D3Damon/iStock by way of Getty Photographs

Taiwan Semiconductor Manufacturing Firm Restricted (NYSE:TSM) is a semiconductor foundry, which implies it manufactures chips for different firms like Superior Micro Gadgets, Inc. (AMD) and NVIDIA Company (NVDA). AMD and Nvidia, on the opposite hand, are fabless semiconductor firms that design and promote their very own chips however outsource the manufacturing to foundry TSMC.

As a result of TSMC’s income is derived from manufacturing providers for varied firms, together with AMD and Nvidia, its income development might indirectly correlate with the income development of its prospects. Elements comparable to general semiconductor market demand, TSMC’s manufacturing capability, and the competitiveness of its know-how nodes can all influence TSMC’s income efficiency relative to its prospects.

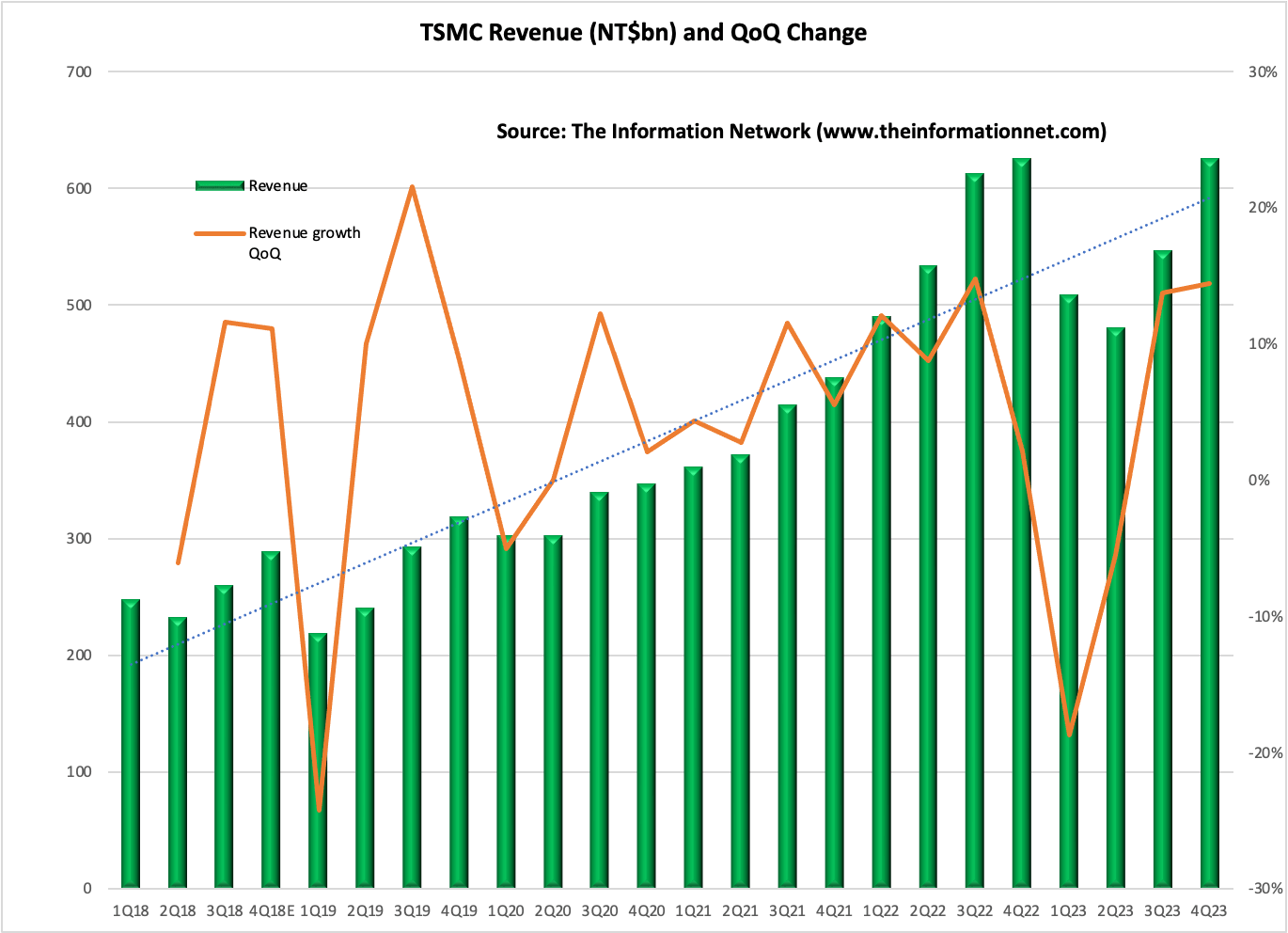

Certainly, in 2023 in the course of the downturn within the shopper electronics market, which by the way decimated reminiscence firms comparable to Micron Expertise, Inc. (MU) and Samsung Electronics Co., Ltd. (OTCPK:SSNLF), TSMC’s revenues dropped 4.4% YoY in 1H 2023 however recovered to develop 18.5% HoH in H2 2023.

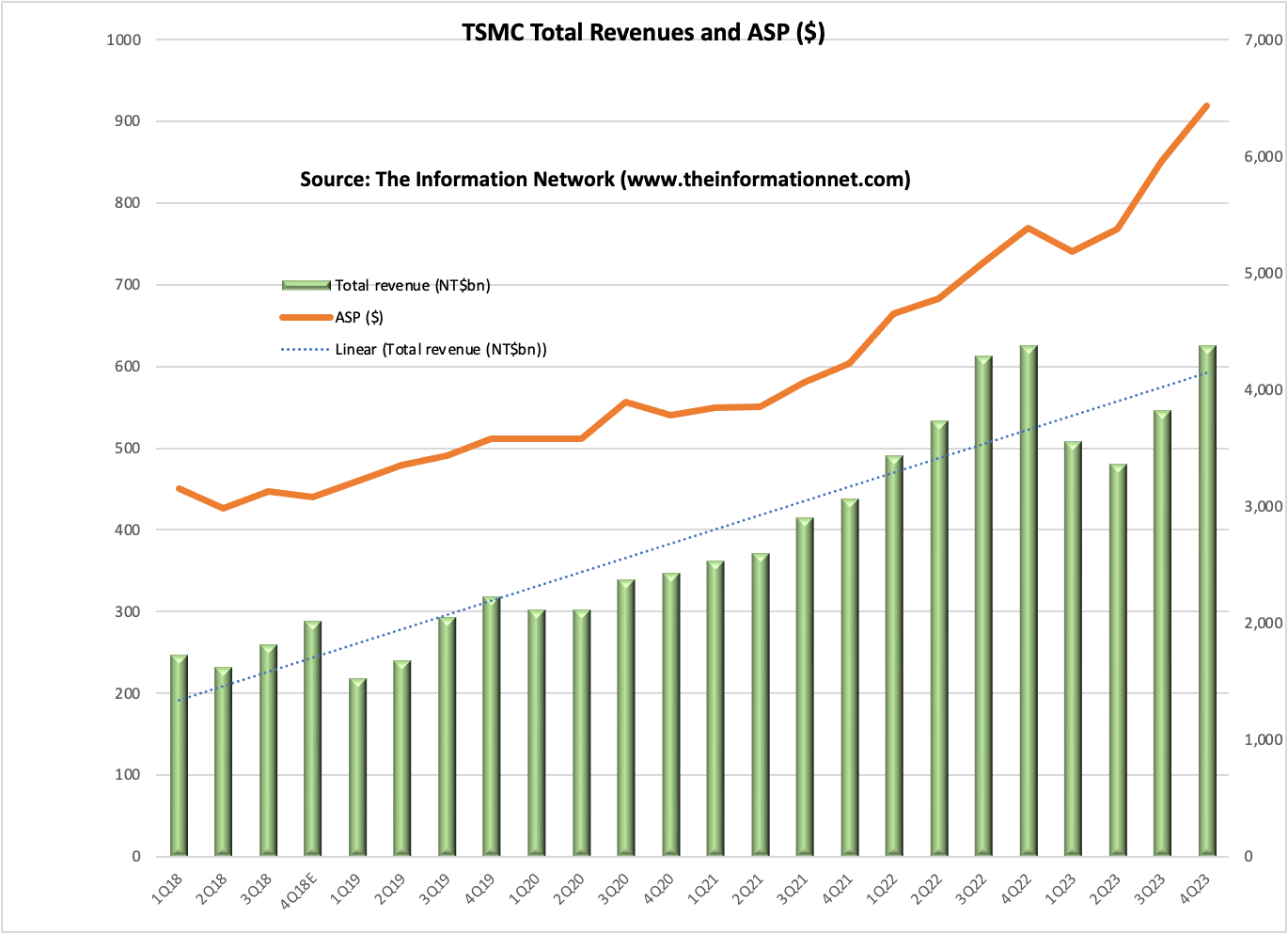

Chart 1 reveals complete quarterly income (NT$ billion) for TSMC between Q1 2018 and This fall 2023, in addition to QoQ income development.

The Data Community

Chart 1

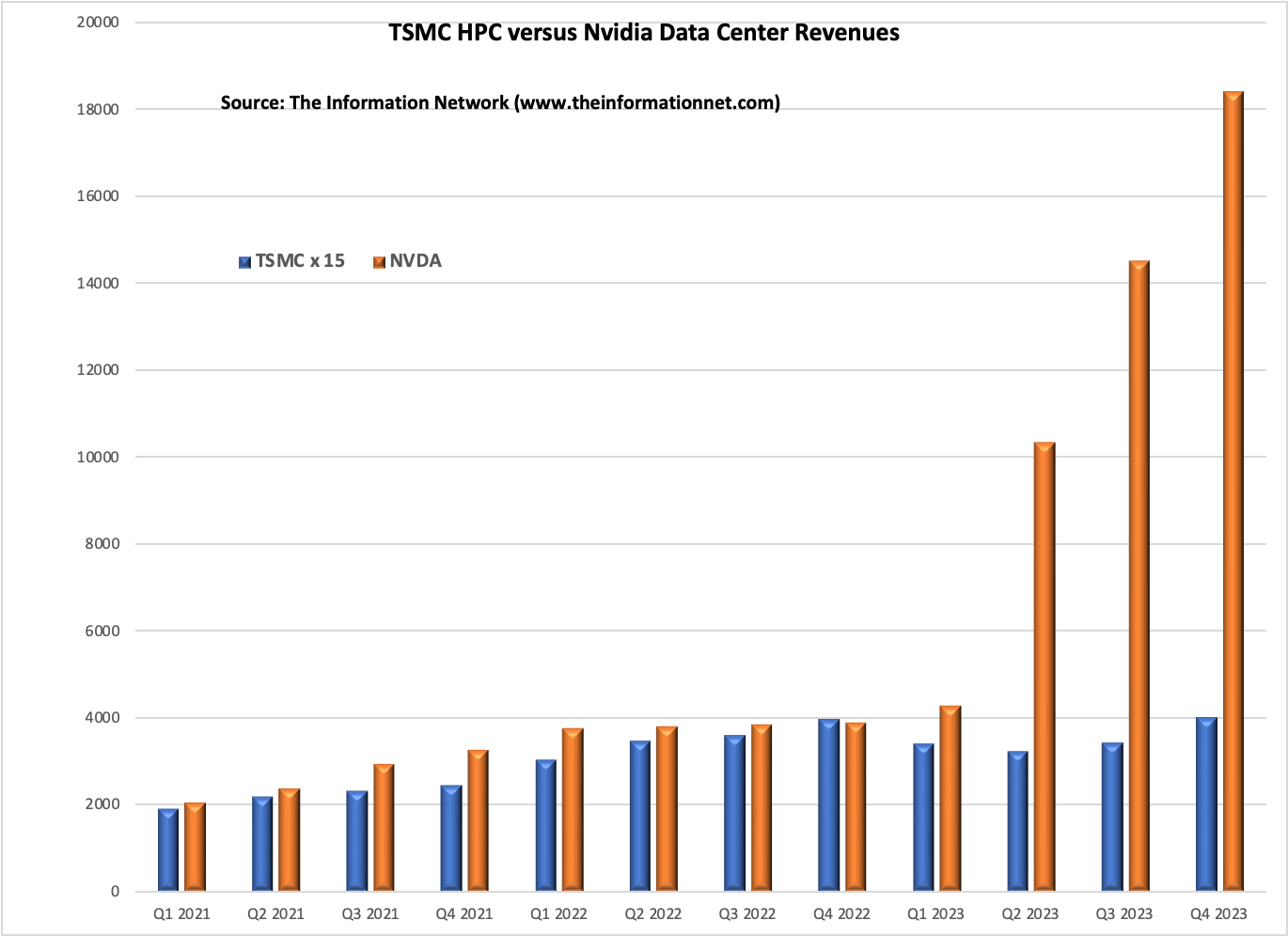

TSMC HPC versus Nvidia Knowledge Middle Revenues

To evaluate whether or not TSMC’s income is underperforming in comparison with AMD and Nvidia, one would want to match the income development charges of those firms over a selected interval, making an allowance for their respective enterprise fashions and market circumstances.

To do an correct comparability, in Chart 2 I plot TSMC’s Excessive Efficiency Computing (HPC) revenues in opposition to Nvidia’s Knowledge Middle revenues from Q1 2021 to This fall 2023. To make sure visible compatibility, I scaled TSMC’s HPC revenues in NT$billion by an element of 15, whereas Nvidia’s revenues are offered in $million.

This helps the argument that there’s a shut relationship between TSMC’s HPC and Nvidia’s Knowledge Middle revenues up till Q2 2023 when Nvidia’s knowledge heart revenues began skyrocketing.

To be clear, TSMC’s HPC merchandise embody private pc central processing models (“CPUs”), graphics processor models (“GPUs”), area programmable gate arrays (“FPGAs”), server processors, accelerators, and high-speed networking chips.

The Data Community

Chart 2

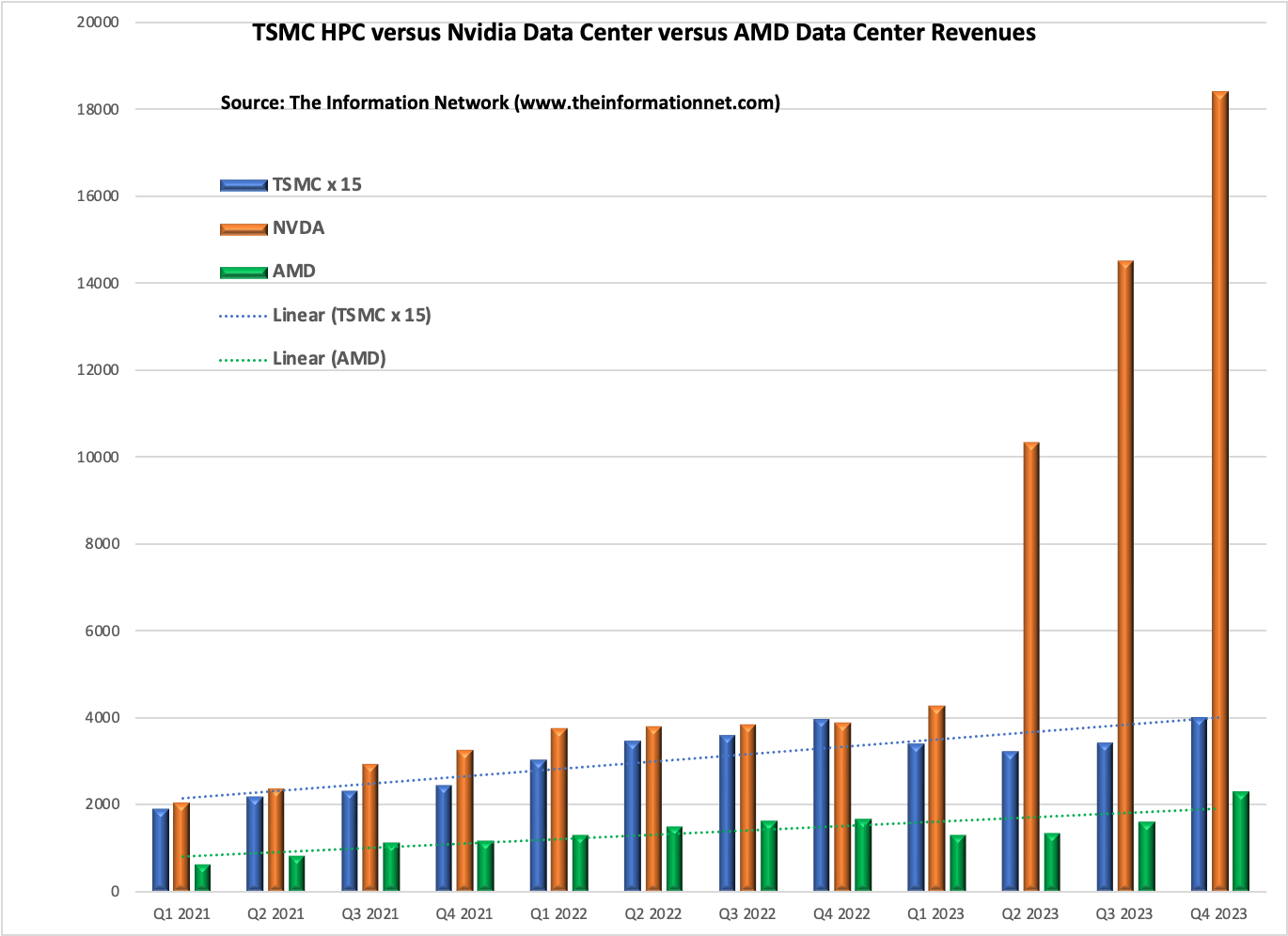

In Chart 3, I add AMD’s Knowledge Middle revenues for a similar interval. Fourth quarter enterprise outcomes have Datacenter section income, of $2.28 billion up 37.9% year-over-year, and up 42.8% sequentially. The robust development was resulting from AMD launching its MI300 accelerator household in December with robust companion and ecosystem help from a number of giant cloud suppliers, all the most important OEMs, and plenty of main AI builders, in line with the corporate. Knowledge Middle steering for Q1 2024 was imprecise, as the corporate solely famous it’s going to develop QoQ in Q1 2024 and exceed $3.5B in 2024.

Chart 3 reveals that trendlines (blue and inexperienced dotted strains) for TSMC and AMD are comparable, and it stays to be seen if AMD can duplicate This fall development as I believe it’s getting ready for the launch of its Mi400 with HBM3 in 2025 to compete in opposition to Nvidia’s B100.

The Data Community

Chart 3

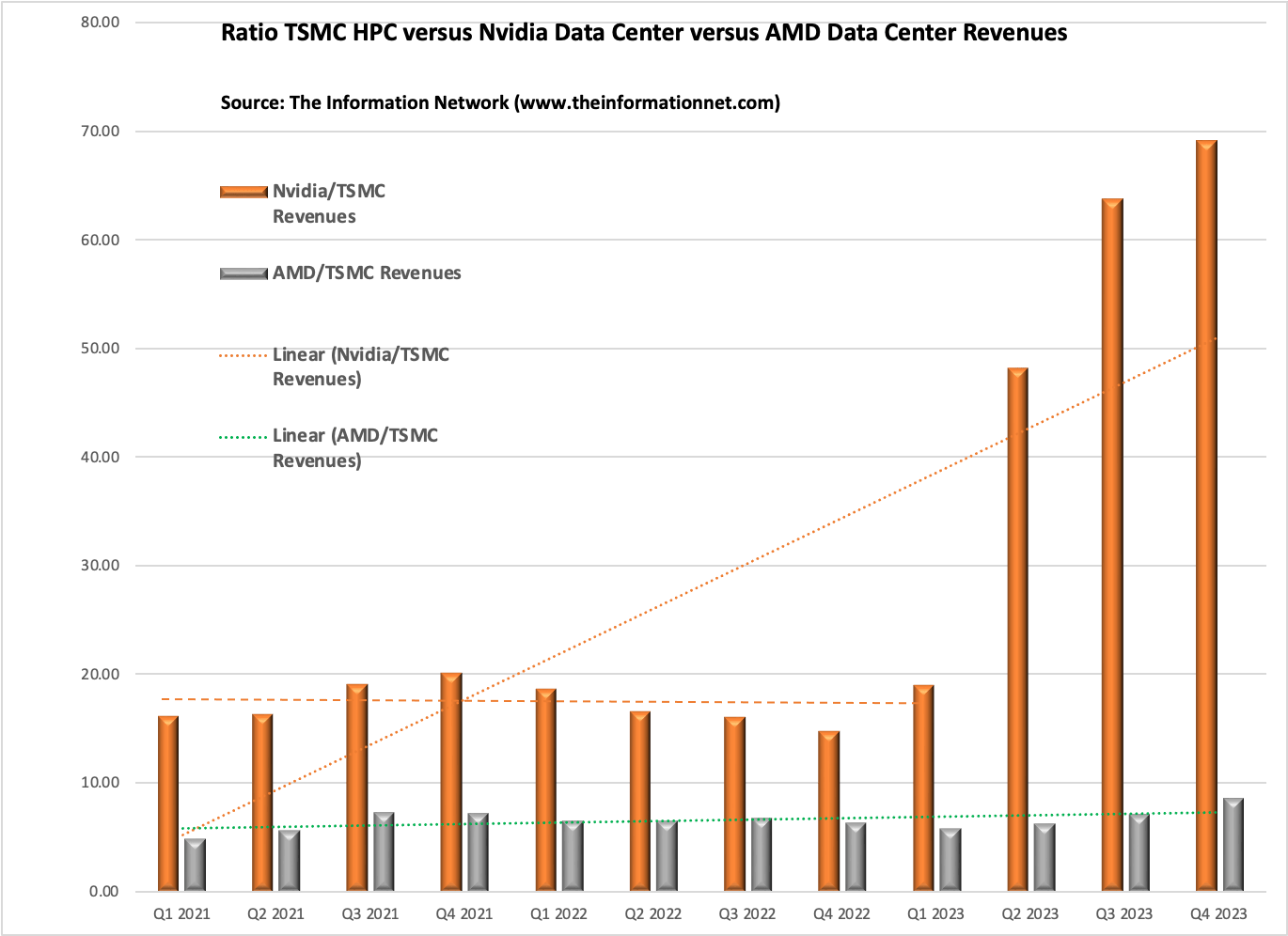

Ratio Comparability of Revenues

I present in graphical kind in Chart 4 the ratio of Nvidia/TSMC revenues (orange bars) and AMD/TSMC revenues (grey bars). These are precise Knowledge Middle revenues for Nvidia and AMD, and HPC revenues for TSMC.

The AMD/TSMC ratio has been flat apart from a This fall 2023 spurt which brought on the development line (dotted grey line) to indicate a constructive slope. The identical is true for the Nvidia/TSMC trendline (dotted orange line) till the ramp in Q2 2023.

Clearly, AI GPUs from Nvidia and AMD are inflicting a divergence in revenues regardless that these chips are made by TSMC.

Mi300 ASPs are estimated at between $10,000 and $15,000 (relying on buyer and amount). Nvidia’s H100 processors are priced between $25,000 and $40,000.

The Data Community

Chart 5

TSMC’s Worth Enhance

TSMC was planning on growing the costs of its chips in mid-2023, however the slowdown within the chip market and its revenues pressured the corporate to recant. Chart 6 reveals TSMC revenues and ASPs between Q1 2018 and This fall 2023.

You will need to acknowledge on Chart 6 that the ASPs usually are not solely correlated with worth will increase, however on product combine as smaller node wafers are priced increased. In This fall 2023, a notable portion of TSMC’s wafer income stemmed from its extra superior course of nodes. Particularly, 15% of the income was attributed to wafers processed with N3 know-how, whereas N5 and N7 applied sciences contributed 39% and 17%, respectively. By way of financial worth, N3 know-how accounted for $2.943 billion, N5 for $6.867 billion, and N7 for $3.3354 billion.

General, TSMC’s superior know-how nodes, encompassing N7, N5, and N3, collectively represented 67% of its complete wafer income. Moreover, a broader class inclusive of all FinFET-based course of applied sciences comprised 75% of the corporate’s wafer gross sales.

The Data Community

Chart 6

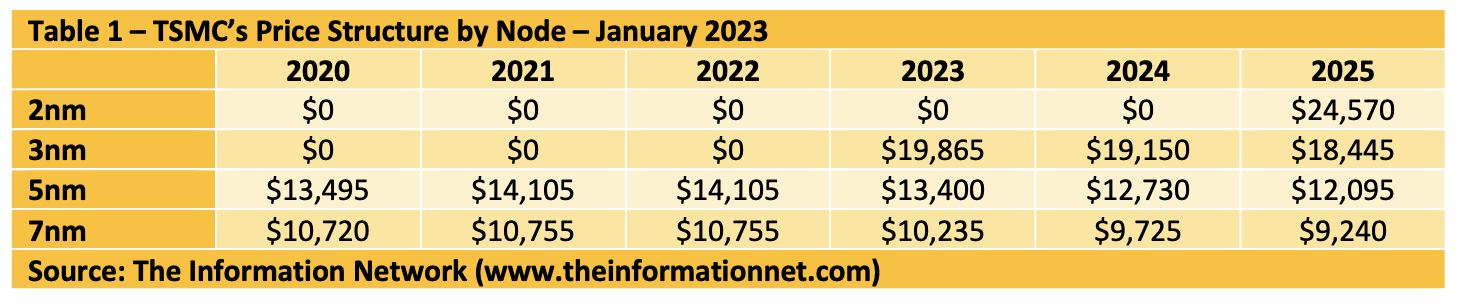

Desk 1 reveals TSMC’s worth construction as of January 2023, in line with The Data Community’s report International Semiconductor Gear: Markets, Market Shares and Market Forecasts.

The Data Community

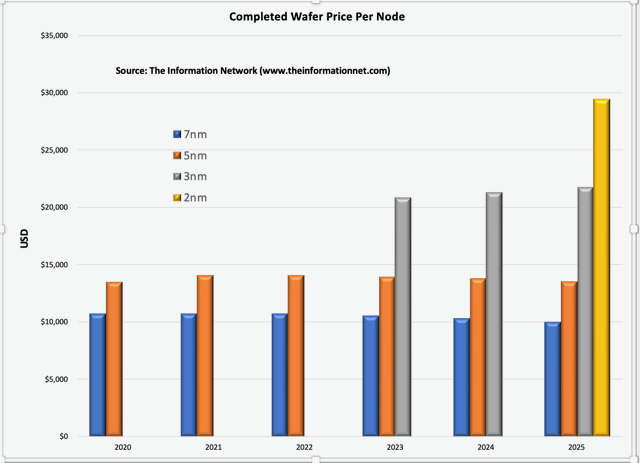

In late 2023, TSMC elevated wafer costs and intends to extend them once more in 2024. Chart 7 reveals the brand new pricing construction for wafers calculated by way of 2024 and estimated for 2025. On combination, TSMC will increase costs by 8.7% in comparison with costs listed in Desk 1.

Importantly, TSMC’s 2nm wafer worth in 2025 will attain almost $30,000. By means of comparability, primarily based on a chip dimension of 814 mm2, TSMC can fabricate 87 H100 chips for Nvidia, primarily based on 100% yield. At an ASP of $30,000, as said above, it signifies that Nvidia can generate revenues 87x higher than what it pays TSMC for every wafer.

The Data Community

Chart 7

Investor Takeaway

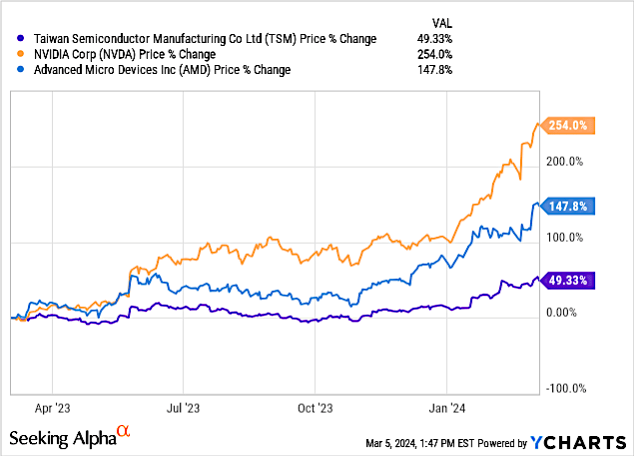

Chart 8 reveals share worth change efficiency for the previous yr for TSM, NVDA, and AMD. It reveals the disproportionate development in NVDA in comparison with the others.

YCharts

Chart 8

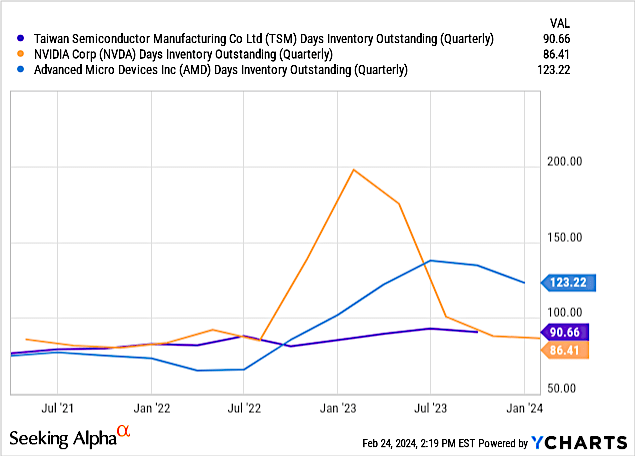

Chart 9 reveals days of stock for TSMC, together with prospects NVDA and AMD for the previous 3-year interval. Days of stock for NVDA and AMD had elevated in 1H 2023 as chip demand softened and subsequently dropped to 123 days for AMD and 86 days for NVDA. TSMC stock has remained flat throughout this era.

YCharts

Chart 9

There was concern that TSMC does not have the capability to fulfill demand from AMD. Nevertheless, this isn’t the case on the fabrication foundry, however is the case for TSMC’s packaging foundry. I mentioned this in a February 13, 2024 Searching for Alpha article entitled “Intel’s Secret Weapon.”

What has occurred on the fabrication foundry is that TSMC has adjusted capability utilization, as a result of semiconductor slowdown in 2023. In Q3 2022, TSMC’s capability utilization was at 111%, which means demand was 11% higher than provide. In This fall 2022, utilization began dropping till it reached a low of 73% in Q3 2023 earlier than growing to 76% in This fall 2023. Because of this at present, provide is outpacing demand by 24%, and in precept, in This fall, 24% of fabs had been idle.

This oversupply was in trailing-edge chips (>20nm), which dropped to 37% of revenues in This fall 2023 from 41% in Q3 2023. That is the important thing for the corporate, because it continues to spend on modern know-how – the transfer to 3nm and 2nm know-how.

In response, TSMC lower capex in the direction of the decrease finish of the 32% to 36% vary for 2023 due to the overhang of sluggish gross sales to PCs and Smartphones. As well as, TSMC has a technique in order that a few of its N3 capability will be supported by N5 instruments, enabling increased capital effectivity with out WFE spend.

Modern know-how accounts for between 70% to 80% of its complete CapEx within the yr, mature specialty know-how between 10% to twenty%, and the remaining is break up between superior packaging and its e-beam operation.

The truth is, CEO C.C. Wei noted:

- “N3 successfully entered volume production and enjoyed a strong ramp in the second half of ’23, accounting for 6% of our total wafer revenue in 2023.

- N3E is already into volume production in the fourth quarter of 2023.

- N2 technology development is progressing well and on track for volume production in 2025.”

TSMC is undervalued. With out the corporate making the chips, Nvidia and AMD wouldn’t be within the place they now take pleasure in, which is a catalyst for Nvidia’s excellent Q2-This fall steering. I price TSM inventory a Purchase.