da-kuk

Tremendous Micro Laptop, Inc (NASDAQ:SMCI), or “SMCI,” just lately had an “Nvidia moment,” as shares surged by 35% after the corporate raised its quarterly guidance significantly. Because of its market-leading place within the AI {hardware} section, SMCI continues to extend gross sales and profitability a lot sooner than anticipated. Tremendous Micro’s earnings are scheduled to be revealed on January 30, and offered SMCI’s stellar pre-announcement, the outcomes ought to be significantly better than beforehand thought.

Additionally, SMCI’s current outperformance means that many analysts could must revise future estimates to maintain up with Tremendous Micro’s stellar progress. Moreover, resulting from SMCI’s doubtless future outperformance, its valuation remains to be comparatively cheap. As a number one {hardware} provider for the AI section, SMCI ought to proceed increasing gross sales and rising profitability, resulting in the next inventory value in future years.

Joyful To Have Elevated My Stake

I highlighted SMCI just lately, as I had a suspicion about it reporting significantly better than anticipated this quarter.

SMCI spotlight (The Monetary Prophet )

The subsequent day, I elevated my SMCI place by 50%, and the next day, the inventory skyrocketed by 35% resulting from its “Nvidia moment.” I offered coated name choices towards 33% of my stake, and I’ll promote extra coated name choices if the parabolic value motion continues. I stay bullish on SMCI long run regardless of the chance of a near-term pull-back/consolidation.

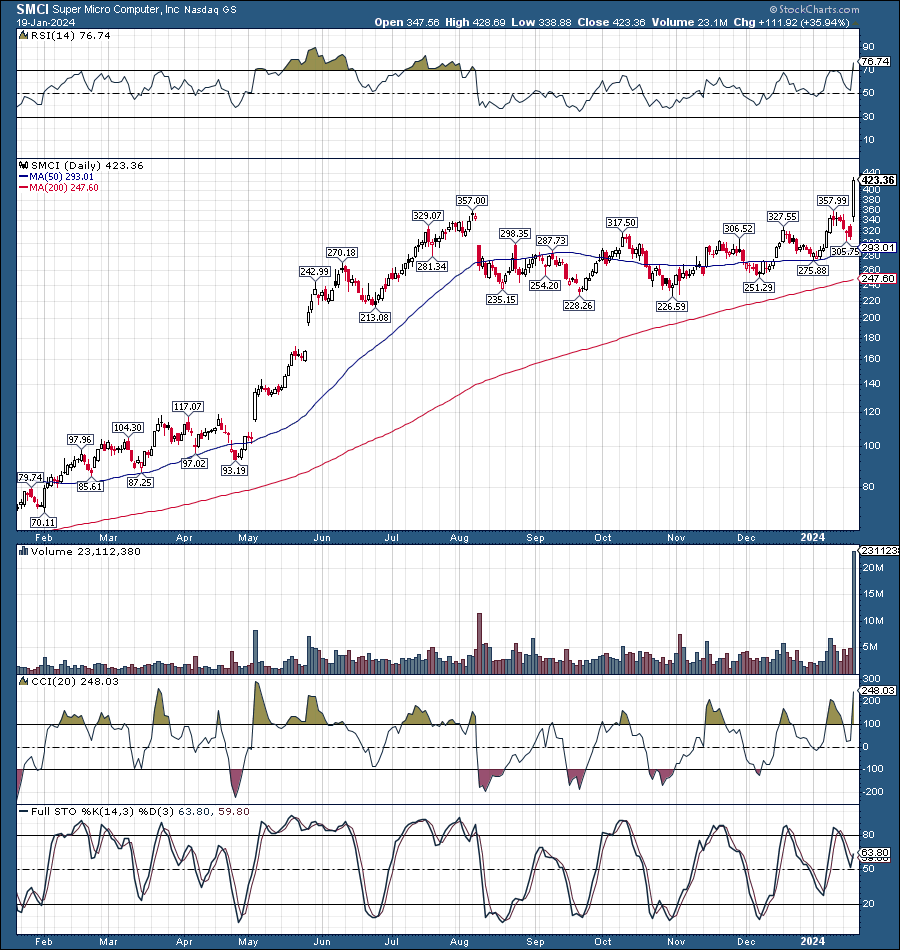

Technically – The Breakout To New Highs

SMCI (StockCharts.com)

Technically, SMCI consolidated for a really very long time. Furthermore, the worth remained low-cost relative to SMCI’s progress and profitability potential. Moreover, about 9% of SMCI’s shares had been offered earlier than its Nvidia second. Brief-covering doubtless exacerbated the current spike and should proceed to contribute right here within the close to time period. Now that we have seen file quantity and the RSI approaching 80, we may see a consolidation/pullback section, particularly post-earnings. Nonetheless, SMCI stays a prime “buy the dip” alternative as we advance within the coming months.

The AI Growth is Right here

The AI increase is right here, and Tremendous Micro’s prime and backside traces proceed to broaden extra quickly than anticipated. Tremendous Micro expects fiscal Q2 revenues of $3.6-$3.65 billion, a lot larger than the $2.7-$2.9 billion prior vary. This ultra-bullish dynamic illustrates that SMCI’s income might be about 32% larger than consensus estimate expectations.

Furthermore, the up to date EPS vary steering is about $5.50, a lot larger than the earlier vary of $4.40 to $4.88. The up to date steering is way larger than the consensus estimate figures for gross sales of $2.84B and revenue per share estimate of $4.55. Tremendous Micro stated it was raising its guidance because it noticed a robust market and finish buyer demand for its rack-scale, AI, and complete IT options.

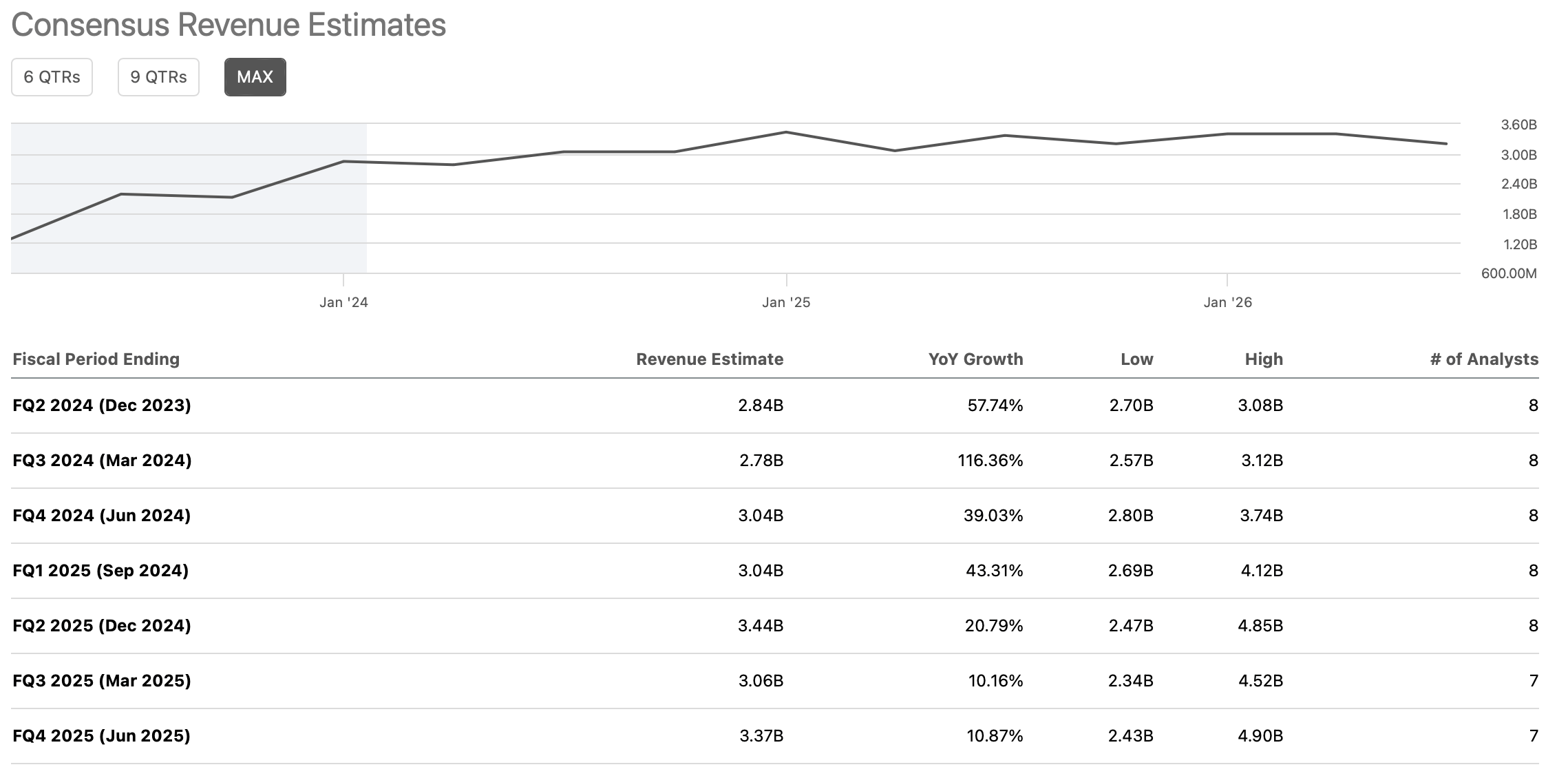

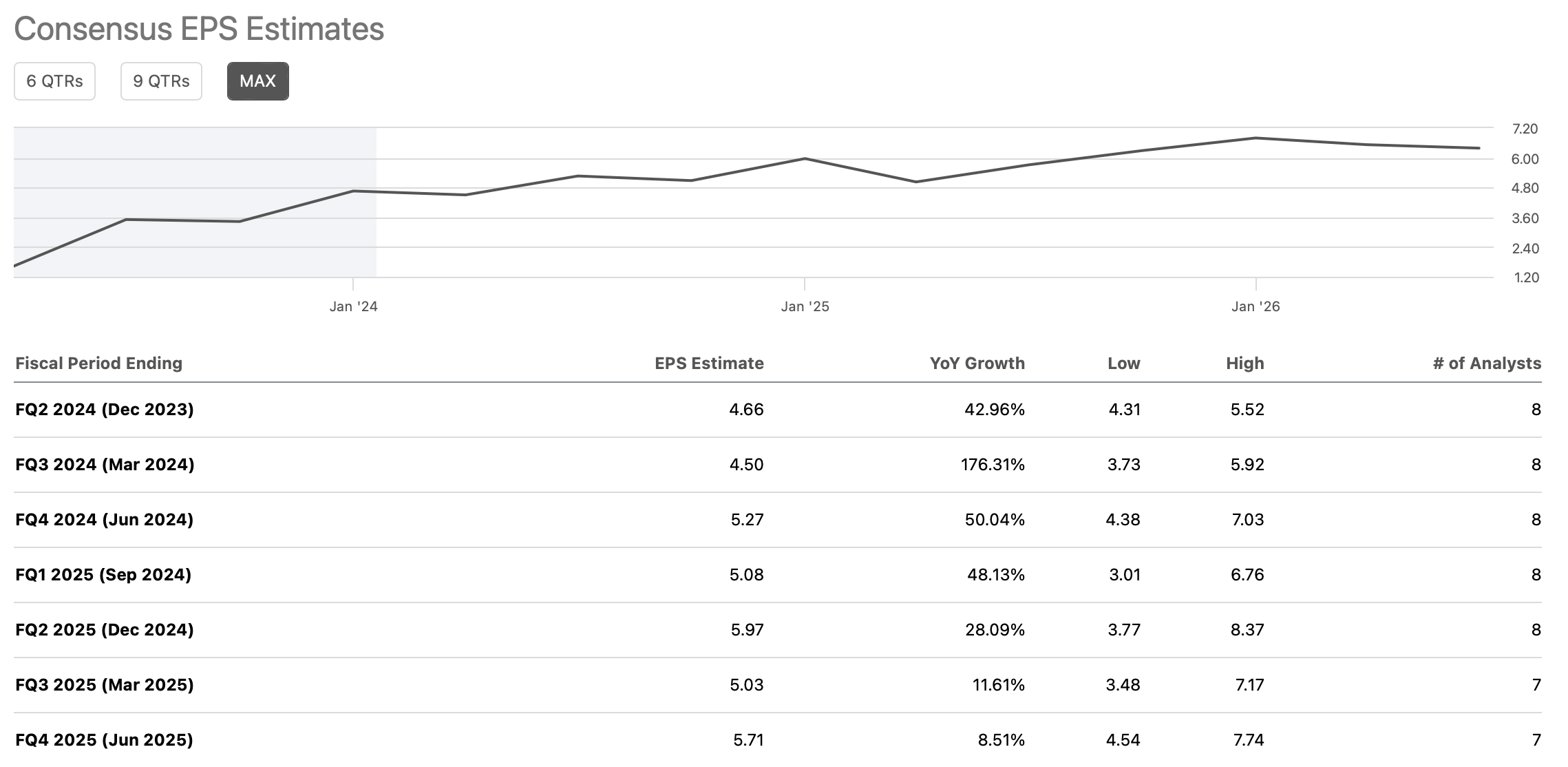

SMCI’s Gross sales Rising Sooner Than Anticipated

Gross sales estimates (SeekingAlpha.com )

SMCI’s gross sales ought to are available in about 32% above the consensus estimates, suggesting that future estimates are too low. The earlier fiscal Q2 income vary was $2.7-$3.08 billion. Nevertheless, SMCI stated it might ship round $3.6-$3.65 billion as an alternative. This dynamic illustrates huge outperformance and means that future income estimates have to be revised larger to replicate the stellar gross sales progress potential of Tremendous Micro.

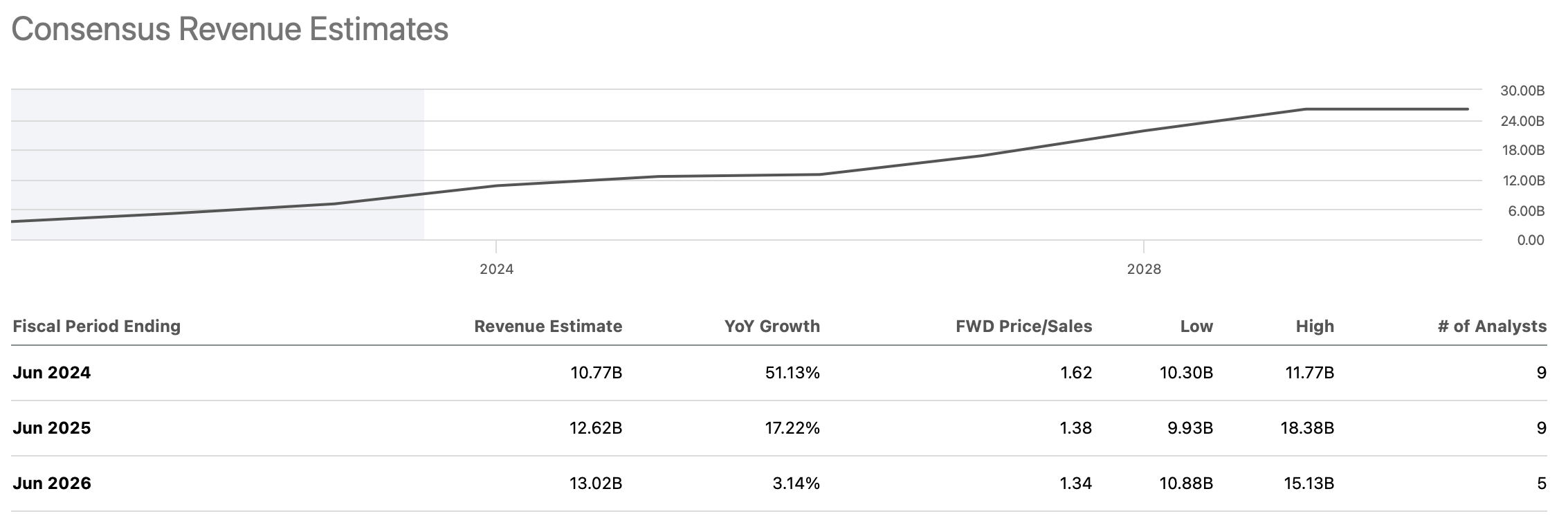

Tremendous Micro – Even Cheaper Than It Appears

Gross sales estimates (annual) (SeekingAlpha.com )

This 12 months’s (fiscal 2024) income estimate vary was $10.3 to $11.77 billion, however given the huge income steering improve, we may see fiscal 2024 gross sales round $13-$14 billion if the outperformance continues in future quarters. Additionally, we may see significantly larger than anticipated revenues within the coming years, illustrating that Tremendous Micro is cheap right here. Due to this fact, SMCI’s ahead P/S a number of is probably going round 1-1.2 as an alternative of the 1.5-1.6 vary.

Profitability To Develop Significantly

EPS estimates (SeekingAlpha.com )

SMCI’s up to date EPS steering is $5.40-$5.55. Due to this fact, SMCI may obtain higher-end estimates or larger for fiscal Q2. Moreover, SMCI may obtain higher-end estimates in future quarters, implying its EPS could possibly be a lot larger than anticipated as we advance. Supplied SMCI continues reaching higher-end figures, it may earn round $20-$22 in EPS in fiscal 2024.

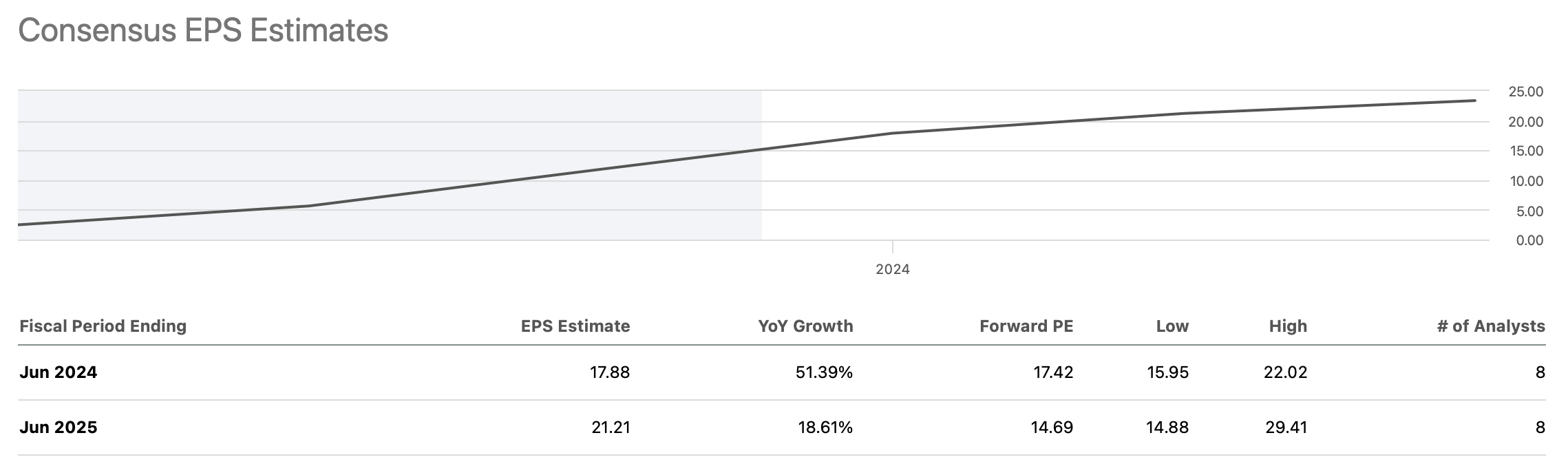

Tremendous Micro’s EPS Estimates Are Too Low

EPS estimates (annual) (SeekingAlpha.com )

As an alternative of the projected $17.88 in EPS, SMCI may obtain round $21 as an alternative. This dynamic illustrates that SMCI’s ahead (fiscal 2024) P/E ratio could solely be round 21.4 right here. Furthermore, SMCI’s EPS could possibly be significantly larger than the projected $21.21 consensus estimate for 2025. Tremendous Micro may proceed outperforming, attaining round $27-$29 in EPS in fiscal 2025. This situation illustrates that SMCI could also be buying and selling round 16 instances ahead (fiscal 2025) earnings now, which is exceptionally low-cost for a corporation in SMCI’s market-leading place with substantial progress forward.

The place Tremendous Micro’s inventory could possibly be sooner or later:

| Yr (fiscal) | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

| Income Bs | $13 | $17 | $21.7 | $24 | $28 | $31 | $34 |

| Income progress | 85% | 31% | 22% | 17% | 15% | 12% | 10% |

| EPS | $21 | $28 | $34 | $40 | $46 | $52 | $58 |

| EPS progress | 87% | 33% | 21% | 19% | 15% | 13% | 12% |

| Ahead P/E | 18 | 19 | 20 | 21 | 20 | 19 | 18 |

| Inventory value | $504 | $646 | $800 | $966 | $1040 | $1100 | $1240 |

Supply: The Monetary Prophet

Dangers to Tremendous Micro

Regardless of my bullish projections, SMCI faces dangers. First, there may be the chance of competitors, as SMCI isn’t alone in its area. Second, there may be the chance of decrease margins, as SMCI is on the {hardware} aspect of AI, and intense competitors could result in margin compression in time. Additionally, there are macroeconomic components to contemplate, corresponding to a attainable financial slowdown and AI. There are considerations that SMCI’s progress could peak, resulting in stagnant or decrease EPS after its AI rise. Traders ought to contemplate these and different dangers earlier than investing in SMCI.

![International Web Entry and Utilization [Infographic]](https://whizbuddy.com/wp-content/uploads/2024/04/bG9jYWw6Ly8vZGl2ZWltYWdlL3dvcmxkX2ludGVybmV0X3VzYWdlMi5wbmc.webp-600x385.webp)