alvarez

While the Biden Administration put what it called a “temporary pause” on pending licenses for liquefied natural gas export facilities, as I (and much of the financial media) have emphasized, a number of projects already have the necessary approvals from the Department of Energy and Federal Energy Regulatory Commission to be built regardless today. Corpus Christi Stage III, Golden Pass, Rio Grande LNG, and Port Arthur LNG all will be online between late 2024 and 2028, adding 11.0 Bcf/d of incremental export capacity; total United States LNG capacity will exceed 25.0 Bcf/d. While we can speculate on what exactly happens in the 2030s, that feedgas demand looks mighty guaranteed.

Many of these projects are in Texas and are going to see the bulk of their feedstock come from the Permian and Eagle Ford. That necessitates new pipelines and might change the pricing dynamics at key market hubs for natural gas in Texas. We will talk about Waha Hub – this topic came up recently in Summit Midstream coverage (see “Summit Midstream: Still No Good“) and what is going on to help fix the price situations there.

The Waha Hub

The Waha Hub is located in Pecos County, on the southeastern edge of the Delaware Basin (which tends to be gassier than the Midland) and just to the west of the Midland. It is a major physical gathering point for natural gas from the region and has rapidly become a major selling point and transit for Permian produced gas.

Prices have often turned negative in Waha when supply coming into the hub has outstripped available pipeline capacity out. That’s happened several times since the Permian Basin started to gain prominence, and it’s begun to happen again recently. Making matters worse is the fact that flaring or burning excess natural gas is now heavily regulated and restricted; in the past, some producers would get away with burning excess. That’s just not a reality now.

Fast-forward to 2024, and available capacity out of Waha has already been tight, but as several pipelines have gone down for seasonal maintenance (Gulf Coast Express, the El Paso Natural Gas System, others), the situation is back to oversupply – unfortunately in an already oversupplied natural gas market. Gas traded at the Waha hub has traded below zero most days since mid-March. The low was -$3.50 per mmbtu in mid-April, or a $5.00 spread to Henry Hub at the time. Producers without pipe capacity out of the Permian have been paying other shippers to take their gas or store it, absorbing the cost to maintain production.

Joint Venture

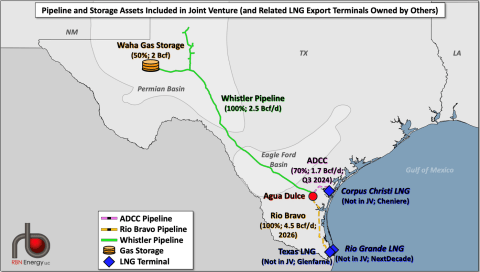

Solving Waha’s problems will take time. New pipelines will have to be built, especially down towards newer Gulf Coast LNG facilities that will create new sources of demand. That helps to explain why three large Permian players – MPLX (MPLX), Enbridge (ENB), and privately held WhiteWater Midstream – recently formed a joint venture to combine assets and build out new ones to help address Waha basis. See the below map from RBNEnergy which helps outline these assets a bit as well:

RBNEnergy

- The Whistler Pipeline, a 2.5 Bcf/d pipeline owned and operated by Whitewater and MPLX, which runs from Waha Hub to Agua Dulce near Corpus Christi.

- 50.0% ownership in Waha Gas Storage, a 10.0 Bcf/d gas storage facility in Waha owned by Whitewater Midstream

- 70.0% interest in ADCC Pipeline, a joint venture between the owners of Whistler and Cheniere (LNG). This is a 1.7 Bcf/d, short run line that connects Agua Dulce to Cheniere’s Corpus Christi liquefaction plant.

- 75.0% of the 4.5 Bcf/d Rio Bravo Pipeline that is under construction by Enbridge, which will have two large lines running in parallel from Agua Dulce to the planned Rio Grande LNG facility.

Everyone is bringing different assets to the table here, and will also have differing ownership interests. Whitewater will hold a 50.6% stake in the venture, while MPLX will own 30.4% and Enbridge will own 19.0%. MPLX and Whitewater are solely contributing assets, while Enbridge will pass along $350mm in cash and fund the first $150mm of project capex. Interestingly, the Matterhorn Pipeline, a 2.5 Bcf/d pipeline that Whitewater is building that runs from Waha to end markets (MPLX is also a minority owner) was not included in this venture.

Whitewater will operate the joint venture’s pipeline and storage projects, perhaps surprising to some reading this, given they are the private party and working with some of the largest names in midstream. Whitewater has escaped (presumably) a litany of takeover bids and offers over the recent years, and has instead managed to grow itself into one of the largest operators in the Permian while remaining a private entity. Continued deals like this shrink the odds of it ever getting taken out by a name we recognize.

Whistler Pipeline is likely to have an expansion announced (via compression) announced later this year. And I expect that the joint venture might announce another Waha Hub egress pipeline in early 2025 to continue to solve challenges faced by the Permian in getting gas out of the basin and out to market, albeit smaller than what we have on the docket already from Whitewater in the form of Matterhorn.

While there is a lot of capacity coming, remember the demand also on the way from LNG. More expansions are on the way. The Gulf Coast Express expansion will add 0.5 Bcf/d of incremental capacity, bringing more gas from Waha (and other interconnects around the Permian) to Agua Dulce. Energy Transfer continues to plan the 2.0 Bcf/d Warrior Pipeline, which would run from the Midland Basin to just south of Dallas in Fort Worth. While not serving Waha directly, Warrior would pull gas that would otherwise end up there into other markets.

Targa Resources (TRGP) also has a 2.0 Bcf/d project planned, the Apex Pipeline, which would also run from the Midland to the Beaumont area, putting natural gas right on the Texas / Louisiana line. The latter would likely serve as a key source of feedgas for Golden Pass LNG and Port Arthur LNG. In total though, all the projects mentioned sum up to 7.0 Bcf/d that bring gas out of the Permian to hubs located closer to the coasts, so arguably there is room for another pipe or two depending on how important the Haynesville ends up being to providing surety of supply for LNG marketers or these new LNG facilities themselves.

Takeaways

The concerted efforts of industry stakeholders to address the challenges of oversupply and constrained pipeline capacity at the Waha Hub underscore the critical importance of infrastructure development in the Permian Basin. Much of the pathways to solving the Waha Hub basis issue are unfortunately months (and in some cases years) away, so expect differentials to continue to spike and be at times wide – particularly during periods like the present where crude oil prices remain strong.

The formation of the joint venture between MPLX, Enbridge, and Whitewater Midstream, along with ongoing expansion projects like the Whistler Pipeline and Rio Bravo Pipeline, exemplifies a proactive approach to meeting the rising demand for natural gas transportation, particularly to support the growing LNG export market along the Gulf Coast. While significant progress has been made, the evolving energy landscape suggests the need for continued investment and innovation to ensure the efficient and reliable delivery of natural gas from production hubs to end-users, both domestically and internationally.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.