grandriver

Last April, I began protection of Transocean (NYSE:RIG) inventory with a “Hold” ranking, saying that whereas the day charges had been enhancing that its debt load was a difficulty. The inventory is down over -20% since then versus an over 20% achieve within the S&P. Extra not too long ago, in September, I mentioned its deleveraging story has changing into clearer, however its valuation and indebtedness in comparison with friends made it a excessive threat/reward inventory. The inventory is down -40% since that write-up. With the corporate not too long ago reporting its This autumn outcomes, let’s compensate for the title.

Firm Profile

As a reminder, RIG owns a fleet of drillships and semisubmersibles that offshore drillers contract out. Drillships are deployed in calmer seas, whereas semisubmersibles are use in harsh sea circumstances.

The corporate owned 37 vessels on the finish of 2023 with a mean age of about 11 years. It had 29 ultra-deep water vessels and eight harsh setting vessels in its fleet. 25 of its vessels are working, 11 are cold-stacked, and one is beneath development.

This autumn Outcomes and 2024 Outlook

One of the crucial necessary issues for RIG continues to be day charges. The trade and RIG got here beneath excessive strain between 2014 by means of the pandemic when day charges stayed low. Nonetheless, charges have been recovering since 2021.

For its This autumn reported in late February, RIG noticed its common day charge climb 24% 12 months over 12 months to $432,000 per day, up from $349,000 per day a 12 months in the past. In Q1, its common day charge was $391,000.

Extra importantly, RIG mentioned that based mostly on its present backlog, it expects its common day charges for Q1 2024 to be $433,000 per day. That may be a 19% improve in comparison with present ranges.

Total, RIG noticed its contract income climb 22% 12 months over 12 months, and 4% sequentially, to $741 million. Analysts had been in search of income of $741.2 million.

Working and upkeep prices climbed 35% to $569 million from $423 million, and had been up 9% quarter over quarter.

Adjusted EBITDA fell -13% to $122 million, and was down -25% sequentially.

Adjusted EPS was a lack of -9 cents in comparison with -48 cents a 12 months in the past and -36 cents in Q3.

The corporate generated $98 million in working money stream within the quarter. Free money stream was -$122 million. It generated $164 million in working money stream for the 12 months, with free money stream of -$263 million.

Turning to its stability sheet, RIG ended 2023 with $7.41 billion in debt and money of $762 million. That may equate to leverage of about 9x on the $738 million in adjusted EBITDA it produced in 2023

RIG famous that it continues to see contract durations improve. It not too long ago contracted out a vessel within the Romanian Black Sea for a minimal period of 540 days, with a day charge of $465,000 per day, which can go as much as $480,000 per day after the preliminary time period.

The corporate additionally famous that the U.S. Gulf market, which has traditionally seen quick lead instances and quick period contracts is beginning to transfer to longer lead instances and longer period contracts.

Trying forward, the corporate guided for Q1 income of about $780 million. It expects working and upkeep expense to be roughly $545 million and G&A bills of $47 million.

For the total 12 months, the corporate is projecting income of between $3.60-$3.75 billion. That is down from an earlier forecast calling for 2024 income of between $3.7-3.9 billion projected in October. The corporate mentioned the lowered steering was as a result of delayed contract commencements for 3 vessels brought on by extended mobilization and contract preparation actions.

On the expense aspect, it’s anticipating O&M bills to be round $2.2 billion, G&A to roughly $196 million, and curiosity expense to be $513 million. CapEx is projected to be $242 million.

On its Q4 earnings call, CEO Jeremy Thigpen mentioned:

“Our fleet is largely contracted through 2024, and we will continue to actively seek work to fill any gaps in utilization. Having said that, our $9 billion backlog and superior assets provide us with the competence and flexibility we need to be selective in the opportunities we pursue as we constantly endeavor to strike the right balance between utilization and day rate optimization. As previously mentioned, we’re encouraged by the longer-term programs we see materialize with start dates well into the future. As we move into 2024 and further into what appears to be a sustained upcycle, our priorities remain, first, converting our industry-leading backlog to cash. We’ll do this by maintaining acute focus on safety and the uptime performance across our fleet, which directly impacts our overall revenue efficiency. Second, deleveraging the balance sheet. Assuming the market materializes, as we expect, we will generate significant free cash flow over the next few years. And while we recognize that operating a growing fleet is a competing priority with deleveraging, we will be sure to balance the two in a manner that best serves our shareholders Third, and finally manage the business with the ultimate goal of returning more value to our shareholders, either through share repurchases or dividends.”

RIG continues to learn from the rebound in day charges, whereas longer contract durations ought to start to provide it extra visibility. Nonetheless, working and upkeep prices have additionally been skyrocketing, and its working money stream has been comparatively modest.

With practically $7 billion in internet debt and 9x leverage, the corporate must generate substantial money to pay down its debt and begin to deleverage. With the capex spent on constructing a brand new vessel, the corporate disappointingly wasn’t in a position to make any dent in its debt load final 12 months, regardless of a a lot improved setting and better day charges.

Decreasing income steering, with no change is expense steering, additionally isn’t nice for a corporation in its debt place.

Valuation

RIG inventory presently trades at practically 9x the 2024 consensus EBITDA of $1.24 billion and 6.7x the 2025 consensus of $1.63 billion.

It trades at a ahead P/E of 12.3x the 2025 consensus of 42 cents. Adjusted EPS is predicted to 1 cent in 2024.

It is projected to develop income by practically 29% this 12 months and about 12% in 2024.

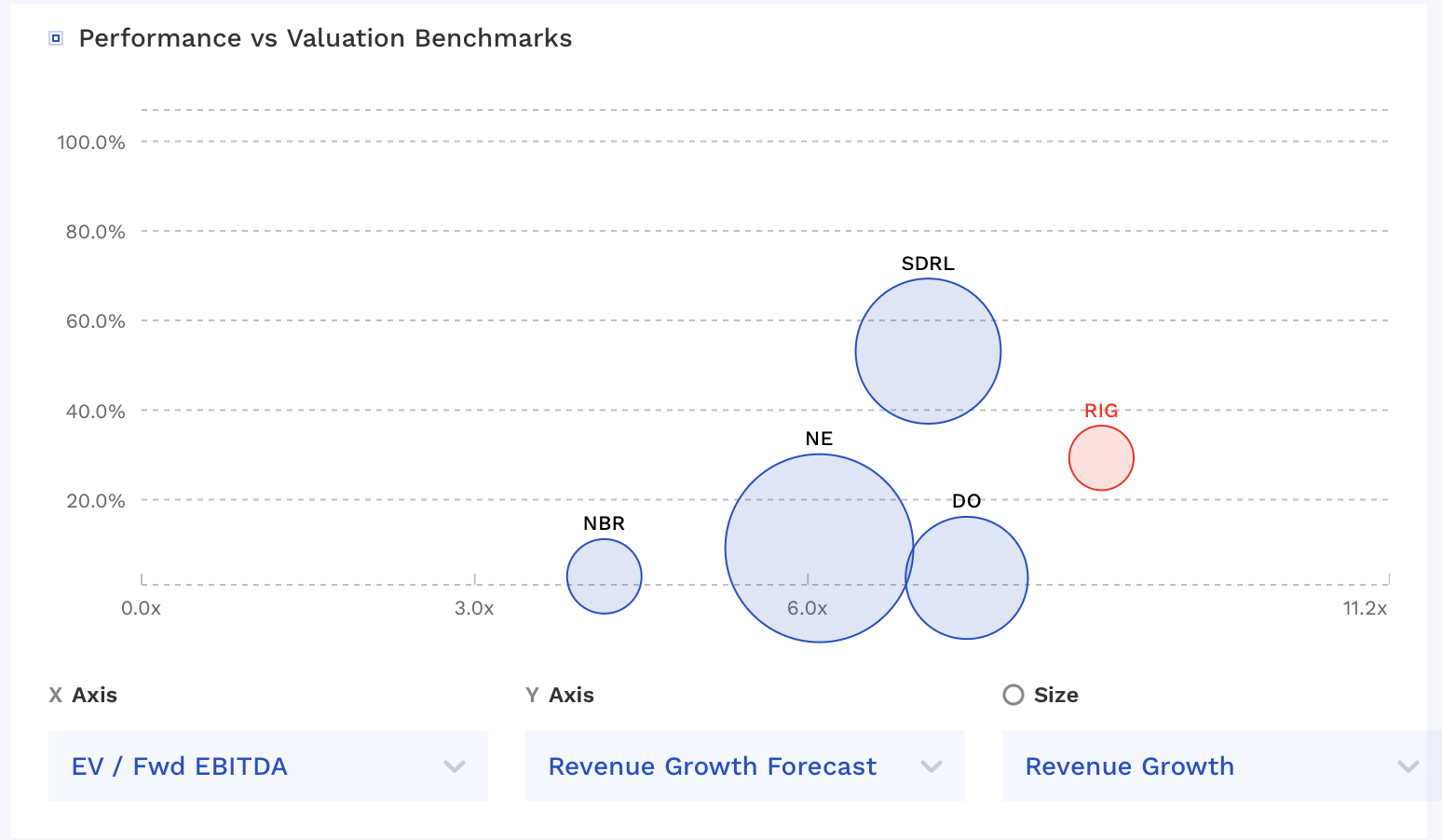

RIG is without doubt one of the dearer shares amongst its friends, and has the next debt/fairness degree than most of its friends.

RIG Valuation Vs Friends (FinBox)

For RIG shares to extend in worth, the corporate actually wants to scale back debt by means of producing free money stream. Proper now, for 2024 it seems like it will likely be in a position to generate free money stream of between $450-500 million. That may transfer leverage down to shut to 5x on the finish of 2024, after which a stronger 12 months in 2025 might see debt lowered by presumably $1 billion in 2025 based mostly on larger EBITDA estimates (helped by stronger day charges and a full 12 months of a brand new ship) and fewer capex. That may deliver leverage right down to a extra cheap 3.3x. Hold a 7x a number of on 2025 EBITDA estimates, and you’ve got an $8 inventory.

Conclusion

The trail for deleveraging for RIG stays over the following two years. Nonetheless, the corporate has proven that the journey will not be a clean one. It should additionally must proceed to see day charges stay sturdy and for it to get its O&M bills in verify.

2024 is an enormous 12 months for RIG, and to this point, it’s not off to a great begin. Nonetheless, if it will possibly begin to reactivate its cold-stack rigs in some unspecified time in the future this 12 months and get them into service, that would shift the narrative on the corporate.

RIG stays a excessive risk-reward inventory. I see good upside potential if issues go as deliberate, however on the identical good, if the market turns it might be a zero given its debt load. I lean extra in direction of the deleveraging story working right now, however acknowledge the massive threat related to the title. As such, I proceed to charge the inventory a “Hold.”