Poulssen

Introduction

I feel everybody actually wants to think about including some shopper staples to their portfolio. Shopper staples typically don’t have the character to outperform however supply a security cushion in unsure occasions. Within the dividend development group shopper staples are additionally widespread due to their stability and consistency. Corporations on this sector are promoting merchandise which can be all the time in demand, so their earnings are way more steady and predictable. That is additionally the explanation that shopper staples are nicely introduced within the listing of dividend aristocrats and dividend kings. Take into consideration corporations just like the Procter & Gamble Firm (PG) , PepsiCo, Inc. (PEP) and the Coca-Cola Firm (KO).

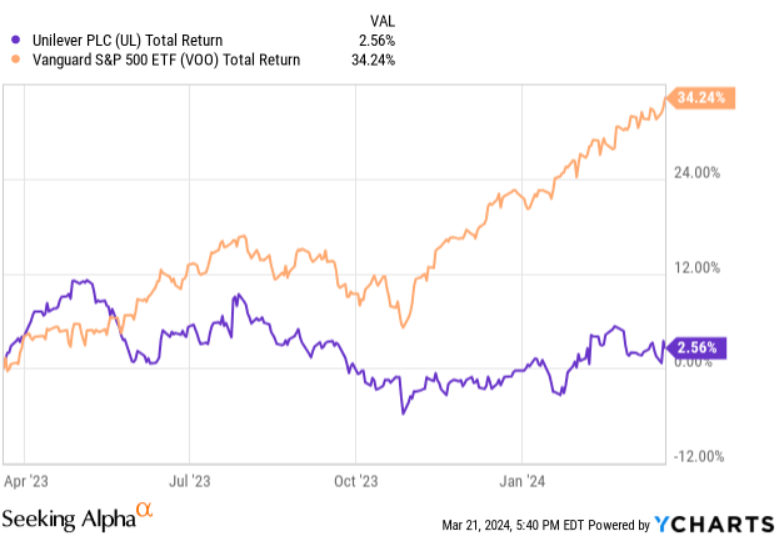

Probably the most well-known European shopper staple giants is Unilever PLC (NYSE:UL). On the 4th of December I wrote an article in regards to the firm and since this second in time the broader market is up significantly. It needs to be stated that the general shopper staple sector is unpopular in the mean time. Most traders are taking a look at expertise shares and are neglecting shares with a extra defensive nature.

UL efficiency vs benchmark (YCharts)

From all the patron staple shares, it seems to be like individuals are inclined to keep away from UL. The corporate is de facto underperforming within the long-term in comparison with its friends and traders typically are sad to say the least.

Nevertheless, I feel UL goes to do issues higher sooner or later. The corporate is making an attempt to reinvent itself and so they have already taken a number of actions.

Right this moment I need to replace my funding thesis with the latest data to find out if the corporate remains to be attractively valued.

Let’s get began!

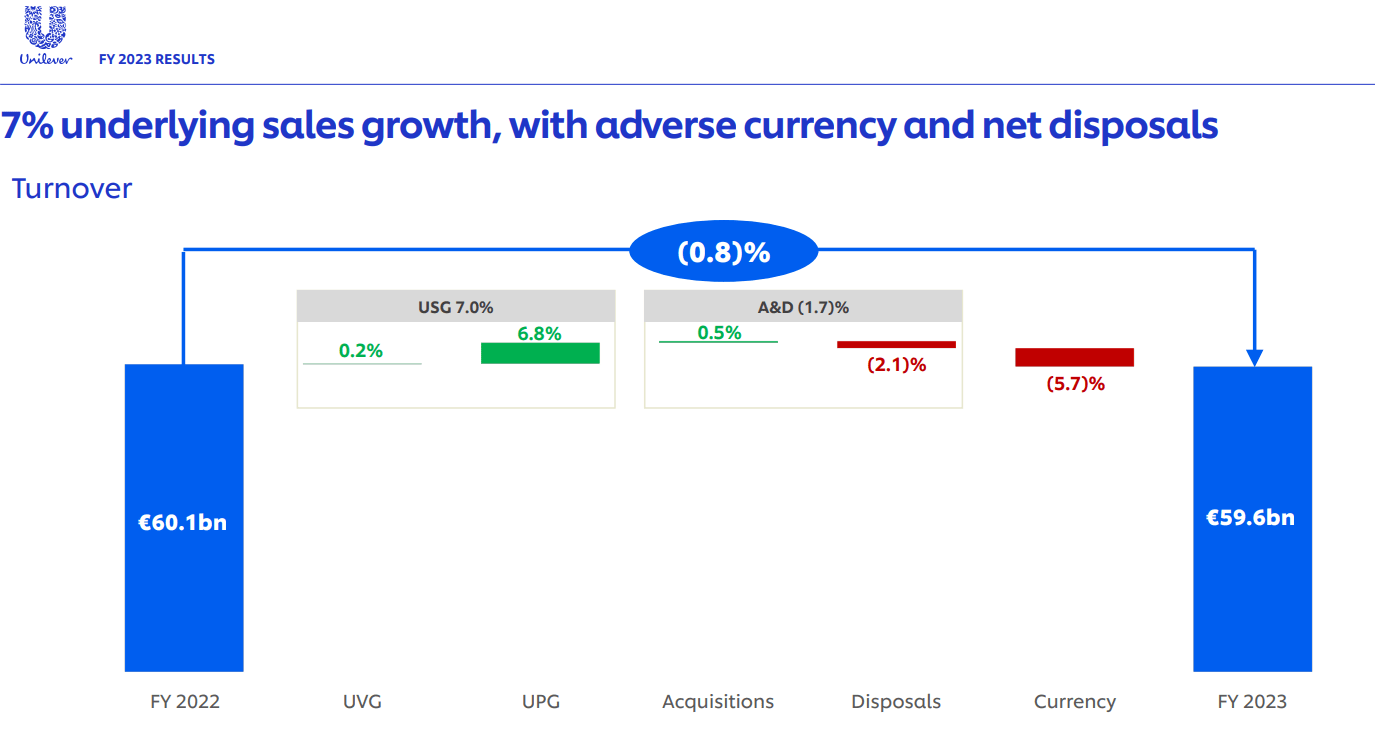

Full 12 months overview

From a turnaround perspective the FY 2023 numbers have been respectable. Income was down 0.8% from €60.1 billion to €59.6 billion which was primarily as a consequence of vital unfavourable forex influence (5.7%).

Pricing is clearly trending downwards due to easing inflation, whereas quantity is slowly trending upwards.

In FY 2023, the corporate had an underlying gross sales development of seven% which was primarily pushed by larger costs (6.8%) and a bit extra quantity (0.2%). UL’s 30 energy manufacturers have carried out comparatively higher with an 8.6% underlying gross sales development and 1.6% development in quantity.

UL gross sales (This autumn and Full Yr 2023 Outcomes)

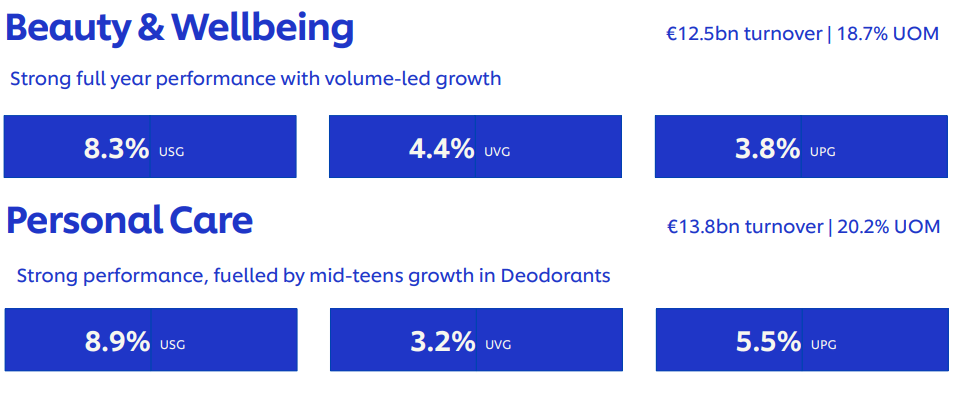

What I actually like in regards to the numbers is the underlying quantity development in Magnificence & Effectively-being (4.4%) and Private care (3.2%).

UL greatest performing segments (This autumn and Full Yr 2023 Outcomes)

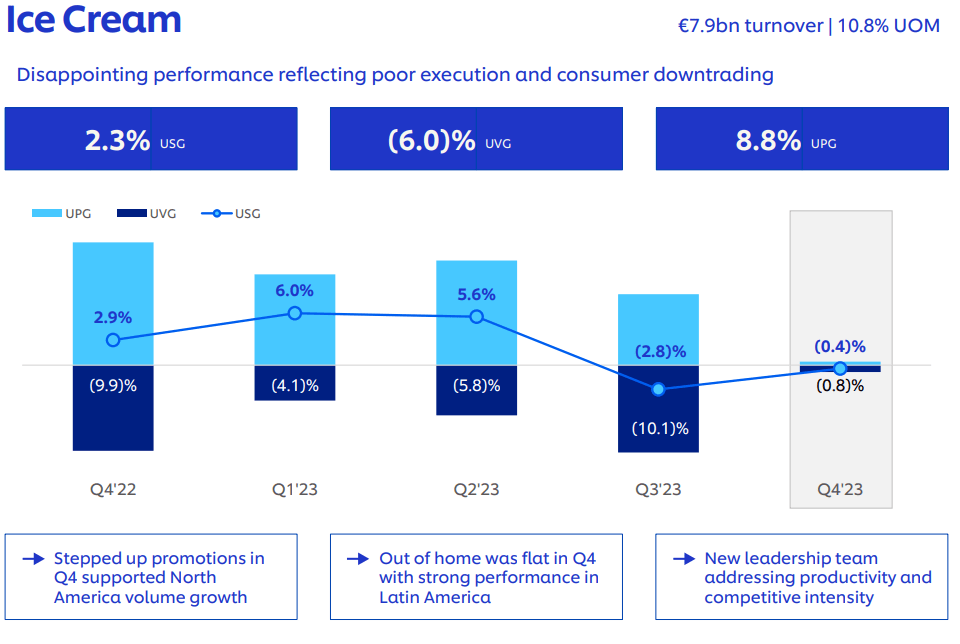

One of many least performing segments is diet, as a consequence of larger enter prices and shrinking volumes (-2.2%). The ice cream section can be performing badly.

UL ice cream efficiency (This autumn and Full Yr 2023 Outcomes)

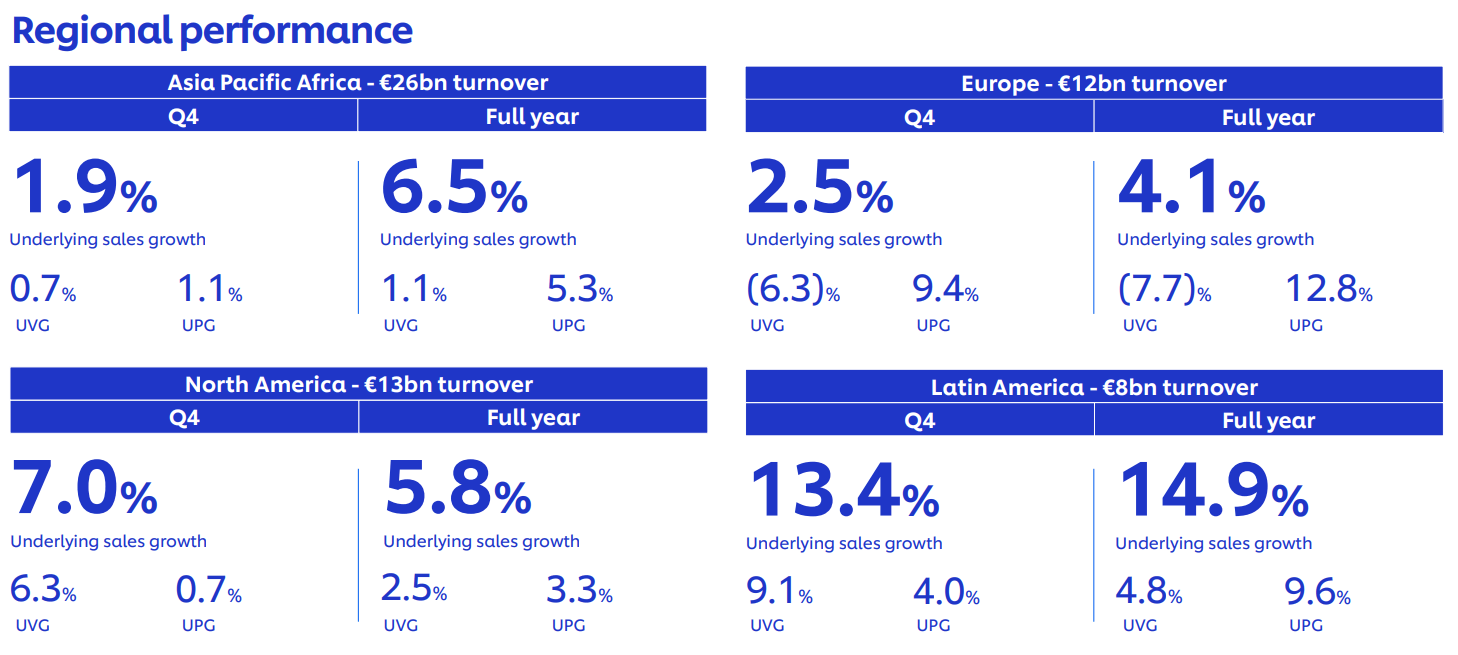

Taking a look at regional efficiency, UL did a wonderful job in Latin America with 14.9% in gross sales development and 4.8% quantity development. Regardless of the financial circumstances in Asia they managed to realize underlying gross sales development of 6.5% with a bit quantity development of 1.1% as nicely. Euro was actually underperforming when it comes to gross sales development and a -7.7% in quantity.

UL regional efficiency (This autumn and Full Yr 2023 Outcomes)

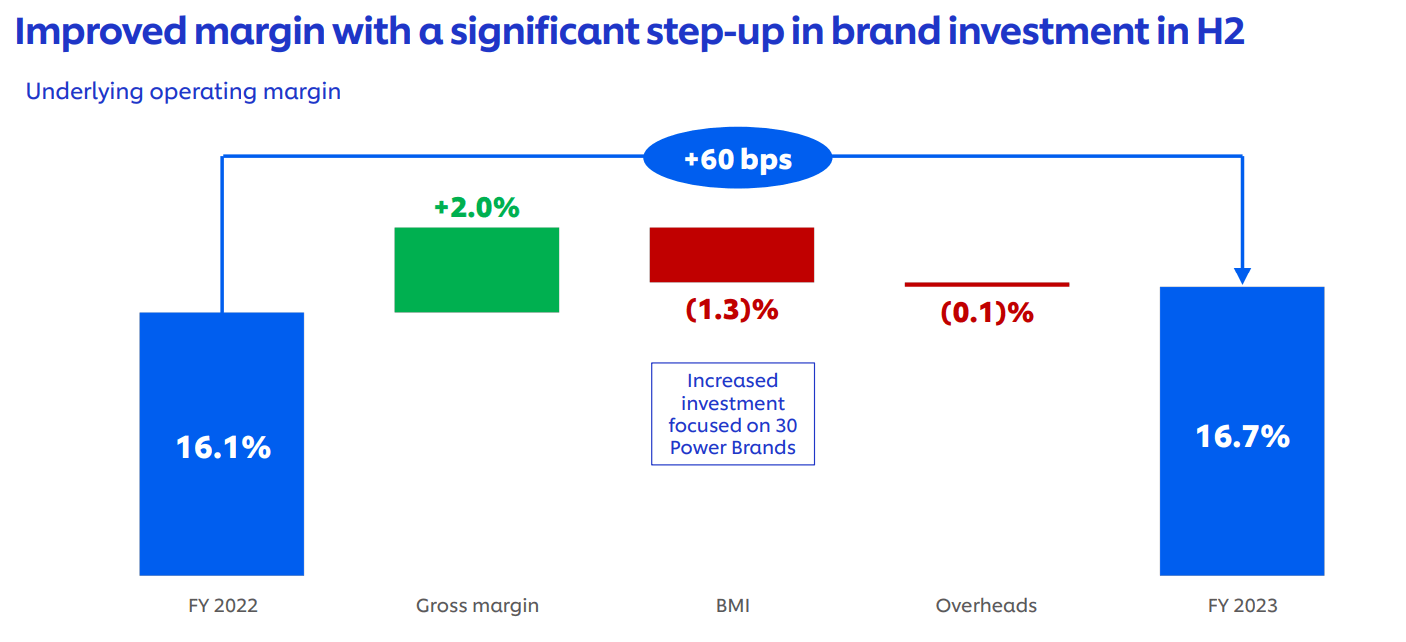

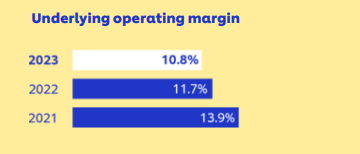

When it comes to profitability issues are enhancing for UL. What is sweet to see is that the underlying working margin is growing once more (0.6%). Gross margin was up nearly 2%, however it has been partly offset by elevated funding into their energy manufacturers.

UL margins (This autumn and Full Yr 2023 Outcomes)

In FY 2023 the FCF was lots larger in comparison with earlier 12 months €7.1 billion vs €5.2 billion. The FCF of FY 2023 was together with €400 million linked to tax refund in India.

All in all I’m pleased in regards to the numbers. Margins are barely recovering and UL is performing fairly nicely within the private care and wonder & wellbeing section, which I consider will likely be their important focus within the years to come back.

For FY 2024, UL is anticipating 3-5% of underlying gross sales development. The corporate can be anticipating the next contribution to quantity development in comparison with FY 2023 and an enchancment in working margin for the complete 12 months.

In relation to capital returns UL stays dedicated to an “attractive and sustainable” dividend. In different phrases, no rising dividend. Along with the dividend there will likely be a €1.5 billion share buyback program in 2024.

The strengths of Unilever

Wanting on the final 5 years, I can totally think about that traders are sad with UL’s efficiency. Particularly if we evaluate the corporate to its friends there are some severe gaps to shut and the “new management” goes to strive that. Investing isn’t about wanting again on the previous, it’s about on the lookout for future prospects. For my part there are nonetheless a good quantity of alternatives the place UL can profit from.

UL remains to be a terrific enterprise however wasn’t managed optimally to create significant shareholder worth. The corporate nonetheless has a formidable portfolio of high-quality manufacturers. There are over 3.4 billion people everywhere in the world which can be utilizing merchandise of UL each day. We, as a household, are utilizing a number of UL merchandise ourselves each day.

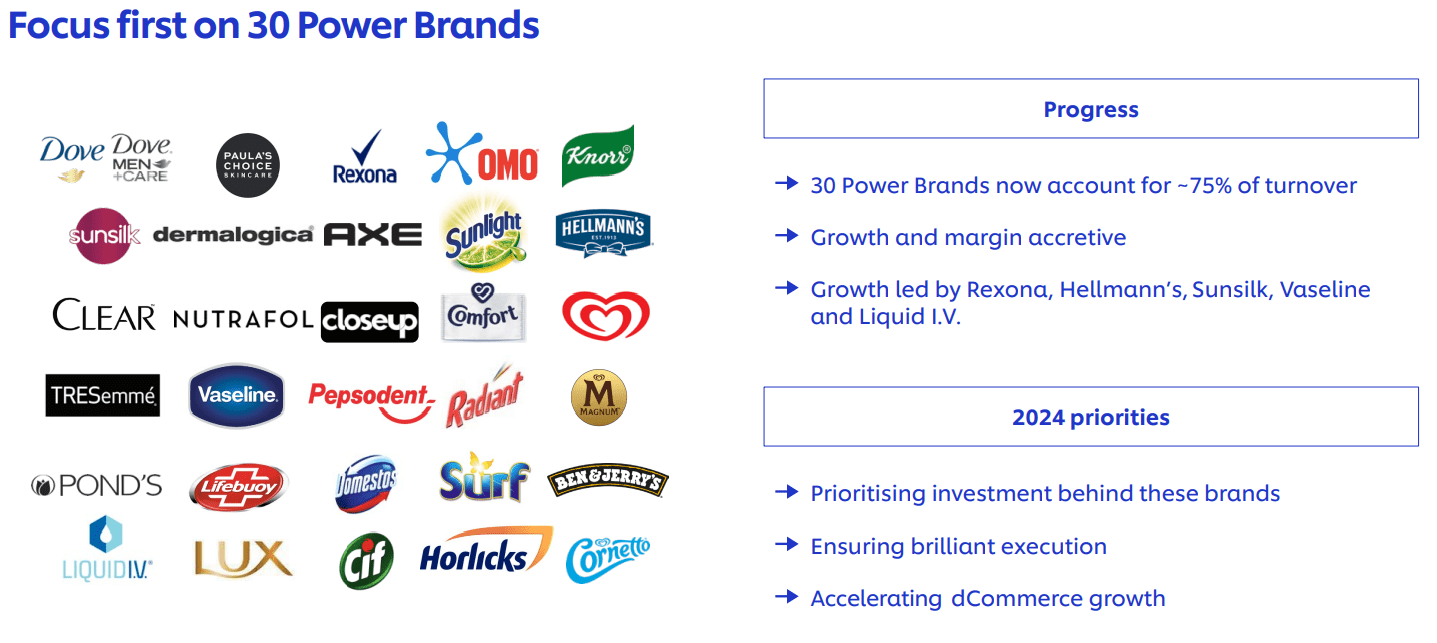

Particularly their energy model portfolio is spectacular. These manufacturers account for 75% of whole income and have been accounting for 90% of whole development.

UL energy manufacturers (This autumn and Full Yr 2023 Outcomes)

UL has additionally dominant presence in rising markets, equivalent to Latin America, Asia, and Africa. Primarily based on their 2023 annual report, 58% of whole income already comes from rising markets and there are definitely alternatives right here to realize additional development.

The corporate is shifting extra in direction of probably the most worthwhile manufacturers/ enterprise segments and needs growing publicity within the “premium segment.” That is additionally a part of their Development Motion Plan, which is initiated by administration.

Administration actions

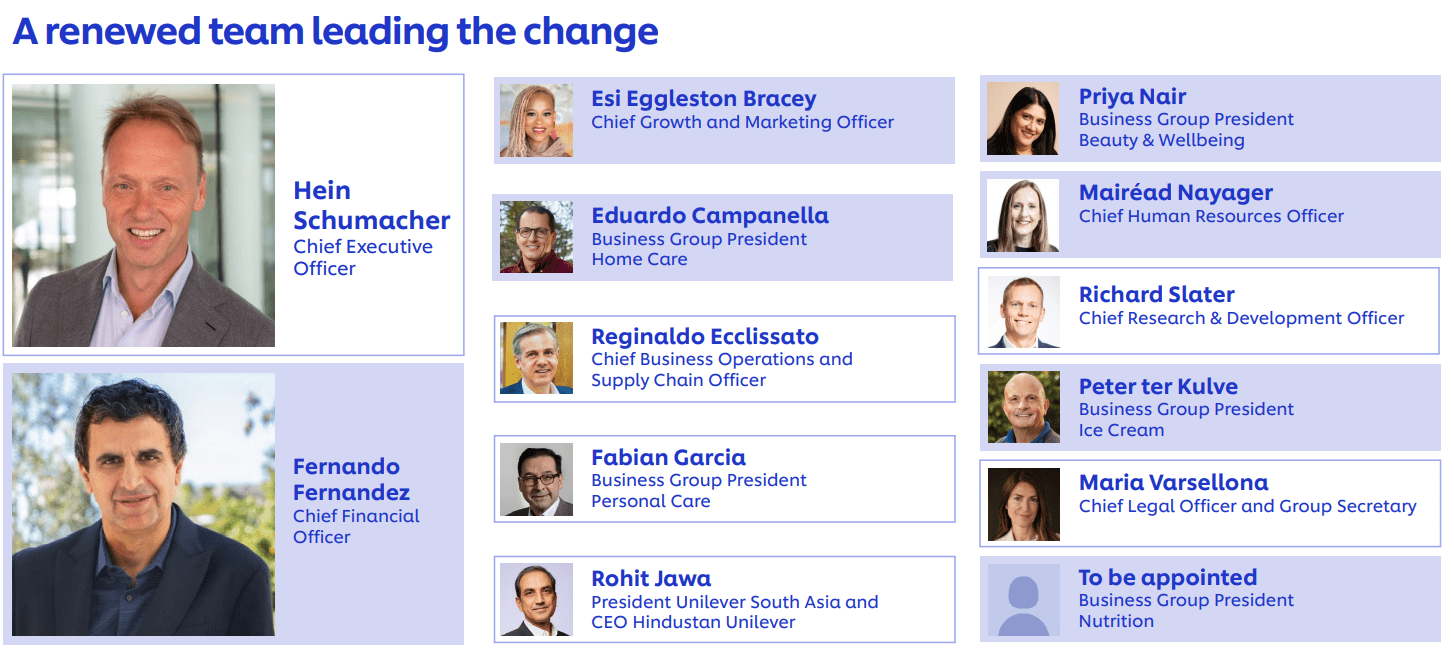

Since Hein Schumacher has joined UL, many positions in administration have modified. Personally, I actually didn’t just like the administration type of the previous CEO Alan Jope and I used to be pleased that issues have been altering. Nevertheless, it have to be famous that the general public in new positions have already labored for UL.

Adjustments in administration (This autumn and Full Yr 2023 Outcomes)

The Development Motion Plan ought to result in quicker development, larger productiveness, and a much less complicated enterprise. In the intervening time UL is unquestionably taking actions to make the enterprise imply and lean. On the 19th of March the corporate has introduced its plans to spin off its ice cream division. There is no such thing as a readability but in regards to the course of, however from this news item evidently UL is speaking with varied banks about attainable non-public fairness curiosity.

From an funding perspective, I like this resolution. As a result of ice lotions have been extra of a standalone section in comparison with their others. The ice cream section additionally lagged far behind on the subject of working margins.

Margins ice cream section (annual report 2023)

Particularly, if we evaluate this to non-public care (20.2%) and wonder & wellbeing (18.7%) in FY 2023, it is a lot much less worthwhile.

UL can be going to launch a productiveness programme. That is what the corporate itself says about it:

Constructing on the early momentum of GAP now we have recognized extra efficiencies that may now be accelerated. Along with the portfolio adjustments, Unilever intends to launch a complete productiveness programme, driving focus and quicker development by means of a leaner and extra accountable organisation, enabled by funding in expertise.

Based on firm estimates, this programme ought to result in €800 million in value financial savings over the subsequent three years. This could greater than offset estimated operational dis-synergies from the separation of the ice cream enterprise section. The funding in expertise remains to be a bit obscure for me, however it appears clear to me that roughly 7500 office-related jobs will likely be lower. The optimistic factor about that is seemingly that it provides Unilever extra flexibility to put money into development.

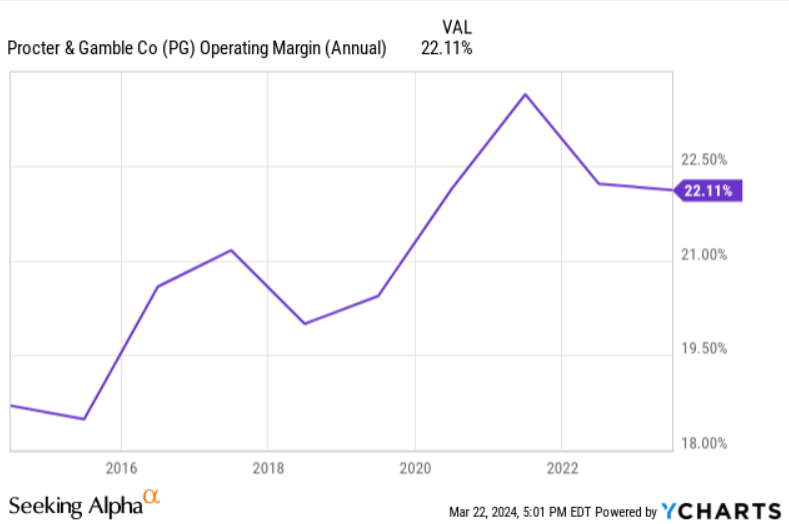

I wouldn’t be shocked if this motion is totally supported by Nelson Pelz, as a result of comparable actions occurred after he joined the board of PG in 2017.

Margin enchancment PG (YCharts)

So, if issues are going to be the identical for UL, we are able to anticipate some additional portfolio streamlining and price slicing sooner or later to extend margins.

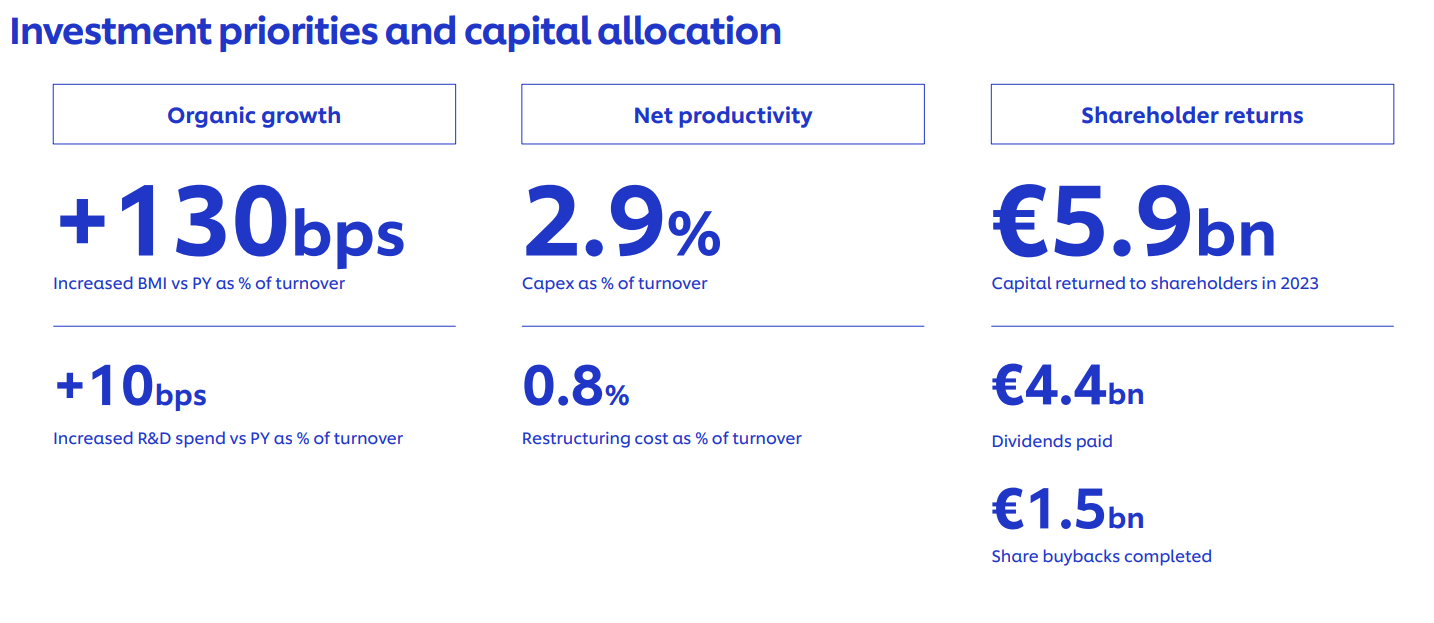

Capital allocation

The expansion motion plan additionally has influence on the capital allocation technique of the enterprise.

Capital allocation priorities (This autumn and Full Yr 2023 Outcomes)

Since development is their precedence, UL goes to take a position extra in model & advertising and marketing and R&D. They’ll give attention to their energy manufacturers, which I feel is a smart factor to do.

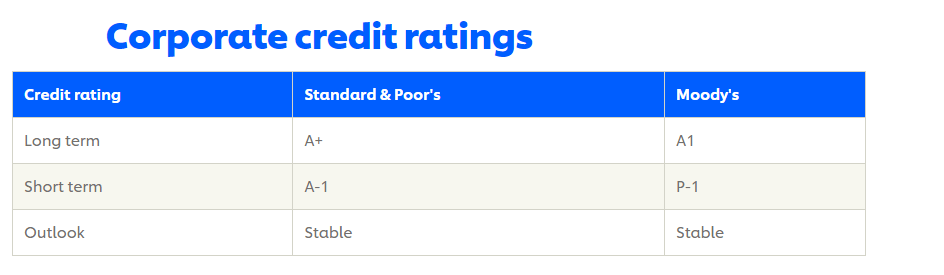

In relation to their stability sheet, UL is making an attempt to keep up their internet debt/EBITDA radio round 2x, so this will likely be in step with their present debt profile of two.1x. That is high quality for my part and UL has additionally a wonderful credit standing.

UL credit score scores (UL investor relations)

As acknowledged of their FY 2024 outlook, a share buyback program of €1.5 billion has been introduced. With a market cap of round €122 billion this will likely be 1.2% of whole share rely. Add this to a dividend of three.7% and have been speaking a few whole shareholder yield of virtually 5%.

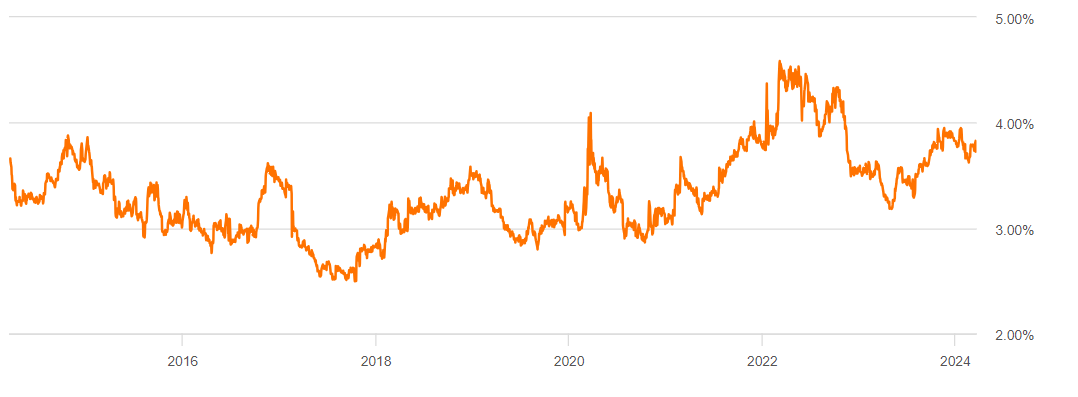

UL is a really constant dividend payer. The corporate has began paying a dividend in 1929 and from that second in time, they continued to take action. Solely throughout the second world warfare UL wasn’t been capable of pay a dividend.

In the intervening time the corporate has a dividend yield of three.7%, which is lots larger in comparison with its sector median of two.69%. Wanting on the firm’s personal historical past it’s on the excessive facet as nicely.

dividend yield improvement (Looking for Alpha)

Sadly, the dividend isn’t rising anymore. Over the past years the dividend per share went nowhere and it seems to be like that is going to be the case for the subsequent years as nicely. My first article about UL was all in regards to the firm as a dividend turnaround play, however I feel that Unilever’s focus is definitely not on the dividend in the mean time.

Within the FY 2023 outcomes they discuss a horny and sustainable dividend. In different phrases, I don’t assume UL will develop its dividend within the short-term. Given the development in FCF, there would definitely have been room for a dividend improve. Personally, I don’t care as a lot, as a result of I’m not a dividend development purist, and if administration has higher alternate options to allocate capital I can perceive this resolution. If UL is getting extra worthwhile sooner or later and their development motion plan is gaining momentum, I anticipate the dividend to develop once more.

Valuation

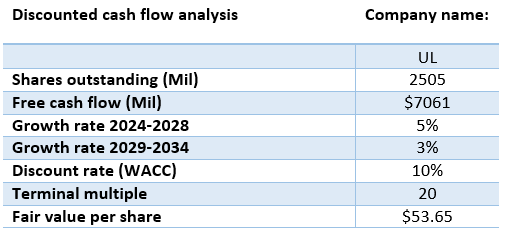

I used discounted money circulation evaluation to calculate a good worth for UL. In FY 2023 the FCF of UL was nearly €7.1 billion. For my calculations, I subtract the €400 million tax refund from India. The corporate can be going to extend its CapEx. Primarily based on their This autumn earnings name transcript they will improve CapEx from 2.9% of income to round 3% or a bit larger. This might additionally influence free money circulation for a couple of hundred million so I’ve adjusted my used FCF for this. Primarily based on these assumptions, I used an adjusted FCF of €6.5 billion ($7.061 billion).

I feel a 5Y FCF development of 5% is affordable. UL itself is aiming for a multi-year underlying gross sales development of 3-5%. If the corporate manages to realize this and their margins are additionally enhancing, 5% FCF development is for my part achievable. and I used a 3% development for the 5 years thereafter, as a result of it’s harder to make correct assumptions over longer intervals of time.

In the intervening time UL has a PE of 17. I used a PE of 20 as a terminal a number of, as a result of that is in step with UL’s historic common and I feel this a number of will be justified.

Lastly, I used a reduction fee of 10%. That is my private hurdle fee and the minimal annual return I demand from my funding in UL.

DCF evaluation (Google spreadsheets)

If we do the mathematics this comes all the way down to a good worth of $53.65 per share. In comparison with the present share value of $49.99 it seems to be 7.3% undervalued proper now.

Conclusion

Given the most recent enterprise outcomes and up to date actions from administration, I get a bit extra optimistic about UL. I already had a BUY score for the corporate, however given the development of the underlying fundamentals, the danger reward has develop into higher.

For the dividend development investor purists on the market, dividend aristocrat like development nonetheless appears far-off, but when the expansion motion plan bears fruit, I anticipate dividend development once more. The advance in FCF in FY 2023 does give administration room to take a position extra into additional development and it’s higher to not distribute all the pieces to the shareholder.

There are definitely funding dangers for UL. The corporate has typically made plans to present their enterprise a optimistic twist however has additionally failed a number of occasions. The primary actions of the brand new administration are for my part smart, however it’s only the start and a number of work must be executed. Even supposing there seems to be an upward pattern in quantity development, it’s nonetheless too variable to talk of a structural enchancment. It’ll in all probability take years for the plans to take full impact. Schumacher indicated within the final earnings name that he expects an preliminary influence within the second half of 2024.

I additionally assume that with the present valuation issues do not should be good. I anticipate UL to be a very good addition to a diversified dividend portfolio, with a pleasant beginning yield of three.7%, mixed with share buybacks and attainable share value appreciation.

Since it’s a turnaround play, I’ll present an replace after the longer term half-year numbers.

Joyful investing everybody.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.