shih-wei

By Pierre Debru

Equities completed the yr with a really robust fourth quarter. International equities gained 11.4% over the past three months to shut the yr with a 23.8% optimistic efficiency. The reducing of the “higher for longer” charges’ fears and the awakening of small-cap shares after three quarters of lackluster efficiency helped shares edge greater. General, markets completed the yr specializing in upcoming price cuts; mixed with lowering inflation, this led to a reversal of the adverse temper noticed in Q3.

This installment of the WisdomTree Quarterly Fairness Issue Evaluate goals to shed some gentle on how fairness elements behaved throughout this reversal and the way this will have impacted traders’ portfolios.

- General high quality and development continued to dominate, however small cap joined the occasion this quarter. Within the U.S. and Europe, small caps even posted the strongest outperformance.

- Excessive dividend, worth and min volatility posted the most important underperformance, affected by the markets’ pivot to optimism.

- In rising markets, the image remained a bit completely different from the remainder of the world, with most elements outperforming. Solely momentum and min vol posted underperformance. High quality posted the strongest returns.

Trying to 2024, the fairness outlook stays optimistic however fairly unsure. It seems price cuts are coming, however a notable deterioration in financial information and continued disinflation could also be required to validate expectations for vital coverage easing in 2024 and to help fairness markets. With non-dividend payers having benefited from an distinctive run over the past decade in comparison with high-dividend payers, 2024 might even see a web growth of the breadth of the market, resulting in some imply reversion in favor of dividend payers. This might play a vital position within the efficiency of high quality within the yr forward, pushing high-quality dividend-growing shares to outperform high-quality tech shares.

Efficiency in Focus: A Shocking Bull Run for This fall

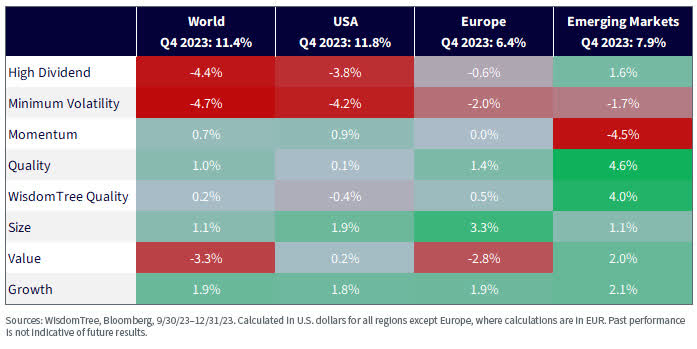

In This fall, MSCI World (+11.4%) and MSCI USA (+11.8%) carried out very strongly. European and rising markets equities had been weaker, however nonetheless returned excessive single-digit efficiency. General, Tech megacaps continued to steer, however the market’s breadth elevated, with small caps within the U.S. and Europe performing fairly strongly.

General, This fall ended up fairly optimistic to issue investing:

- In international developed markets, development and high quality posted the strongest returns, in step with the remainder of the yr. Small cap completed third in a late revival after three quarters of lackluster efficiency.

- Within the U.S. and Europe, small caps posted the strongest outperformance, adopted by development. High quality carried out nicely in Europe, ending third, however within the U.S., momentum grabbed the third place.

- General, in developed markets, excessive dividend, min volatility and, to a smaller extent, worth suffered the majority of the underperformance.

- In rising markets, high quality and momentum dominated, however like in earlier quarters, most elements had been capable of produce outperformance over the quarter. Momentum was the standout loser within the area.

Determine 1: Fairness Issue Outperformance in Q3 2023 throughout Areas

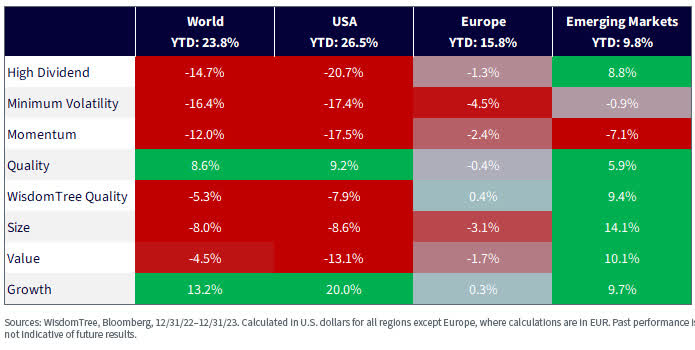

2023 in Evaluate

Trying again on the full yr, development remained the clear winner in developed and U.S. equities with double-digit outperformance versus the market. In each areas, solely high quality managed to comply with its lead, outperforming by virtually 10% in each markets. All the opposite elements underperformed, with excessive dividend, min vol and momentum posting massive underperformance.

In Europe, high quality and development additionally dominated the opposite elements however posted solely minor outperformance. Minimal volatility and small caps had been the standout losers in that area.

In rising markets, all elements however momentum and min volatility did fairly nicely in 2023. Small cap posted the strongest returns, adopted by worth and high quality.

Determine 2: Fairness Issue Outperformance in 2023 throughout Area

Is It Time for the Revenge of the Dividend Payers?

Analysis has proven that throughout markets, over the long run, big-dividend payers are inclined to outperform low-dividend payers or firms that don’t pay dividends in any respect. Nonetheless, after the robust outperformance of Tech megacaps, together with many non-dividend payers in 2023 and over the past decade on the whole, information from Dartmouth’s Ken French exhibits that over the past 20 years, the businesses that paid no dividend outperformed the quintile that paid the best dividends by the most important quantity on file. Assuming some imply reversion, this might level to some resurgence of dividend payers.

That is of specific curiosity when wanting on the high quality issue. High quality continued to do nicely over the yr, however over the past two years, we now have noticed a powerful divergence in conduct between high-quality firms that pay dividends and those who don’t. In 2022, the standard dividend payers dominated, whereas the standard non-dividend payers did higher in 2023.

To take a look at the influence of that divergence on “investable” portfolios, we take into account:

- The MSCI USA High quality Index, which presently allocates a big proportion of the portfolio to Tech and high-quality, non-dividend-paying firms

- The WisdomTree U.S. High quality Dividend Progress Index, which focuses on high-quality, dividend-growing firms and, due to this fact, invests solely in dividend-paying firms, resulting in smaller allocations to Tech and the Magnificent Seven.

In determine 3, we observe that MSCI USA High quality, following the robust rally of Tech and the Magnificent Seven in 2023, is traditionally costly in comparison with the market. Quite the opposite, with a reduction of -2, the WisdomTree U.S. Quality Dividend Growth is presently fairly low-cost and getting cheaper.

Determine 3: Historic Worth-to-Incomes Ratio Premium/Low cost vs. the MSCI USA Index

Taken collectively, this might point out that prime high quality with a dividend tilt might be poised to take the lead in 2024.

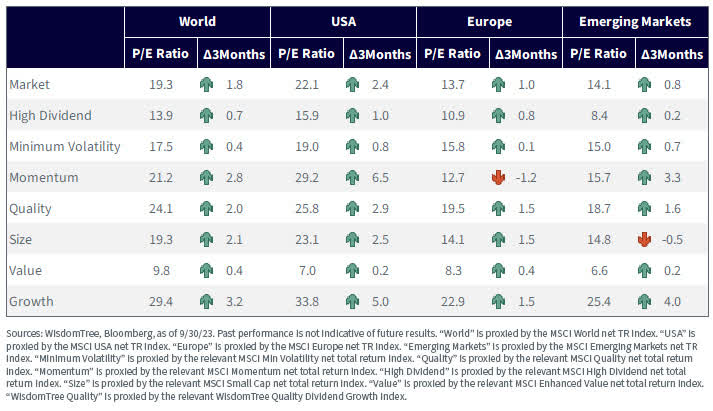

Valuations Elevated in This fall

In This fall 2023, developed markets obtained dearer following the sharp rally. All elements noticed the price-to-earnings ratio enhance over the quarter, aside from momentum in Europe. Progress noticed the most important enhance throughout areas on common. Small caps and momentum comply with simply behind. In rising markets, valuations elevated throughout most elements bar small caps.

Determine 4: Historic Evolution of Worth-to-Earnings Ratios of Fairness Elements

Trying Ahead to 2024

The fairness outlook stays optimistic however fairly unsure. It seems price cuts are coming, however a notable deterioration in financial information and continued disinflation could also be required to validate expectations for vital coverage easing in 2024 and to help fairness markets. With non-dividend payers having benefited from an distinctive run over the past decade in comparison with high-dividend payers, 2024 might even see a web growth of the breadth of the market, resulting in some imply reversion in favor of dividend payers. This might play a vital position within the efficiency of high quality within the yr forward, pushing high-quality dividend-growing shares to outperform high-quality tech shares.

Pierre Debru is an worker of WisdomTree UK Restricted, a European subsidiary of WisdomTree Asset Administration Inc.’s dad or mum firm, WisdomTree, Inc.

Editor’s Observe: The abstract bullets for this text had been chosen by Looking for Alpha editors.