Urupong

UiPath’s (NYSE:PATH) progress has picked up considerably during the last 12 months and is prone to proceed accelerating. Whereas sentiment in direction of software program shares has improved considerably over the previous 12 months, UiPath is without doubt one of the few corporations that has demonstrated a transparent enchancment in fundamentals. UiPath’s valuation has improved on the again of this, however nonetheless seems low relative to friends. That is seemingly partially on account of the truth that UiPath’s losses stay comparatively giant. Margins will enhance in time, however it’s truthful to query the gross sales effectivity of the corporate. UiPath can be in a class that hasn’t engendered a lot love from traders. Whereas UiPath is the clear market chief, questions have continued to drift across the prospects of RPA. UiPath’s platform growth in all probability ensures it stays related, however the class stays too near the strategic pursuits of Microsoft (MSFT) for my liking.

Market

UiPath’s enterprise continues to be impacted by the weak demand environment. This has been most obvious on the low end of the market amongst small and mid-sized companies. The vast majority of UiPath’s churned prospects fall into this phase and this seemingly explains why the corporate’s buyer depend has stagnated. Whereas this can be a trigger for concern, it’s softened by the truth that UiPath has nonetheless managed to reaccelerate progress on this setting.

Competitors

There are questions round UiPath’s long-term aggressive positioning however to this point, the corporate has confirmed dominant. UiPath has established a big market share inside RPA and the rising capabilities of its platform have solely solidified its lead.

Whereas Microsoft is usually pointed to as a menace, UiPath continues to recommend that they aren’t actually in direct competitors. Microsoft is targeted on private productiveness, whereas UiPath is targeted on enterprise-grade productiveness. There may be in all probability fact to this, however Microsoft may view RPA as a strategically vital class. The power of RPA to enhance productiveness and tie collectively disparate workflows and purposes may strengthen the remainder of Microsoft’s enterprise.

Whereas ServiceNow can be usually thought-about a menace, UiPath has instructed that it sees ServiceNow in lower than 1% of its offers. ServiceNow is targeted on explicit use instances, whereas UiPath’s platform has broad applicability. There may be additionally some stage of cooperation between ServiceNow and UiPath, as ServiceNow is probably the most downloaded connector for UiPath’s platform.

UiPath

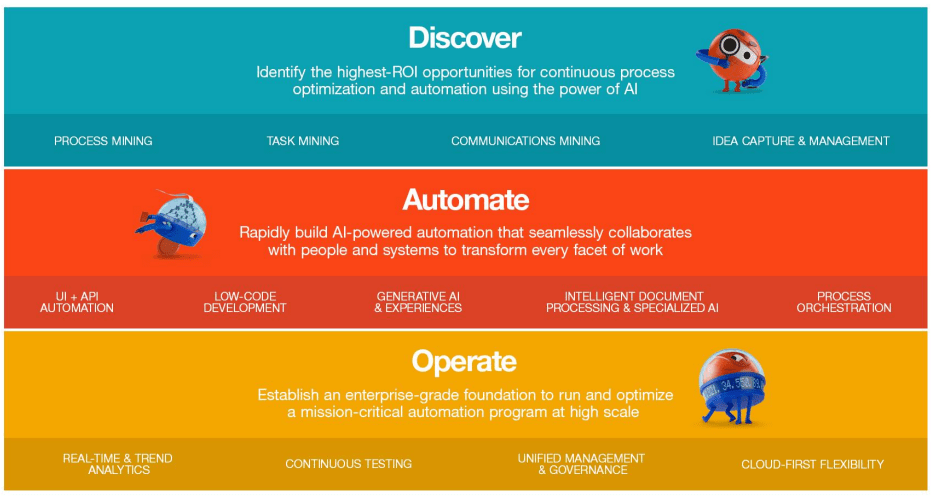

UiPath continues to increase the capabilities of its platform with new merchandise, which each expands the corporate’s addressable market and strengthens its aggressive place. Specifically, I’d recommend that course of and activity mining, together with options that make utilizing the platform simpler (low-code growth and autopilot), strengthen UiPath’s enterprise.

Autopilot is an assistant that gives a variety of AI-powered capabilities to builders, testers, analysts and frontline personnel, and is designed to boost the consumer expertise throughout the UiPath platform.

UiPath additionally lately launched Clever Doc Processing. Clever Doc Processing leverages AI to allow anybody to coach AI fashions to know paperwork. Generative AI is used to assist with annotation, classification and knowledge extraction.

Determine 1: UiPath’s Platform (supply: UiPath)

UiPath lately shifted its go-to-market movement to give attention to promoting your entire platform to senior administration. This has additionally meant a better give attention to giant organizations that present important growth potential. This transfer in all probability goes hand in hand with the increasing capabilities of UiPath’s platform however can also be in response to weak point on the decrease finish of the market.

Monetary Evaluation

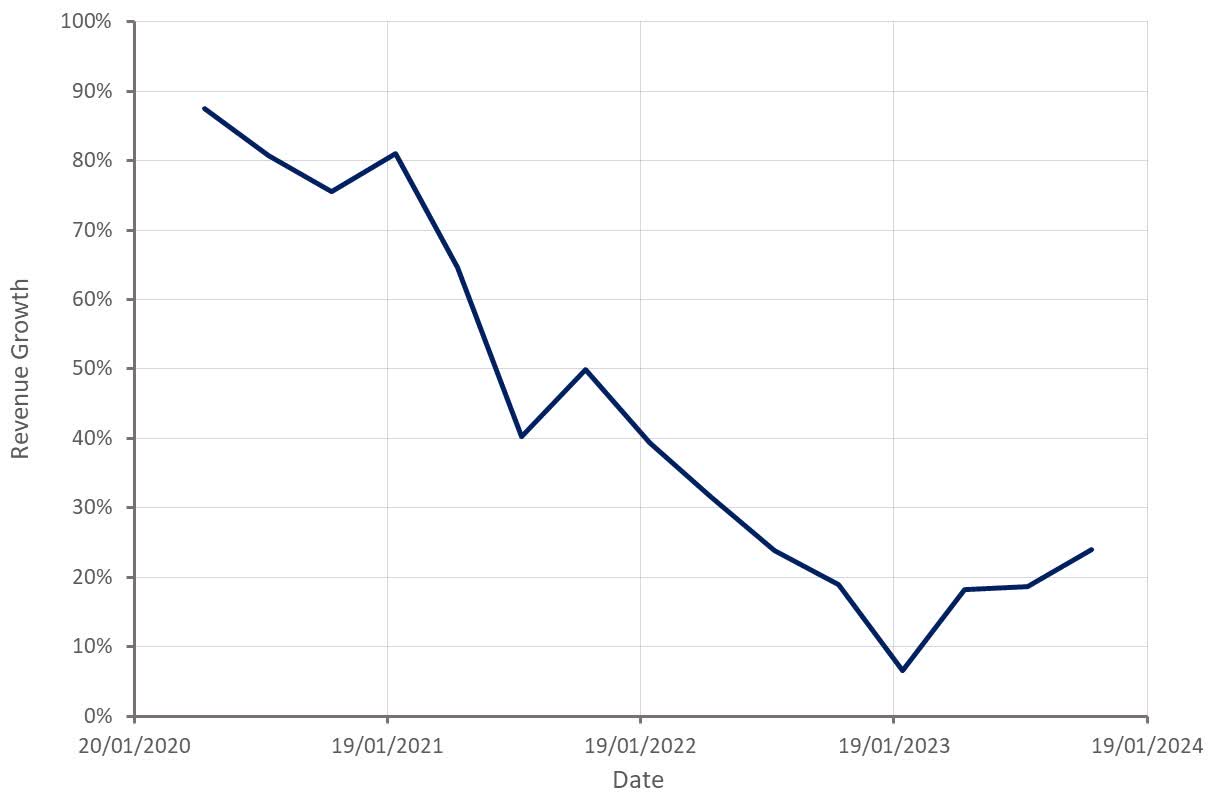

UiPath’s income was up 24% YoY within the third quarter, together with a 24% enhance in ARR. UiPath’s progress is now up considerably from the lows of late 2022, and extra importantly, this progress acceleration seems to be sustainable.

The supply of the surge in progress is considerably unclear although. UiPath remains to be struggling so as to add to its buyer base, with progress largely pushed by growth amongst present prospects. Progress may very well be as a result of elevated breadth of UiPath’s platform and elevated give attention to top-down gross sales at bigger organizations or better buyer demand for automation. The rise in progress is much less obvious at public rivals, suggesting the development is UiPath particular.

UiPath is at present solely guiding to 381-386 million USD income within the fourth quarter, which might characterize roughly 24% progress on the midpoint. This steering is probably going fairly conservative although, and I’d count on one thing extra like 390-400 million USD income. UiPath has instructed that the macroeconomic setting continues to be variable, which is probably going behind the conservative steering.

Determine 2: UiPath Income Progress (supply: Created by writer utilizing knowledge from UiPath)

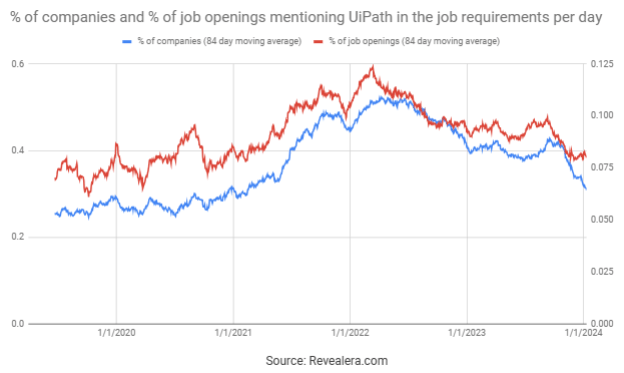

UiPath has struggled to increase its buyer base in latest quarters, which is probably going the results of elevated churn amongst smaller prospects and the corporate’s shift in focus in direction of bigger organizations. This seems prone to be ongoing because the variety of job openings mentioning UiPath within the job necessities continues to fall. UiPath’s giant buyer depend continues to extend at a wholesome clip although, suggesting the corporate’s go-to-market technique is working.

Determine 3: Job Openings Mentioning UiPath within the Job Necessities (supply: Revealera.com)

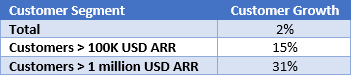

Desk 1: UiPath Buyer Progress (supply: Created by writer utilizing knowledge from UiPath)

UiPath’s greenback based mostly web retention fee was a wholesome 121% within the third quarter. Given the corporate’s give attention to increasing the breadth of its platform and driving adoption inside bigger organizations, this metric might be extra vital than the shopper depend. UiPath’s dollar-based gross retention was 97% within the third quarter.

Determine 4: UiPath Prospects (supply: Created by writer utilizing knowledge from UiPath)

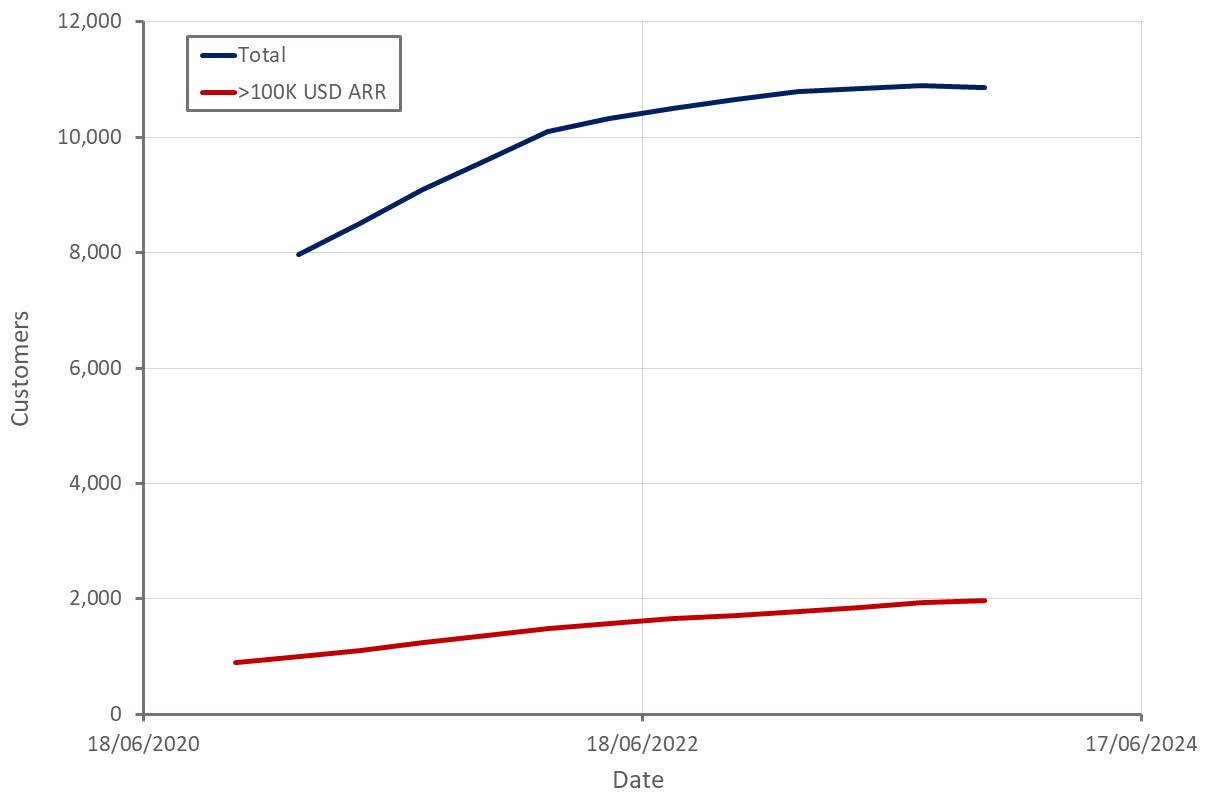

UiPath’s gross revenue margins stay excessive and have been pretty steady. Whereas this can be a constructive, it’s also largely reflective of UiPath’s reliance on on-prem income.

Determine 5: UiPath Gross Revenue Margin (supply: Created by writer utilizing knowledge from UiPath)

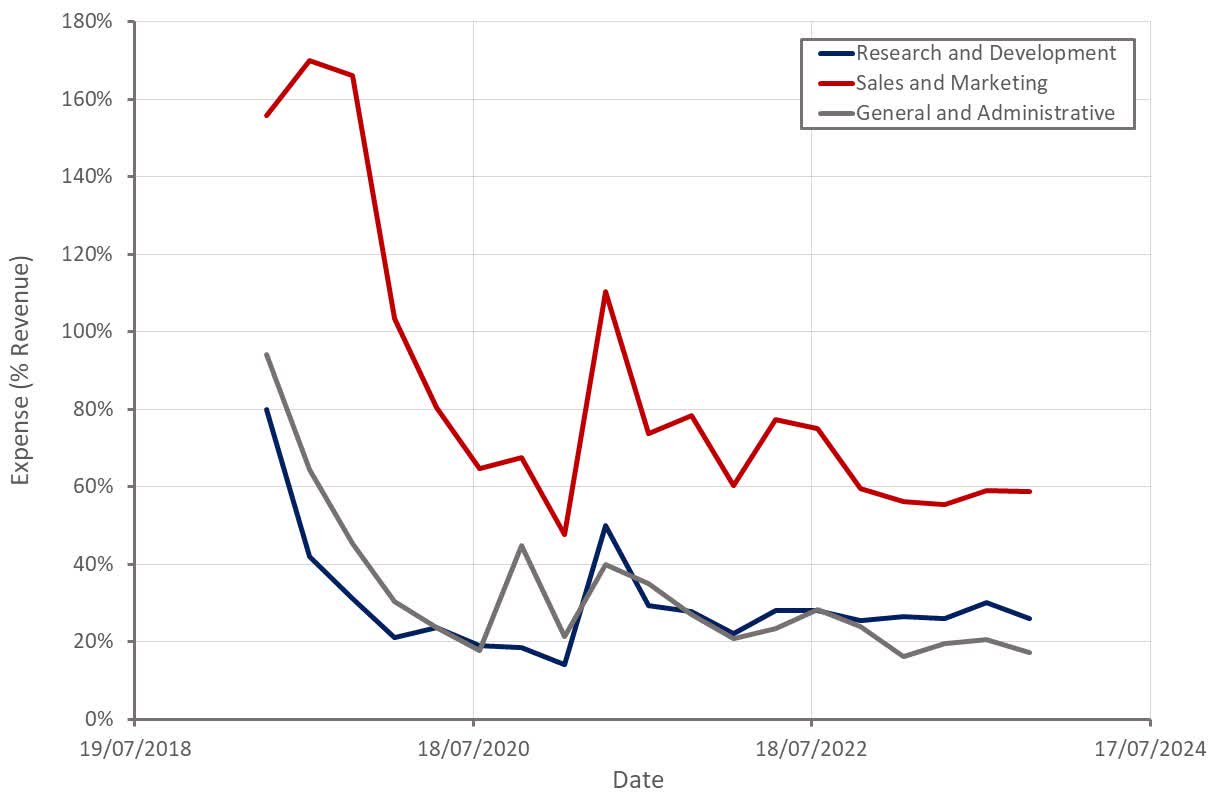

UiPath’s losses stay comparatively giant given the corporate’s dimension and progress fee. That is largely on account of giant gross sales and advertising and marketing bills which have to this point failed to enhance with scale. Finally, I imagine UiPath’s excessive gross retention fee will result in stable profitability, however it’s also in all probability truthful to query the corporate’s effectivity. That is presumably on account of the truth that UiPath is concentrating on enterprise scale automation. That means adoption is a strategic choice for patrons that requires shut scrutiny and excessive contact gross sales. UiPath has instructed long-term margins are prone to be around 20%.

Determine 6: UiPath Working Bills (supply: Created by writer utilizing knowledge from UiPath)

Conclusion

UiPath is the clear chief inside a rising market. This could usually warrant a premium valuation, however traders could also be skeptical of RPA. UiPath’s progress can be inefficient however low churn ought to imply the corporate turns into extremely worthwhile in time. If sentiment in direction of the class improves there may be important room for UiPath’s income a number of to increase. Significantly if the corporate’s progress continues to speed up in coming quarters.

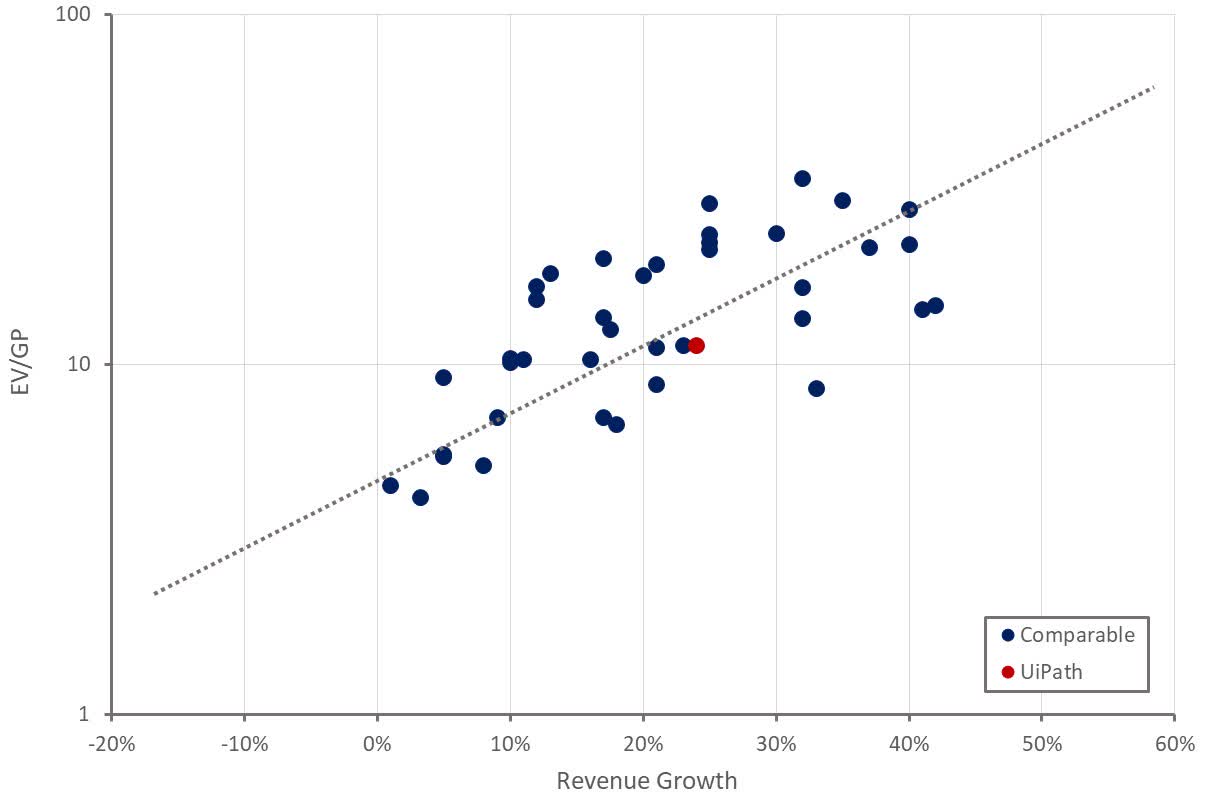

Determine 7: UiPath Relative Valuation (supply: Created by writer utilizing knowledge from Searching for Alpha)