maybefalse

I have been long Intel Company (NASDAQ:INTC) inventory for a number of years, and was a bit shocked by the response of the inventory value on the current information the place Intel broke down the losses on their foundry enterprise. Intel announced their foundry misplaced $7 Billion {dollars} final 12 months, and can lose extra this 12 months. Whereas it definitely has some which means, a few of it’s also how Intel makes use of their accounting, and it simply means their different divisions are rather more worthwhile. It isn’t damning for the corporate; we already knew the corporate is not the place it must be in manufacturing maturity, know-how and effectivity. The big investments in new websites and course of R & D had been all the time going to be an enormous drag on the corporate till they may translate into advantages. These advantages are, and had been all the time meant to be, sooner or later.

I need to begin with lots of this text shouldn’t be based mostly on chilly info, as a result of we’re trying ahead to nodes that we do not have full data for, and the longer term can also be by no means sure. Inventory costs look ahead, so do I, and so we’ve got to make the very best of what we’ve got now to attempt to finest estimate the longer term.

Some Fundamentals

So, let’s begin with some fundamentals. Intel not solely designs their chips, however additionally they manufacture (most of) them. They’ll use exterior corporations, specifically TSMC (TSM), when it is sensible. Many think about TSMC to be forward technologically, and though that is not utterly true, it’s shut. Intel’s 7 is best than something TSMC has when it comes to uncooked efficiency at pretty absurd energy eventualities (which Intel does use), however in nearly each different manner, Intel 7 is behind. And that is vital, as a result of it is a sign of what Intel values, or no less than did, and what TSMC does.

Intel 4 is tough to categorize, but it surely does not appear any extra environment friendly than Intel 7 in energy use, as Meteor Lake makes use of basically the identical structure as Raptor Lake, and does not display clear clock pace enhancements in laptop computer chips. It additionally does not appear to have the uncooked efficiency of Intel 7, based mostly on the maximum clock speeds we see. It’s much more dense although.

I ought to level out, names like 3nm, or 10nm, are usually not significant. As Intel mentioned, they may simply as simply name their node “George,” as it is not an precise measurement anymore, however only a title. So, for instance, it is uncertain something in Intel 7, or TSMC 3nm, is definitely 7nm, or 3nm, and if there’s, it is purely coincidental. Firms will attempt to make the title significant, so, you’ll count on Intel 4 to be extra dense than Intel 7 (which it’s), however on the finish of the day, it is only a title. And processes with the identical quantity are usually not equal; Intel 3 and TSMC’s 3nm will probably be considerably totally different, as every firm locations a special emphasis on their design objectives.

Even now, nobody makes processors that clock as excessive as these based mostly on Intel’s 7 process. It is probably TSMCs processes are usually not as effectively fitted to this, though clock pace can also be based mostly on structure, so it is not a certainty. However this can be a clear indicator of what Intel has traditionally thought of an important, and which TSMC doesn’t prioritize to the identical extent. I point out this as a result of this sample will lengthen into the longer term, though I think to a lesser extent.

Intel’s Present and Future Nodes

Intel has proudly talked in regards to the 5N4Y plan, which suggests 5 nodes in 4 years. Whereas it good Intel has launched two actual nodes in these 4 years, it’s miles much less spectacular than they might have you ever imagine. Intel 7 is a (spectacular in some methods) derivation of 10nm, so is not a brand new node. It is an improved node. Intel 4 and Intel 3 are basically the identical, or for those who favor, two half nodes, however both manner depend as one actual node. Intel 20a and 18a are related. It is nonetheless a formidable achievement, contemplating their points with 14nm and 10nm nodes, but it surely’s actually nonsense in the way it’s offered, and to dilute the accomplishment by being deceptive.

Proper now, Intel 7 is the dominant node utilized by Intel, with Intel 4 now ramping up with Intel’s Meteor Lake processors (however just for the CPU a part of the chiplet; loads is made by TSMC). Intel 4 is actually an inside node, though it does have no less than one external customer. Intel 3 may be very intently associated to Intel 4, and would be the node Intel affords to exterior prospects, and also will be Intel’s final FinFET node. Intel 7 makes use of what is known as DUV (Deep Ultraviolet Lithography), which is a comparatively method on forefront processes, and requires extra steps (multi-patterning) to create the tiny transistors in fashionable nodes. This provides price, and might decrease yields, making Intel 7 a really costly node.

Did Intel care? Not that a lot, since they had been promoting costly processors, and that largely masked (forgive the pun) the expense of the node. Intel 4 partially makes use of EUV, which is an abbreviation of Excessive Ultraviolet Lithography, to a restricted extent, which simplifies the method in comparison with a pure DUV method. A really crude mind-set about it’s, is slicing with a sharper knife. Intel 3 will enhance the usage of EUV, which lowers the quantity of steps wanted even additional, and thus decrease price.

Wafer price is essential exterior of the context of Intel promoting its personal processors. It has been estimated the expense of an Intel 7 wafer is roughly the identical as what TSMC expenses for theirs, even with their earnings, so it is very inefficient. Intel 3 must be higher, however in response to Intel, nonetheless dearer than TSMC’s 3nm nodes (of which there are a number of).

What to Count on

Does this actually matter? Not that a lot, as a result of the battle of Intel 3 and TSMC’s 3nm is actually over earlier than Intel even launched their node. Firms have to start out designs effectively prematurely, so we all know TSMC has largely received this spherical. The “2” (which means Intel 18A vis-a-vis TSMC/Samsung 2nm) is the place there will probably be some kind of battle, and clearly the place Intel will do higher. For that motive, I am not going to waste an excessive amount of time on Intel 3, it is not going to generate some huge cash or curiosity, though it might generate curiosity as Intel improves the method with new derivations, and for individuals who want to keep on with FinFETs. However, it should by no means be an enormous node.

Intel 18a, nevertheless, appears promising in some methods. CEO Pat Gelsinger has indicated he’s betting the corporate on it, though together with his penchant for useless drama, it is not that vital an announcement. Rather a lot needs to be decided when it comes to the way it will match up towards TSMC 2nm. Intel will probably be forward by utilizing PowerVia, which ought to enhance effectivity and efficiency. However, that is not a transparent indicator of superiority, as there are different traits which are in all probability extra salient.

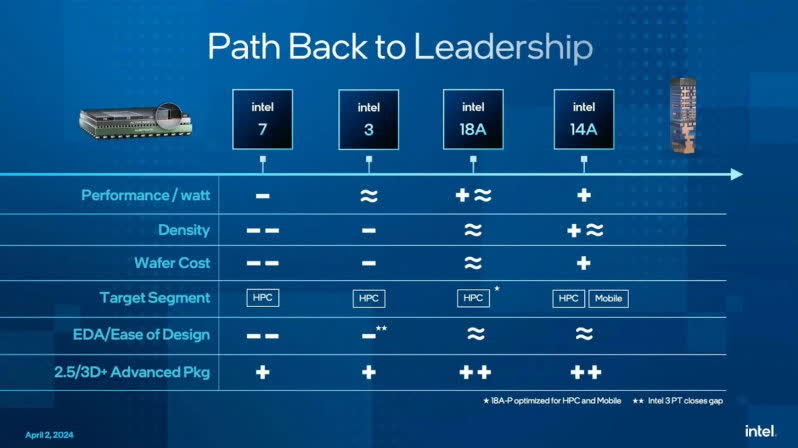

Beneath is Intel’s picture describing how they view the aggressive panorama going ahead.

Intel

For one, Intel is in some methods a prisoner of its personal success. TSMC has by no means had tremendous excessive performing nodes, since it is a comparatively small market in comparison with the cellphone market, for instance. Intel needs actually good clock speeds, as a result of they promote merchandise which profit from them. Outdoors of Superior Micro Gadgets (AMD), which is fortunate to have 20% market share in the PC segment, they do not have many purchasers that require this. Effectivity? Sure. Density? Sure. This isn’t to say TSMC cares nothing about efficiency, and it is dreadful. It isn’t. It is simply inferior to Intel’s, and certain will not be. And they’re superb with that.

Intel has traditionally cared about efficiency first. And possibly second as effectively. After all, the others matter, even to Intel, however when it comes all the way down to it, they’re going to take clock pace. Even now, Intel’s CCG group dominates their revenue, so it is not a misplaced precedence. However, for exterior prospects? It isn’t as extensively helpful as different elements.

My guess, based mostly on data and estimates by individuals who know greater than I do, and data given by Intel, is 18A will lead in efficiency, be roughly equal in energy effectivity, no less than as cost-efficient, however considerably much less dense (which is why I believe price effectivity will probably be good; they’re associated).

I believe it pretty apparent that density will probably be extra vital than absolute efficiency in additional eventualities that exterior prospects are concerned in, however definitely 18A can have benefits, and will probably be aggressive. It isn’t even that vital within the higher scheme of issues although. Intel has an enormous benefit over TSMC in that nearly everybody exterior of TSMC needs one other forefront fab to select from, as competitors can solely assist them. That is the place it ends although. TSMC has the benefit of being a identified associate, and one which has many profitable partnerships. No main firm will threat their main line on Intel but, and even Intel has indicated this. On prime of this, TSMC shouldn’t be a competitor in any market their prospects are in. And naturally, their PDAs are extra mature, and Intel continues to be studying issues TSMC has identified for years.

With this actuality, Intel cannot probably even come near TSMC in attracting as many exterior prospects within the 18A period. I believe a practical manner to take a look at it’s, Intel 3 goes to be fairly unsuccessful in attracting exterior prospects, and that battle has just about been fought, and misplaced. If it is even been fought. This isn’t to say it will not assist Intel promote their very own merchandise, no less than servers, however for exterior prospects, it is already been determined.

18A is actually step one. It is in all probability extra enticing from a technical perspective vis-a-vis TSMC 2nm, than Intel 3 is when in comparison with TSMC’s a number of 3nm nodes. However, greater than that, corporations have had extra time to guage it, and Intel has had extra time to pursue them. It is nearly a pipe-cleaner node (not technically, 20A really is) for brand spanking new prospects within the sense that corporations will probably commit comparatively decrease quantity components to it, however not their most vital merchandise; the chance is simply too excessive. However, if these relationships work out and have success, it might begin a sample the place Intel can achieve momentum as their relationships mature, in addition to their expertise in working as a foundry.

I believe it is untimely to speak about 14A exterior of this context. I have never actually seen a lot on its technological deserves, so will not remark a lot about it. Intel will probably be utilizing High-NA EUV, however not a lot past that’s identified about it but. I believe they’ve a higher alternative with it than 18A, if for no different motive than these said above; extra mature relationships, and higher expertise. However, in the event that they screw up, that might simply work towards them as effectively.

Is Intel’s Technique Wise?

Many individuals think about this complete factor as too dangerous, both in investing an excessive amount of in new fabs and such, or in even holding the fabs as a part of the corporate. I’d say these are precisely why it is such a profitable components; it is extraordinarily tough for anybody else to enter this business, though Rapidus appears to be attempting. It is extraordinarily capital intensive, it takes a really very long time to construct the fabs and fill them, and it is also tough to develop the expertise and supporting know-how that permits exterior prospects to effectively make processors.

Then, you need to construct belief. Evaluate that with processor designs, the place we see cloud suppliers popping out with new inside solely designs on a regular basis. There’s additionally a synergy with having your personal fabs and designs, one which advantages Intel processors, even with their present fab know-how being largely behind.

It may take time, and cash. In case you’re a affected person investor, the payoff may be enormous. In case you’re not, it in all probability looks like Intel is killing itself. Even Intel is giving indications they don’t seem to be assembly expectations (which they won’t come out and say straight), by first saying they will not have any main product line on 18A, the 18A ramp being in 2026, and of their foundry information indicating the corporate doesn’t have to extend exterior income to make their manufacturing worthwhile.

Little question there’s some fact to this, as they will definitely enhance their effectivity and technological place. The corporate additionally indicated they count on to maneuver from outsourcing 30% of their manufacturing to twenty%, which is said to the earlier comment. We additionally see delays in construction of Intel’s new fabs. Put collectively, it is tough for me to not see this as Intel considering they might get rather more enterprise by this time, or no less than a lot stronger curiosity, than they’ve. And now they should put collectively a marketing strategy that extra realistically assesses the slower exterior income progress than was anticipated.

One firm I’ve not noted is Samsung (OTCPK:SSNLF). Sure, they type of, kind of, effectively, make superior transistors. In concept. At the very least in response to their revealed papers. And numbers they provide you with. Besides, they haven’t any loved success, no matter their rhetoric. Whereas historical past information Intel as typically having the very best processes, with TSMC at present having extraordinarily sturdy product traces. Even so, we will not say for certain Samsung will proceed to be non-competitive, however Intel has to purpose increased than this flightless chook, so I centered totally on TSMC. Intel could not should move TSMC in each metric, however they should be aggressive, and have benefits in some eventualities. I believe they’ll (and do), significantly in efficiency. However additionally they higher not be so severely deprived in every part else.

Nevertheless you take a look at it, the foundry enterprise goes to be a painful grind. It is tremendous costly, it is time consuming, and it is going to take a very long time earlier than it is very worthwhile. Firms are usually not going to leap ship en masse to the nice Intel foundries. They don’t seem to be nice anymore; it is not 2010. They not solely have to enhance capability and know-how, but in addition have all of the instruments in place for his or her prospects. They want expertise, which solely occurs slowly. After that, they want belief, and that’s even a slower course of. Intel has lots of good folks, and I believe they’re higher understanding this market now, and are being extra sensible about it. However even when they execute very effectively, it is nonetheless a really lengthy course of to turn out to be very worthwhile. It’s sensible to count on enchancment within the losses with the brand new nodes and higher focus, nearer time period, nevertheless.

After all, this text is essentially about their foundry, and doesn’t mirror the general alternatives of the corporate. After all, nodes like Intel 3 will affect their server line, for instance, and presumably very favorably, however I needed to focus extra on the exterior foundry enterprise. I’m nonetheless very optimistic on Intel as a complete, and even on the foundry enterprise. I believe it is a very tough enterprise to get into, but it surely additionally permits Intel to revenue in much more eventualities than promoting their very own processors straight. It additionally will generate earnings that may enable additional growth prices attainable, as every node is enormously costly. It is going to additionally enable Intel to make use of tools for much longer for trailing nodes that exterior prospects will nonetheless want lengthy after Intel’s merchandise wouldn’t discover them significant.

Conclusion

All of this convinces me that is the suitable technique for Intel Company. I by no means anticipated the foundry enterprise to be a fast payoff, and all the time simply needed to see iterative enchancment. We’re nonetheless actually early within the recreation, and whereas we see the know-how changing into extra aggressive, we do not see vital design wins but, or main prospects producing vital product traces at IFS. Nor would we count on to but, in order that half is inconclusive. We should always see some uptake on 18A, and hopefully continued momentum going ahead. However nevertheless you take a look at it, it is going to be gradual, and can take time for Intel Company to completely develop it.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.