UiPath (NYSE:PATH) shocked investors with a remarkably poor outlook for fiscal 2025. And to be clear, as we headed into this earnings report, I was bullish on PATH.

However, I know from experience that there’s no point in compounding one poor investment decision, through sunken cost biases, with another poor investment decision.

In fact, I believe that the only way to outperform the market is by being upfront and recognizing one’s mistakes. Everyone makes investment decisions. But the amateur blames someone else, while the professional blames themselves and works to rectify and recoup their poor decision.

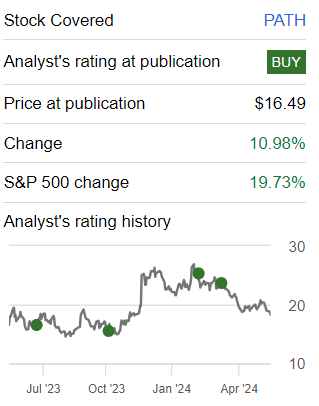

As it stands right now, including the premarket sell-off of 30%, PATH is being priced at 50x forward operating profits. A completely unjustified premium for what it offers investors.

Rapid Recap

In my previous article, I said,

[…] after a rocky few years, UiPath is turning around its prospects, and for now, the stock is attractively valued.

Author’s work on PATH

With the benefit of hindsight, this turns out to have been a falsehood. UiPath was able to pull together an alluring narrative and convince many notable investors of its strong market positioning. But alas, aside from an alluring narrative, there wasn’t enough to support its valuation.

UiPath’s Near-Term Prospects

UiPath creates software to help businesses automate repetitive tasks. That’s the pitch.

Think of it like a digital assistant that can handle routine work, such as data entry. UiPath’s software, often called a “robot” or “bot,” can do these mundane tasks quickly and accurately. This helps customers save time, reduce errors, and allow employees to focus on more important work.

Now, beyond its narrative, the reality is slightly less compelling. The departure of UiPath’s CEO, Rob Enslin, introduces untimely uncertainty during this critical period.

Additionally, UiPath described a challenging environment with slower deal closures and increased scrutiny on multi-year contracts, particularly affecting mid-market customers.

The inconsistent execution, including contract challenges and changes in sales compensation, has led to its outlook being dramatically altered from 90 days ago.

Therefore, given this context, let’s now delve into its financials.

UiPath’s Guidance Negatively Surprises

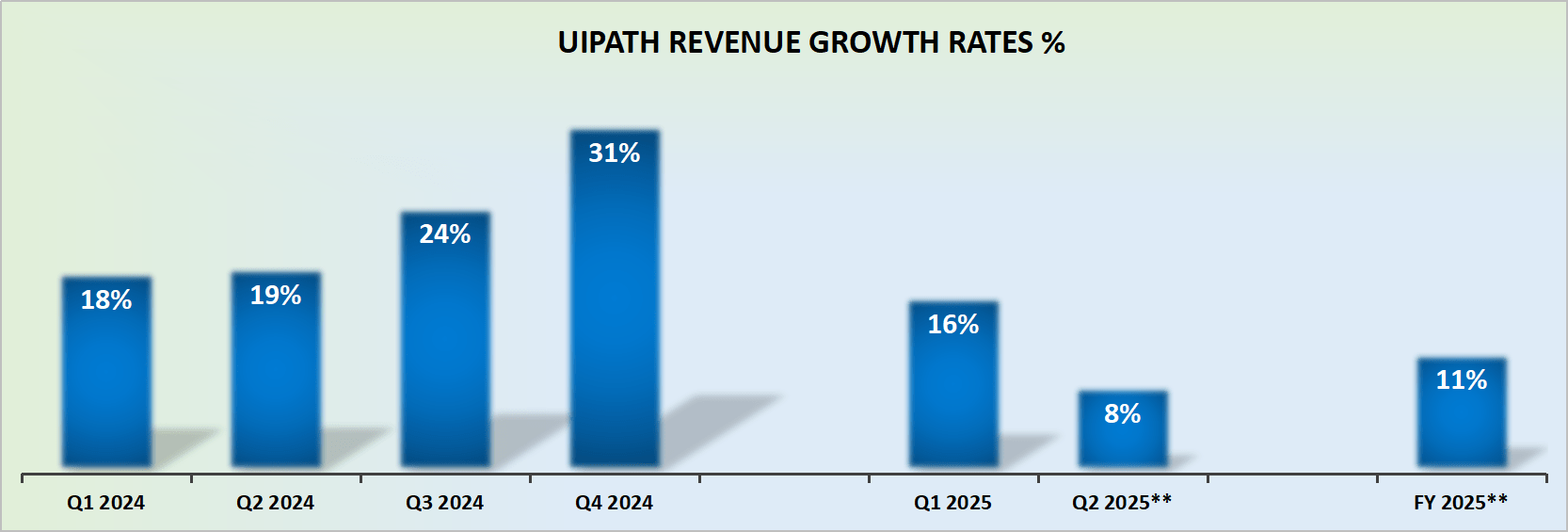

PATH revenue growth rates

A lot can be forgiven about growth companies. Indeed, a lot of a CEO’s colorful stories can be bought into provided the company continues delivering strong growth. Essentially, a growth company must deliver strong growth.

What a growth company must not do, in any conditions, is pull back on its guidance. This, my fellow readers, is one cardinal sin that cannot be forgiven. And that’s the sin that UiPath committed.

And not only that, but to downwards revise a company’s full-year guidance just 90 days after the previous result, by no less than approximately 1,000 basis points at the midpoint of the range? Oh my, that leads to a complete and unmitigated loss of faith in the company’s colorful stories. And along with that, the premium that investors are willing to pay.

Including the premarket drop of 30%, PATH is being priced at 50x forward operating profits.

For a while, this thesis was one of a company that could be counted on for some reacceleration of its topline, combined with rapidly improving profitability.

More specifically, UiPath was supposed to be growing its non-GAAP operating profits from $233 million last year to approximately $300 million in this fiscal year. And now?

Now, not only is there not going to be any increase in profitability, but the profitability is actually expected to shrink by 35% y/y.

Given this context, are investors truly likely to pay 50x forward non-GAAP operating profits? Evidently not.

The Bottom Line

In conclusion, UiPath has taken investors on a wild ride with a bleak outlook for fiscal 2025, leading to a substantial premarket sell-off and raising serious doubts about its valuation.

Initially, the promise of UiPath’s automation solutions convinced many prominent investors of its potential. However, the departure of its CEO and a challenging economic environment have exposed cracks in the narrative, resulting in slower deal closures and inconsistent execution.

The company’s drastic revision of its full-year guidance, just 90 days after its previous forecast, shattered investor confidence and highlighted the cardinal sin of growth companies: pulling back on guidance.

As investors reassess the 50x forward operating profit valuation, it’s clear that UiPath’s once alluring tale has taken a turn for the worse. After all, in the unforgiving world of investments, failing to deliver on growth is a sin too grievous to be pardoned.