Just_Super

Abstract

Following my coverage on Thoughtworks (NASDAQ:TWKS), which I upgraded to a purchase score as I believed the enterprise was executing a lot better than anticipated – as seen from how they modified their technique to adapt to the macro setting – this put up is to offer an replace on my ideas on the enterprise and inventory. I’m downgrading my score from purchase to impartial because the TWKS has executed very poorly in 4Q23 and is anticipated to proceed underperforming friends in FY24. Additionally, on the present premium valuation, the inventory worth just isn’t enticing in any respect.

Funding Thesis

My final replace on TWKS was in June 2023, and though the share worth fell sharply, I believed the enterprise was nonetheless doing alright (3Q23 income progress beat consensus by 1% and earnings and gross margin got here in means forward, ~200 bps greater than anticipated). Nevertheless, the 4Q23 performance was actually horrible and disappointing. The outcomes had put a significant dent in my confidence in my administration capability to proceed executing on the degree that I initially anticipated.

Within the 4Q23 quarter, TWKS reported income of $252 million, lacking consensus expectations of $267 million. What was worse is that the unfavorable progress truly accelerated to -18.8% from -15.7% in 3Q23. On a relentless foreign money foundation, income was down much more (-22%). By segments, Tech/Companies had been down probably the most at -23% y/y; Retail/Client down 19%; Vitality/Public/Well being down -12%; Auto/Journey/Transport down 7%; and Financials/Insurance coverage down 3%, respectively. Development was weak throughout all areas as properly (all down double digits, with LatAm down 37%). This set of outcomes made it clear that TWKS is closely impacted by provide challenges, pricing stress, and continued macro headwinds. In consequence, gross margin got here in low at 33.6% vs. consensus expectations of 37.9%. This additionally led to adj. EBITDA margins got here in a lot decrease than anticipated at 5.5% vs. expectations of 11.5%.

Round two-thirds of the income shortfall was resulting from particular supply-side limitations. This was primarily as a result of scale of the construction change in our working mannequin, which prompted some disruption to our operations within the fourth quarter.

Continued shopper warning resulted in smaller mission ramp-ups, extra mission delays, and we had barely greater pricing stress than we anticipated. We anticipate this cautious habits to proceed into 2024. 4Q23 earnings results call

Bloomberg

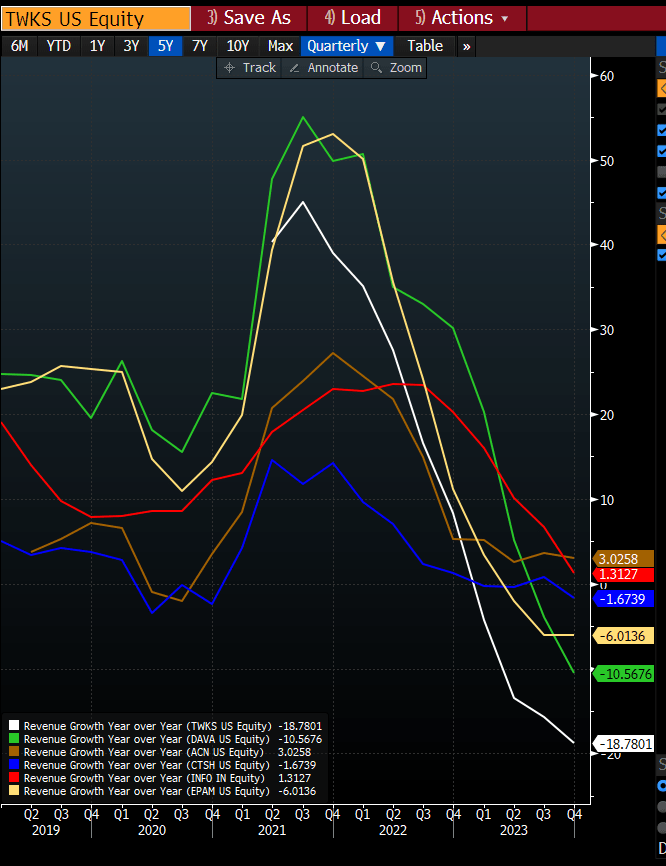

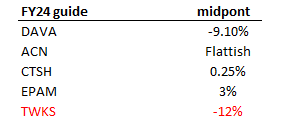

My greatest concern is the relative efficiency of TWKS towards different friends, which is a pink flag that signifies a significant market share loss. Should you take a look at the chart (4Q y/y efficiency), TWKS 4Q23 efficiency suggests not less than 800bps of share much less (when in comparison with DAVA, the second-weakest performer). Initially, I believed that it was a matter of scale (i.e., extra distribution capability so they may discover extra offers). However that does not appear to be the case since Endava has roughly the identical income measurement however outperformed by ~750 bps. This actually makes me query the execution of administration.

Administration steering for FY24 additionally implies additional progress stress. TWKS 2024 steering requires $980 to $1.01 billion in income, or 11 to 13% decline on a relentless foreign money foundation, which is 1000bps under consensus pre-results expectation for 1.121 billion in income and much more when in comparison with my expectation of $1.4 billion in income. Once more, this steering fares a lot worse than friends as properly, suggesting additional share losses. Qualitative feedback by administration additional help the narrative that efficiency goes to remain weak. Whereas they stated progress is stabilizing with respect to mission cancellations, pricing stress, delays, and slower ramps stay. Particularly, whereas budgets are additionally anticipated to be flat in comparison with final 12 months, pricing goes to face extra stress. The hope is for pricing to be stabilized in order that TWKS will see sequential enhancements; nonetheless, at this level, I believe the weak execution that drove the massive share loss goes to be the principle focus of the market. Till TWKS exhibits higher execution (i.e., progress inflects again to be consistent with or higher than friends), the market is prone to proceed punishing the inventory.

Personal calculation

TWKS can also be prone to face stress on the margin aspect of issues. The apparent motive is the decrease income. The second motive is that TWKS is ramping up its offshore supply capabilities, which suggests plenty of mounted prices are going to movement into the P&L till utilization picks up over time (which depends on the macro setting and administration executing higher). Whereas the offshore combine shift will seemingly enhance margins in the long term, the difficulty is that it’s going to lower into the higher-margin onshore enterprise within the quick time period (extra stress). Lastly, TWKS can also be nonetheless within the midst of restructuring. Whereas restructuring prices in 2024 must be lower than in 2023, administration did anticipate CAPEX to extend from 2023 ranges, which places additional stress on the free money movement margin (which is already below stress from decrease revenue margins).

Valuation

Personal calculation

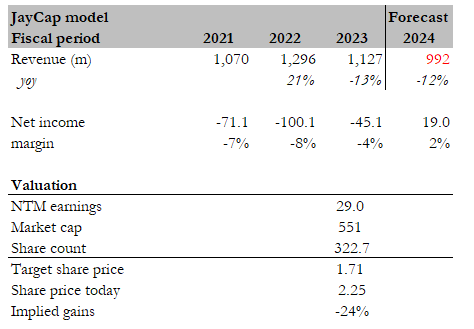

My goal worth for TWKS, primarily based on my mannequin, is $1.71. This can be a large downgrade from my earlier goal worth of $12.74. I acknowledge the error I made in overestimating TWKS’s administration capability to execute, which could be very evident within the 4Q23 outcomes and FY24 information. I’m not adopting a way more conservative method to modeling the enterprise, specializing in the near-term outlook quite than the mid-term (3-year outlook). Utilizing FY24 steering as a information (giving administration the advantage of doubt), I forecast income to fall by 12% to $992 million. As for margins, I used administration EPS steering to work backward into ~$19 million of earnings, implying a 2% internet margin. Right here is the factor: even when administration does obtain this and valuation stays on the present excessive degree of 29x, the share worth continues to be not enticing at this degree. Whereas consensus is anticipating internet earnings to inflate to $60 million (income to develop 9% in FY25), I’m not keen to connect any worth to FY25 figures provided that near-term execution is a query mark.

Conclusion

I downgraded TWKS to impartial. The core motive for the downgrade is the weak execution that TWKS has showcased in 4Q23. Particularly, the current 4Q23 outcomes had been a significant disappointment, with income and margins falling wanting expectations throughout all segments and geographies. Much more regarding is TWKS’s underperformance in comparison with friends, indicating potential market share loss. TWKS’s FY24 steering paints a grim outlook. The corporate expects income to say no additional, and commentary suggests ongoing headwinds from mission delays, pricing pressures, and funds constraints.