Bloomberg/Bloomberg through Getty Photographs

“We are here and it is now. Further than that, all human knowledge is moonshine.“― H.L. Mencken

In the present day, we put luxurious and well-known house builder Toll Brothers, Inc. (NYSE:TOL) within the highlight. Regardless of the worst yr for present homes sales of the century in 2023, the shares of most house builders have superior over the previous 12 months. Regardless of this rise, TOL nonetheless seems low cost at below 10 occasions earnings. Can the rally within the shares proceed in 2024 regardless of common 30-year mortgage charges remaining stubbornly close to the seven p.c threshold? An evaluation follows beneath.

Looking for Alpha

Firm Overview:

Toll Brothers is likely one of the largest house builders within the nation and is headquartered in Port Washington, PA. The corporate is primarily centered on the posh finish of the market. Toll Brothers’ fiscal yr begins on October 1st. The inventory at present trades simply above $100 a share and sports activities an approximate market capitalization of $10.7 billion. The shares pay a small dividend of 21 cents a share at present.

Fourth Quarter Outcomes:

The corporate posted its This autumn numbers on December fifth. Toll Brothers delivered GAAP earnings of $4.11, greater than 35 cents a share above expectations. This got here at the same time as gross sales fell over 18% on a year-over-year foundation to $3.02 billion, which was some $320 million above the consensus. It additionally was solidly larger than the $2.69 billion in gross sales within the earlier quarter.

Of observe, houses delivered fell 27% from the identical interval a yr in the past, which was considerably offset by larger common promoting costs. The typical house promoting value in the course of the quarter was $1.03 million. Order backlog additionally dropped to $6.95 billion from $7.9 billion on the finish of 2Q2023 and $8.87 billion on the finish of the third quarter of 2022.

Along with beating prime and bottom-line consensus, administration offered FY2024 steering that was barely above expectations as effectively. Toll Brothers expects to ship between 9,850 to 10,350 houses within the upcoming fiscal yr. Management additionally expects its group to rise roughly 10% to 370. Administration sees $12.00 to $12.50 a share in earnings in FY2024 and believes it’ll finish the fiscal yr with a ebook worth of roughly $78 a share.

Analyst Commentary & Steadiness Sheet:

Since fourth quarter earnings posted, 13 analyst companies together with JPMorgan, RBC Capital and Financial institution of America have reiterated/assigned Purchase/Outperform scores on the inventory. Value targets proffered vary from $100 to $127 a share. Six analyst companies, together with Goldman Sachs and Wedbush, have maintained/assigned Maintain/Promote scores on the inventory since This autumn numbers hit the wires. Value targets from this half dozen pessimists vary from $87 to $106 a share.

Roughly one p.c of the shares excellent in Toll Brothers are at present held quick. Insider gross sales seem to have picked up noticeably in current months. Within the again half of 2023, insiders bought simply over $17 million price of shares collectively. Simply over half of that promoting occurred in December. A director additionally bought almost $1 million price of inventory in late January of this yr.

10-Okay for 2023

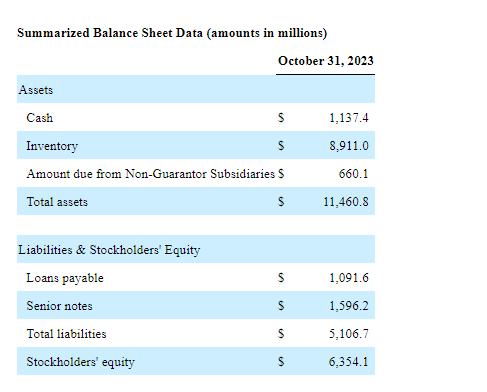

Toll Brothers exited the third quarter of 2023 with $1.3 billion in money and marketable securities on its steadiness sheet and has one other $1.8 billion of liquidity accessible through a revolving credit score facility. The corporate delivered operational money stream of $1.3 billion in FY2023. Toll Brothers reauthorized a 20 million share inventory buyback program in mid-December.

Verdict:

Toll Brothers made $12.36 (GAAP) a share in FY2023 on $9.87 billion price of gross sales. The present analyst agency consensus sees each earnings and revenues falling very barely in FY2024 earlier than transferring as much as $12.86 a share in FY2025 on low single-digit gross sales development.

The inventory trades at some eight occasions earnings and simply over 1.1 occasions revenues. Low-cost in comparison with the general S&P 500 P/E market a number of of roughly 20. Nevertheless, the house constructing sector is notoriously cyclical and usually trades for half or much less of the general market a number of. The shares of enormous house builders like PulteGroup, Inc. (PHM) commerce at comparable valuations.

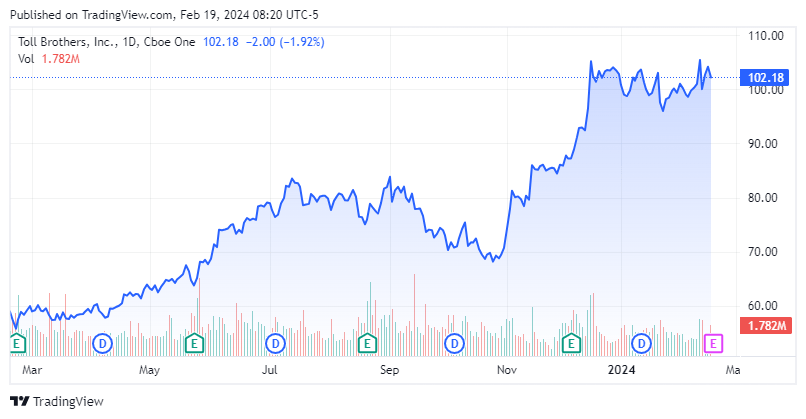

Hotter than anticipated CPI and PPI stories final week reminded the market that the ‘final mile’ on the inflation entrance is likely to be stickier than hoped. This implies hopes that the Federal Reserve will minimize its Fed Funds fee by 5 – 6 occasions in 2024 (as was the consensus to start out 2024) are more likely to be placed on maintain. January housing starts and permits additionally simply fell considerably greater than anticipated. TOL inventory is up some over 70% over the previous 12 months, partially as a consequence of these hopes, together with outcomes which have crushed expectations.

Nevertheless, the inventory is now up close to even some bullish value targets. Insiders additionally appear to be taking some chips off the desk in current months and the corporate has seen almost a $2 billion drop in backlog over the previous yr. Due to this fact, I’m going to stay on the sidelines on this identify regardless of an affordable P/E ratio.

“Weak people believe what is forced on them. Strong people what they wish to believe, forcing that to be real.“― Gene Wolfe