niphon/iStock by way of Getty Pictures

Introduction

With essentially the most great time of the 12 months upon us it is solely proper I discuss constructing your dividend snowball going into 2024. Once you consider Christmas, you consider lights, items, household & mates, and snow. In fact, that is all depending on the place you reside. In case you stay in San Diego like I do, then you aren’t getting the luxurious of enjoying with household and mates within the snow, however you may construct your dividend snowball. The following 12 months shall be crucial, particularly for dividend traders. Know why? As a result of everyone seems to be on the fence about price cuts. Will the Fed hold charges elevated all through 2024, will they minimize, deflation worries, and so forth. Me personally, and I’ve talked about this, I anticipate our first minimize someday within the latter half of the 12 months. However whether or not they determine to chop, hold them the identical, or elevate these two shares will assist construct your dividend snowball. Let’s get into these two implausible shares and why they’re nice for compounding.

#1 Essential Road Capital (NYSE:MAIN)

How might one write an article about constructing their dividend revenue with out the month-to-month paying BDC, Essential Road Capital? I final mentioned MAIN in an article printed final month which you’ll be able to read here. MAIN has lengthy been considered one of my favourite BDCs. I’ve held them earlier than and have been ready for some time to get again in at worth. However for good purpose the inventory normally trades at a fairly large premium to its NAV. I just like the inventory within the mid to low $30’s however actually do not see them touching that worth anytime quickly. However one factor the market has taught me is persistence, and I’ve realized that I’ll doubtless get my likelihood to personal them once more.

Together with the common month-to-month dividend of $0.235 payable this week, in addition they declared a particular dividend of $0.275 payable on the finish of this month, simply in time for the brand new 12 months. Merry Christmas! So, in complete traders get a dividend payout of $0.51 for the month of December. That is well-covered by the NII of $1.04 the BDC introduced in for the 3rd quarter this previous November, exceeding the month-to-month dividends paid by 51%. In addition they introduced in $123.24 million which missed estimates by $0.55 million. These had been each down from Q2’s $1.12 and $127.6 million respectively.

One purpose MAIN is ready to payout particular and supplementals together with a rising month-to-month dividend is their internally managed construction. These sometimes align extra with shareholders which normally results in extra elevated dividends over time. Externally managed BDCs however are usually extra conservative just like Ares Capital (ARCC), preferring to roll over their additional revenue.

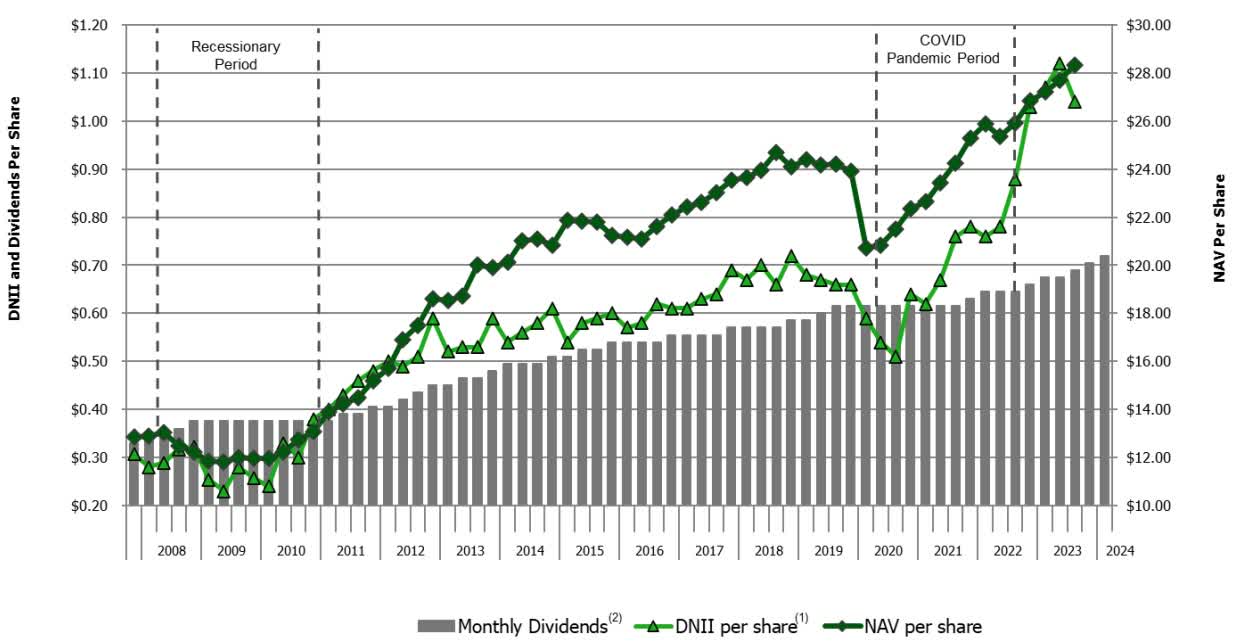

Moreover, the month-to-month paying BDC has already declared a complete of $0.72 in dividends for the primary quarter of 2024. Since its inception, they’ve by no means decreased its common month-to-month dividend, which is spectacular. This even consists of in the course of the Nice Monetary Disaster and the current pandemic in 2020. As seen within the chart under, not solely has MAIN elevated their dividend, however in addition they managed to develop their NAV and DNII properly over the identical interval. So, traders haven’t got to fret about if the yield is sustainable or not. And also you additionally get a rising month-to-month dividend to assist compound and construct your dividend snowball a lot faster.

Essential Road Capital

Portfolio High quality

A method the BDC has been capable of develop their NAV, DNII, and month-to-month dividend is by sustaining a well-diversified portfolio. At quarter finish, the BDC had a complete of 195 corporations throughout 50 industries. That is compared to the most important BDC and peer, ARCC, who’s diversified in half the quantity (25). Moreover, their portfolio has an astronomical first lien focus at 99%! That is essential particularly within the present macro atmosphere as extra corporations are dealing with downward pressures. Being invested in first-lien loans assures the corporate has a better chance of gathering revenue as a result of they’ve the pinnacle of the road privileges of mortgage funds.

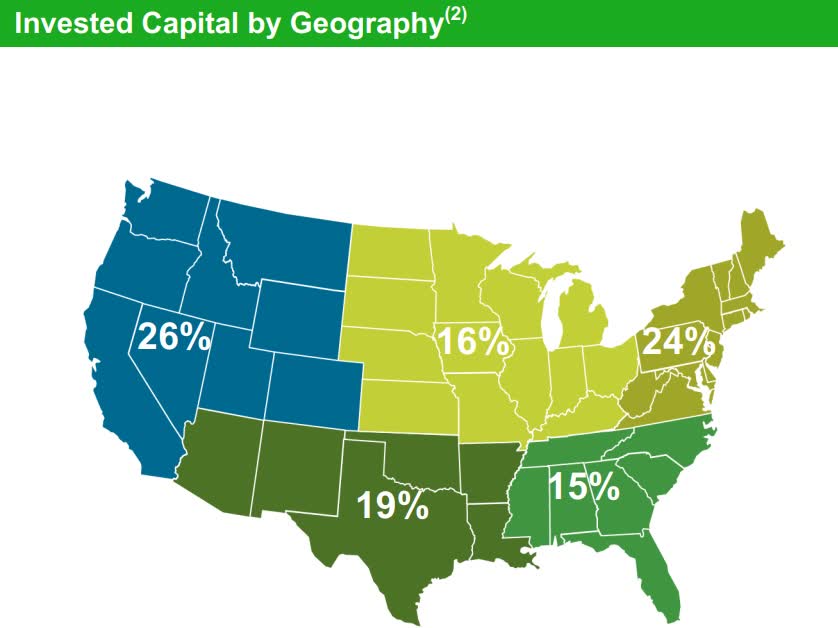

They’ve 8% of their portfolio invested in Web Software program & Providers with 6% in each Skilled Providers and Building & Engineering. Moreover, the BDC is well-diversified by geography and never simply concentrated in a single location. As you may see under, a bigger share of their portfolio is invested on the Western Coast of the US.

Essential Road Capital

#2 Oaktree Specialty Lending Company (NASDAQ:OCSL)

This BDC is a newcomer for me. I’ve heard a number of good issues about them from readers right here on SA and now they’ve jumped on my radar due to their excessive dividend. As compared, that is increased than considered one of my absolute favourite BDC holdings, ARCC. So, they’re an ideal addition to any dividend-focused portfolio. In contrast to MAIN, Oaktree is externally managed. In addition they pay a quarterly dividend of $0.55 as a substitute of a month-to-month one like MAIN. Moreover, they declared a particular dividend of $0.07 which is payable together with the common dividend on the twenty ninth of December. Throughout their Q4 earnings in November, the BDC’s adjusted web revenue was $0.62, in step with Q3. This was up practically 13% from $0.55 on the finish of 2022 and $0.61 in Q1.

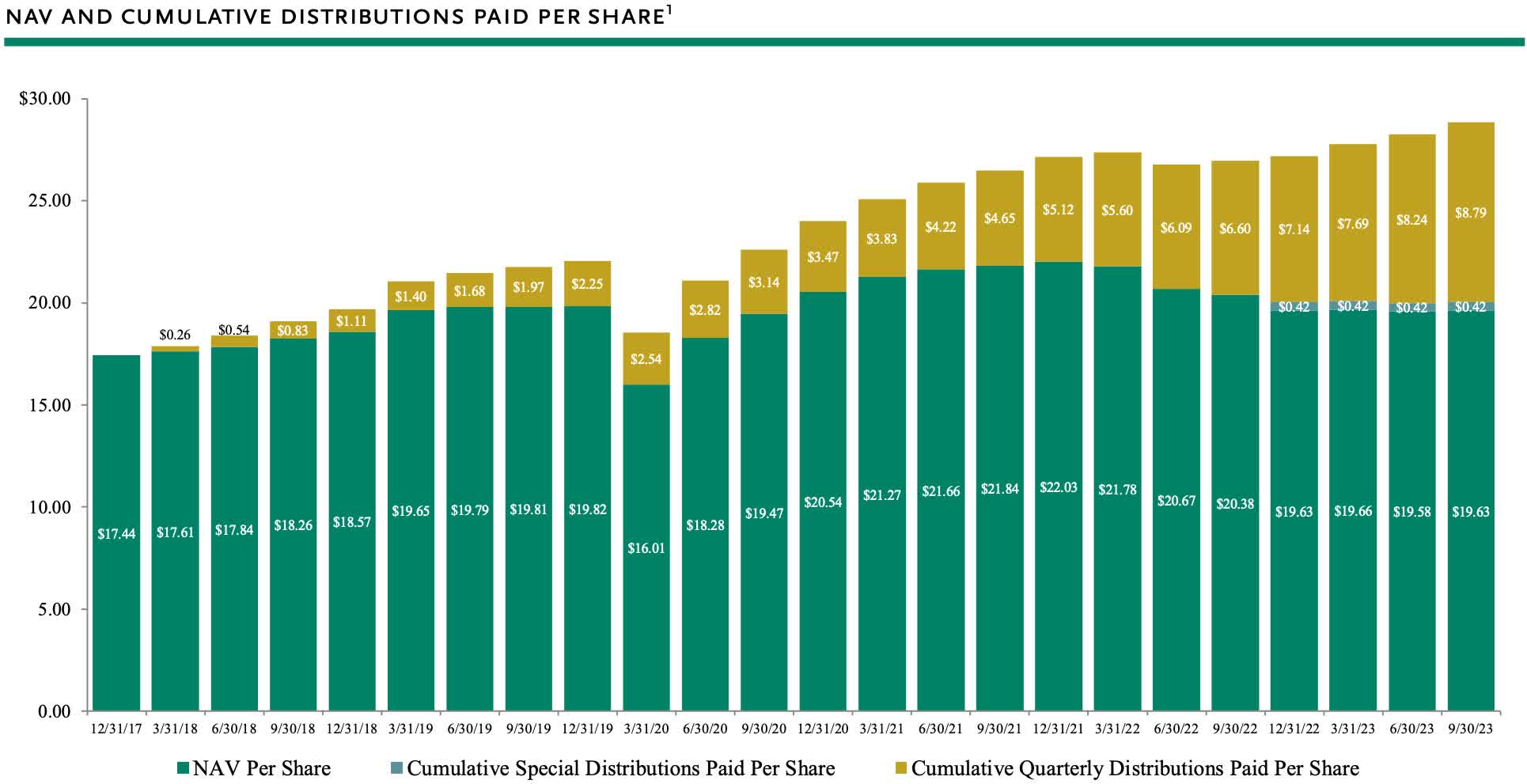

As you may see under, the cumulative quarterly distributions paid per share have elevated steadily over the past 6 years. NAV has additionally elevated steadily through the years however remained flat this 12 months at $19.63 per share. Complete web funding revenue of $2.47 for fiscal 12 months ’23 exceeds the full dividend quantity of $2.27 paid this 12 months by $0.20. This consists of the particular of $0.07.

OCSL investor presentation

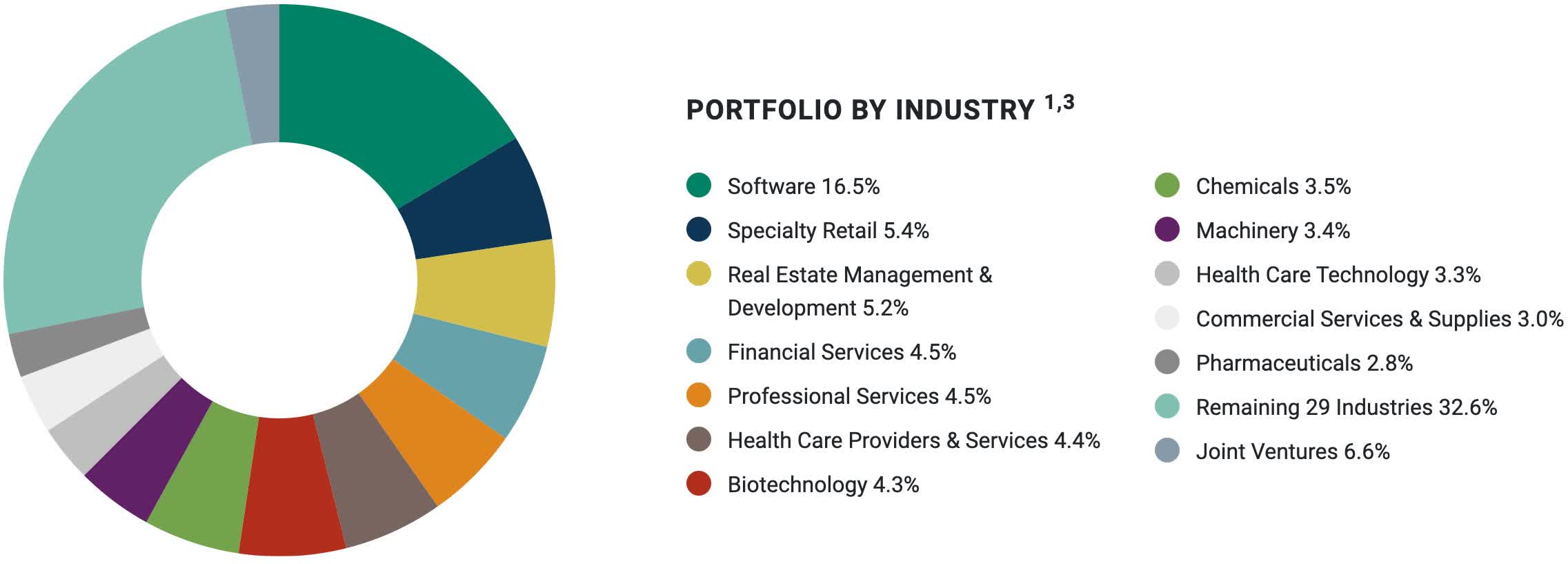

Portfolio High quality

Like MAIN and several other different BDCs, OCSL additionally focuses on the Software program business with 16.5% of their portfolio on this section. A big distinction between the 2 is whereas MAIN’s different two largest industries are Building & Engineering and Skilled Providers; Oaktree’s is Specialty Retail and Actual Property Administration & Growth at 5.4% and 5.2% respectively.

Throughout the quarter the BDC additionally continued to develop and diversify their portfolio with $87 million in new investments, all first lien. Moreover, in addition they managed to extend their first-lien publicity from 71% to 76% whereas reducing their second-lien publicity from 16% to 10%. That is one thing I prefer to see as a result of it improves the chance/return profile which in flip helps them higher navigate financial uncertainty.

OCSL investor presentation

In totality, OCSL’s portfolio worth stood at $2.9 billion diversified throughout 143 corporations. This comprised 86% in senior-secured loans with 76% first lien publicity and 86% of their debt investments being floating price, making them well-prepared for a better for longer atmosphere. Within the coming quarters, I anticipate them to proceed to deal with rising their first lien mortgage publicity additional strengthening their portfolio.

Stability Sheet Comparability

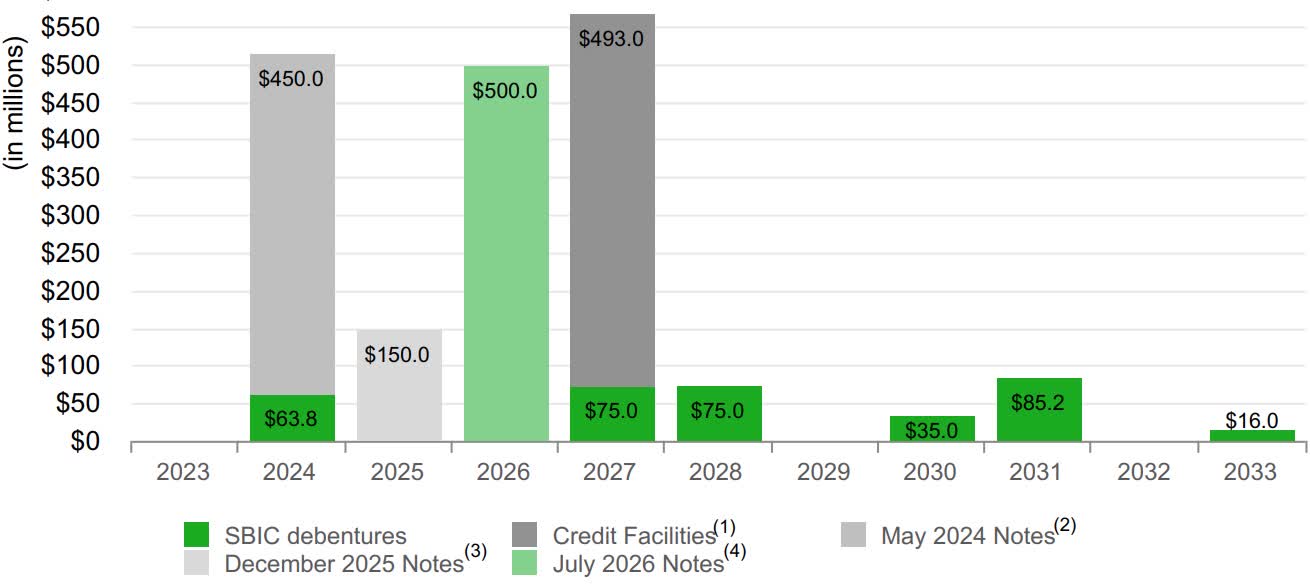

Going into 2024 traders ought to search for corporations with not solely nice administration groups however robust stability sheets, primarily due to the macro atmosphere. Each BDCs have robust ones with no important quantity of debt maturing within the subsequent 12 months. MAIN has $450 million due in MAY of subsequent 12 months compared to OCSL who has no debt maturing till 2025. And even that quantity is insignificant in comparison with their accessible liquidity. MAIN has a lesser quantity of solely $150 million due in 2025.

MAIN investor presentation

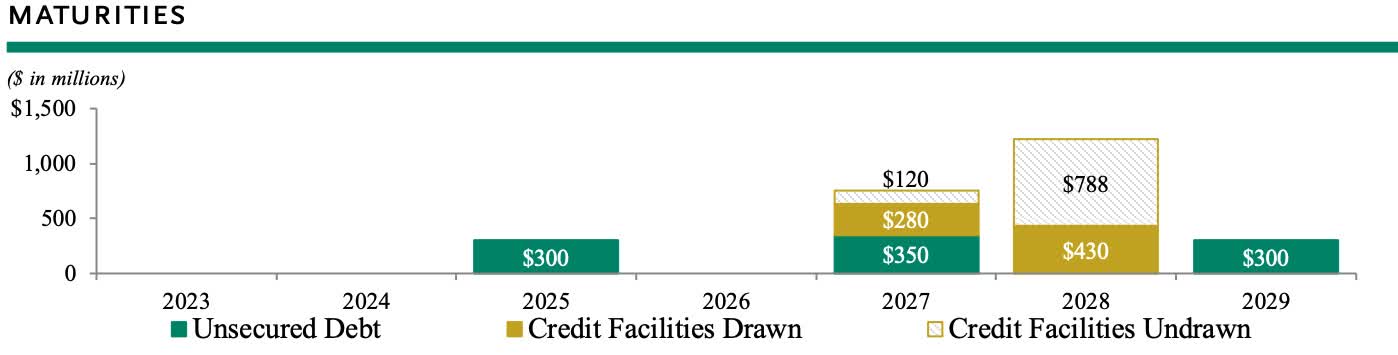

OCSL’s maturities you may see they’ve double the quantity of MAIN in 2025. However they’ve none maturing after that till 2027 whereas Essential Road has $500 million due. MAIN had $843 million accessible liquidity on the finish of the quarter whereas OCSL elevated theirs to $1.2 billion from $1 billion.

Moreover, they managed to lower leverage to 1.01x, down from 1.14x, bringing them inside their focused vary of 0.9x to 1.25x. In addition they had $136 million in money accessible and each sport funding grade credit score scores.

OCSL investor presentation

Dangers & Valuation

I am certain many traders know an enormous threat particularly in the course of the present macro atmosphere is the upper potential for mortgage defaults. Throughout MAIN’s newest quarter, their non-accrual standing stood at 1.0% of their complete funding portfolio at truthful worth and three.1% of value. OCSL’s non-accrual standing accounted for 1.8% of their complete portfolio at truthful worth and a pair of.4% of value. Going ahead that is one thing traders ought to keep watch over going ahead. Particularly if the Fed decides to make good on their promise of a higher-for-longer atmosphere. I believe traders will get a really feel for this on the upcoming assembly this month.

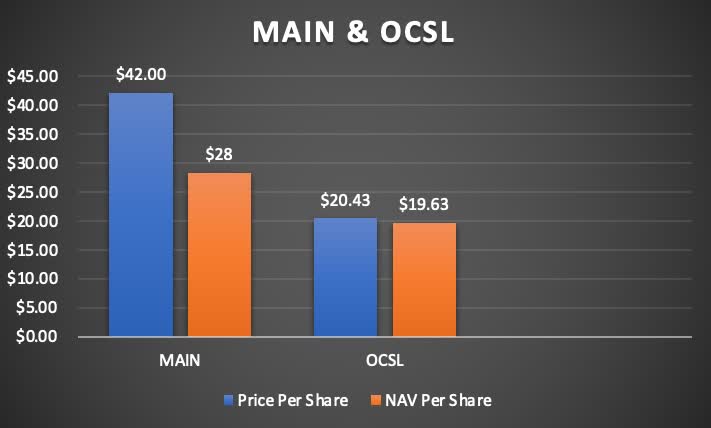

As I said beforehand, I anticipate a minimize however within the latter a part of 2024 so portfolio corporations will proceed to face pressures a minimum of for just a few months of the brand new 12 months. Each BDCs at present commerce at premiums to their NAV with the extra recognized MAIN being bigger at 1.5x. OCSL however trades at a smaller premium at 1.0x. Even with MAIN’s excessive premium, that is nonetheless lower than their 3-year average of 59% which signifies it might be barely undervalued, particularly within the present atmosphere. OCSL’s 3-yr common low cost of -2.30% signifies it might be overvalued barely.

Creator creation

However because of the top quality of each, I view paying a small premium as acceptable, particularly for these targeted on revenue. These two haven’t solely secure and secure dividends, however each have grown their NAVs through the years which speaks to their administration. And being top quality enterprise, paying a small premium just isn’t out of the norm, particularly for many who pay dividends. And with excessive rates of interest seemingly coming to an finish, traders ought to get pleasure from the additional revenue for so long as they will.

That is additionally compared to the 2 largest BDCs by market cap ARCC who trades at 1.1x to NAV and Blue Owl Capital Company (OBDC) who trades at 1.0x. However as I discussed earlier within the article, Essential Road Capital normally trades at a notable premium as a result of their lengthy monitor file of month-to-month dividends.

I normally like a larger margin of security and a reduction to NAV when seeking to put money into BDCs. However because of the present state of rates of interest, I view each as buys proper now, particularly if charges stay right here all through 2024. In that case, I anticipate each corporations to proceed rewarding their shareholders with particular dividends for the foreseeable future due to their predominantly floating price portfolios.

Conclusion

Each Essential Road Capital & Oaktree Specialty Lending Corp have performed properly within the present macro atmosphere as a result of their predominantly floating price portfolios. Though the Fed has said a better for longer atmosphere on a number of events, I believe we’re nearer to the tip of the speed hike cycle. In flip, many BDCs will doubtless minimize their particular and supplemental payouts leaving traders with much less revenue to develop their dividend snowball. However I do not see this occurring till the second half of the 12 months so traders get to get pleasure from the additional dividends for a while. Their costs may also decline probably as a result of traders rotating again into lower-yielding investments as BDCs grow to be much less engaging. However proper now, that is the right alternative for traders with a shorter-term outlook to make use of the revenue from each of those high-quality BDCs to develop their revenue earlier than charges are minimize someday in 2024.