vm

Introduction

It is time to speak about an organization I’ve adopted for a few years. An organization that, albeit with vital volatility, has become one of many greatest wealth turbines in the marketplace.

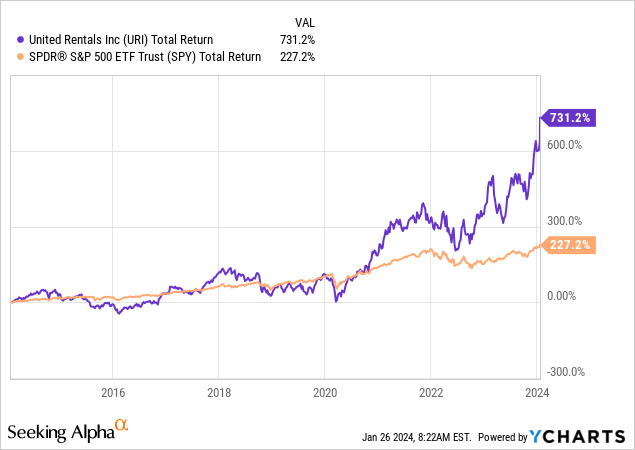

That firm is United Leases (NYSE:URI), which has returned greater than 730% over the previous ten years, which is greater than 500 factors larger than the already spectacular 227% return of the S&P 500.

On November 28, I wrote my most up-to-date article on the corporate, titled “What Makes United Rentals One Of The World’s Best Companies.”

This is part of my takeaway again then:

United Leases stands out as a prime performer, incomes a spot on TIME’s World’s Greatest Corporations 2023 checklist.

Regardless of financial challenges, URI’s strategic give attention to expertise and distinctive buyer calls for has fueled its development.

The corporate’s latest robust Q3 outcomes, constructive indicators for 2024, and strong monetary place underscore its resilience.

Since then, URI shares have risen by 41%.

Let me say that once more. Because the finish of November, roughly two months in the past, United Leases has added greater than 40% to its market cap.

On this article, we’ll re-assess the danger/reward utilizing the corporate’s just-released earnings, which not solely inform us so much concerning the firm but additionally concerning the market/financial surroundings.

So, as we now have so much to debate, let’s get proper to it!

United Leases Is Firing On All Cylinders

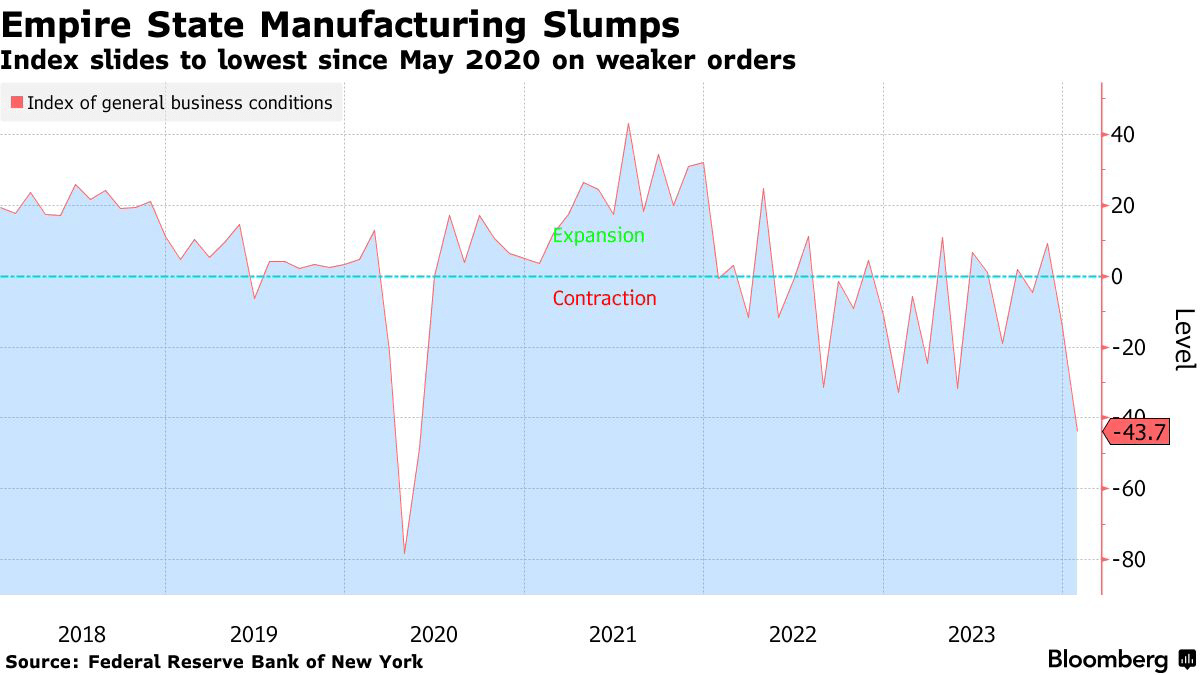

Though we’re seeing some financial weak spot in manufacturing – certainly one of them being the New York (Empire State) Fed Manufacturing Index – building is doing simply wonderful.

Bloomberg

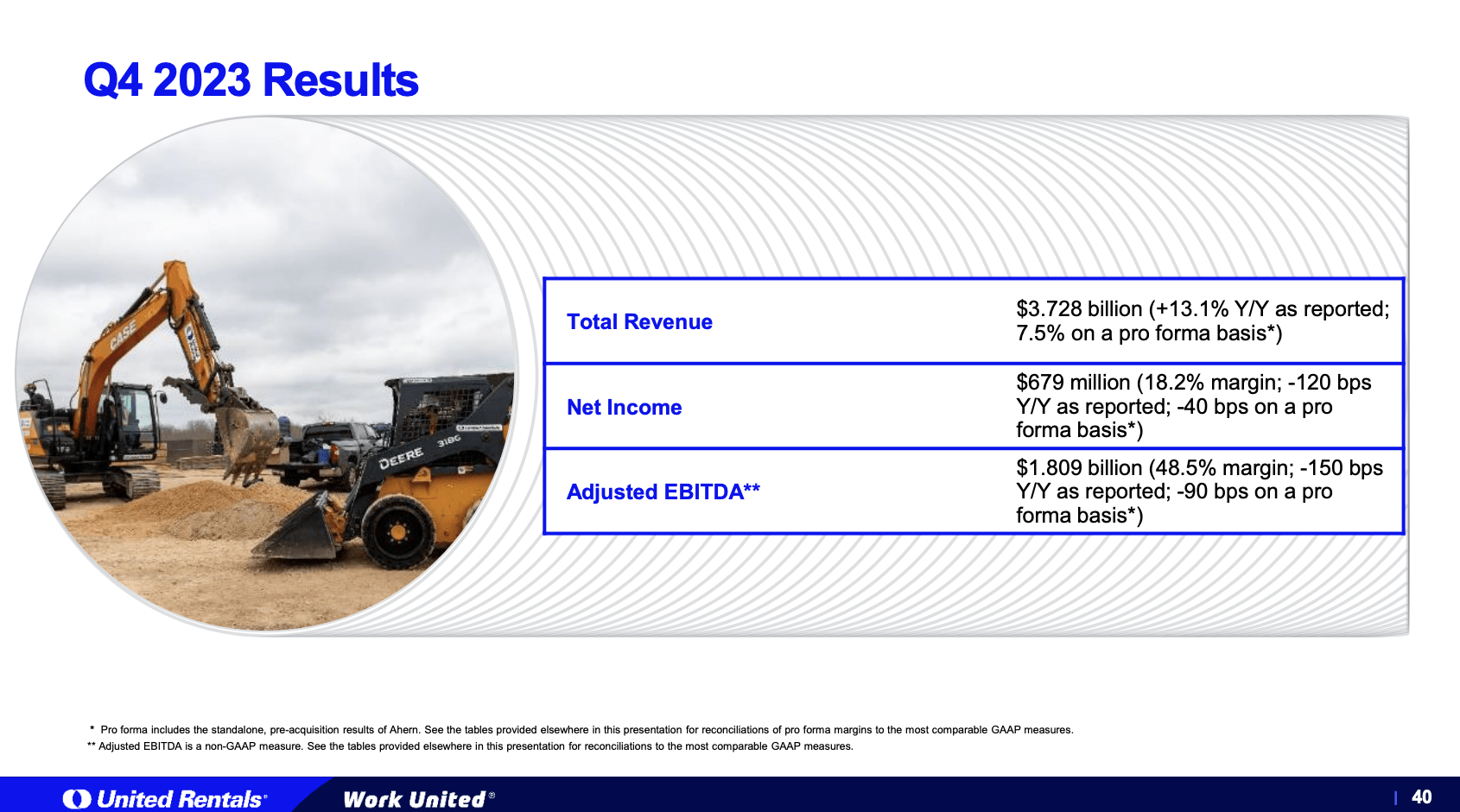

Rental income for the fourth quarter reached a record $3.12 billion, marking a considerable year-over-year improve of $372 million or 13.5%.

This spectacular development was attributed to the corporate’s stable positioning in giant initiatives and the various power noticed throughout varied finish markets.

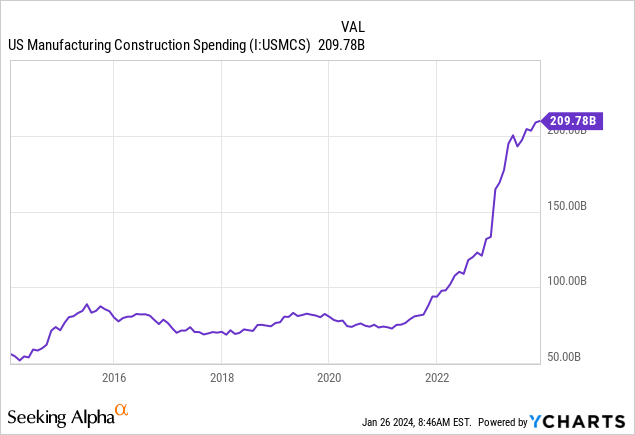

In any case, that is what manufacturing building spending within the U.S. appears to be like like:

Breaking down the rental income, Working Gear Rental noticed a big improve of $313 million or 13.9%. This development was facilitated by an enlargement within the common fleet dimension, contributing 15.1%, whereas fleet productiveness added a marginal 0.3%. Nonetheless, there was a partial offset as a consequence of assumed fleet inflation of 1.5%.

Ancillary revenues inside the rental phase additionally skilled a big rise, larger by $61 million or 14.2%.

United Leases

Moreover, the used tools phase noticed constructive outcomes, with proceeds growing by over 7% to $438 million within the fourth quarter.

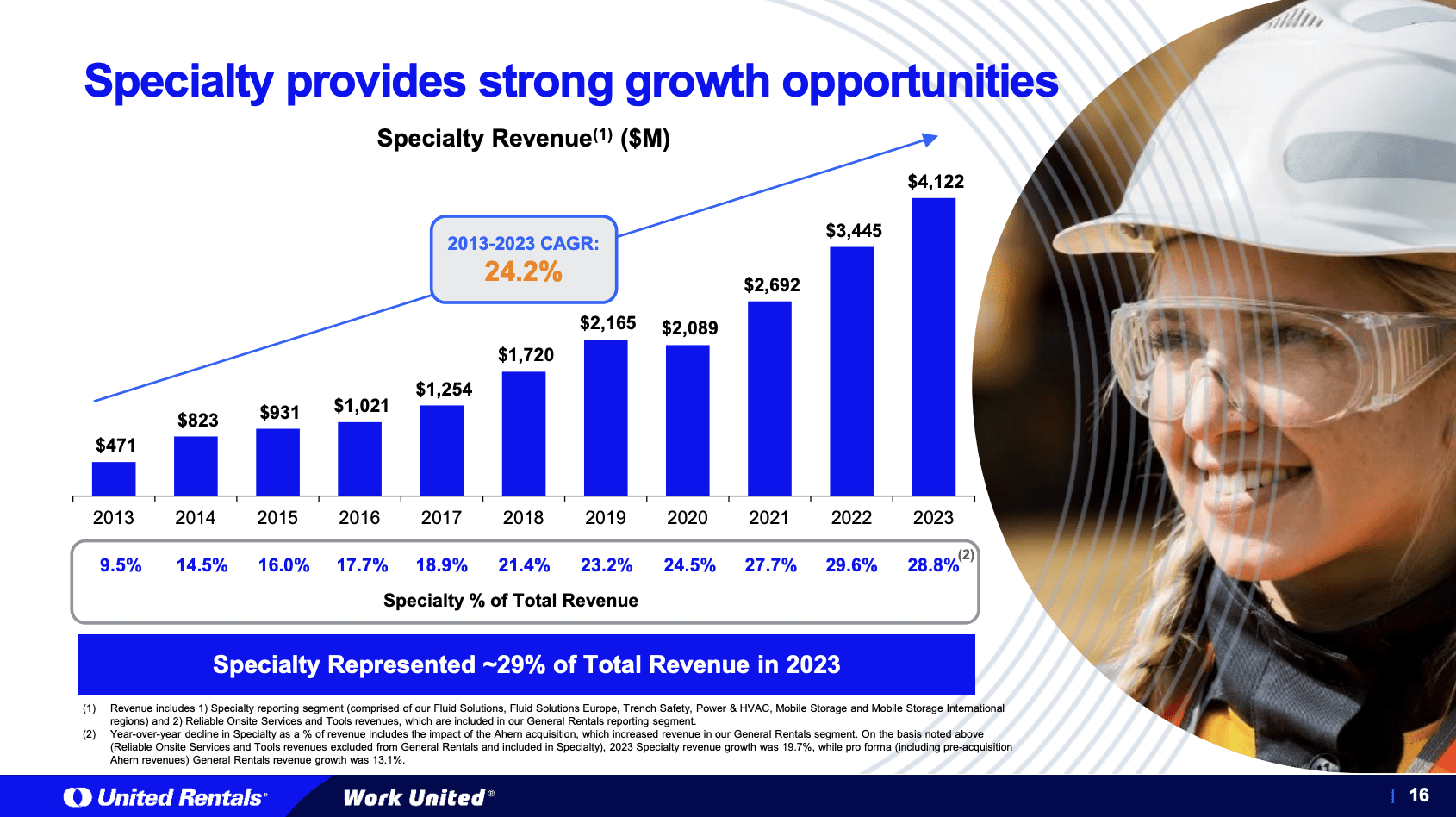

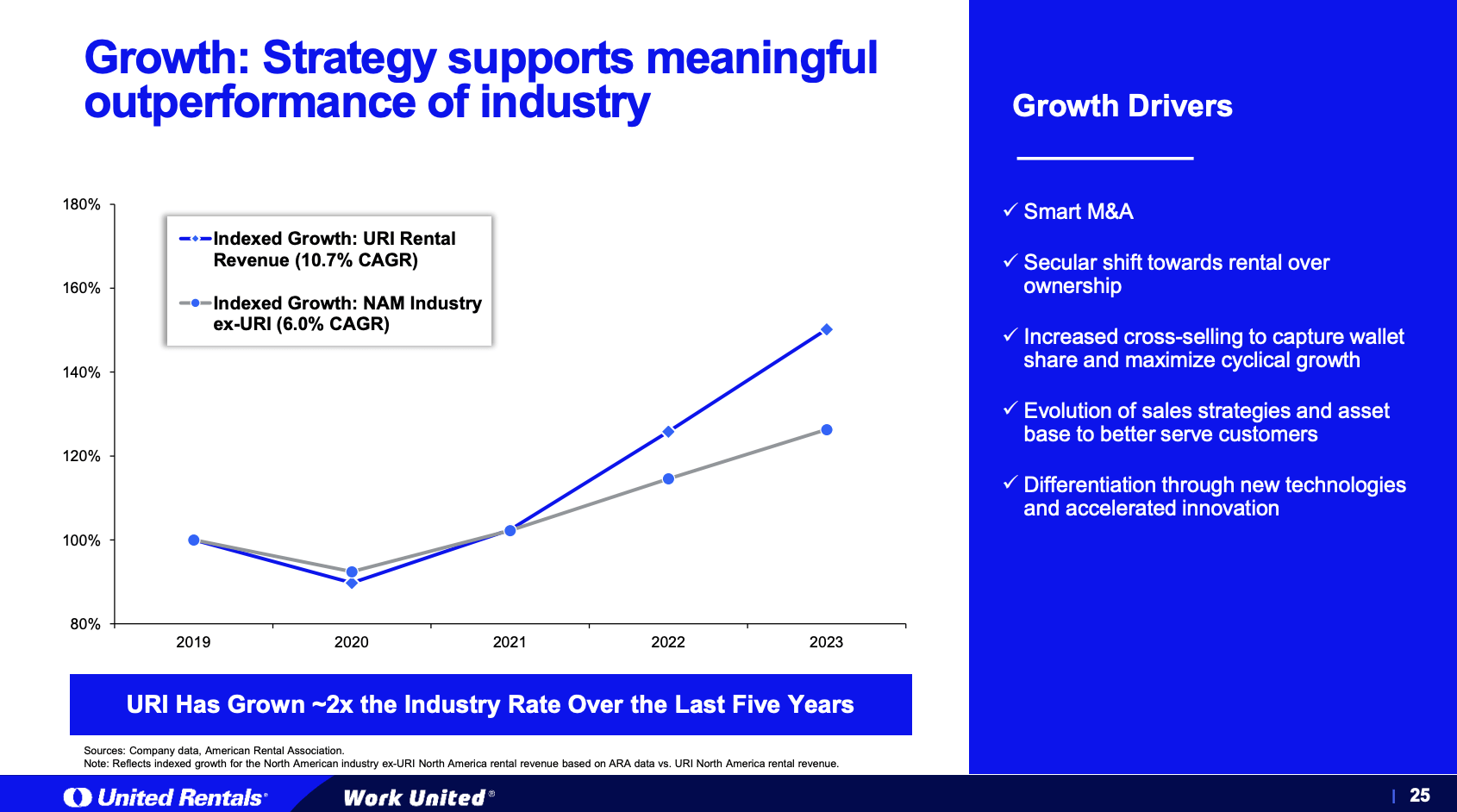

The Specialty enterprise phase delivered one other robust quarter, with rental income up 15% year-on-year. This development was unfold throughout all companies inside the Specialty phase and is an effective signal that the corporate’s investments in specialty tools are paying off.

Keep in mind that this phase has grown by 24.2% per 12 months since 2013!

United Leases

In the meantime, the adjusted use margin remained flat sequentially at 55.3%, whereas adjusted EBITDA for the quarter reached a file $1.81 billion, reflecting a big 10% year-on-year improve.

Nonetheless, regardless of these numbers, the EBITDA margin decreased to 48.5%, primarily because of the mixed influence of the Ahern acquisition and used margins.

Including to that, the return on invested capital (“ROIC”) elevated by 90 foundation factors year-on-year to 13.6%.

This quantity exceeded the weighted common price of capital by over 260 foundation factors, indicating a robust monetary efficiency.

Unsurprisingly, adjusted EPS noticed notable development, increasing by 16% to achieve $11.26.

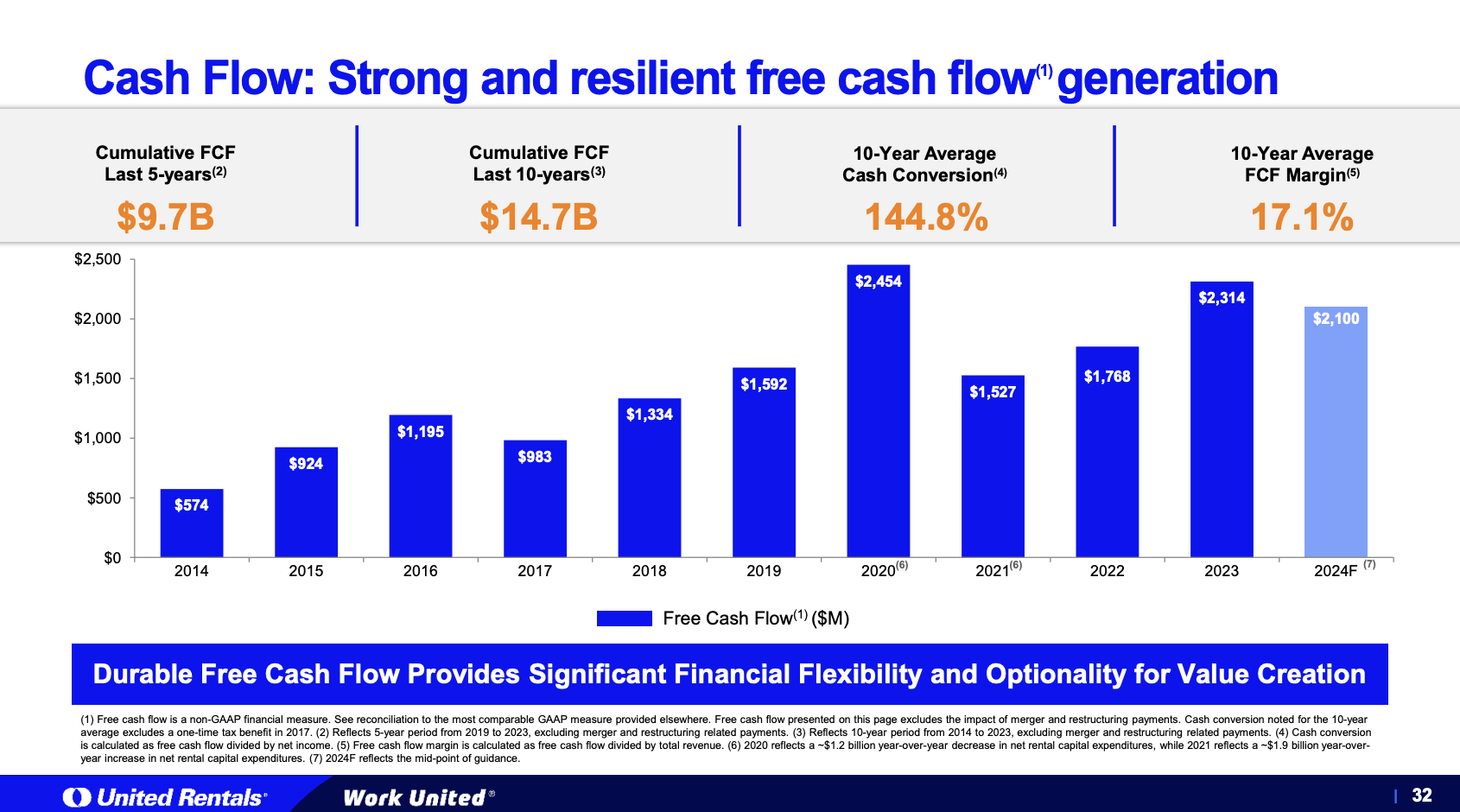

Associated to that, free money stream for the complete 12 months surpassed $2.3 billion, translating to a sturdy free money margin of 16.1%.

United Leases

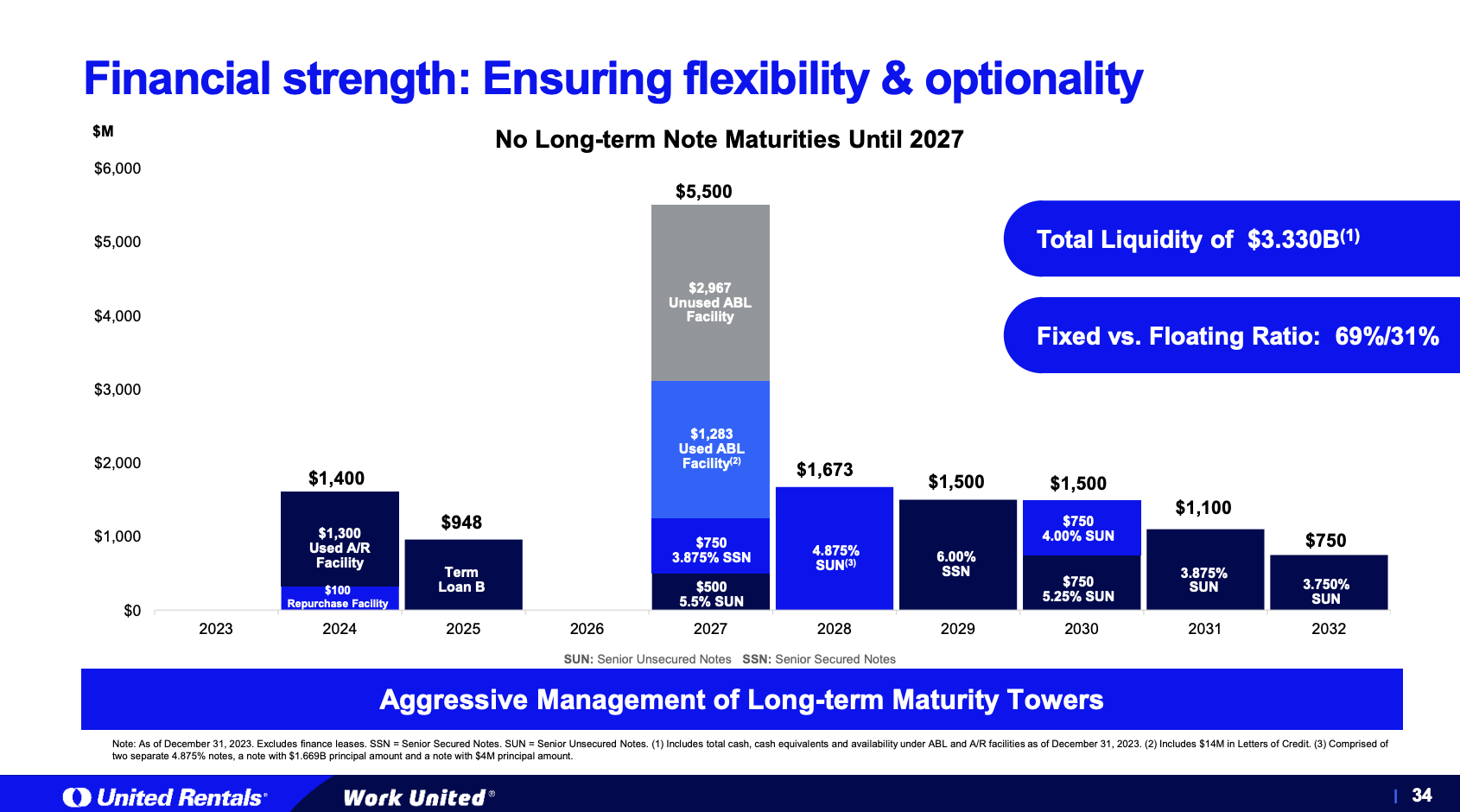

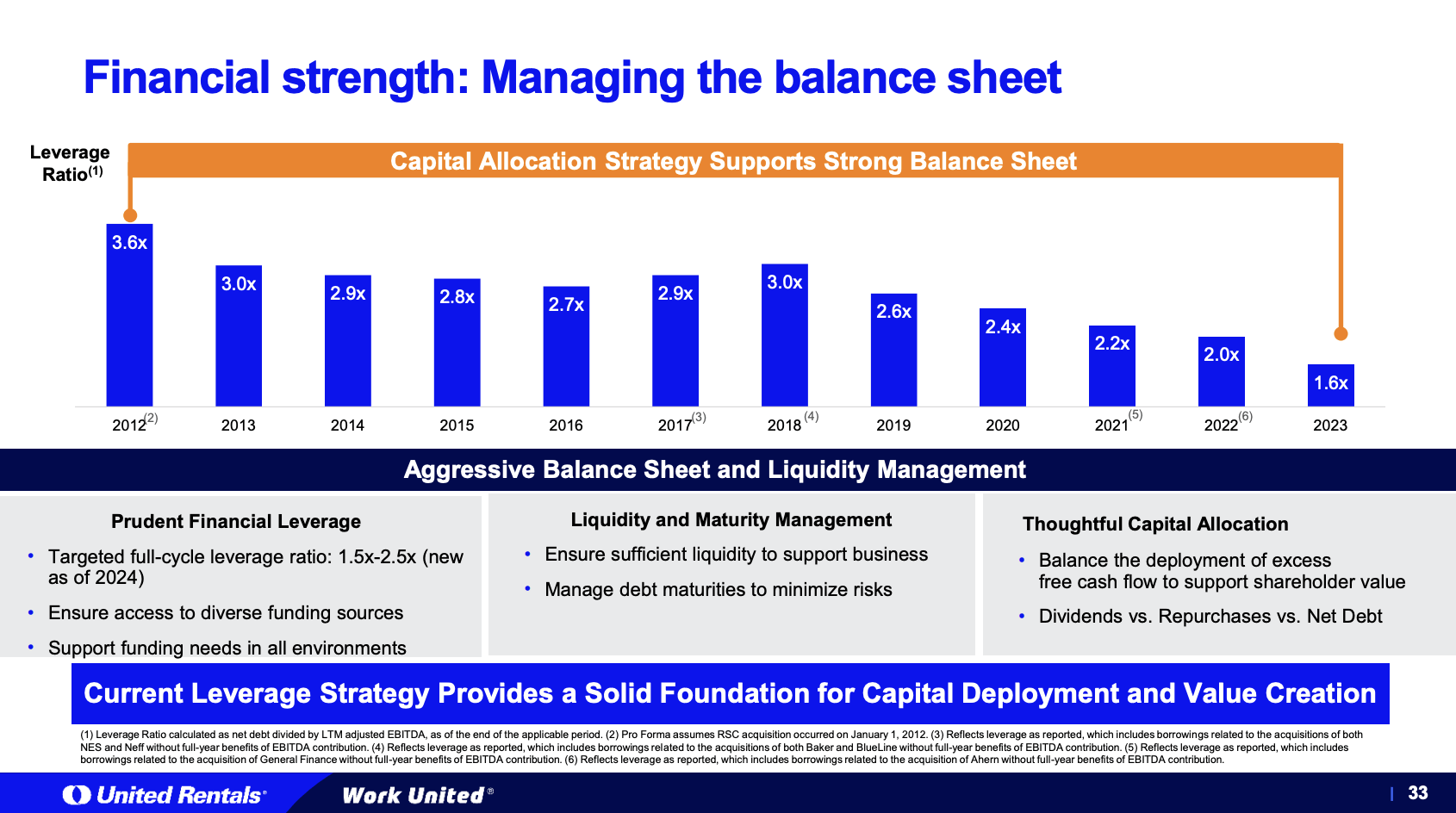

On prime of that, the corporate lowered its internet leverage ratio to 1.6x EBITDA. Whole liquidity exceeded $3.3 billion, and URI has no long-term maturities till 2027, which buys it a variety of time within the present surroundings of elevated charges.

United Leases

Going into 2024, the corporate has a internet leverage ratio near the underside of its 1.5x to 2.5x vary.

United Leases

With all of this being mentioned, let’s take a better take a look at the market surroundings and the corporate’s outlook.

What’s Subsequent?

Throughout its earnings name, the corporate famous that buyer exercise and market tendencies revealed broad-based demand throughout geographies, verticals, and buyer segments.

Industrial finish markets skilled wholesome development, with a specific emphasis on industrial manufacturing and energy sectors.

Inside building markets, each infrastructure and nonresidential demand confirmed stable development year-over-year.

Notable initiatives included these in battery crops, semiconductor-related jobs, energy, infrastructure, and knowledge facilities.

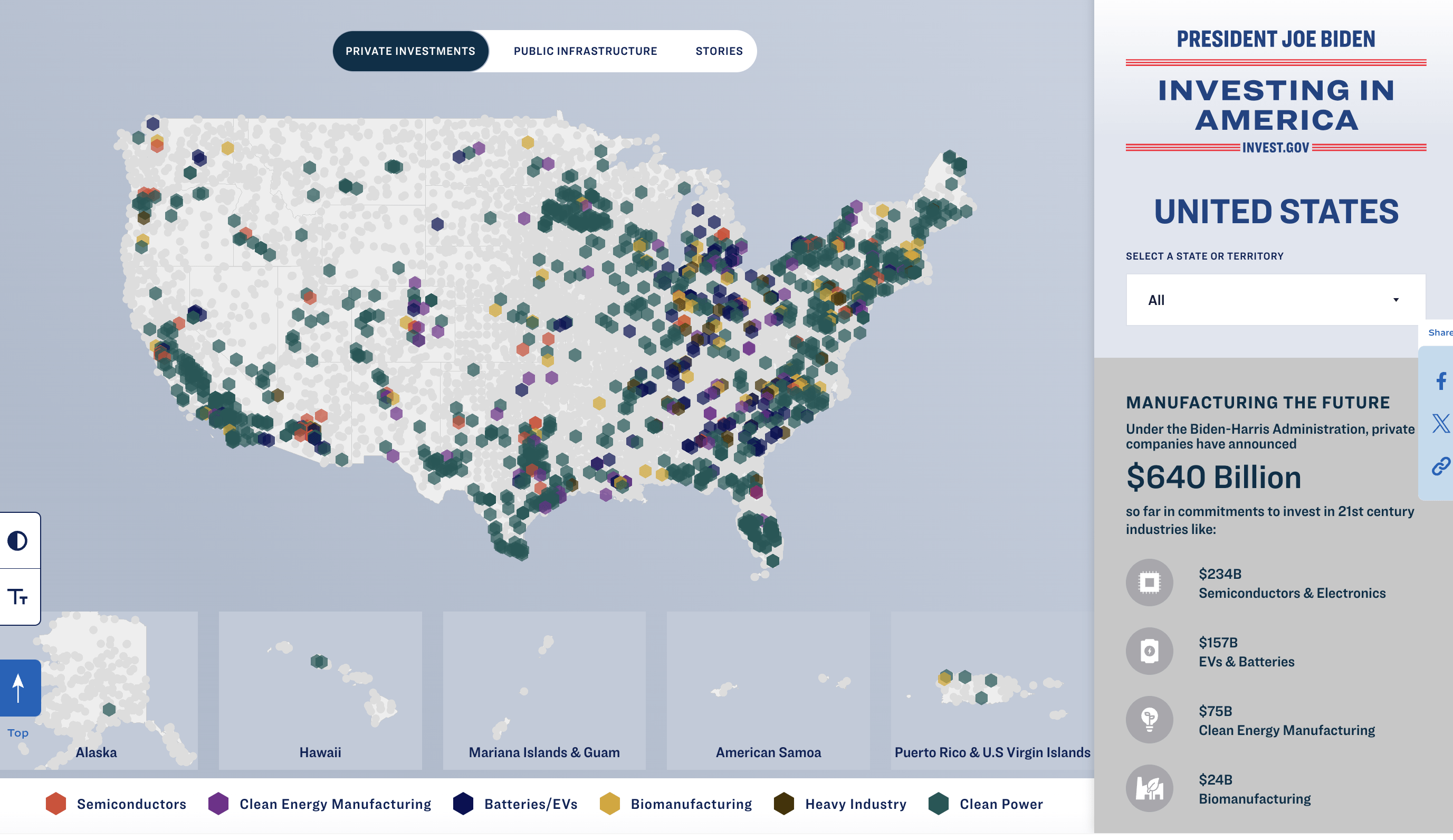

Associated to those developments and the manufacturing building spending chart I confirmed on this article, the map below reveals main personal building investments in initiatives like semiconductors, clear vitality, and others.

The White Home

With these developments in thoughts, the corporate made clear that it believes that the longer term stays shiny, with expectations of 2024 being one other 12 months of development, primarily led by giant initiatives.

This optimism is supported by constructive buyer sentiment indicators, stable backlogs, and suggestions from subject groups.

Through the earnings name, the corporate additionally expressed confidence in its capability to outperform the business, capitalize on alternatives, and obtain one other file 12 months in 2024.

United Leases

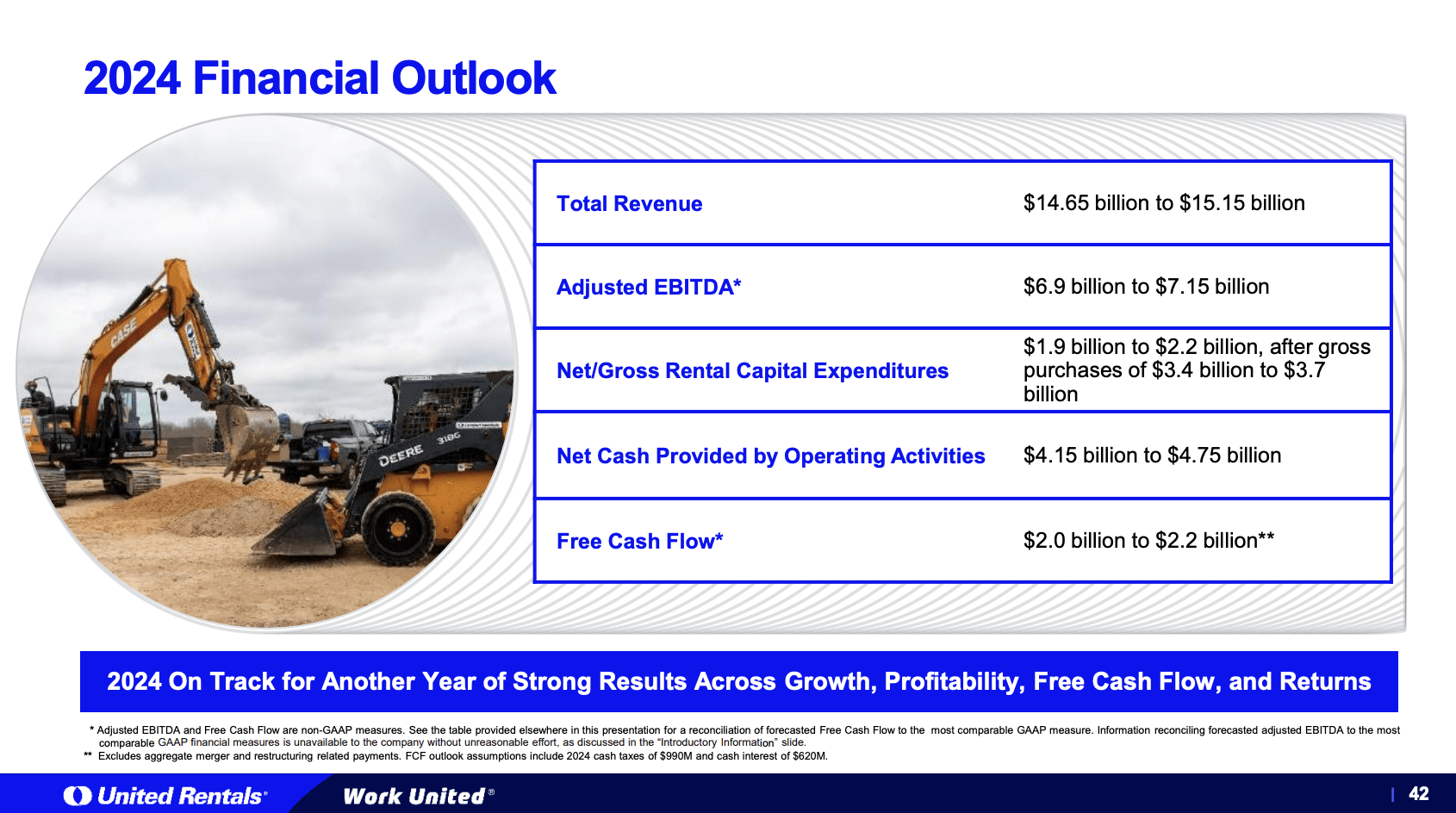

In consequence, whole income is anticipated within the vary of $14.65 to $15.15 billion, implying a full-year development of about 4% on the midpoint.

Adjusted EBITDA steerage was set at $6.90 to $7.15 billion.

United Leases

Including to that, one of many the reason why the corporate lowered its internet leverage goal vary is to pave a more healthy approach for long-term shareholder distributions and monetary well being.

When including this robust outlook, it’s no shock that administration determined to ramp up shareholder distributions.

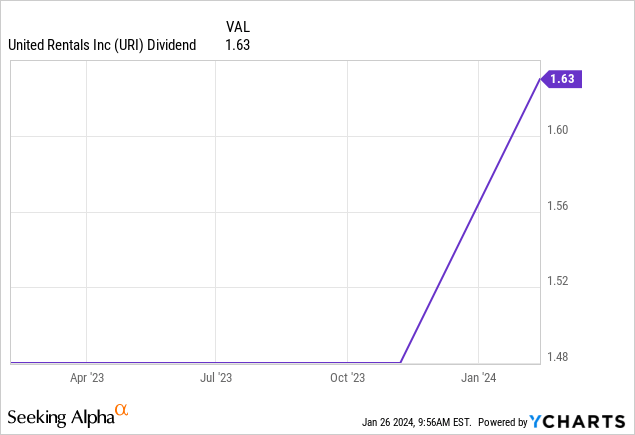

The corporate announced that the quarterly dividend could be elevated by 10.1%, which displays its dedication to constant dividend development aligned with long-term earnings.

URI at the moment pays $1.63 per share per quarter, which interprets to a yield of 1.0%.

That is the corporate’s first dividend hike because it initiated its dividend final 12 months.

Moreover, the corporate announced plans to repurchase $1.5 billion of frequent inventory in 2024, representing 3.5% of the corporate’s present $43 billion market cap.

Valuation

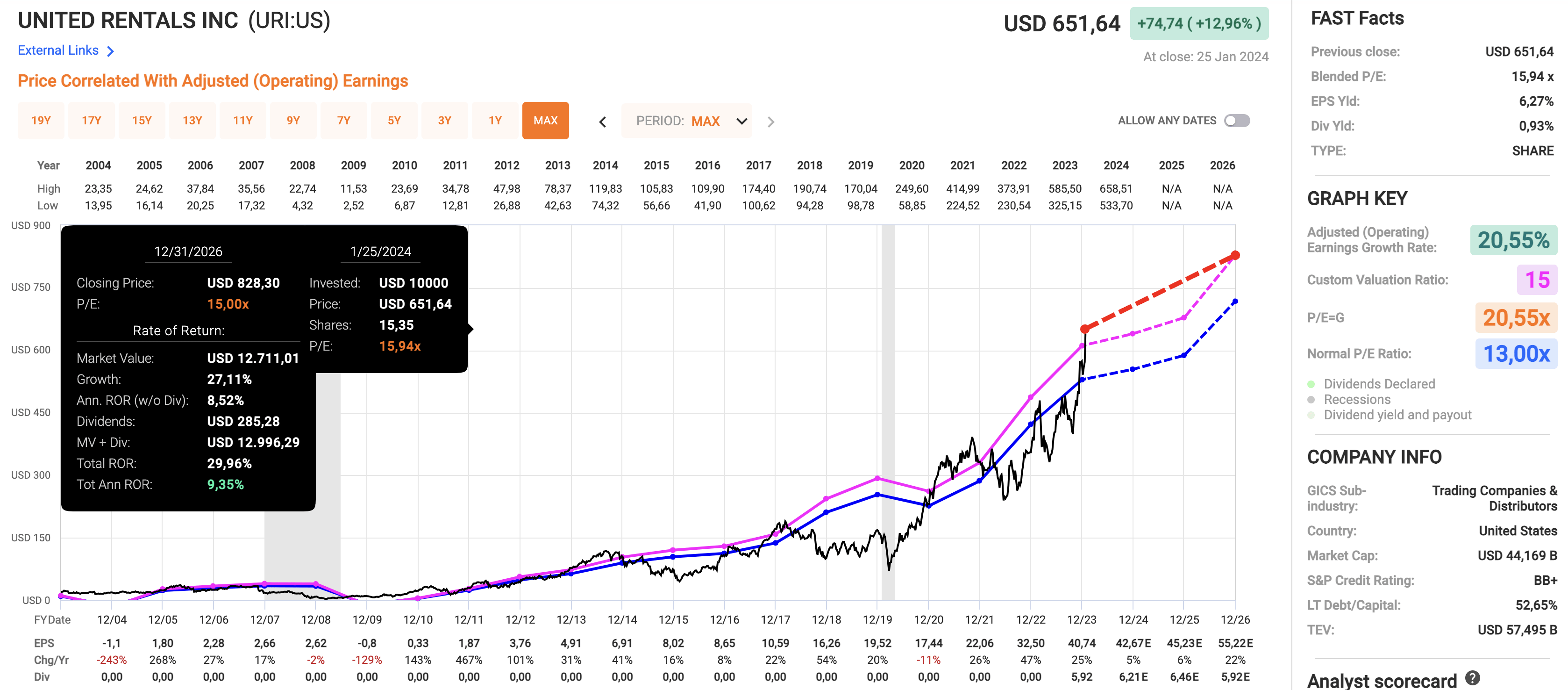

In terms of URI’s valuation, the inventory continues to take pleasure in upside potential.

Utilizing the information within the chart beneath:

- This 12 months, EPS is anticipated to develop by 5%, adopted by 6% development in 2025 and 22% development in 2026.

- At present, URI trades at a blended P/E ratio of 15.9x, which is above its long-term normalized a number of of 13.0x.

- Nonetheless, as URI has develop into extra mature and considerably improved its monetary place, I consider a 15x a number of is warranted.

FAST Graphs

Primarily based on these numbers, the corporate has the potential to return roughly 9% per 12 months by way of 2026. Since 2004, URI shares have returned 18.4% per 12 months.

Nonetheless, though I’ll stay bullish on URI, it must be mentioned that after such a rally, it could be finest to attend for a correction earlier than leaping in. Until manufacturing sentiment improves quickly, we may see some promoting strain as market contributors probably guess on a producing recession.

On a long-term foundation, I anticipate URI to shine, benefitting from secular business development, a fragmented market, rising dividends, buybacks, and a wholesome steadiness sheet.

Takeaway

United Leases continues its spectacular efficiency, demonstrating resilience within the face of financial challenges. The latest This autumn outcomes confirmed substantial development, with rental income hitting an unprecedented $3.12 billion. The corporate’s strategic give attention to expertise and numerous finish markets, particularly in giant initiatives, contributes to its success. Regardless of the EBITDA margin dip, URI’s monetary efficiency stays strong, with a big improve in adjusted EPS and free money stream.

Wanting forward, the corporate anticipates one other 12 months of development in 2024, supported by constructive buyer sentiment and stable backlogs. In the meantime, the choice to extend shareholder distributions displays confidence in URI’s future prospects, making it a compelling long-term funding – ideally on inventory value weak spot.

![The 5 Most Common Cybersecurity Mistakes [Infographic]](https://whizbuddy.com/wp-content/uploads/2024/05/bG9jYWw6Ly8vZGl2ZWltYWdlL2N5YmVyc2VjdXJpdHlfbWlzdGFrZXNfaW5mb2dyYXBoaWMyLnBuZw.webp.webp)