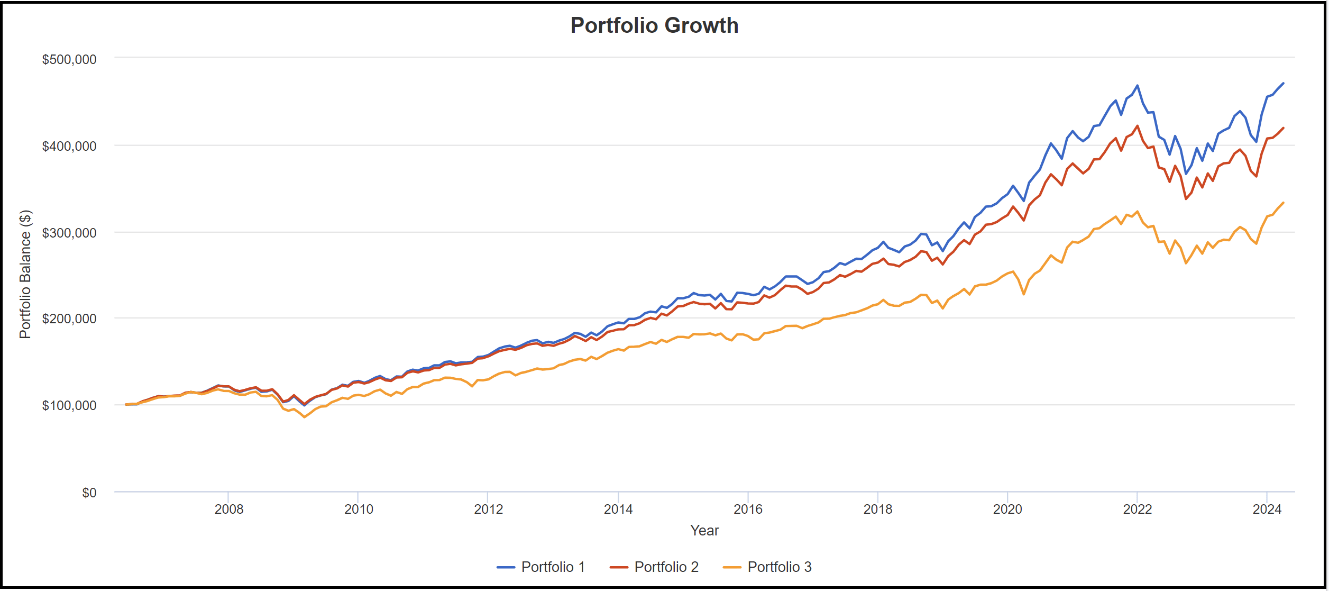

Right here’s a chart which provides the flavour of the outcomes from our earlier article. It employs Portfolio Visualizer.com, an impressive web site (free for the fundamental model) which gives instruments for portfolio analysis in addition to a variety of different monetary metrics.

Portfolio Visualizer

It’s value taking a couple of minutes to grasp the outcomes right here. Portfolio 1, the blue line, is what we name “Buffett’s Widow”, primarily based on Warren Buffett’s onetime comment that if he have been recommending a portfolio for his spouse within the occasion of his loss of life, it could be 90% a broad market index fund (we’ve used Vanguard Whole Inventory Market Index Fund ETF Shares (VTI)) and 10% a short-term treasury invoice fund (we’ve used SHY, the iShares 1-3 yr Treasury bond index.) Portfolio 2, the pink line, is Julia as we offered it in our unique article, which we’ll focus on slightly additional under. The inexperienced line is the basic 60/40 portfolio as represented by Vanguard’s VBIAX fund; and Portfolio 3 is the “Permanent Portfolio” propounded by Harry Browne (Libertarian candidate for President, 1996 and 2000.) Our unique article analyzed a number of different AWPs, such because the Ray Dalio portfolio as popularized by Tony Robbins, however Portfolio Visualizer solely permits comparability of three portfolios at a time plus an index, so that you’ll should seek the advice of our prior article for additional info.

It is useful to contemplate the statistical evaluation of this graph as offered by Portfolio Visualizer, for our take a look at interval of June 2006 to the current. (We begin in June 2006 as a result of that’s the inception date of considered one of Julia’s core elements – VIG, the Vanguard Dividend Appreciation index, and consists of the vital stress take a look at of the World Monetary Disaster of 2007-9):

|

Portfolio |

Initiated 6/2006 |

CAGR |

Steadiness 3/2024 |

30 Yr Projection |

Most Drawdn |

Sharpe Ratio |

|

1-Buffett’s Widow |

100,000 |

9.60% |

512,878 |

1,564,288 |

-45.95% |

0.62 |

|

2-Julia |

100,000 |

8.37% |

397,458 |

1,114,993 |

-18.95% |

0.87 |

|

3-Browne |

100,000 |

6.39% |

297,813 |

641,245 |

-15.85% |

0.70 |

|

Vanguard 60/40 |

100,000 |

7.72% |

376,738 |

930,873 |

-32.45% |

0.66 |

Portfolio Visualizer and Authors’ Projection

Contemplate what these statistics present. Sure, Portfolio 1 (“Buffett’s Widow”) has the superior Compound Common Progress Fee (CAGR), showing as the highest line on the graph, however on the value of a horrendous 45.95% drawdown in the course of the take a look at interval (word the pandemic yr 2020.) Additionally word how lengthy Portfolio 1 lagged the others, particularly Julia, within the aftermath of the World Monetary Disaster. (This could most likely be of little concern to Mrs. Buffett, however take into account the impact on a retiree of modest means getting down to comply with the 4% withdrawal rule.) Sure, Portfolio 3 (Browne’s “Permanent Portfolio”) has a most drawdown of solely 17.20%, however on the expense of a CAGR of solely 6.39%, with a last stability of solely $297,813 over the take a look at interval, the worst of all of the AWPs within the group. (The impact of compounding turns into significantly stark when projected out to 30 years.) The 60/40 portfolio comes out someplace within the center. However the Sharpe ratio – the ratio of development to draw back danger – comes out massively in Julia’s favor. This one abstract desk can’t inform the entire story, however as of final yr’s publication, we consider it was indicative of a considerable benefit in favor of the way in which Julia is constructed.

And the way was Julia constructed? As we defined in our previous article, the essential distinction from the normal 60/40 was to interrupt the inventory part down into three components:

|

Regular Earnings and Earnings Progress |

(VIG) Vanguard Dividend Appreciation Index |

16% |

|

Dynamic Progress and Innovation |

(QQQ) Invesco Nasdaq 100 |

16% |

|

Steady, Defensive Sluggish Progress |

(XLP) Shopper Staples Sector SPDR (XLV) Well being Care Sector SPDR (XLU) Utilities Sector SPDR |

6% 6% 6% |

|

50% |

||

The online results of this division was to enhance the efficiency of Julia’s inventory part by nearly 1% over pure VTI. As proven within the desk above, even a tiny share distinction in CAGR can produce dramatic variations in web outcome, when compounded over a interval of two or three a long time.

The remainder of Julia, as we offered it final yr, was designed much less systematically, as a result of it was TRI’s precise working portfolio on the time, and shows all of the quirks that distinguish actual portfolios from idealized digital creations. Right here is TRI’s private account of how Julia grew to become his private portfolio:

After a busy 2020 COVID yr of shopping for and promoting (each particular person corporations and funds), at age 74 I realized that I used to be not getting any youthful or smarter, and that my spouse had neither the data nor inclination to handle such a portfolio. So, in late 2020 I reversed course. Consolidating the winners and abandoning the losers, I ended 2020 with an 11.3% achieve, allotted as follows: 25% in a single whole US market inventory fund, 40% in a single combination bond fund, 20% in a brief time period Treasury fund, and 15% in financial institution CDs and brokerage money. It was not a foul place to catch my breath, however was clearly too conservative to be a everlasting answer. By the spring of 2021, the hunt was on for one thing higher.

I grew to become fascinated with Ray Dalio’s well-publicized AWP (see our unique article for its particulars), and regularly started assembling it. Initially issues went properly, however as 2021 wore on, I suspected that there have been considerably higher AWP potentialities. That fall, oriented extra to Portfolio Adviser evaluations, I exited Dalio’s beneficial DBC broad commodities at a really good revenue, exited GLD at a wash, and in the reduction of considerably on my march in direction of Dalio’s advice for 40% in long run Treasuries (thank goodness!)

Originally of 2022, I was holding roughly equal 22% parts of long run Treasuries and combination bonds, a 6% dollop of inflation protected Treasuries in a nod to inflation (which was clearly heating up), and 42% in shares, largely in a broad market inventory fund. The remaining 8% was equally divided between brief time period Treasuries and money. Over the course of 2022, the broad inventory fund was regularly allotted to extra centered alternate options, as we detailed in final yr’s article. By early 2023, Julia as described in final yr’s article was basically in place.

Whereas Julia 2023 was a major enchancment upon the “usual suspects” within the AWP lineup, we consider that it will possibly nonetheless be improved. We start with an vital distinction that usually lurks within the background of portfolio evaluation, however is seldom if ever clearly drawn.

The Distinction Between Working and Reserve Belongings

We now draw a basic distinction between an individual’s Working and Reserve belongings. (Monetary belongings; actual property is past the scope of this dialogue.) Working belongings, as we now consider them, are invested with the aim of incomes a major favorable return, relative to inflation. Reserve belongings are centered on the preservation and utilization of wealth. For example, a checking account stability (and a few folks want to maintain a big one) is a Reserve asset. It’s usually not meant to generate a critical return; it’s meant to pay upcoming payments and ongoing bills. Many monetary advisors counsel sufficient prepared money to maintain a household for six months to a yr in case of sudden emergencies; once more, the purpose is to have a very liquid reserve, to not maximize return on funding. Easy “walking-around money” can be a reserve. Conceptually, reserve belongings must be utterly segregated, mentally if not bodily, from working belongings which might be meant to supply a optimistic return.

However precisely the place is the dividing line between Working and Reserve belongings? Properly, cash in a single’s pockets or below the mattress (a minimum of in a very safe and inflation-free world) would most likely be the clearest instance of a reserve asset: “pure cash,” authorized tender. SHY, the one-to-three yr Treasury invoice ETF (at the moment yielding round 3.2% in an setting the place the final reported CPI was… 3.2%), can on uncommon events provide a optimistic return (although not in the long term.) BIL, the one-to-three month Treasury invoice ETF, at the moment yields slightly greater than 5%, however that yield will come down rapidly assuming the Fed begins to chop the fed funds price. The place to attract the road?

Properly, there is no vivid line to attract. Bond funds are available all durations. Whereas it’s categorized as a bond fund, SHY is a well known, highly-liquid, short-duration instrument broadly considered “parking place” for money – as a result of it behaves rather more like money than longer period bonds that supply the potential for a minimum of some actual return. With out additional ado, or any pretense of deep data of the bond market, we arbitrarily set the inflation-adjusted actual return of SHY because the boundary line between Reserve and Working belongings. We’ll name SHY or any of its many family capital-C Money.

The vital level to understand is how the quantity of reserve belongings held impacts the speed of return on whole belongings. Contemplate the next desk of whole asset returns throughout our take a look at interval, starting with the 14% in reserve belongings that TRI reviews above, after which lowering the reserve belongings to 7% and 0%:

|

Whole Belongings 6/2006 |

% Reserve Belongings |

% Working Belongings |

CAGR of Whole Belongings |

Steadiness 3/2024 |

30-Yr Projection |

Most Drawn |

Sharpe Ratio |

|

100,000 |

14 |

86 |

7.59% |

366,397 |

897,754 |

-19.87% |

0.86 |

|

100,000 |

7 |

93 |

8.11% |

399.134 |

1,037,471 |

-21.19% |

0.86 |

|

100,000 |

0 |

100 |

8.61% |

433,201 |

1,191,501 |

-22.48% |

0.86 |

What we see right here is the basic monetary idea of danger/reward trade-off at work. Reserve belongings are held in very low-risk, low-reward devices (Money); working belongings reminiscent of TRI’s Julia portfolio produce larger reward in return for being extra weak to market fluctuations. The much less danger one chooses to take (by holding a larger share of reserve belongings), the less {dollars} a working portfolio has with which to earn its projected return. Since Money produces a decrease return than any of the opposite belongings usually held in a working portfolio, holding extra Money will inevitably end in a decrease return on whole belongings {that a} working portfolio can produce. Nevertheless, the Sharpe ratio, reward gained for every unit of danger taken, stays precisely the identical.

What’s the proper share of reserve belongings to carry? The reply will differ for every particular person. Some persons are merely extra risk-averse than others (as with the authors of this text.) Some folks could fairly anticipate a larger chance of emergency bills sooner or later. Some could select to lower the proportion of belongings held in reserve as whole belongings improve, whereas others could not. There’s merely no accounting for monetary style.

However one vital benefit of segregating reserves from working belongings is that it permits a fairly exact dedication of the prices of security. TRI describes his private state of affairs:

I didn’t personal Julia till early 2023. Nevertheless, if I had held Julia since June, 2006, then our again take a look at could possibly be used to research the prices of the 14% I now maintain in reserves towards the prices or advantages of different potential percentages.

For instance, if I had held solely half of that 14% in reserves over the past 18 years, then my spouse and I’d be capable of safely transfer into the luxurious retirement village of our goals three years sooner. As it’s, actuarial tables and Monte Carlo simulations present that, ought to we transfer there in 2024, we might not be utterly out of the woods for going bankrupt in our late-90s, within the unlikely however potential state of affairs the place we dwell that lengthy. Since going bankrupt with one’s private belongings set out on the curb at that age is the worst conceivable finish to lives which have gone fairly properly thus far, we select to not run that danger. So we are going to examine again in a couple of years, after we are nearer to the end line. A further three years of cooking, cleansing, dwelling upkeep, yard work, and so forth. was the fee to us of holding 14% fairly than 7% in reserves since 2006. That’s as exact and vivid an instance of the price of one stage of reserves vs one other as will be drawn.

Such hindsight is ideal, however what about going ahead? I’m not comfy going ahead with solely 7% in reserves, as a result of I’m not assured the following 18 years will go as properly for us personally because the final 18 have. In actual fact, I can be fairly shocked in the event that they do. Age 96 will not be but, and doubtless by no means can be, the brand new 78. I’m fairly ignorant concerning the prices of varied hazards we would confront—e.g., the potential prices of pharmaceuticals over and above what a Medicare drug plan will cowl, the common measurement of well being emergencies occurring abroad and therefore past Medicare protection, or the common quantity not lined by householders insurance coverage for pure disasters in our space. There could possibly be black swan potentialities that aren’t even remotely on our radar. Happily, there are on-line websites with disinterested consultants whose job is to know and quantify such issues. Relying closely upon their estimates, I tentatively settle upon a variety of 12-22% going ahead for individuals in our circumstances.

Regardless of the measurement of the reserves a person settles upon, nonetheless, the authors consider that it’s vital to not muddy the excellence between reserve and dealing belongings by placing reserve belongings into a working portfolio. Contemplate Browne’s Everlasting Portfolio, most likely essentially the most well-known instance, which specifies 25% held in Money. Examine the outcomes if we take Money fully out of the Everlasting Portfolio, or scale back it to a extra modest 10%, whereas sustaining equal proportion between the opposite components.

|

Everlasting Portfolio, 6/2006-3/2024 |

Preliminary Steadiness |

Ultimate Steadiness |

30-Yr Projection |

CAGR |

Most Drawn |

Sharpe Ratio |

|

Browne’s Authentic: 25% every VTI, TLT, GLD and Money |

100,000 |

300,254 |

641,245 |

6.39% |

-17.20% |

0.69 |

|

No Money within the PP: 33.3% every VTI, TLT and GLD |

100,000 |

385,594 |

978,686 |

7.90% |

-21.45% |

0.69 |

|

30% every VTI, TLT, GLD, with 10% Money |

100,000 |

348,103 |

823,309 |

7.28% |

-19.73% |

0.69 |

That’s fairly dramatic! Now, maybe Browne was actually so risk-averse that he was keen to surrender very massive quantities of cash to keep up 25% in reserve funds. Maybe he had merely not thought-about how variations in particular person circumstances can produce nice variations within the quantity wanted in reserves. We suspect, nonetheless, that he was merely entranced by the symmetry of a portfolio divided into equal fourths. Had he began out from a distinction between working and reserve belongings, considering the discount of return launched by every incremental improve of reserves, he may properly have ended up allocating much less to Money. (The 30-30-30-10 allocation brings Browne as much as nearly precisely the CAGR of the basic 60/40 portfolio, with a far superior most drawdown.) In any case, we consider that mentally separating the working portfolio from the specified quantity of reserve belongings can have a clarifying impact on the considering of most buyers.

Whereas we’re on this topic, we should always word that the “Buffett’s Widow” AWP – 90% VTI, 10% SHY – additionally suffers from the identical drawback of blending Working and Reserve belongings. Is 90-10 actually the perfect match for each investor’s danger tolerance? Mrs. Buffett may nonetheless need to put aside 10% prepared Money from her working portfolio, however people with a extra modest quantity of belongings or a extra conservative temperament may need significantly extra. Once more we see that the composition of the working belongings, and the proportion of reserve belongings, are two totally different questions. Buffett’s recommendation may extra helpfully be generalized as “Put all your Working assets in a broad market fund like VTI, after setting aside the amount of Reserves that will make you feel comfortable.”

The Additional Evolution of Julia

TRI: A yr in the past, Julia and my private portfolio have been basically similar. Since then, as talked about above, I’ve conceptually (however not bodily) moved SHY and SNOXX ETFs right into a separate reserve portfolio. I’ve additionally completely closed the TIP ETF, with many of the proceeds going to supply a lift to reserves. Not solely did I need to increase the reserves; I additionally couldn’t see how TIP was serving any portfolio goal distinct from AGG. Backside line: TIP is gone, and our reserves now comprise 14% of our whole monetary belongings.

Excluding the reserve belongings SCHO, SNOXX, and TIP brings Julia to an allocation of 56% shares, 44% bonds. This led the authors to marvel what would occur if we took Julia the remainder of the way in which to 60/40, whereas retaining the division of the inventory portion described above, and simplifying the bond portion to comprise solely the combination and long-duration bond funds. Additional trial-and-error experimentation in Portfolio Visualizer additionally led us to eradicate XLU, the weak sister among the many three SPDR defensive sector funds. The ultimate outcome was a enormously simplified Julia consisting of QQQ, 20%; VIG, 20%; XLP, 10%, XLV; 10%; TLT, 20%, and AGG, 20%.

Let’s begin with a straight-up comparability of the brand new 60/40 Julia to the basic 60/40 (as embodied in Vanguard’s VBIAX fund.) Outcomes are up to date by way of March 31, 2024.

|

Portfolio |

Initiated 6/2006 |

CAGR |

Steadiness 3/2024 |

30-Yr Projection |

Most Drawn |

Sharpe Ratio |

|

Julia 60/40 |

100,000 |

9.32% |

490,000 |

1,448,724 |

-21.89% |

0.89 |

|

Vanguard 60/40 |

100,000 |

7.72% |

376,738 |

930,873 |

-32.45% |

0.66 |

We confidently draw some conclusions from this outcome. The basic 60/40 portfolio is a venerable contender amongst AWPs, and outperforms a variety of latest, extra unique designs. However utilizing a broad or whole market index like SPY or VTI for all the inventory part of a 60/40 portfolio fails to separate the wheat from the chaff. Through the use of a balanced collection of established dividend payers, dynamic development corporations, and dependable defensive sectors (VIG, QQQ, and XLP/XLV), Julia tends to seize the extra reliable earnings growers of the broad market, that are on stability the higher performers. It tends to exclude the dinosaurs, the large-cap corporations which might be adrift or in decline.

In consequence, Julia has a greater compound common development price, holds up higher in “bad weather”, and produces larger returns for the danger taken. The division of Julia’s bond part between a broad market fund (AGG) and long-term Treasuries (TLT) could have the same profit, however we take no place on the query – it’s a topic for additional analysis. General, nonetheless, we predict a 60/40 portfolio with a segmented inventory part clearly outperforms an undifferentiated broad market index.

And the way does Julia of 2024 carry out towards the 2023 mannequin? To reply this query, we should do not forget that Julia 2023, as described by TRI, contained a built-in 14% allocation to order belongings. The one option to make an apples-to-apples comparability of Julia 2024 and Julia 2023 is to have a look at the entire return for an investor who units apart 14% of his/her whole wealth in reserve belongings, after which evaluate the outcomes. Whereas we’re at it, we will additionally examine the outcomes for an investor who holds 86% in VBIAX, the Vanguard 60/40 fund, and the identical 14% in reserve belongings. Portfolio Visualizer provides us the next outcomes for our take a look at interval:

|

Whole Belongings |

Initiated 6/2006 |

CAGR |

Steadiness 3/2024 |

30-Yr Projection |

Most Drawn |

Sharpe Ratio |

|

1-86% Julia 2024, 14% reserve belongings |

100,000 |

8.77% |

447,663 |

1,245,300 |

-21.02% |

0.90 |

|

2-Julia 2023, 14% reserve belongings built-in |

100,000 |

8.37% |

419,052 |

1,114,993 |

-20.04% |

0.88 |

|

3-86% Vanguard 60/40, 14% reserve belongings |

100,000 |

7.72% |

332,834 |

930,873 |

-27.33% |

0.67 |

Portfolio Visualizer

And so, on equal footing, Julia 2024 represents an incremental enchancment from Julia 2023, with barely higher return for danger taken and barely larger long-term return, on the expense of barely larger potential drawdown. Both model leaves basic 60/40 with undifferentiated inventory and bond elements within the mud. However the construction of Julia 2024 is actually less complicated and extra intuitive than Julia 2023.

And moreover the slight optimization, we consider that the separation of Working and Reserve belongings makes Julia 2024 a lot simpler to conceptualize and handle. Suppose an investor desires to maintain most drawdown to lower than 20%, the generally-accepted definition of a bear market. Superb; slightly trial-and-error with Portfolio Visualizer will reveal that conserving 20% in reserve belongings reduces most drawdown to 19.87%. Suppose the investor desires a CAGR of 9% (which in response to the rule of 72, will double working belongings each 8 years); Portfolio Visualizer says that 10% in reserve belongings will permit that outcome to be achieved (on the value of a 21.79% most drawdown.) In return for slightly work, the construction of Julia 2024, together with utterly segregated Working and Reserve belongings, permits (or challenges) the investor to determine precisely what danger/return trade-off they like.

TRI once more: Making substantial alterations to a digital portfolio is a snap, however making them to an actual one is more durable. I’m en route in direction of full implementation of the brand new Julia, however am not there but. As of April 1, my funding portfolio is QQQ, 18.9%; VIG, 19.2%; XLP, 10%, XLV, 10%; TLT, 20%; and AGG, 21.9%. The remaining swap of extra AGG funds for extra QQQ and VIG is on maintain till the 2 inventory ETFs take a major dip. As for an acceptable stage of reserves, our present 14% is in direction of the low finish of the 12-22% talked about above, however I really feel comfy with it. I’ve no plans to maneuver it both decrease or larger.

I’ve made a couple of minor, judgment-based rebalancing trades over the past twelve months, the main points of which aren’t value recounting. Extra importantly, I’ve determined that at most I’ll make solely such minor, selective rebalancing strikes. This coverage will proceed so long as I handle the household portfolio. If at some future date my spouse has to take over, then restructuring and rebalancing will instantly and completely finish. Like many SA spouses, she has no data of nor curiosity within the markets. This has been a significant component in my seek for a portfolio that at some future date might properly change into utterly hands-off.

This raises the entire topic of periodic portfolio rebalancing. Portfolio Visualizer defaults to rebalancing Julia yearly—no muss, no fuss. In distinction, rebalancing an precise portfolio is extra tedious, and might carry dangerous tax penalties. Frankly, it’s not clear that even an entire failure to rebalance could be all that dangerous; it might even be an enchancment. A Portfolio Visualizer take a look at reveals that when the Rebalancing choice in Julia is about to None, its max drawdown will increase lower than 3%, whereas its CAGR will increase 0.7%, over all the 18-year take a look at interval! The Sharpe ratio is unchanged. On an preliminary funding of $100k, the un-rebalanced portfolio’s worth will increase $60k greater than the worth of 1 that’s rebalanced yearly. Extrapolate these outcomes to the following 18 years, and the extent of danger creep is just not value fretting over. The acquired knowledge concerning the need of rebalancing wants a lot nearer examination. May or not it’s that the market itself does a greater job of rebalancing than a numeric components that dictates at all times holding to a share allocation that’s precisely the identical?

Conclusions

- The basic 60/40 portfolio units a danger/return baseline that any AWP ought to be capable of match, though as we demonstrated in our earlier article, many well-known proposals for AWPs fail to beat the return of 60/40, contain larger danger, or make claims primarily based on cherrypicked time durations.

- A 60/40 portfolio reminiscent of Julia that makes use of a segmented collection of ETFs inside its inventory part produces outcomes which might be clearly superior to utilizing a broad market index.

- Traders ought to draw a pointy distinction between Working belongings, i.e. belongings meant to supply a return measurably above inflation, and Reserve belongings, i.e. belongings put aside for emergencies and on a regular basis transactions, that aren’t primarily meant to supply investment-like returns.

- AWPs ought to comprise solely Working belongings, and be evaluated solely on their funding efficiency; Reserve belongings (“Cash”) shouldn’t be included in AWPs. As soon as buyers determine what share of their whole belongings must be put aside as Reserves, they will consider the AWP they like primarily based purely on efficiency measures, and allocate the rest of their belongings to it accordingly.

- Julia 2024 gives the perfect danger/reward proposition of any AWP within the broad custom of 60/40 allocation.

Postscript

It happens to us that Julia will not be the one software by which a extra focused collection of inventory funds may yield clear enchancment to an AWP. Julia has advanced and has been designed to enhance upon average AWP’s, of which the 60/40 is the enduring mannequin. However not everyone seems to be desirous about taking the broad, center path. Perhaps individuals whose pursuits lie in direction of every finish of the rewards continuum might additionally profit from the identical primary method that now we have used to make Julia profitable amongst average AWPs.

We’re at the moment investigating this chance, and hope to share our findings in a later article. Ideally, we wish to present that Julia is only one software of a basic principle concerning the employment of centered vs broad funds in AWPs.