CHENG FENG CHIANG/iStock Editorial by way of Getty Pictures

Writer’s Be aware: All quantities are in Canadian Forex except specified

Pricey readers/followers,

On this article, I am going to provoke protection on the at present undervalued – as I see it – utility TransAlta (NYSE:TAC). This is an organization that for years has been lauded and referred to as “undervalued” by many, solely to then defy these assumptions and steerage by dropping additional. My positions in utilities like Enel (OTCPK:ENLAY) are up this yr, in addition to delivering important total dividends.

TAC isn’t up – neither is it delivering a “great” dividend, on the present 2% yield. The corporate trades each on the NYSE and the TSX, and on this article, I am going to undergo it as a possible long-term funding.

It ought to be talked about that whereas the corporate isn’t an excellent yielder, it is truly dividend grower – the final bump was lower than 3 weeks in the past and got here at a 9.1% price.

So, let’s have a look at what TransAlta affords us and what could be anticipated for the long run right here.

TransAlta Company – Double-digit destructive returns for 2023 to date

The corporate is, as implied above, down greater than 10% this yr to date. This could not essentially be thought-about reflective of the corporate’s fundamentals, as a result of these are extra strong than you would possibly count on.

This can be a enterprise with a $3.5B market cap and a $8.7B EV with 1,280 workers. The corporate can be one of many oldest utilities in all of Canada with a 6,400 MW portfolio with diversified producing amenities not solely in Canada however within the US and Australia as properly.

That is additionally an organization that generates upwards of $900M of FCF, regardless of what you are at present seeing within the firm’s quarterly traits. TransAlta alone can be accountable for over 30M tonnes of emission reductions since 2005, which is a full 10% of Canada’s goal.

You possibly can see, due to this fact, that the corporate is a clear vitality enterprise with a deal with generational belongings in Hydro, Photo voltaic/Wind, and Gasoline, in addition to companies in Vitality advertising and pipeline and developments.

Since 2021, this firm has made giant leaps of enhancements. TAC has put in 800 MW of wind and photo voltaic, and one other 2,700 MW within the growth pipeline. The identical quantity, 800 MW, of thermal era has been retired in the identical time. Additionally, this has been executed throughout a time when the corporate has not seen decrease or worse earnings, however higher outcomes.

TAC IR (TAC IR)

Based on TAC, the corporate has giant alternatives within the transition to electrification. Decarbonization is shifting ahead, and this requires important funding from market-leading gamers as a way to be met.

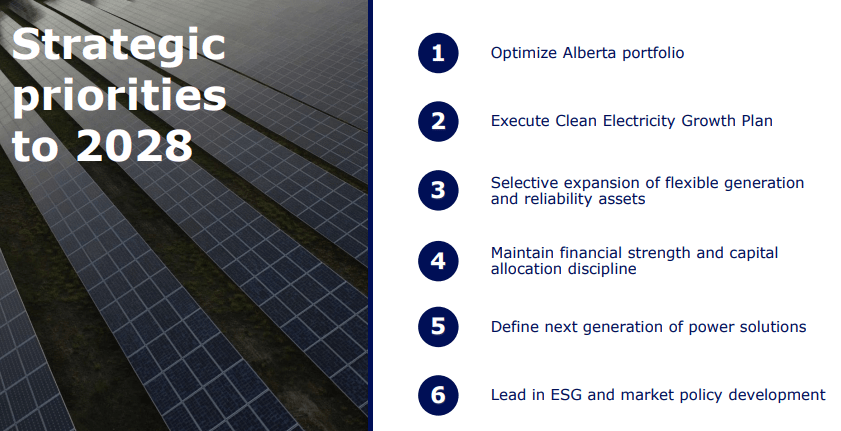

To this finish, the corporate has the next priorities till the 2028E fiscal.

TAC IR (TAC IR)

This plan includes one other 10,000 MW of fresh electrical energy from $3.5B of development CapEx that’ll add $350M to the corporate’s annual EBITDA, which might put the corporate at above $1B per yr. The main target right here might be onshore wind, photo voltaic, storage, and hybrid options, and optimizing the legacy Alberta combine to maximise firm money movement.

Actually the corporate already expects to hit that billion in adjusted EBITDA for the subsequent fiscal, at a steerage of $1.15B and $1.3Bn and one other $450-$600M value of FCF.

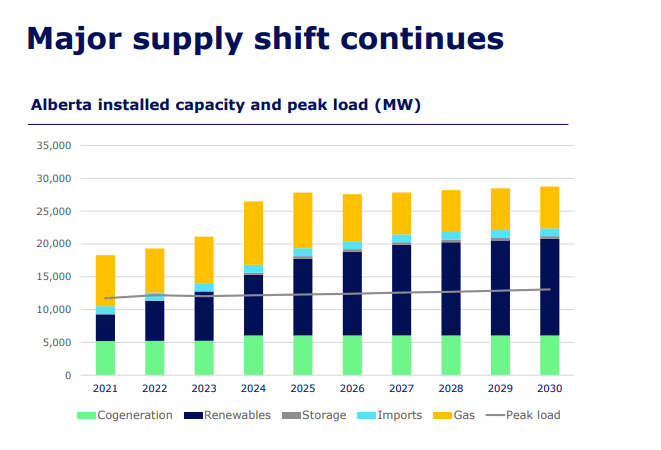

Nevertheless, the corporate has not too long ago paused the event of renewables in Alberta, in response to land use, system reliability, and reclamation considerations, anticipated to be in place not less than till February to make sure that sufficient time is given for regulatory opinions. There’s a important shift anticipated in Alberta particularly that can massively cut back the fuel combine within the firm’s era. Have a look.

TAC IR (TAC IR)

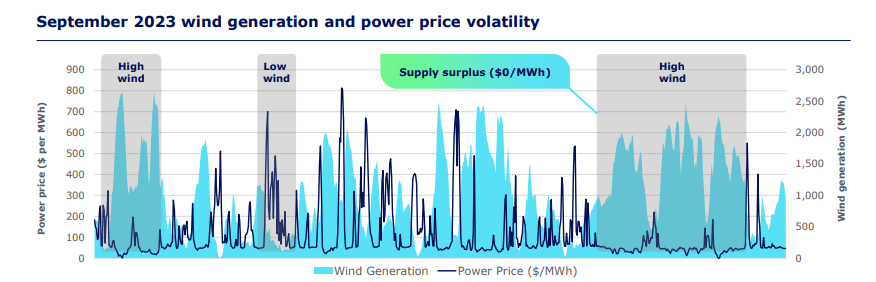

The principle problem for the corporate is the anticipated worth on a per-MWh foundation. Provide traits are anticipated to melt this worth within the subsequent 2-3 years earlier than it climbs again as much as across the 2021-2023 stage on the finish of this decade. In fact, apart from the associated fee challenges, the corporate additionally must navigate the challenges in output that wind and photo voltaic carry to the desk – these types of era are inclined to hour-to-hour modifications that must be thought-about – and that is difficult the reliability of the system, which can be the rationale for the present regulatory pause.

Wind particularly will enhance the volatility in worth – this has been confirmed over time.

TAC IR (TAC IR)

This implies TAC is positioning itself with a excessive diversification of belongings, each in Wind, Hydro, Storage, Gasoline, and different sectors. Thermal fuel particularly is a required “compensator” when renewable sources are on the low facet.

The corporate applies a complete hedging technique, with many of the manufacturing for 2024 already hedged by way of pricing, and over half of the 2025E already hedged as properly.

3Q23 is the newest set of operational outcomes we have now to contemplate right here. These had been constructive, with important $450M+ EBITDA on an adjusted foundation, and over $ 225M value of FCF with availability of just about 92% for the grid. TAC additionally continues to have entry to simply south of $2B value of liquidity.

The corporate has a number of high-value initiatives within the pipeline.

TAC IR (TAC IR)

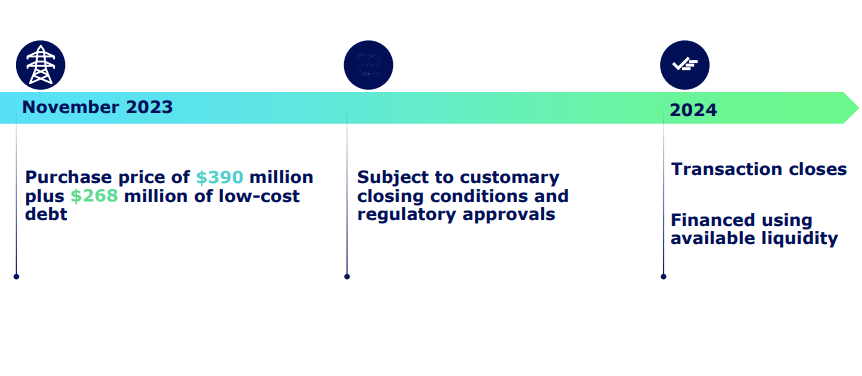

The present growth pipeline requires bringing a complete goal of 5,000 MW by 2025E. The corporate is at present the truth is on monitor to beat this goal. There are some information on the M&A entrance, with the Heartland transaction at a 5.5x A number of with a really enticing EBITDA contribution on an annual foundation, however extra importantly, this transaction provides versatile capability to the corporate’s portfolio with a 55% share of contracted income.

TAC IR (TAC IR)

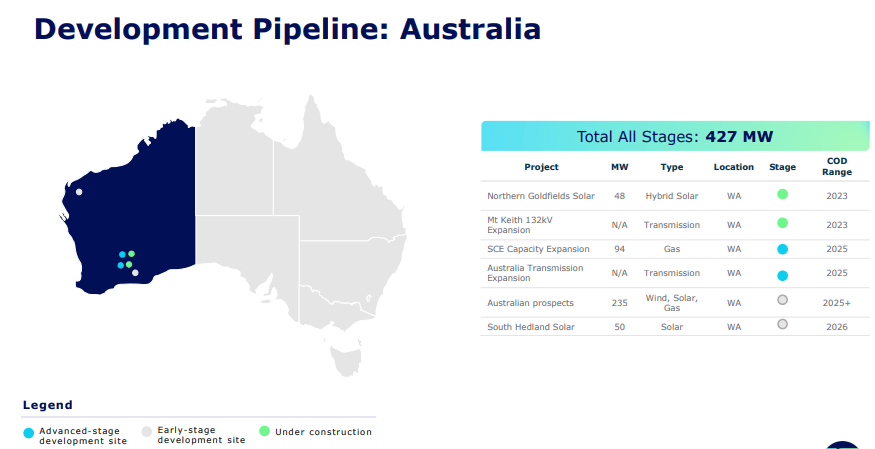

The corporate is not simply growing within the US both, however has important developments within the US, with initiatives all the way in which till 2027 and past. In Canada, the corporate’s fundamental point of interest is clearly Alberta, the corporate’s core, and in Australia, the corporate’s focus is on the western a part of the nation.

TAC IR (TAC IR)

Going ahead, I count on TAC to proceed to have the ability to develop and execute on its initiatives, and I do not see any operational points that may be trigger for considerably elevated dangers that aren’t already talked about.

Let’s make clear this within the Threat & Upsides to the corporate.

Dangers & Upside

The principle danger that I see to TA/TAC within the subsequent few years is the mix of pricing and era uncertainity as the corporate switches to a much more risky total combine. Sustaining versatile percentages of belongings can solely accomplish that a lot when, as you may see within the footage above, among the elementary ups and downs in complete generations are depending on very clear traits – that means both wind or sunshine. This isn’t only a danger to TA/TAC however to all corporations energetic on this business.

Along with this, elementary dangers to the corporate do exist, albeit minor (as I see it). The corporate isn’t IG-rated, however solely BB+, and has a long-term debt/cap of just about 61%, which is considerably elevated right here. These are actually the 2 fundamental dangers.

The upside to the corporate may be very strong return and profitability metrics. The draw back is sub-par debt and leverage metrics, with an curiosity protection of lower than 4x (although that is truly good in comparison with the place TAC has been traditionally).

Valuation

To state this very clearly, I consider the corporate goes into a number of years of comparatively destructive operational traits, that means earnings. I consider earnings will truly be declining for so long as we see decrease costs on a MWh foundation, and I consider the indicators are clear that that is going to be occurring within the subsequent few years, not less than till 2025E-2026E.

Why is that this the case in Canada particularly?

As a result of there’s loads of competitors coming to the markets, and there are few modifications thought-about. RRO might be declining in each 2024-2025E and present expectations are for these costs to normalize to the degrees seen throughout 2020 – if not precisely at these low cost ranges.

I would watch out estimating the corporate at any kind of huge upside within the close to time period. The analysts following TransAlta have been anticipating the corporate to attain $15-$17/share for the Canadian ticker for over a year- the corporate has the truth is gone in the other way. S&P International targets for the corporate and the primary TSX ticker vary from $12/share to $18/share with a mean of $15. Nevertheless, even though each single goal by each single analyst is not less than $1.2/share increased than the present share worth, solely 2 analysts out of 9 at present think about this enterprise to be a “BUY”. That is weak conviction, or not less than plenty of uncertainity on the operational facet.

I might say, typically talking, you are higher off investing within the firm’s desire shares and debt devices. The reason being the operational uncertainity that can play into the widespread share valuations for the foreseeable future. Many of those prefs are yielding between 4.5-6% right now, making them first rate choices for those who’re taking a look at earnings investments, particularly for those who think about the resets which might be in impact for a few of them.

I do not see particular particular person benefits on account of its operational diversification, on condition that geographic diversification additionally will increase the prices of compliance, FX and different issues.

Due to these components, I at present think about the corporate to be a conservative “HOLD”, however near a possible entry level the place the minimal worth of $12/share would imply a double-digit annual RoR.

Right here is my introductory thesis for this firm.

Thesis

- TransAlta is among the main renewable gamers in Canada, with a robust era profile with each Canadian, Australian, and American publicity. Its combine is well-prepared for the challenges which might be more likely to are available the long run, and I count on this firm’s upside and fundamentals to develop positively over the long run.

- Brief-term, I count on stress from decrease RRO and energy costs in Canada which at present appear more likely to backside throughout the subsequent 2-3 years. Whereas I consider that the corporate affords an interesting entry level at an inexpensive worth – together with this one – there’s a multitude of danger components that also make this one a little bit of a doubt for me.

- I would say I wish to enter the corporate beneath $10.5/share to be secure, and this makes the corporate a “HOLD” right here. The corporate has a robust historical past of premiumization by way of worth targets, and it has by no means reached the heights anticipated – not for the previous few years not less than.

Keep in mind, I am all about :1. Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly huge – corporations at a reduction, permitting them to normalize over time and harvesting capital beneficial properties and dividends within the meantime.

2. If the corporate goes properly past normalization and goes into overvaluation, I harvest beneficial properties and rotate my place into different undervalued shares, repeating #1.

3. If the corporate does not go into overvaluation, however hovers inside a good worth, or goes again all the way down to undervaluation, I purchase extra as time permits.

4. I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed below are my standards and the way the corporate fulfills them (italicized).

- This firm is total qualitative.

- This firm is essentially secure/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is at present low cost.

- This firm has a practical upside primarily based on earnings development or a number of growth/reversion.