sruilk/iStock through Getty Photos

At a Look

Within the dynamic world of biotech/pharma shares, Journey Medical Company’s (NASDAQ:DERM) current surge has been nothing in need of meteoric. The corporate, targeted on dermatological circumstances, has seen its inventory endure a parabolic transfer, catapulting it to the highest of In search of Alpha’s general Quant ranking. This ascent is a testomony to Journey’s strategic imaginative and prescient within the pharmaceutical trade, significantly in dermatology, the place it has made vital inroads with progressive merchandise and savvy enterprise maneuvers. Nonetheless, beneath this success lies a fancy monetary panorama marked by each vital achievements and challenges. The next article delves into Journey’s journey, inspecting its strategic deal with dermatology, the implications of its current monetary efficiency, and the potential of its promising drug, DFD-29, amid the intricacies of the healthcare sector.

The Dermatological Pursuit: Journey’s Strategic Imaginative and prescient

Journey, established in 2014, has been navigating a fancy panorama within the healthcare sector. Famend for its deal with dermatological circumstances, Journey’s product portfolio consists of eight branded and two approved generic pharmaceuticals. These merchandise kind the spine of its enterprise mannequin, which is centered on licensing, creating, and commercializing FDA-approved prescribed drugs.

Journey’s specialization in dermatological merchandise positions it uniquely within the pharmaceutical trade. This specialization has been each a energy and a problem. As an illustration, the corporate confronted difficulties with its Ximino merchandise, resulting in a major intangible asset impairment cost of $3.1 million within the 9 months ending September 30, 2023 (page 8). This example underscores the dangers inherent in a targeted product portfolio, the place the underperformance of 1 product can have substantial monetary implications.

Notably, Journey has made significant strides with DFD-29, a modified launch oral minocycline for treating rosacea.

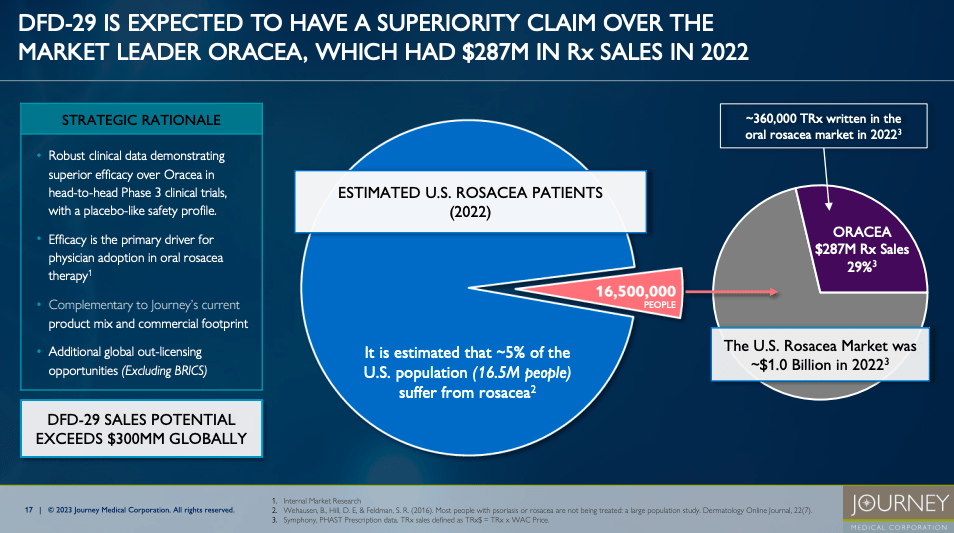

Journey Investor Presentation

In June 2021, the corporate obtained the worldwide growth and commercialization rights from Dr. Reddy’s Laboratories, committing to contingent regulatory and business milestone funds as much as $158.0 million, together with royalties on web gross sales (page 9).

DFD-29 seems poised to make an impression within the remedy of reasonable to extreme rosacea, aligning nicely with present remedy tips that favor oral antibiotics, particularly tetracyclines. This growth is especially related as rosacea typically escalates past the efficacy of topical therapies, necessitating a extra systemic strategy. The anti-inflammatory properties of minocycline deal with the core signs of rosacea, together with inflammatory papules, pustules, and erythema. The successful outcomes of two Phase 3 clinical trials and the anticipated FDA approval in late 2024 spotlight DFD-29’s potential as an efficient and doubtlessly superior remedy different. DFD-29’s modified launch formulation might supply a more practical and doubtlessly safer strategy whereas additionally becoming into the present shift in the direction of subantimicrobial doses in rosacea administration. This positions DFD-29 not solely as a promising new choice for sufferers with extra extreme rosacea but additionally as a testomony to Journey’s progressive strides in dermatological therapeutics.

Q3 Efficiency

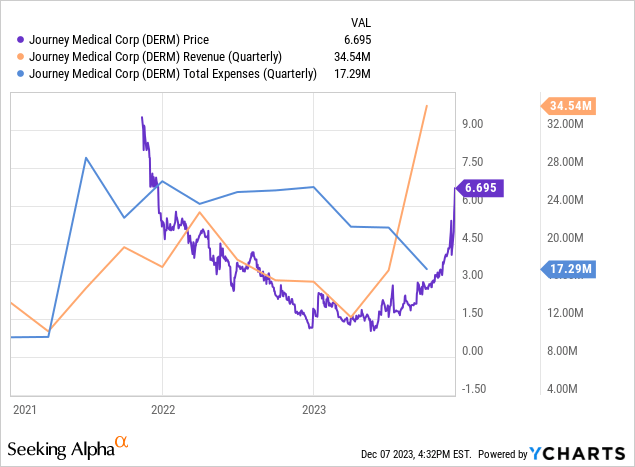

Within the third quarter of 2023, Journey skilled a major monetary turnaround, with whole income surging from $16.12 million in Q3 2022 to $34.54 million in the identical interval in 2023. This outstanding progress was largely pushed by a profitable licensing settlement with Maruho for Qbrexza in Asian markets, contributing an upfront cost of $19.0 million, and accounted for the substantial rise in different income from $73,000 to $19.3 million. Regardless of this, the corporate’s web product income declined barely from $16.04 million to $15.28 million, signaling volatility in its core enterprise operations. Notably, the gross revenue margin improved as the price of items offered decreased from $7.2 million to $6.4 million, demonstrating environment friendly value administration. Moreover, a discount in promoting, normal, and administrative bills from $15.6 million to $8.6 million, coupled with a lower in whole working bills from $25.6 million to $17.3 million, resulted in a optimistic earnings from operations of $17.2 million, reversing a lack of $9.5 million from the earlier 12 months. The quarter concluded with a web earnings of $16.8 million, a stark distinction to the web lack of $10.1 million in 2022.

Stability Sheet

Turning to Journey’s balance sheet, their property, together with money and money equivalents ($24.7M), present a notable lower from the earlier interval. The present ratio, calculated as present property divided by present liabilities, stands at roughly 0.92 ($44.7M/$48.5M), indicating potential short-term liquidity challenges. When evaluating property to liabilities, there’s an evident enhance in short-term obligations like accounts payable ($28.2M) and accrued bills ($16.0M), with a complete present legal responsibility of $48.5M in opposition to a complete asset worth of $65.9M. The web money offered by working actions over the past 9 months is $21.8M, indicating a optimistic money stream.

Speculating on the necessity for added financing inside the subsequent 12 months, given the present monetary state and optimistic working money stream, the chances appear medium. The corporate’s present ratio under 1.0 and the discount in money and money equivalents may necessitate future financing, however the optimistic money stream from operations may offset some fast issues.

My Evaluation & Advice

Wrapping it up, Journey stands out as an funding decide, particularly given its monetary comeback and the thrill round DFD-29, their promising rosacea remedy. The corporate’s spectacular income uptick in Q3 2023, fueled by good licensing offers and savvy value management, factors to a strong restoration path. However let’s not overlook, investing in smaller corporations like Journey comes with its personal set of challenges. Their laser deal with pores and skin merchandise is a double-edged sword – it is a area of interest energy but additionally makes them extra vulnerable to market swings, as we have seen with their most important enterprise actions.

DFD-29 figures to see uptake within the massive rosacea market – its specialised formulation and adherence to present remedy requirements place Journey on the slicing fringe of skincare therapies. The drug’s potential in tackling rosacea, and the excessive hopes for FDA nod, are main components in driving the corporate’s progress going ahead. But, the bumpy street of drug growth and regulatory approvals can’t be neglected.

For many who wish to play it safer, spreading their investments throughout completely different areas can reduce the chance of placing an excessive amount of into one microcap inventory. Holding a detailed eye on Journey’s monetary well being, significantly money stream and liquidity, is vital. Additionally, staying up to date on DFD-29’s regulatory and market journey will give some good insights into the place the corporate is headed.

Given Journey’s strategic path, monetary bounce-back, and the intense prospects for DFD-29, I’d lean in the direction of a cautious however optimistic “Buy” ranking. Their current monetary success and strategic strikes in drug growth spotlight their potential to develop and revenue within the advanced healthcare sector. The current parabolic inventory transfer seems warranted. However as at all times with smaller shares, buyers ought to tread rigorously, weighing the prospect for giant beneficial properties in opposition to the everyday dangers of microcap investing.

Dangers to Thesis

In evaluating Journey’s funding potential, I could have underemphasized sure dangers inherent of their enterprise mannequin and sector. Firstly, the corporate’s heavy reliance on a targeted dermatological portfolio, whereas a strategic benefit, additionally exposes it to vital market and product-specific dangers. The difficulties confronted with Ximino illustrate how dependency on a restricted vary of merchandise may end up in substantial monetary implications if any product underperforms.

Concerning DFD-29, whereas its potential is promising, I could have underestimated the challenges in drug growth, significantly within the dermatological area the place affected person response variability is excessive. The drug’s efficacy and security profile, although seemingly aligned with present wants, should nonetheless navigate the rigorous and unsure FDA approval course of. Moreover, market reception post-approval shouldn’t be assured, given the aggressive panorama and evolving remedy paradigms.

My evaluation might have additionally positioned extreme optimism on the corporate’s monetary turnaround in Q3 2023. Whereas the income progress pushed by licensing agreements is encouraging, the slight decline in web product income raises issues in regards to the sustainability of its core enterprise. The discount in money and money equivalents, coupled with a present ratio under 1.0, signifies potential liquidity points, that are essential for a microcap firm like Journey, relying closely on steady capital infusion for R&D and operational bills. Journey might should resort to an fairness increase that may end in vital dilution.

Lastly, investing in microcap corporations like Journey comes with particular dangers. These shares typically exhibit greater volatility and decrease liquidity, resulting in higher worth swings and doubtlessly difficult entry and exit methods. Microcaps sometimes have restricted entry to capital markets, constraining their progress and R&D funding. There’s additionally the next threat of data asymmetry as a result of much less analyst protection, which might result in much less knowledgeable funding choices.