Yongyuan Dai/DigitalVision via Getty Images

Dividend investing sits at the core of REITer’s Digest, which provides a platform for discussion of income producing assets. While real estate is the focus, dividends can be found far and wide. We’re not alone in our love for dividends. The great John D. Rockefeller once said, “do you know the only thing that gives me pleasure? It’s to see my dividends coming in.”

Dividends come in all shapes and sizes. Most dividends rise over time, some tragically fall or fade away entirely. The stock market in totality has provided a solid platform for growing dividends for decades. Historically, dividends have increased faster than inflation and with relative consistency.

Today, we will focus on two REITs which pay monthly dividends. They invest in unique areas and operate different businesses, but they share three primary commonalities. First, each has an established track record of not only paying, but increasing, their monthly dividends. Second, each company is a top competitor in their respective niche. Third, each carries an investment grade credit rating, providing confidence in their balance sheets and capitalization.

Why Monthly Dividends?

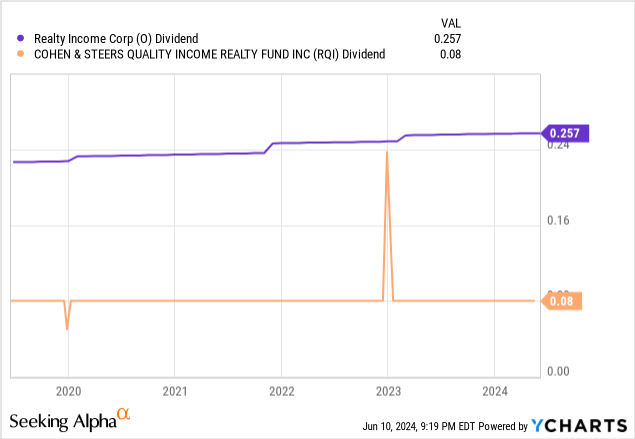

Monthly dividends are becoming increasingly common as a shareholder incentive. More specifically, real estate lends itself to a monthly dividend model, as investors expect the collected rent to pass through to their pockets. Coupled with the tax structure of REITs and public real estate companies have become some of the most noteworthy dividend behemoths. Consistent income delivered to accounts is an appealing value proposition for shareholders. There are many REITs and real estate funds that distribute monthly income such as Realty Income (O) or the Cohen & Steers Quality Income Realty Fund (RQI).

Why Net Lease?

While real estate in general lends itself to the monthly dividend model. Net lease REITs cater themselves to a rising dividend model. Most net lease agreements are long term and include negotiated rent increases with some degree of predictability.

Triple net, or NNN, leases are lease agreements where the lessee is responsible for reimbursing the landlord for certain property level expenses. These include property taxes, insurance, and maintenance costs. Net leases come in a variety of shapes and sizes. Most triple net leases have comprehensive reimbursement structures for the landlord, known as absolute triple net leases. However, there are other variations, including double net leases.

Triple net real estate allows the tenant to maintain ownership responsibilities while leveraging the capital which was trapped in the real estate. Alternatively, it allows the company to remove real estate from their balance sheet and reinvest the capital for growth. Triple net leases are generally a minimum of five years when signed.

The lease structure also allows investors to avoid capital expenditures required with property level maintenance, insulating from rising costs. Over the past several years, this has been important given the elevated rate of inflation.

Triple net leases are generally limited to select categories of assets. For example, retail and industrial are the largest net lease subcategories. In contrast, the operations of hotels or apartments do not lend themselves to a NNN lease structure.

Building A Complete Net Lease Portfolio

Constructing a complete net lease portfolio combines a series of considerations. While there are now dozens of publicly traded net lease REITs available to investors, most have significant overlap within their business models. There are three key differentiators for net lease REITs: asset class, geography, and investment philosophy.

While the net lease world is limited in terms of diversity, there are still opportunities to spread across different asset classes including retail, industrial, and other smaller niche areas like single tenant data centers. A prospective investor must consider the appropriate mix of assets, diversifying appropriately. Picking REITs with unique areas of focus is important to not only diversify but also cover bases as performance across asset classes diverges.

A secondary consideration is geography. This consideration has become less and less important over time as most REITs diversify nationally. However, there are still REITs which maintain specific geographies, such as Rexford Industrial (REXR) or SL Green (SLG). Within the net lease sector, most REITs are widely diversified across the United States. Some REITs even invest internationally, opening a new opportunity set entirely.

Finally, investment philosophy is another critical consideration. Net lease investing is a highly specific niche of the real estate market. However, there are still important intricacies that differentiate each participant. For example, some REITs focus on investing in properties with high credit quality tenants, such as Agree Realty (ADC). Others choose to pursue more aggressive growth models through high yield sale leaseback transactions with middle market tenants, such as Essential Properties Realty Trust (EPRT). Finally, net lease development is growing as REITs pursue avenues for additional yield. Net lease REITs including O have recently created platforms to pursue development funding opportunities around the world.

With these considerations, let’s explore two REITs that create a comprehensive portfolio.

1. Realty Income Corporation (O)

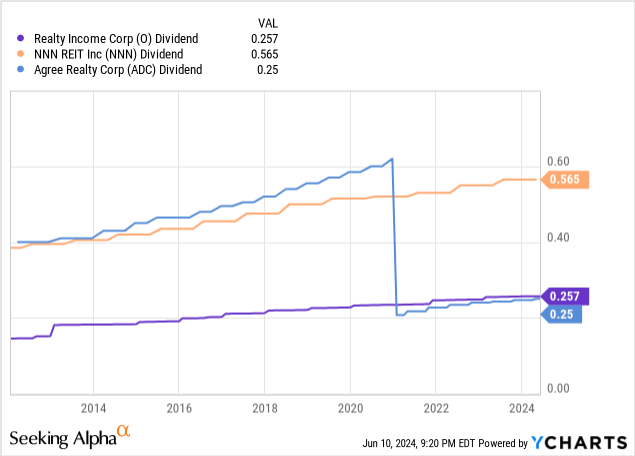

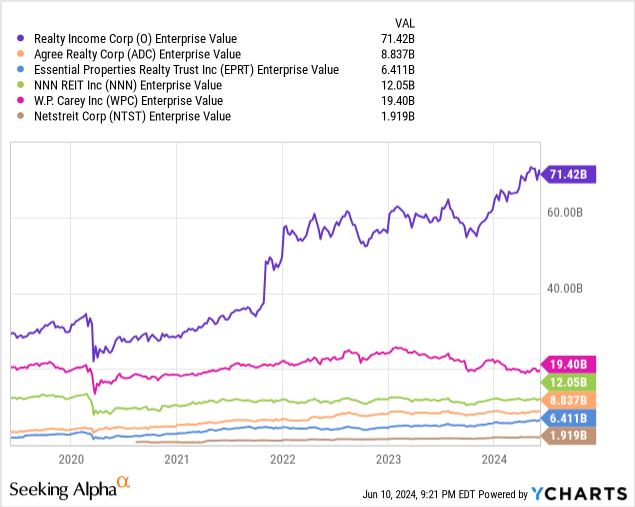

O is simply an unparalleled net lease REIT. It’s difficult to publish a list of all star REITs without including “the monthly dividend company.” Founded in 1969, O has slowly transformed from a fast food and childcare investor to the world’s largest net lease REIT. Today, O has grown to become a “net lease index fund” owning a material portion of the entire net lease market. Based on their current portfolio of over 15,000 properties, Realty Income’s portfolio is larger than Agree Realty, NNN REIT (NNN), Essential Properties Realty Trust, and NETSTREIT (NTST) combined.

O has quickly grown to become one of the largest landlords in the world. Today, O sits amongst the largest REITs by enterprise value, overshadowing the remainder of the net lease market by a significant margin.

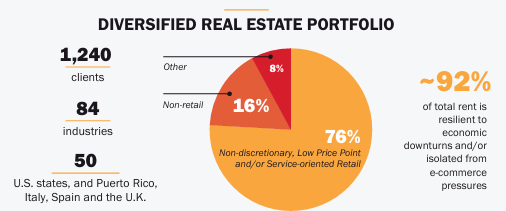

O owns and operates a portfolio throughout all 50 states, Puerto Rico, the United Kingdom, Spain, Italy, Ireland, France, Germany, and Portugal. Across these geographies, O invests in stabilized assets and development deals. O is a retail REIT at heart, owning a diversified portfolio of properties leased by household names. However, O has also ventured into other asset classes including data centers and industrial, including cold storage. O is also one of the largest landlords in Napa Valley, owning a large portfolio of vineyards on NNN leases.

O Investor Presentation

O has a storied history, changing, improving, and growing over the years. However, the company has never deviated from its mission, which is literally sending monthly dividends to shareholders. Realty Income’s Mission & Values statement is:

For more than 50 years, Realty Income has been guided by our mission to invest in people and places to deliver dependable monthly dividends that increase over time. We do this by nurturing long-term, meaningful relationships that enable people to achieve a better financial outlook. We understand that when individuals succeed financially, they are able to provide for their families, support local businesses and pursue their greatest ambitions—creating a lasting positive impact on communities.

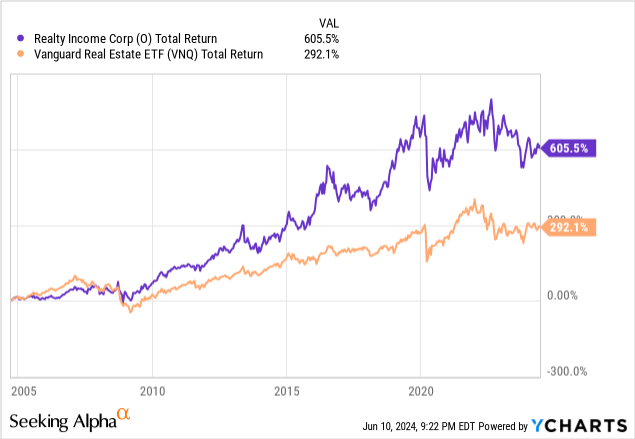

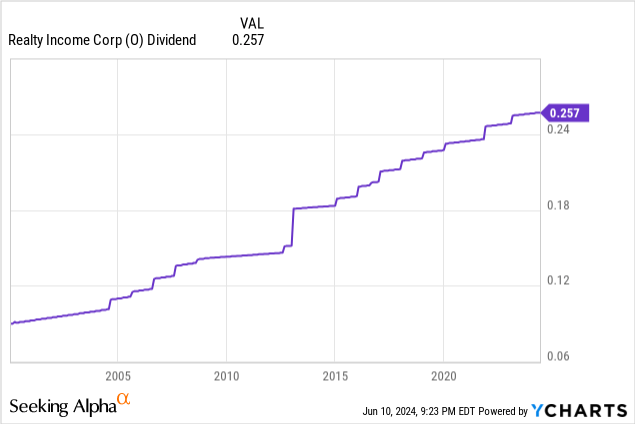

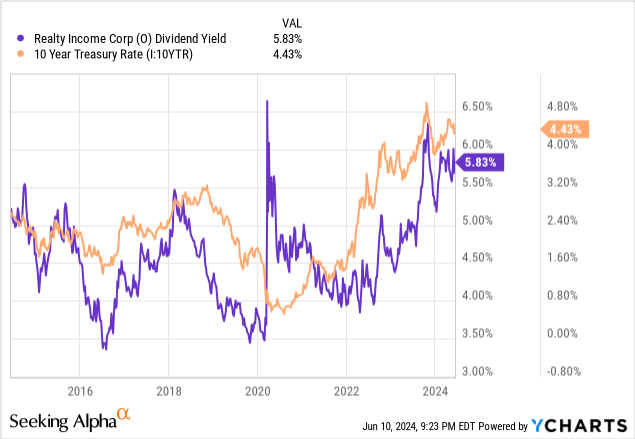

O’s track record of dividend growth is literally unparalleled in real estate. O is one of few REITs to maintain dividend aristocrat status. O became a public company in 1994. Since, O has raised the dividend annually, setting a 30-year track record of increasing dividends as a public company. O was also increasing the dividend prior to IPO. O’s monthly dividend has become a staple in many income portfolios, offering an attractive combination of yield and long-term growth. O increases the dividend on a quarterly basis. Over the past five years, the compound annual growth rate has averaged 3.55%.

Based on current share prices, O’s dividend yield is nearly 6%. Over the past several years, O’s yield has increased significantly because of an increasing ten-year treasury yield.

O’s fundamentals remain strong, including A and A3 credit ratings from S&P and Moody’s, respectively, and billions in available liquidity. In fact, on the first quarter earnings calls, O’s management team suggested that this year’s $3 billion of investment guidance will be covered by settled equity, free cash flow, and dispositions with no need to tap capital markets.

After the Spirit merger closed in January, our annualized free cash flow available for investments is approximately $825 million. This provides us significant organic investment capacity to finance our growth plans without being required to tap into the debt or equity markets to meet current investment guidance. I would also note this also excludes any additional capacity generated by our disposition program, which I will discuss later.

An elevated yield paired with a growing dividend and an investment grade balance sheet is a recipe for success, making O one of our favorite monthly paying REITs.

2. STAG Industrial (STAG)

Over the past years, industrial has emerged as one of the most attractive real estate asset classes with a strong outlook. Accordingly, adding an industrial net lease investment will help round the retail-heavy portfolio of O. O’s non-retail portfolio accounts for nearly 25% of assets, split between data centers, hotels, vineyards, industrial, etc. Accordingly, we introduce STAG Industrial.

STAG is a net lease industrial REIT focused on the acquisition and development of single and multitenant industrial properties across the country. Like O, STAG owns assets under net leases, meaning limited landlord liability. STAG owns a 112 million square feet portfolio leased to nearly 600 tenants.

STAG’s portfolio is different from many industrial focused REITs like Rexford Industrial Realty or Terreno Realty Corporation (TRNO). STAG owns properties in secondary and tertiary markets, most of which are leased under longer lease terms. These assets often have significantly higher acquisition capitalization rates than the assets acquired by REXR and TRNO. In STAG’s 2023 annual report, STAG reported an average acquisition capitalization rate of 6.2%.

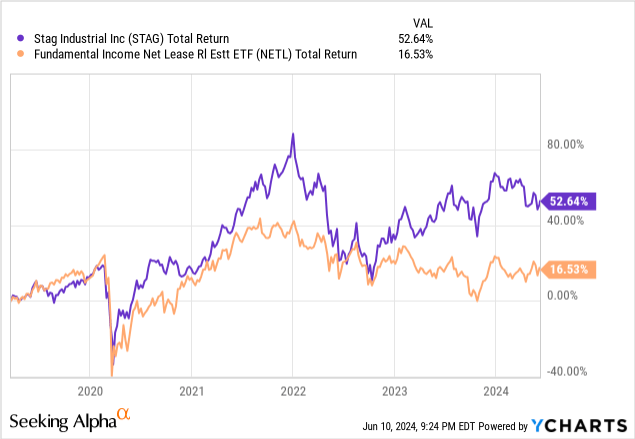

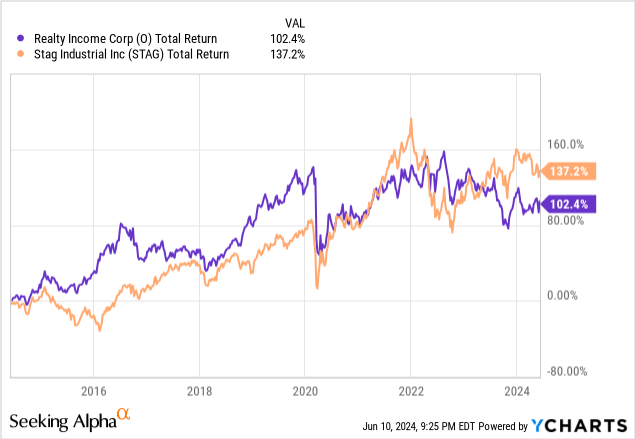

STAG’s industrial focus has led to outperformance of the net lease sector over the past five years. Tailwinds stemming from the pandemic have precipitated significant increases in market rent for industrial assets across the country. Increasing rents have supported increasing property values, even in the face of softening capitalization rates.

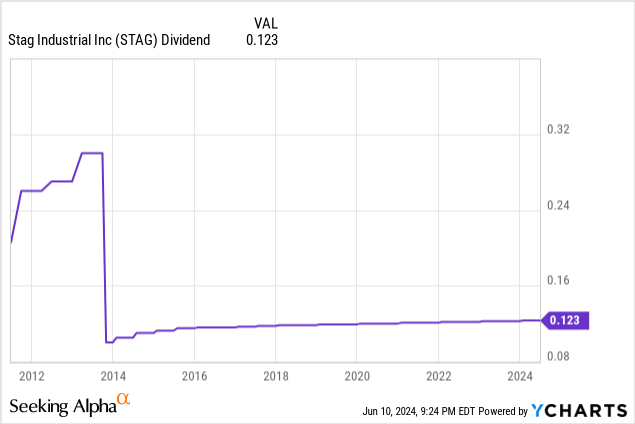

The monthly dividend distributed by STAG has grown each year since going public in 2011. STAG initially distributed quarterly dividends until 2013 when the REIT opted to send monthly payments. Historically, STAG has provided a modest annual increase to the dividend.

Investors often complain about the anemic dividend growth, especially as compared to the net lease sector at large. Put simply, STAG has opted to reinvest capital into their assets through value add projects and conservatively capitalized acquisitions, rather than prioritize the dividend growth rate.

Recent earnings have highlighted extraordinary leasing spreads within STAG’s portfolio. Recently, leasing spreads have landed from 30%-50%, marking significant increases to cash flow at the portfolio level and AFFO growth. For STAG, this means asset level performance is remarkably strong, outpacing what is typical for net lease leasing spreads. As a point of reference, O’s long-term spreads in release scenario are 2%. STAG’s portfolio also has a shorter weighted average lease term than most net lease competitors investing outside of industrial. STAG’s 4.3-year weighted average lease term means a larger portion of the portfolio is consistently marking to higher market rents.

Over time, STAG has prioritized a broad reduction in the dividend payout ratio. From 2022 to 2023, the payout ratio declined by 3%, from 78% to 75%, indicating management’s plan is working. A declining payout ratio combined with a growing dividend has earned STAG Industrial an investment grade credit rating from S&P and Moody’s.

Conclusion

Building a complete real estate portfolio does not have to be rocket science. While there are a variety of bases to cover, net lease REITs like O and STAG are a good place to begin. With dependable business models, fortress balance sheets, and long histories of increasing dividends, these two companies are blue chips in the net lease sector.

O is one of the largest real estate companies on the planet. With over 15,000 properties in the portfolio, O owns a material portion of the entire net lease universe. We’ll continue repeating that O is close to a “net lease index fund.” Nevertheless, the company is a blue chip in the real estate game, investing in a variety of asset classes around the world. O alone could be argued as a sufficiently diverse investment in and of itself. However, the primary focus on retail leads us to invest in another top performer.

STAG is a unique net lease REIT, focusing on industrial investments nationwide. While most net lease REITs invest in long-term assets, STAG has a more active business model. This means buying properties with a value add strategy or the intent to lease the property more frequently. Tailwinds over the past several years have provided an extraordinary foundation of growth for STAG. The company has transformed itself into a formidable player in the industrial space, outperforming the net lease sector.

Combining these two REITs can build a comprehensive portfolio, diversified across asset classes, geographies, and investment styles. A multicylinder approach paired with experienced management is a recipe for long-term success.