Peach_iStock

By Wealthy Mathieson and Christopher DiPrimio, CAIA

The post-COVID period has marked a shift from many years of stagnant financial development to a regime of reflation characterised by constructive nominal development and structurally larger inflation (and rates of interest).

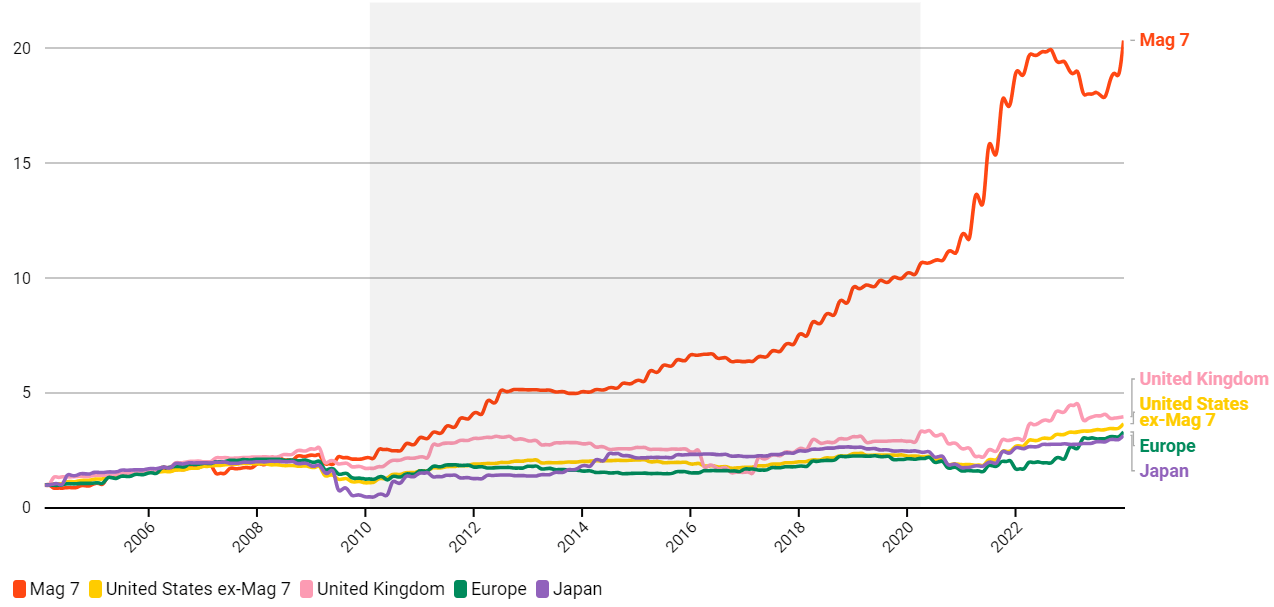

The beneath sequence of charts illustrates the affect of this shift by way of the lens of company earnings. The primary chart reveals that within the ten years following the World Monetary Disaster (GFC), previous to the pandemic, depressed ranges of nominal development meant that solely a small variety of tech firms (often called the “Magnificent 7”) had been in a position to considerably develop their earnings.

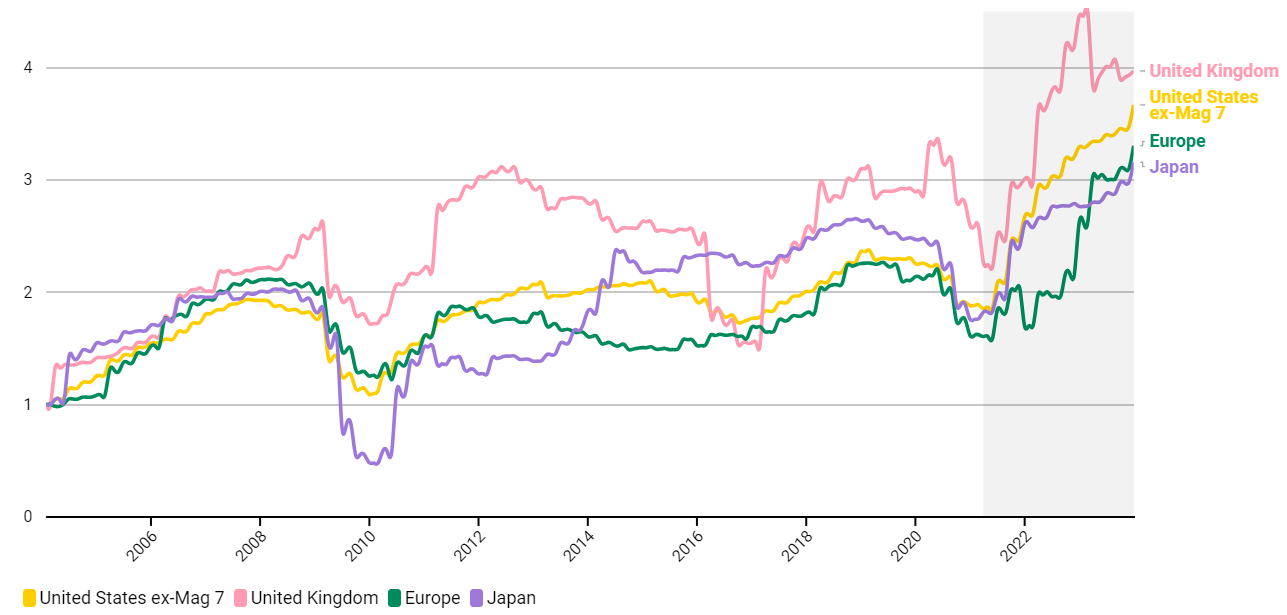

Excluding the Magnificent 7 within the second chart highlights that in that point, working earnings for US firms – together with their friends in Europe and Japan – primarily flat-lined. By the point COVID hit, earnings had been no larger than that they had been in 2007, instantly prior to the GFC. This has begun to alter as inflationary pressures have re-emerged within the post-COVID world, with common firm earnings now breaking to the upside.

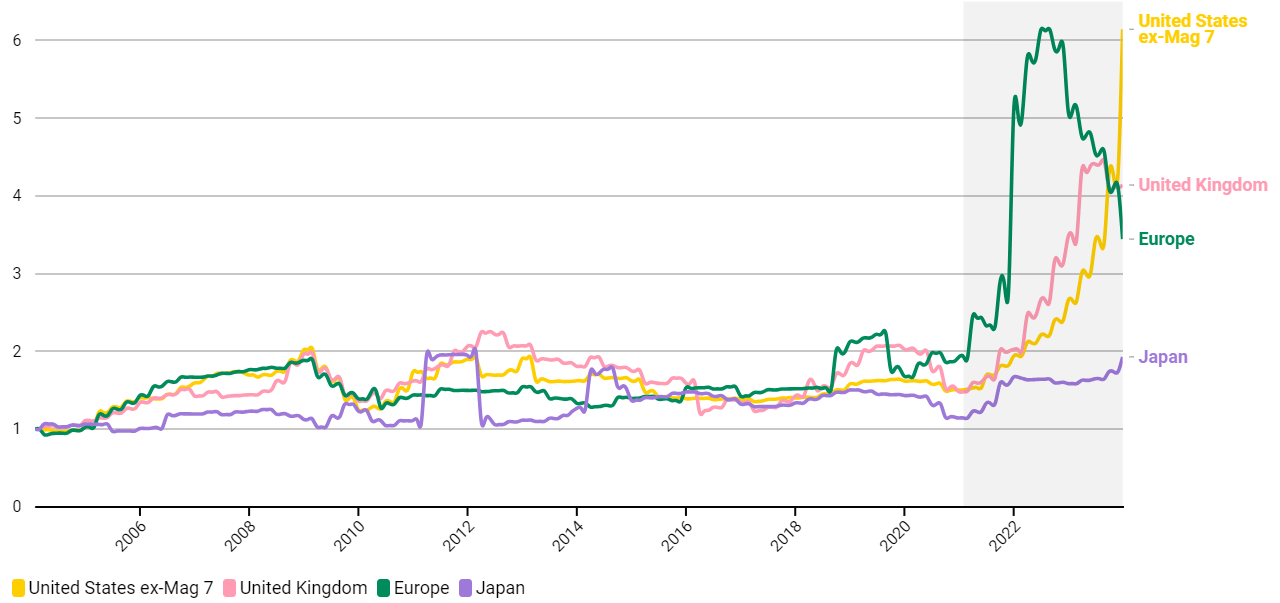

The ultimate chart within the sequence reveals {that a} additional vital nuance of the brand new regime could be noticed in notably larger cross-sectional dispersion in earnings.

Stagnant nominal development within the ten years main as much as COVID-19 stored earnings development restricted to a small group of US tech firms (Magnificent 7)

Common working earnings (rebased 1/1/2004)

Supply: BlackRock, with knowledge from Worldscope, as of February 2024. Measures of working earnings are rebased at a price of 1 (beginning 1/1/2004) for every group of firms to focus on relative variations over time from a typical place to begin.

Excluding the Magnificent 7, we discover that after years of principally muted earnings development throughout the broader cohort of firms, common earnings have elevated within the post-COVID period

Common working earnings (rebased 1/1/2004)

Supply: BlackRock, with knowledge from Worldscope, as of February 2024. Measures of working earnings are rebased at a price of 1 (beginning 1/1/2004) for every group of firms to focus on relative variations over time from a typical place to begin.

As common earnings have elevated throughout areas, so has the extent of cross-sectional dispersion in firm earnings

Customary deviation of common working earnings (rebased 1/1/2004)

Supply: BlackRock, with knowledge from Worldscope, as of February 2024. Measures of working earnings are rebased at a price of 1 (beginning 1/1/2004) for every group of firms to focus on relative variations over time from a typical place to begin.

Why would possibly this be the case? Reflation and the return of constructive nominal development can present extra runway for earnings growth in basically robust firms. The flexibility to cross on larger costs to prospects varies throughout firms. Moreover, some firms are higher than others at capturing nominal income development in backside line earnings. On the similar time, this enhanced alternative set comes with challenges like a better price of capital and muted coverage help relative to latest many years that may expose vulnerabilities in firms with basic weaknesses. The result’s a wider vary of potential outcomes, and a considerably enhanced funding alternative set relative to the one which inventory pickers confronted for a lot of the earlier cycle.

Basic dispersion interprets to return dispersion throughout shares

Within the pre-COVID interval, dynamics like zero rate of interest coverage and quantitative easing each suppressed return dispersion and lifted broad fairness market efficiency. This meant that static market index exposures and methods tilted in direction of beta generated robust absolute and risk-adjusted returns.

Now, a better charge regime units the stage for extra reasonable fairness beta efficiency and better safety dispersion as returns are extra intently tied to particular person firm traits like earnings development and profitability fairly than broadly benefitting from the earlier ‘rising tide lifts all boats’ macro atmosphere.

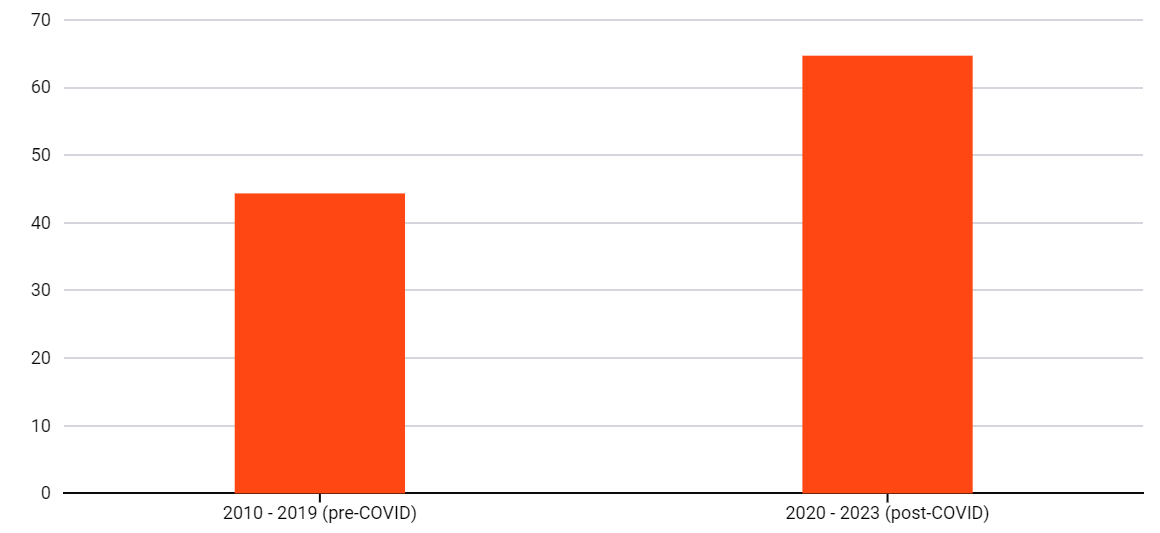

Inventory dispersion is elevated within the post-COVID period

Common annual complete return distinction between high half and backside half of MSCI ACWI Index (%)

Supply: BlackRock, with knowledge from FactSet as of 12/31/2023. Annual inventory dispersion is calculated by taking the common complete return of the highest half performers of the MSCI ACWI Index (above or equal to the median) and subtracting the common of the underside half. The inventory dispersion chart reveals the common of the annual dispersion observations throughout every interval.

Dispersion creates an expansive alternative set for lengthy/brief fairness buyers

However a more difficult backdrop for market beta doesn’t imply a scarcity of funding alternative. In a world of upper dispersion, it signifies that the chance set is shifting in direction of a richer atmosphere for producing alpha by way of safety choice.

Past choosing the winners of the brand new regime, managers who make investments each lengthy and brief can deploy safety choice insights to harness dispersion as a return supply. This may be accomplished by positioning lengthy/brief portfolios to replicate anticipated return variations throughout the funding universe, taking lengthy positions in anticipated relative winners and brief positions in anticipated relative losers. This method seeks to generate returns within the cross-section of markets, exploiting the unfold in efficiency between lengthy and brief holdings in an atmosphere the place absolute market returns could also be extra muted.

Inside BlackRock’s Global Equity Market Neutral Fund (BDMIX), we analyze over 7,000 world equities every day by way of a data-driven course of that informs our lengthy/brief portfolio positioning. A comparatively even break up of lengthy and brief investments leads to a web market publicity of near zero, vastly reducing the influence of market direction on efficiency. As an alternative, returns are pushed by our means to forecast relative winners and losers as alternatives emerge – focusing on an uncorrelated alpha return stream. In 2023, we noticed this in follow because the technique delivered a 14.58% return (versus 5.09% for the class benchmark) with only a 0.07 correlation to the S&P 500 Index.1

Evolving portfolios with uncorrelated alpha

Financial and market dynamics have shifted post-COVID. Dispersion in firm fundamentals and inventory returns is rising, and static beta exposures might face headwinds relative to latest many years. This atmosphere introduces an expansive alternative set for methods like BDMIX that may benefit from larger dispersion to generate uncorrelated alpha – serving to to evolve investor portfolios for a brand new period.

This post initially appeared on the iShares Market Insights.