UniFirst Company (NYSE:UNF) not too long ago obtained important consideration from buyers on account of recent implementation of new ERP and CRM techniques. In my opinion, analysts elevated their quarterly EPS expectations as a result of they count on web revenue development coming from new effectivity from automatization of sure processes. A 5 12 months dividend development charge of close to 24%-25% and up to date inventory repurchase of shares might deliver demand for the inventory very quickly. Apart from, I believe that UniFirst seems considerably undervalued.

UniFirst

UniFirst is an organization that gives large-scale masterwork companies for companies, industries, and workplace buildings. The corporate’s exercise extends to various kinds of cleansing companies that embrace uniforms that have been uncovered to radiation work amongst others.

UniFirst has its personal manufacturing and design capabilities for anti-flammable protecting clothes or clothes to be used in laboratories, together with a large line of merchandise for pants, T-shirts, jackets, and overalls amongst others.

The corporate additionally sells and rents cleansing provides for industries together with cleansing bogs and meals areas. The corporate additionally gives coaching in security practices for industries, distributors, and companies linked to the service.

In different phrases, this firm presents an built-in suite of cleansing companies, together with the manufacture, design, and distribution of security clothes, and its primary exercise consists of offering its shoppers with clothes and niknaks on a weekly foundation, amassing the objects used for later cleansing and reuse.

Throughout the year 2023, roughly 60% of the clothes distributed have been manufactured by the corporate in its three manufacturing amenities positioned in San Luis Potosí in Mexico, along with the plant in Managua, Nicaragua, in addition to different subcontracted producers that serve the overall price discount technique that the corporate maintains.

The benefit of getting its personal manufacturing capabilities is that it might probably supply its shoppers custom-made merchandise, establishing long-term contracts within the provide of security clothes and associated cleansing companies.

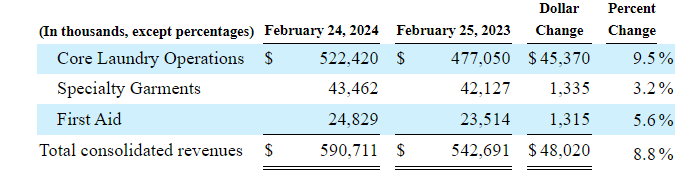

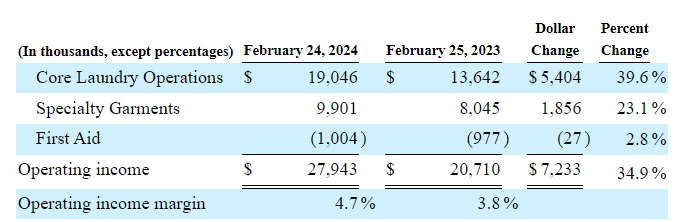

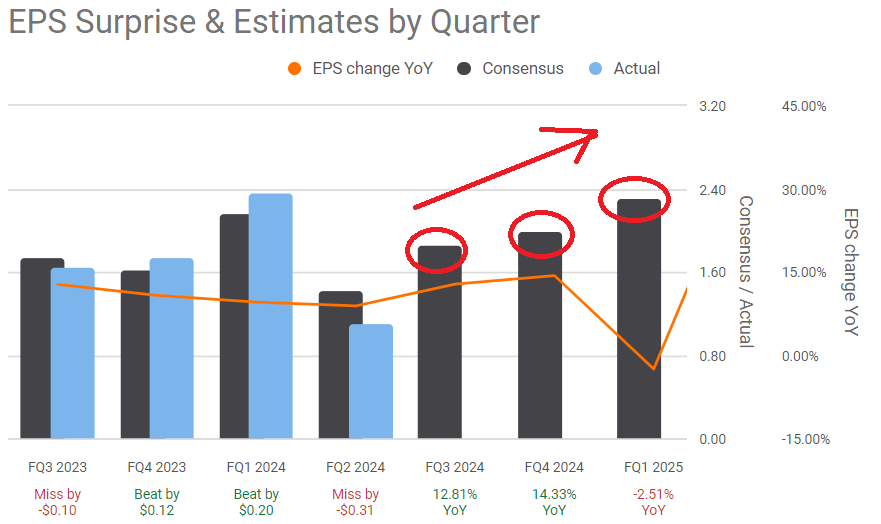

Within the final quarterly report, UniFirst reported important development in a number of areas in comparison with the identical interval final 12 months. We discovered near 8.9% increase in revenue and 34% enhance in working revenue. I additionally respect fairly a bit that CFO elevated to $106.7 million within the first half of 2024, which represents near 66.3% greater than what UniFirst reported in the identical interval in 2023.

Supply: 10-Q

Supply: 10-Q

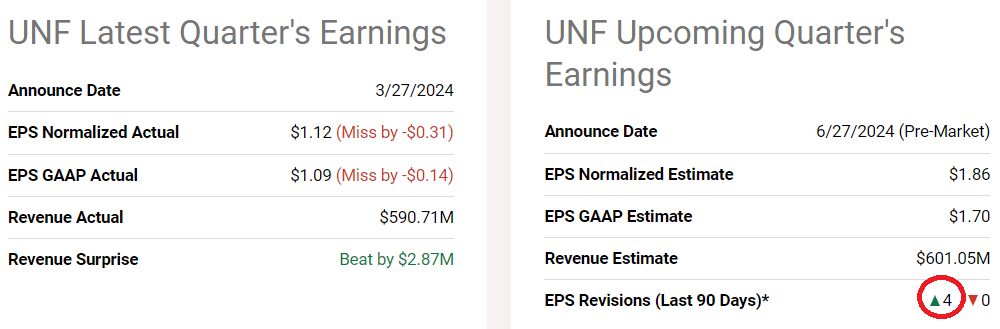

Although UniFirst didn’t ship higher than anticipated EPS, with higher than anticipated quarterly income, I believe that current enhance in CFO and web gross sales expectations are fairly helpful.

For the 12 months 2024, the corporate expects to report income near $2.415 billion and $2.425 billion. Apart from, 4 analysts on the market elevated their EPS expectations for the following quarter, and the consensus estimates for 2024 and Q1 2025 embrace EPS will increase.

Supply: In search of Alpha

Supply: In search of Alpha

Assessment Of Enterprise Segments, And 300k Energetic Purchasers

The corporate’s exercise is grouped into six enterprise segments, three of which correspond to the kind of service it gives, these being additionally current in Canada, and a sixth devoted to company exercise.

The actions similar to companies associated to the availability of security clothes in addition to their cleansing and reuse are meant primarily for industrial shoppers. None of those represented greater than 10% focus within the firm’s income in recent times, and by the top of 2023, there have been greater than 300 thousand lively shoppers, which UniFirst serves with 270 service areas below its operation. One of these service is by far the one which represents the best quantity of revenue for the corporate.

Alternatively, there’s the garment manufacturing section, organized from the aforementioned amenities in addition to the subcontracted producers, whose manufacturing is used totally throughout the earlier section, since it’s the clothes that it gives to its shoppers. On this sense, it’s value saying that over the past 12 months, 60% of the clothes distributed by the corporate got here from its personal manufacturing capacities, together with subcontracted industries, which additionally reveals that at the moment the demand for these companies exceeds the productive capability of the corporate.

The primary assist section, which represents the least revenue for the corporate, gives companies to its shoppers, with the availability of all of the merchandise and gadgets mandatory for emergency care inside its industries.

Steadiness Sheet

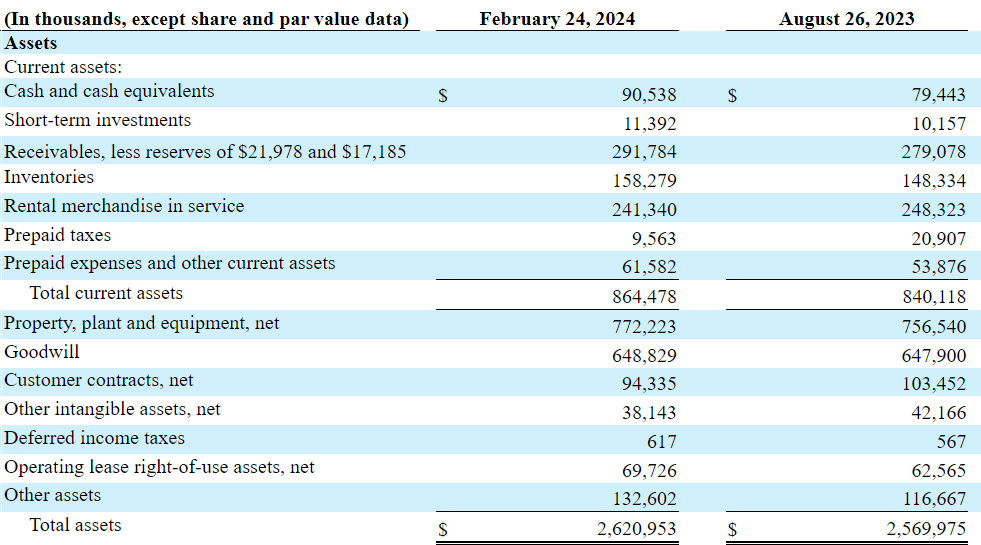

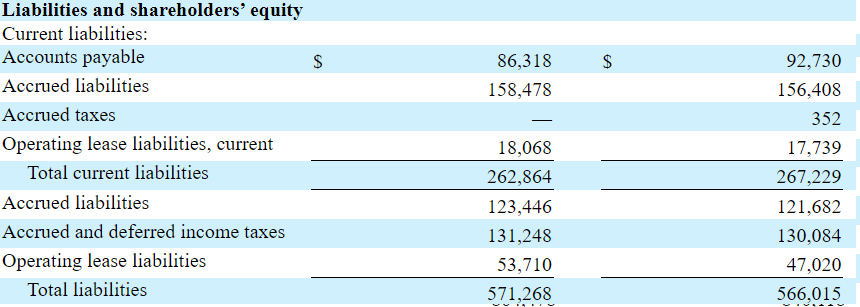

As of February 24, 2024, UniFirst reported $90 million in money, with rental merchandise in service near $241 million and accounts receivable of $291 million. The present ratio stands at near 3x, so I imagine that the corporate experiences a considerable quantity of liquidity. The asset/legal responsibility ratio is near 4x. In sum, the stability sheet seems fairly secure.

Supply: 10-Q

UniFirst doesn’t appear to report debt. Suppliers appear to supply financing. With quick time period accrued liabilities of $158 million and long run accrued liabilities of $123 million, complete liabilities are near $571 million.

Supply: 10-Q

Assumption 1: UniFirst Enjoys A Market That Grows At Near 4.6% CAGR, Which Could Push The Firm’s Web Gross sales Up

In accordance with market specialists, the workwear and uniforms market might develop at near 4.6% CAGR from 2022 to 2030. With this in thoughts, I imagine that UniFirst might report web gross sales development of a minimum of near 4.6%. Beneath my greatest case state of affairs and my worst case state of affairs, UniFirst consists of web gross sales development of round these figures.

Knowledge Bridge Market Analysis analyses that the workwear and uniforms market which was $24.26 billion in 2022, would rocket as much as $34.76 million by 2030, and is anticipated to bear a CAGR of 4.6% in the course of the forecast interval. Supply: Databridge Market Research

Assumption 2: The New ERP And CRM Initiatives Might Speed up Effectivity

UniFirst not too long ago reported a big quantity of bills associated to CRM and ERP initiatives, which I imagine might deliver important effectivity advantages within the coming years. Because of this, I imagine that UniFirst might ship will increase within the web margin from 2024 to 2033. I included these assumptions in my dividend fashions.

In fiscal 2022, we initiated a multiyear ERP venture that we at the moment anticipate will proceed by 2027, with early phases targeted on grasp information administration and finance capabilities adopted by subsequent phases with a powerful concentrate on provide chain and procurement automation and expertise. Supply: 10-Q

We check with our CRM and ERP initiatives collectively as our. For the 13 weeks ended February 24, 2024, we expensed $3.2 million of non-recurring prices associated to our Key Initiatives, primarily regarding our ERP venture. Supply: 10-Q

Assumption 3: Inorganic Progress Will Most Possible Carry Economies Of Scale And Enhance In Margins

The corporate’s technique is hybrid, and consists of the natural development of its companies and acquisitions associated to its growth, whether or not by storage or cleansing facilities or growth of its productive capacities. With this in thoughts and considering the stability sheet, I believe that new acquisitions might deliver extra web gross sales development, economies of scale, and web gross sales development.

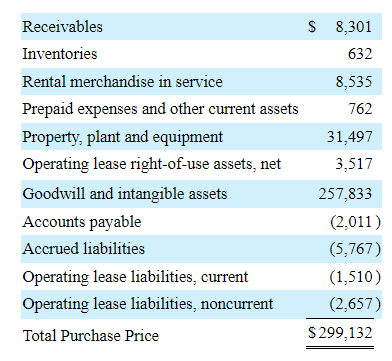

In 2023, as an illustration, the corporate reported the acquisition of belongings from Clear Holdco. Within the final quarterly report, the corporate offered details about the belongings acquired. The overall quantity of goodwill registered seems important, which I imagine implies that there’s a important quantity of price synergies included within the deal.

In the course of the third quarter of fiscal 2023, the Firm accomplished the acquisition of the enterprise and sure actual property belongings of Clear Uniform from Clear Holdco, Inc. and sure of its associates for an mixture buy worth of $299.1 million, web of money acquired. Supply: 10-Q

Supply: 10-Q

Assumption 4: Repurchase Of Inventory Could Decrease The WACC, And Improve The Inventory Valuation

UniFirst additionally declared a big quantity of inventory repurchases, which I imagine might speed up the demand for the inventory. In accordance with the final quarterly report, UniFirst might purchase $91.9 million of inventory within the close to future.

On October 24, 2023, our Board of Administrators approved a brand new share repurchase program to repurchase as much as $100.0 million of our excellent shares of Widespread Inventory, inclusive of the quantity which remained accessible below the prevailing share repurchase program authorized on October 18, 2021. Supply: Quarterly Press Release

The Firm repurchased 45,250 shares of Widespread Inventory for $7.9 million within the second quarter of fiscal 2024. As of February 24, 2024, the Firm had $91.9 million remaining below its current share repurchase authorization. Supply: Quarterly Press Launch

In my opinion, the inventory repurchases, dividend yield of near 0.8%, and dividend development of near 23% within the final 5 years could deliver new buyers. Because of this, we may even see a lower within the WACC within the coming years. I included a WACC shut to six.9% and seven.05%.

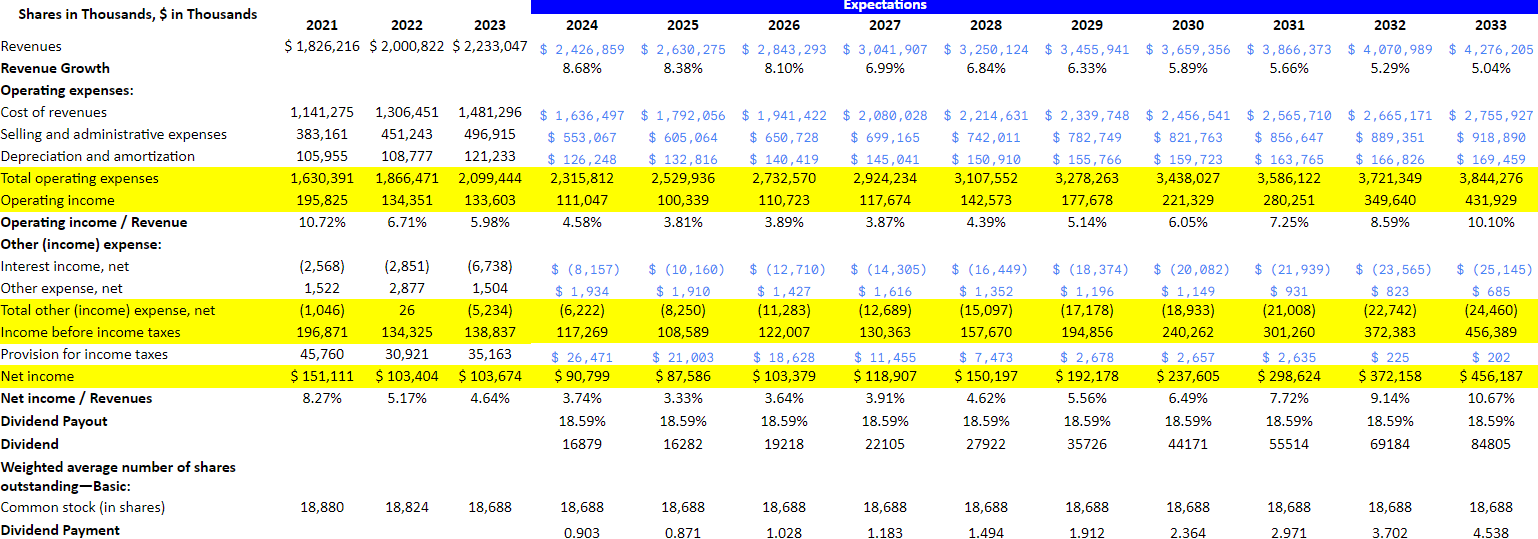

Beneath My Finest Case Situation, My Dividend Model Would Indicate A Valuation Of $287 Per Share

Beneath my greatest case state of affairs, I assumed that my earlier assumptions have been appropriate. Because of this, we may even see web gross sales development, reasonable will increase within the working margin, and revenue margin. It’s value noting that I included monetary figures that have been in step with my previous income statements. I imagine that my figures are conservative.

My expectations embrace 2033 income of $4276 million, with income development between 5% and eight%. I additionally assumed 2033 price of revenues of about $2755 million, with 2033 promoting and administrative bills near $918 million and depreciation and amortization value $169 million. T

Whole working bills would stand at about $3844 million, with working revenue near $431 million. Additionally together with 2033 curiosity revenue near $26 million, 2033 web revenue would stand at about $456 million.

Supply: My Expectations

If we assume a dividend payout of near 18%, which is in step with earlier figures, the 2033 dividend could be $84 million. Now, with a weighted common variety of shares excellent near 18.4 million, a WACC of 6.9%, and a PE ratio of 22x, my dividend mannequin implied a valuation of $287 per share.

Supply: My Expectations

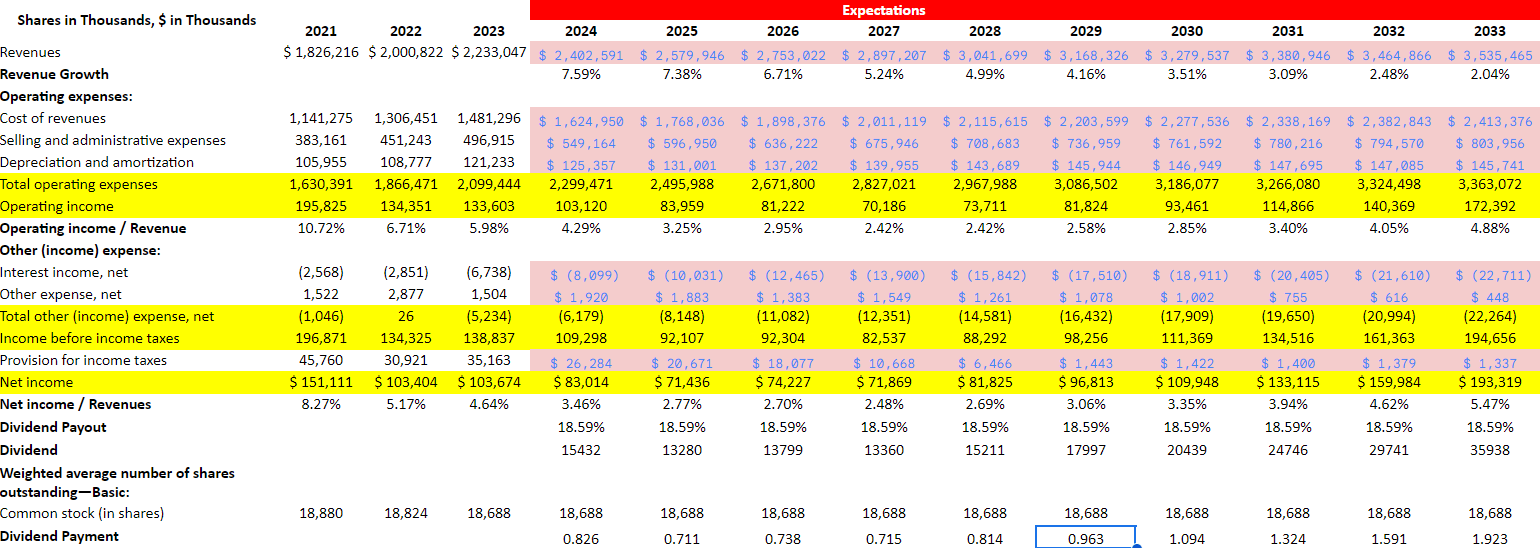

My Worst Case Expectations Together with Failed Assumptions

Beneath this state of affairs, I assumed 2033 revenues near $3535 million, with income development starting from 7% to 2%. Price of revenues could be near $2413 million, with promoting and administrative bills value $803 million and depreciation and amortization of about $145 million. 2033 complete working bills would stand at about $3363 million, with 2033 working revenue value $172 million.

My outcomes additionally embrace revenue earlier than revenue taxes value $194 million, provision for revenue taxes near $1 million, and 2033 web revenue of about $193 million.

Supply: My Expectations

Taking into consideration a dividend payout of 18%, 2033 dividend could be near $35 million. If we additionally embrace weighted common variety of shares excellent of 18.4 million, an exit PE of 20x, and a WACC of seven.05%, the implied worth would stand at $111.7 per share.

Supply: My Expectations

Opponents

The uniform rental and rental market is very aggressive. Though it’s dominated by a number of giant firms with nationwide attain, it additionally has the participation of greater than 600 small companies with regional attain in numerous inside markets. Main rivals of UniFirst are Cintas Company (CTAS), Alsco, and Vestis Company (VSTS). Competitors is anticipated to extend within the quick time period as a result of participation of latest producers and the rise in industries devoted to one of these manufacturing.

Dangers

In fact, any state of affairs of lower in industrial exercise in Canada and america might translate right into a drop in demand for the corporate’s services and products, primarily within the vitality trade, the place probably the most concentrated shoppers come from. Together with this, I’d take into account potential will increase or variations in transportation costs and different components that suggest a rise in prices in distribution and provide chains, which might undermine the corporate’s aims of sustaining a low-cost construction. As well as, the loss or lack of ability to retain its prospects in addition to dependence on subcontracted producers might be threat components for the corporate.

Conclusion

UniFirst is making important efforts to implement new ERP and CRM techniques, which can most probably deliver revenue margin will increase within the coming years. Furthermore, with a strong stability sheet, I believe that the corporate is in a very good place to amass extra targets, which can additionally complement the expansion of the workwear and uniforms market. Additionally considering the 5 12 months dividend development charge of near 24%-25% and the inventory repurchase program, the WACC could decrease within the coming years. There are clearly some dangers on the market from modifications in labor regulation, variations in transportation costs, or decrease demand than anticipated. Nevertheless, I imagine that UniFirst seems considerably undervalued.