Juanmonino

Funding thesis

Our present funding thesis is:

- U-Haul’s (NYSE:UHAL) diversified income stream and robust enterprise mannequin positions it completely as a long-term compounder. The corporate has a powerful asset base that’s rising quickly, alongside a market-leading place in the UK. We suspect it could actually proceed to develop at an analogous price to traditionally achieved, whereas sustaining its EBITDA-M of ~35%.

- The corporate’s FCF place shouldn’t be ideally suited for short-term actors however you will need to recognize these are into laborious belongings and might be lowered aggressively if required. Money move from operations has grown according to income, whereas many belongings nonetheless have to ramp up.

- The one obstacle at the moment confronted is the timing of price cuts and the potential of a recession, which given the upcoming nature of both or each, we imagine indicators a maintain ranking.

Firm description

U-Haul is a distinguished participant within the do-it-yourself shifting trade, providing a complete vary of companies together with truck and trailer leases, storage options, and packing provides. Established in 1945, the corporate is headquartered in Phoenix, Arizona, and has grown into one of many largest and most acknowledged names within the shifting and storage enterprise.

Share worth

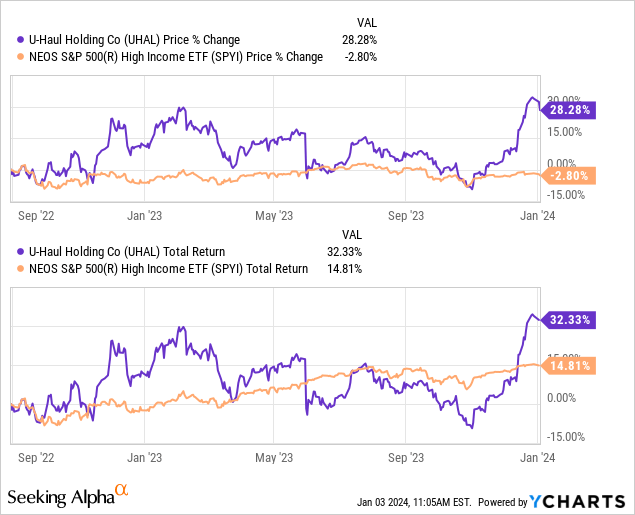

UHAL’s share worth efficiency has been sturdy because it was listed, gaining over 20% at a time when the broader market has broadly traded flat, significantly when contemplating that is closely weighted towards the magnificent 7.

Monetary evaluation

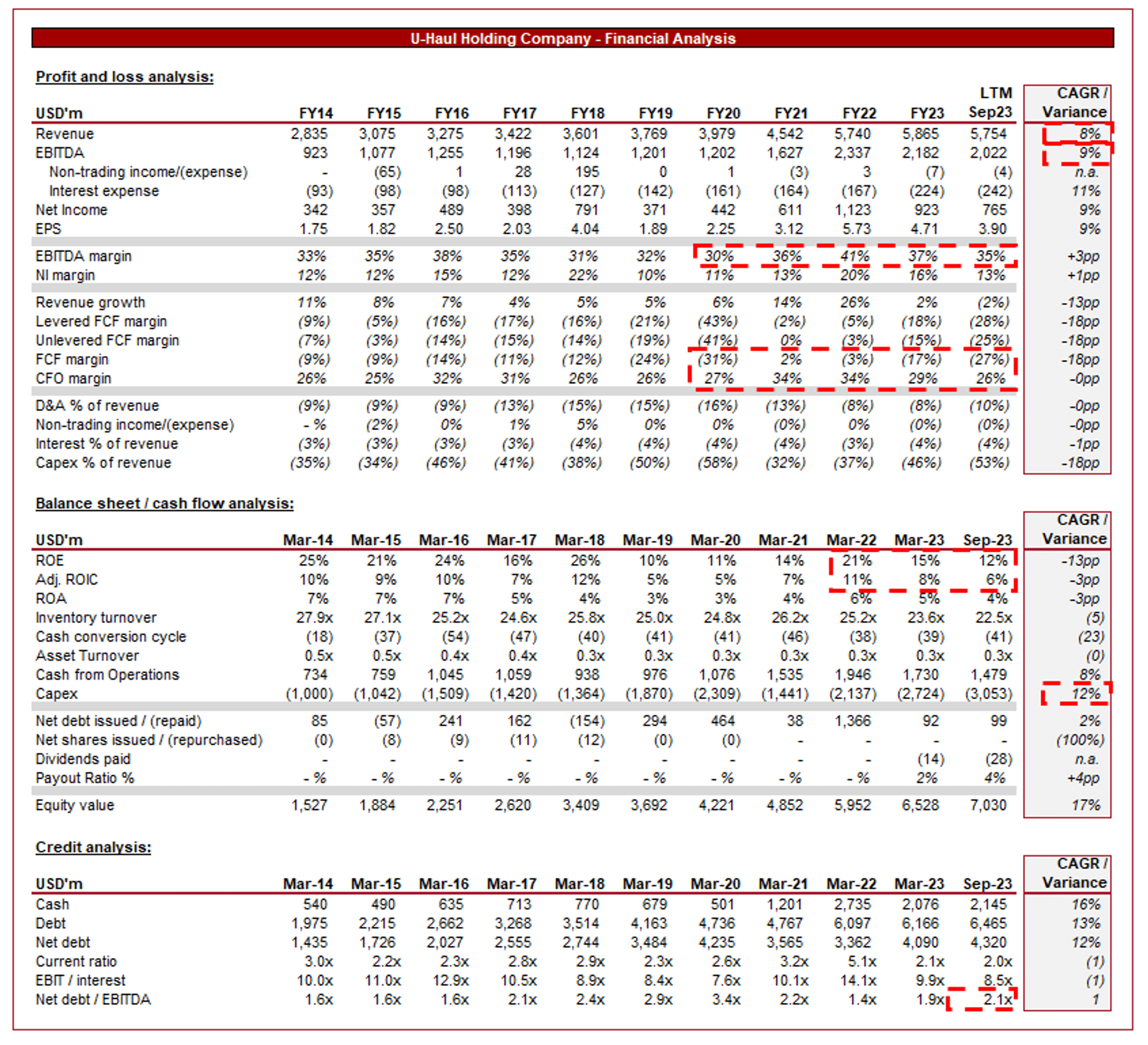

U-Haul financials (Capital IQ)

Offered above are UHAL’s monetary outcomes.

Income & Business Elements

UHAL has generated spectacular progress over the past decade, with a CAGR of +8% into the LTM interval. Along with this, its EBITDA-M has broadly traded flat.

Enterprise Mannequin

UHAL primarily operates within the tools rental trade (~69% of FY22 income), providing a variety of merchandise equivalent to vehicles, trailers, and towing tools. Prospects lease this stuff for transporting items throughout relocation, with the corporate having a protracted historical past with this section and a recognizable model that’s extremely seen on its automobiles.

Along with shifting tools, UHAL is more and more increasing its storage options by means of a community of self-storage amenities (~11% of FY22 income). Prospects can lease storage models for short-term or long-term wants, positioned to behave as an extra income stream with lowered cyclicality.

UHAL pioneered the idea of DIY shifting, empowering prospects to deal with their relocations independently. This idea appeals to people searching for a cheap and versatile shifting answer, with UHAL remaining essentially the most cost-effective and versatile choice out there given its nationwide asset base and scale throughout the US.

U-Haul goals to be a one-stop-shop for patrons throughout the shifting course of. Past truck and trailer leases, the corporate gives a variety of extra companies, which collectively (alongside funding and curiosity earnings) comprise ~20% of FY22 income.

Aggressive Positioning

UHAL’s sturdy aggressive place relies on the next key elements:

- Scale – UHAL has a major scale throughout the US, each within the areas it companies and the variety of out there belongings for customers. UHAL has over 180k vehicles, 120k trailers, 46k towing units, and 58k sqft of cupboard space. That is vital to making a community impact. For instance, a shopper can transit merchandise throughout the US and sure has the choice to drop off its rented car at one other UHAL location, minimizing the prices to UHAL and thus the value it expenses.

- Advertising and marketing and Branding – UHAL’s advertising and marketing efforts and robust branding contribute to visibility. That is vital as in lots of instances, customers may have restricted information of high quality and so will search well-known and revered manufacturers when making a alternative.

- Adaptation to Market Tendencies – UHAL has tailored to market traits and technological developments. On-line reservations and digital instruments, for instance, improve the client expertise. This has staved off competitors and related technology-driven innovation in different industries.

- Innovation in Providers – The introduction of extra companies, equivalent to storage options and shifting assist, diversifies UHAL’s choices by making the lifetime of its (potential) buyer simpler. This innovation permits the corporate to cater to a broader vary of buyer wants and is a degree of differentiation that many native gamers can’t compete with.

- Strategic Location Placement – UHAL’s monetary assets have allowed it to strategically place its areas, usually in proximity to residential areas and shifting hotspots, making certain that prospects can simply entry its companies.

Mobility Business

UHAL competes with Penske Truck Leasing, Finances Truck Rental, and Enterprise Truck Rental, alongside many native gamers in what is a reasonably fragmented trade.

Competitors Dynamics revolve across the following elements:

- Pricing and rental phrases.

- Fleet measurement and distribution community.

- Customer support and satisfaction.

From the evaluation above, and basic buyer suggestions analyzed, UHAL is actually a market-leading participant that’s importantly not shedding sight of the easy issues it must do nicely to maintain its prospects glad.

Key trade traits embody:

- Distant Work Impression – Shifting patterns in shifting on account of distant work has the potential to contribute to larger migration from bigger cities and states outward.

- Broader Mobility Tendencies – Societal traits, equivalent to elevated mobility and relocations, contribute to a constant demand for UHAL’s companies.

- Sustainability – UHAL is investing closely within the modernization and growth of its fleet (mentioned intimately later), though Administration should contemplate the necessity to transition to scrub vitality within the not-to-distant future and the related price profile to take action.

- Digital Integration – Additional expertise and digital integration, equivalent to in good reservations (potential for AI-managed inventory to well allocate belongings to areas) and customer support, has the potential to streamline operations and asset administration to maximise returns.

- Financing surroundings – The present financing surroundings will make it troublesome for companies to broaden their fleet / storage capability. Though this can be a potential challenge for UHAL, the enterprise is probably going one of many best-placed within the trade, thus creating the potential for market share progress.

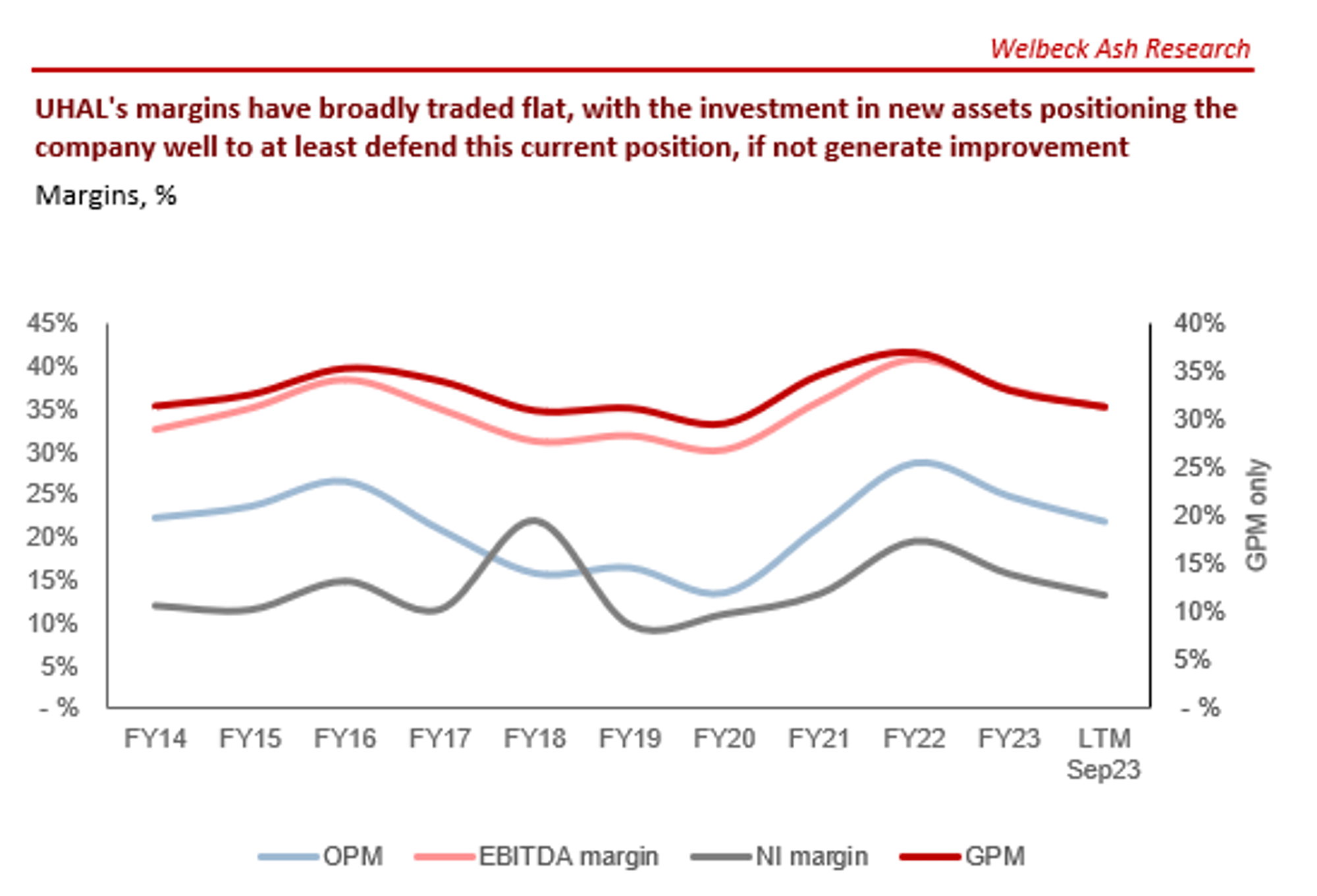

Margins

Margins (Capital IQ)

UHAL’s margins have been flat for the final decade, implying new product launches and adjustments within the combine have been impartial at a minimal. On condition that EBITDA-M is a cool 35%, that is a powerful achievement.

It’s value highlighting that the corporate has appreciable D&A bills given its asset-heavy nature (~10% of income), nevertheless, these are solely accounting prices with no related money influence, permitting for a money move from operations (”CFO”) margin of 26%.

Wanting forward, we suspect UHAL can keep this present degree at a minimal, though has scope for appreciation if funding in fashionable belongings can enhance unit economics.

Quarterly outcomes

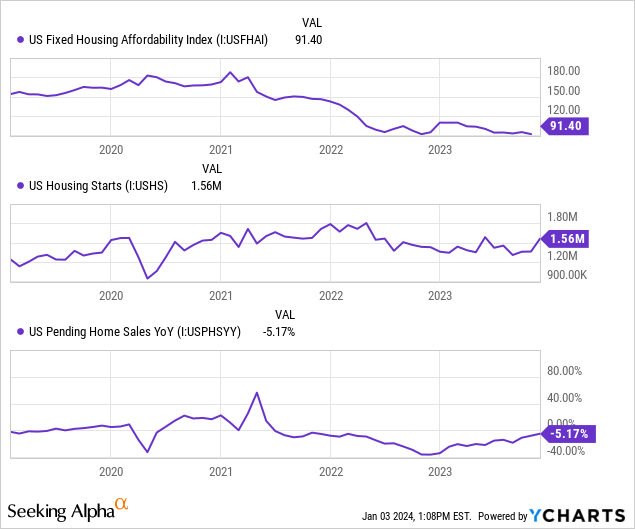

UHAL’s top-line income progress has materially slowed in current quarters, with progress of (2.1)%, (0.8)%, (3.6)%, and (3.1)% in its final 4 quarters. Importantly, nevertheless, margins have but to stabilize, implying additional decline is feasible.

The corporate’s decline is nearly wholly attributable to its rental section, because the storage section continues to develop nicely whereas occupancy exceeds 80%. The rental enterprise has a level of cyclicality related to the well being of the housing market, as customers primarily demand mobility companies when buying a brand new residence.

With charges elevated and the influence of inflation, customers are experiencing a value of dwelling disaster. When compounding the influence of elevated rates of interest on the affordability of properties, now we have seen a speedy slowdown within the housing market. It seems customers are awaiting a decline in charges, which many expect in 2024, lowering the demand for mobility companies.

That is more likely to be a problem within the first half of 2024, though you will need to observe we don’t see UHAL shedding any aggressive benefit because of this. The corporate continues to spend money on new belongings to develop its income technology potential, positioning it nicely as soon as charges fall.

Stability sheet & Money Flows

Regardless of vital funding in its asset base, it’s value instantly recognizing that UHAL is reasonability financed, with restricted solvency danger. The corporate has an ND/EBITDA ratio of two.1x whereas its curiosity protection is 8.5x.

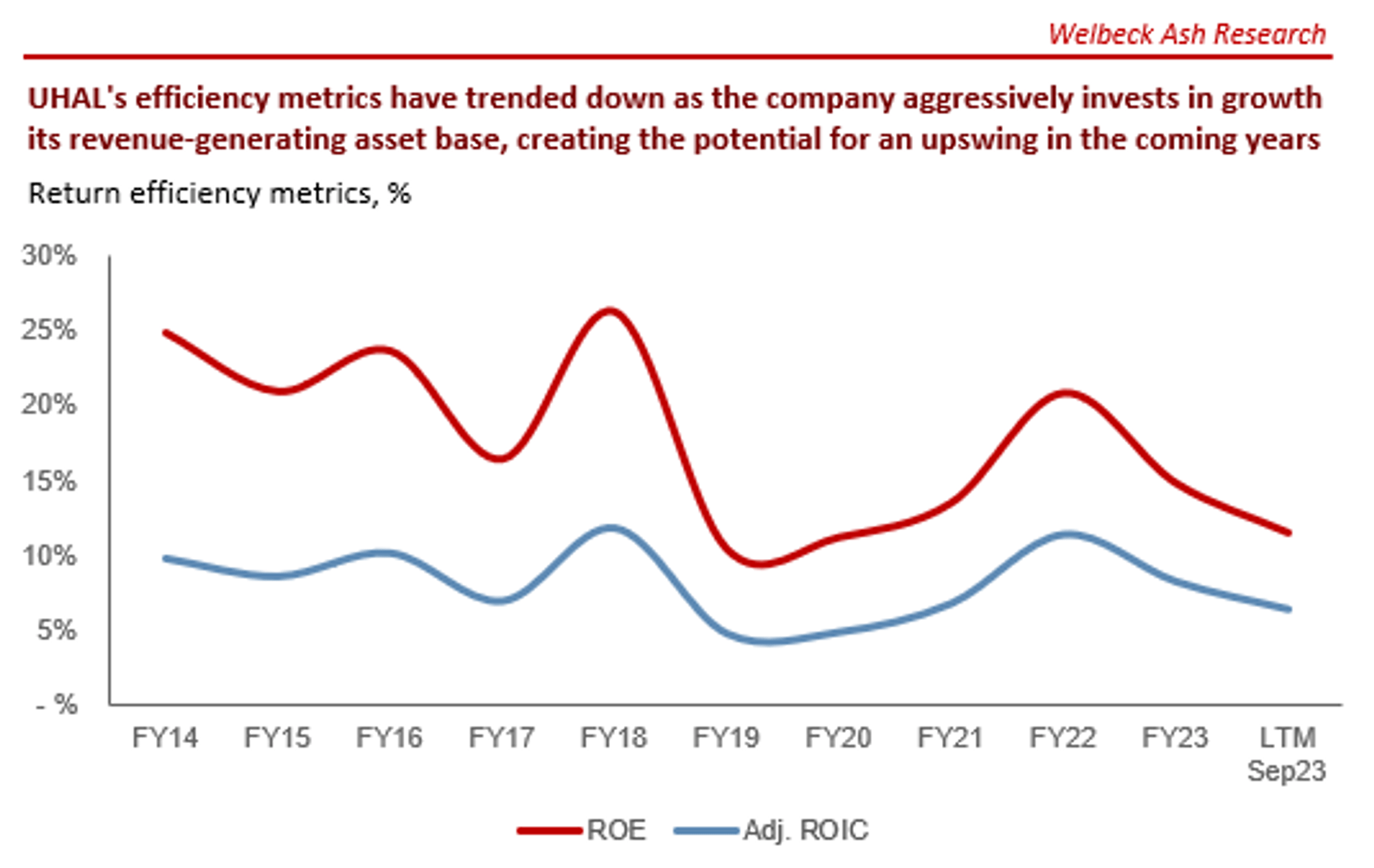

While a lot of this paper has made UHAL seem good, there may be one clear downside. The corporate’s FCF technology has been closely destructive, owing to capex commitments at the moment exceeding 50% of income (offset considerably by asset gross sales). This primarily pertains to funding in revenue-generating belongings, which we count on to be accretive over time as they transition towards a mature degree as soon as on-line.

This requires traders to be affected person with UHAL, with no distributions at the moment and a declining ROE. We imagine its sturdy margins and progress trajectory ought to make sure that as soon as Capex begins to step down, returns will speed up.

Returns (Capital IQ)

Business evaluation

In search of Alpha

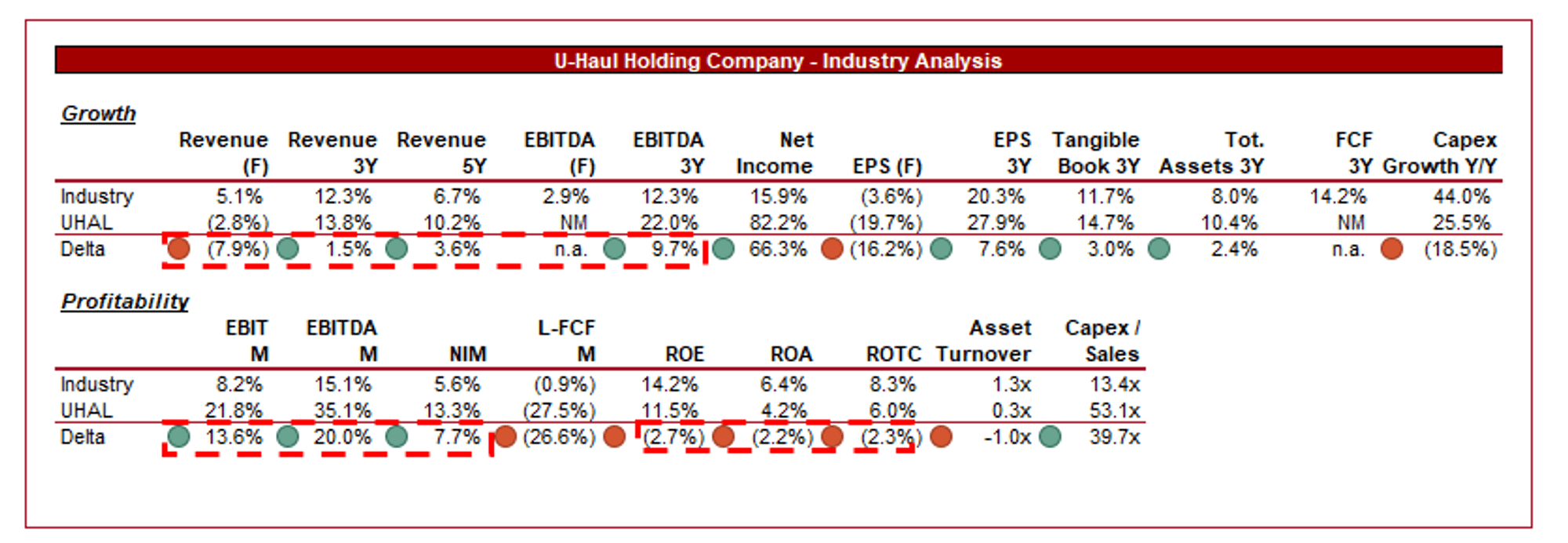

Offered above is a comparability of UHAL’s progress and profitability to the typical of its trade, as outlined by In search of Alpha (20 corporations).

UHAL performs nicely relative to its friends, with superior progress and profitability. Importantly, even when factoring in its excessive D&A prices, the corporate boasts a superior NIM. This can be a reflection of its sturdy aggressive place out there, alongside its funding in future progress.

Valuation

Valuation (Capital IQ)

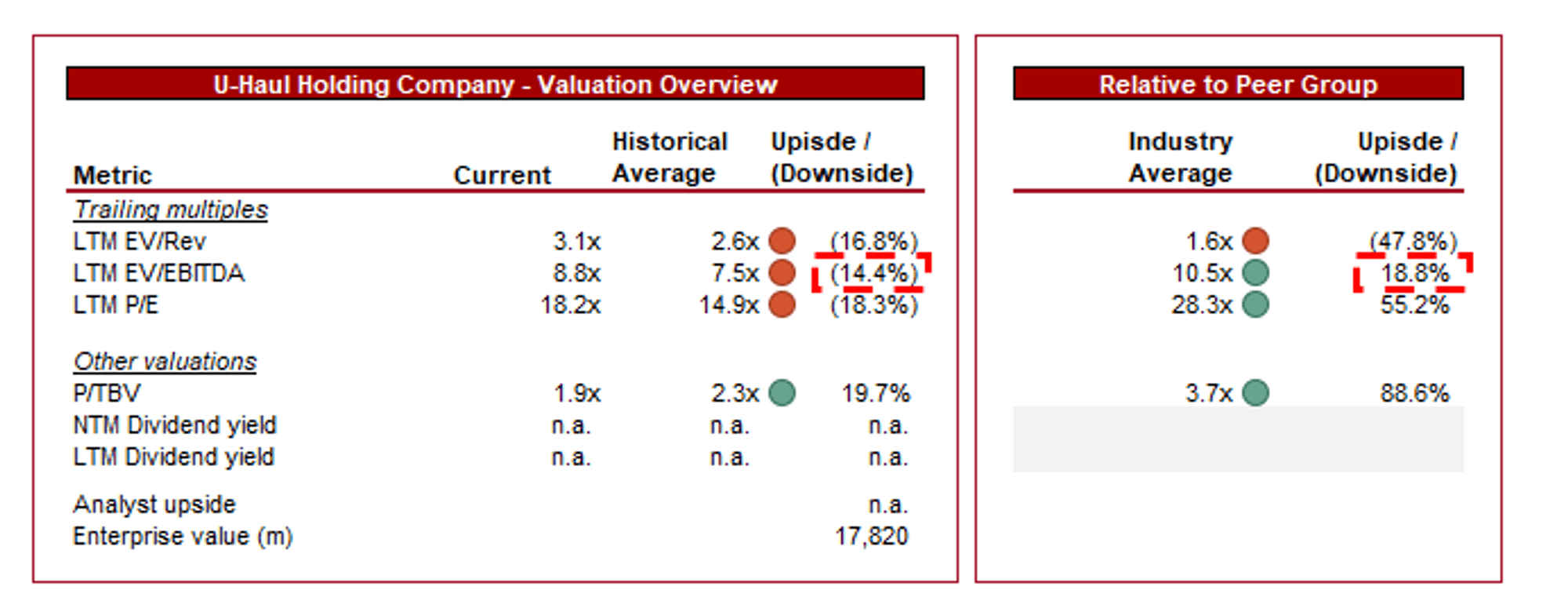

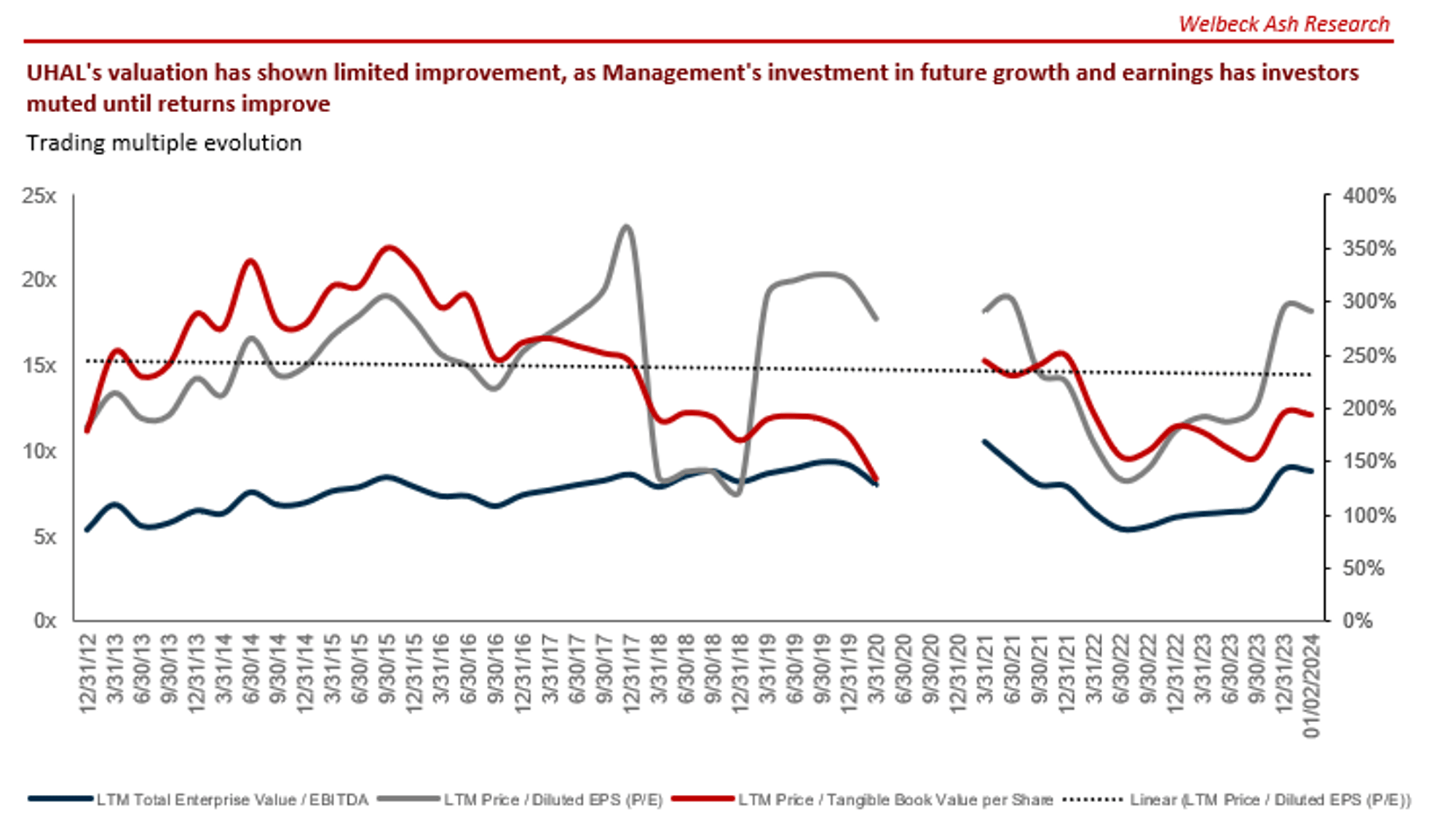

UHAL is at the moment buying and selling at 9x LTM EBITDA and 1.9x ebook worth. This can be a premium to its historic common on an EBITDA foundation.

A small premium to its historic common seems cheap in our view, owing to the elevated asset base, growth of various income streams, and the potential for growth as market situations enhance.

This mentioned, the corporate is buying and selling at a reduction to its peer group and its historic common ebook worth. We imagine each reductions are illustrative of the money move danger. The corporate has, and continues to, make investments closely in future earning-generating belongings, which creates execution danger. If the unit economics of those belongings change, its potential returns are materially impacted.

Broadly, we imagine the corporate is probably going barely undervalued, as its monetary superiority exterior of FCF, and the relative “safety” of laborious asset funding (actual property and automobiles), imply a deep low cost is unwarranted.

Valuation evolution (Capital IQ)

Key dangers with our thesis

The important thing danger and catalyst elements revolve wholly round financial growth. The timing of rate of interest actions, whether or not the US enters a recession, and even election outcomes may have a fabric impact on the US economic system and thus UHAL’s monetary efficiency. We see restricted share worth growth till the housing market improves.

Remaining ideas

UHAL is a high-quality enterprise in our view, and an attention-grabbing instance of going “all in” on future profitability. The corporate seems nicely managed, with growth at an inexpensive tempo and clever strategic decision-making to develop the corporate’s wider income profile.

This mentioned, we imagine traders will profit from endurance, given the significance of the housing market’s well being on the expansion potential of the corporate. With price hikes extremely unlikely in Q1-Q2 2024, we see restricted share worth motion.