Ingenious Buddy

The iShares 20+ 12 months Treasury Bond BuyWrite Technique ETF (BATS:TLTW) is a comparatively new ETF with an inception date again in August, 2022. The funding goal of TLTW is to supply the next benefits for the traders:

- Enhanced revenue or yield: the next yielding various for traders, who search to hold an publicity in the direction of conventional U.S. Treasury bonds by promoting month-to-month coated name choices.

- Diversification: due to the presence of coated name technique, TLTW can function a diversification component offering a compelling hedge beneath a situation of rising rates of interest.

-

Easy accessibility: a cheap and slightly easy entry to a scientific possibility technique on the U.S. Treasury market (i.e., the avoidance of guide trades or costly brokers).

All of that is provided for traders at comparatively low cost worth (i.e., 0.35% expense ratio) regardless of the embedded coated name technique, which per definition is extra complicated and harder to handle than pure-play fairness or mounted revenue ETFs.

Now, if we take a look at TLTW’s construction virtually the whole AuM quantity is allotted into iShares 20+ 12 months Treasury Bond ETF (NASDAQ:TLT). In different phrases, TLTW carries a base publicity in the direction of lengthy length Treasury bonds, which, in flip, implies that TLTW is slightly concentrated within the length issue.

Which means that with out the presence of the embedded optionality, TLTW would reply to any modifications within the rates of interest in a extra magnified style than Treasuries or company funding grade bonds with shorter maturities.

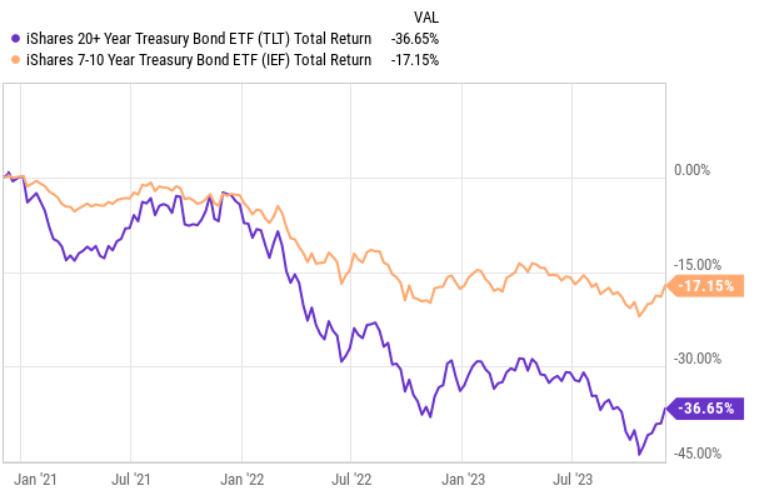

Ycharts

We are able to clearly seize the essence of a length issue within the chart above, which illustrates how TLT has responded to the sudden tightening of financial coverage in early 2022 relative to an ETF carrying Treasuries which are certain by shorter maturity dates.

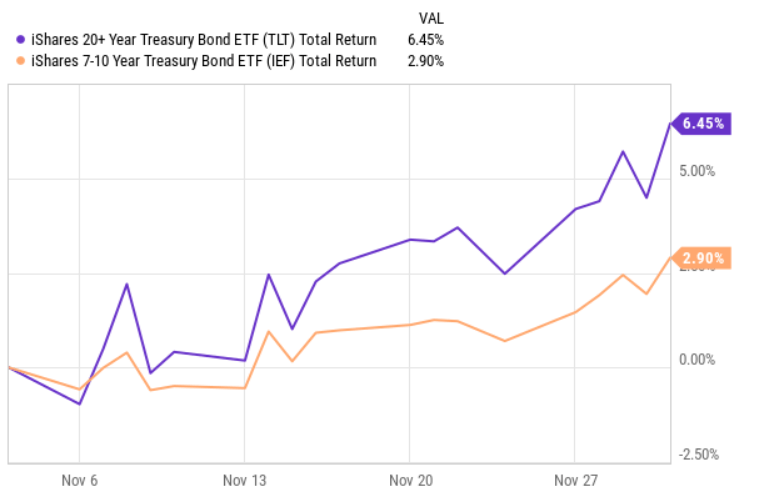

Ycharts

An analogous logic or sample applies, when the market begins to calibrate its expectations on experiencing charge cuts within the foreseeable future. The truth is, that is what we now have seen previously couple of weeks. So it is just logical that TLT has bounced again in a extra materials style than a lot of the different mounted revenue ETFs with extra restricted length issue.

But, in TLTW’s case there’s a coated name technique that’s included on high of the allocations into TLT. What this implies is that TLTW sells name choices which expire one month after their issuance and correspond to the variety of TLT shares owned, thereby maximizing the protection of base publicity to TLT.

By doing so, TLTW successfully ensures the next:

- Ceiling on the utmost month-to-month worth acquire or capital appreciation of TLTW that’s restricted to the strike of the bought name possibility.

- Further month-to-month revenue on high of the underlying yield of TLT stemming from the pocketed premium of written name choices.

- Barely protected draw back as a result of collected premium within the case of additional charge will increase, extra hawkish expectations or credit-risk pushed decline within the U.S. Treasuries.

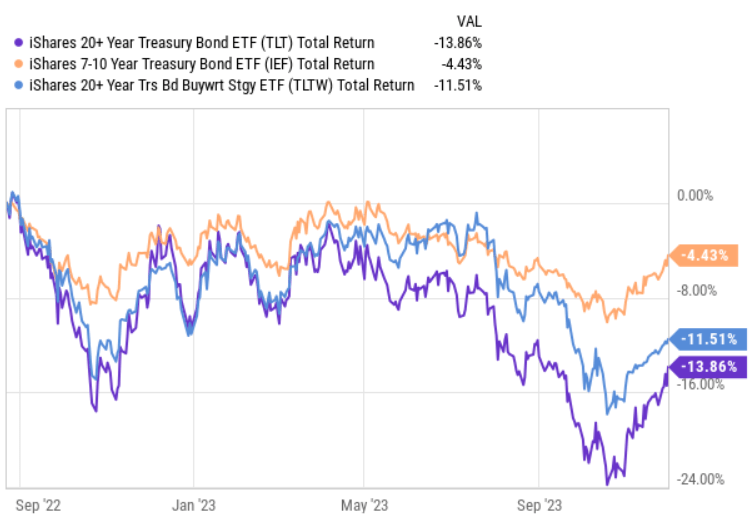

Ycharts

By wanting on the chart above, it’s fairly evident how the aforementioned dynamics have performed out for TLTW. Specifically, within the interval when the mounted revenue traders received more and more punished, TLTW managed to outperform TLT, whereas over the previous couple of weeks, when the market’s sentiment has develop into extra dovish, TLTW has recovered in a bit extra muted method than TLT.

Thesis

All in all, TLTW supplies an fascinating publicity for traders to contemplate of their portfolios as at the least a component of further diversification. Plus, the notion of accessing optionality at so low prices appears additionally enticing.

Nevertheless, in my view, this isn’t the proper second to go closely lengthy on TLTW; and the explanation for that is slightly easy.

We now have to know that the added coated name technique per definition works nicely when the marketplace for bonds is buying and selling sideways or if the rates of interest are rising and the traders nonetheless want to keep some portion of their portfolios in mounted revenue securities.

Within the state of affairs of dropping charges, TLTW’s coated name technique really imposes a structural headwind for the Fund to understand the good thing about the underlying length issue (i.e., capitalizing on the decline in rates of interest). It’s because every time the TLT place appreciates past the strike degree at which the calls have been written (plus the pocketed premium quantity), the entire good points above that strike and premium cash are misplaced.

With this in thoughts, the next two charts justify my stance on TLTW.

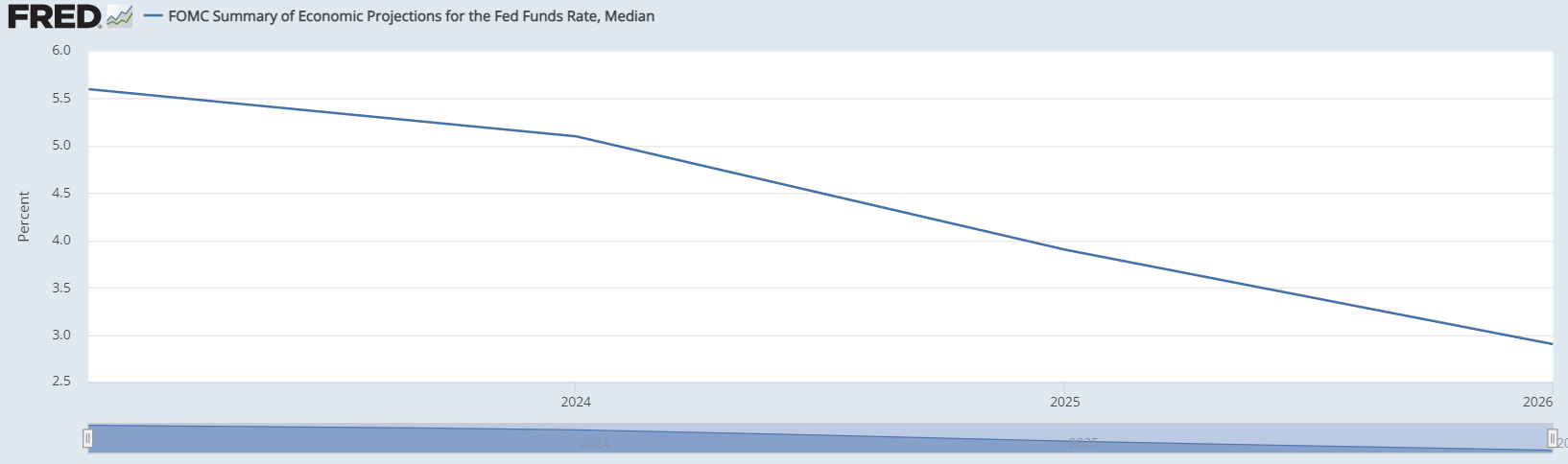

FOMC; St. Louis Fed

The Fed Funds Fee is clearly set to normalize over the foreseeable future. As we expertise decrease rates of interest, TLT can be inherently pressured to maneuver increased. Right here traders can be in a comparatively worse state of affairs by proudly owning TLTW than TLT because the cap from coated calls would restrict a full realization of the capital good points part.

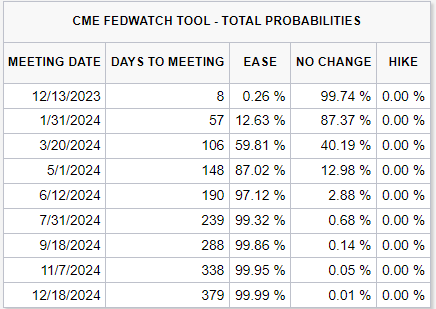

CME Group Inc

Lastly, as we are able to see within the desk above, the market appears to cost in slightly appreciable possibilities of getting decrease rates of interest some level in 2024.

The underside line

In my humble opinion, contemplating the prevailing rate of interest backdrop and the probably trajectory how the rates of interest may evolve in 2024, there isn’t a actual motivation or foundation of proudly owning TLTW. By including TLTW to portfolio, the chances are excessive that traders will underperform TLT or different lengthy length mounted revenue securities as a result of inherent restrict of the potential capital good points that would come from rate of interest cuts.

It’s also true that basing funding determination on how the market presently sees rates of interest transferring within the close to future is a dangerous concept. Nevertheless, within the context of my opinion on TLTW it does probably not matter whether or not the charges go down early 2024 or late 2024 as the one factor that issues is that the general trajectory of future rates of interest appears to imagine a structural downward pattern that may inevitably restrict the return potential.