Try Media/iStock via Getty Images

With our past coverage of Cirrus Logic (NASDAQ:CRUS) noting revenue forecasting for 2024 in Cirrus Logic Beats Wall Street Again And More, we offer an update drawing from a significant level of new and important information. Cirrus held two conferences confirming ASP increases with new iPhones launching in September plus continued ASP growth over the next few years. The road ahead appears clearly labeled and bright. Shall we go for a drive? What kind do you favor, a thrill or slow and leisurely? Your choice.

June Through the Windshield

We begin with a look at June. The company guided:

-

Revenue to range between $290 million and $350 million.

-

GAAP gross margin to be between 49 percent and 51 percent.

-

[N]on-GAAP operating expense range between $118 million and $124 million.

- Non-GAAP tax rate of 22% – 23%.

Since the announcement, Apple (AAPL), Cirrus’ largest customer, was reported to have significantly increased unit sales year over year in China. “Shipments of foreign-branded phones in China increased by 52% in April to 3.495 million units from 2.301 million a year earlier…” Knowledgeable followers strongly believe that this was mostly iPhones. Apple employed heavy discounts driving this change. In other articles, we noted that the new Huawei competitive phones have severe technical issues, thus likely limiting future impacts.

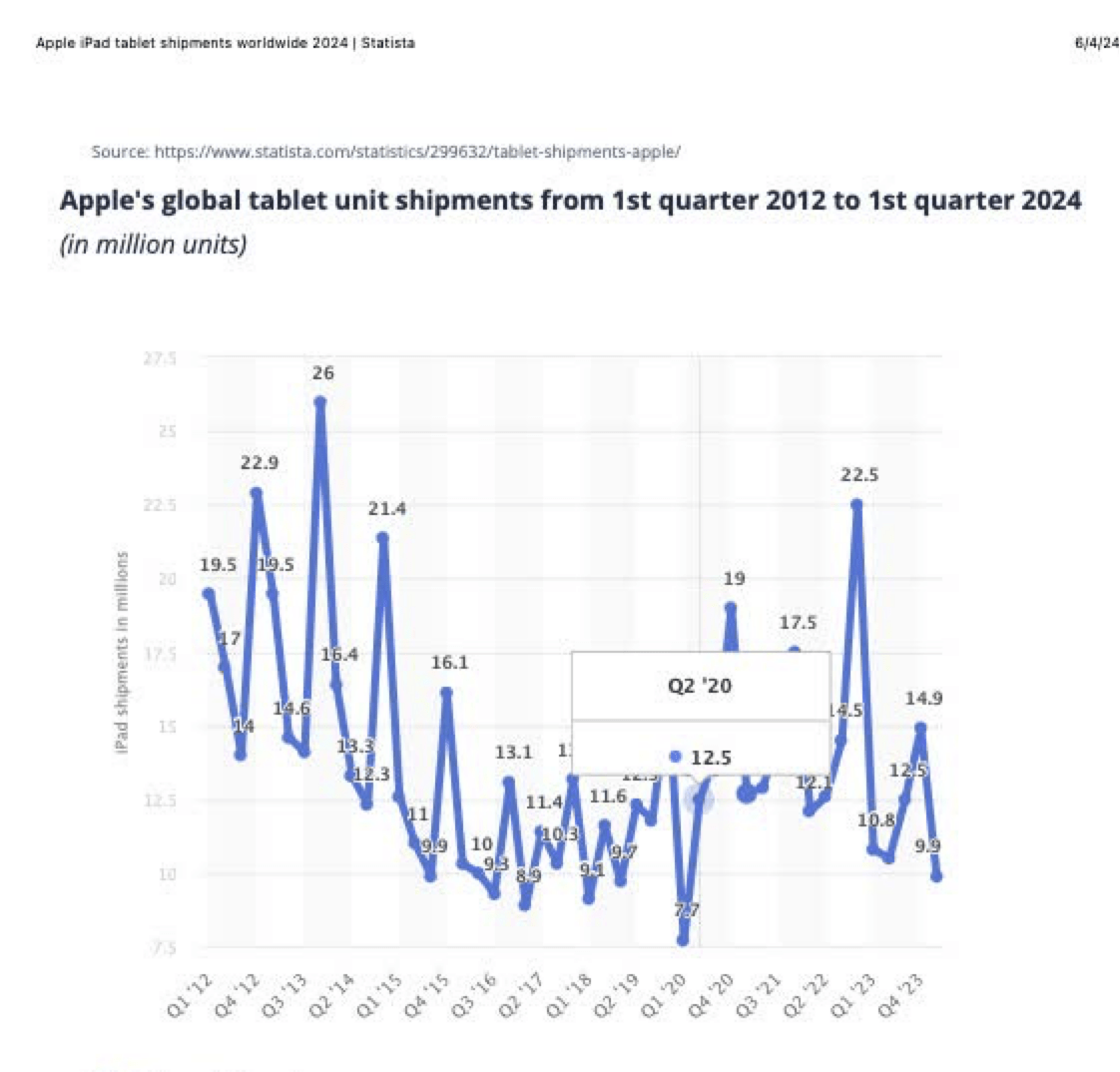

Apple also released highly talked about new tablets in early May. Although, we could not find sales data, reviews rave about the new products. We suspect that sales improved. From Statista, a chart shows the present weakness in unit volumes. The probability of a significant increase in unit sales is high.

statista

Continuing further with the state of the business, at the Stifel Cross Sector Insight Conference, John Forsyth, CEO, stated, “like our last fiscal year and particularly the last couple of quarters, what we’ve seen actually recently is steady and sustained demand… actually surprising to us.” Taking the updates into account, our comfort in predicting June increased. June revenue will exceed the guidance top-end reaching at least $360 million or $0.90 per share versus $0.67 a year ago.

The Latest

Now, for more news updates, let’s continue the trip. In our last article, we noted that Counterpoint Research estimated iPhone unit sales at 125 million for December and March, with September at approximately 50 million. This is our basis. Forsyth reinforced several paths forward at these conferences including continual ASP growth with the camera controls, codec/amplifiers, PCs and other future products.

With respect to the camera controllers, he noted:

- Continued accretion of ASP for the foreseeable future.

- Deeper penetration with the latest highest ASP product.

- Higher ASP products coming.

- The company is not likely to focus at all on Android.

- A continued growth, using this term “a healthy tailwind.”

We sense that $0.05 – $0.10 ASP increases per controller, four inside 90% of the phones or $0.20 – $0.40 per phone on a yearly basis, is likely to continue. This represents $50 – $80 million a year in revenue growth.

Forsyth continues with greater detail on the coming codec/amplifier update with:

- Confirming at the Cowen Conference, ASP increases without revealing a value.

- We now view this at least $1.5.

- $1 for the codec.

- $0.50 in total for the three new amplifiers.

- We now view this at least $1.5.

- Confirming natural accretion into the future.

- Clear that iPhone 16s use is only with the Pros.

- Next cycle, meaning 2025, continued accretion.

- Noting amplifiers will remove more passive parts.

At Cowen, Matt Ramsay asked:

Anything that, I guess, this audience should expect, hugely different from a content, ASPs, margins perspective as you go through that refresh?”

For the first time, Forsyth answered:

Well, we’ll certainly see some ASP accretion yeah, and that’s really reflective of the fact that there’s a lot of innovation in those products, even though they’re replacements for products that are there today. There’s a lot of R&D investment that goes into that, and we need to get paid for that. We also feel that we’re bringing a lot of additional value to the customer.”

With PCs, Cirrus management confirmed the path with real revenue starting in September significantly steepening next calendar year. A reminder, the SAM equals $1.3 billion.

Management still keeps investors in the detail dark with the next one, but in our view, this is huge, power management. Product development, for improving power management, both charging and conversion, progresses. Our interest resides with power conversion. Noted in a past conference, Cirrus portrayed this product with:

- Requiring fewer passive parts.

- Reducing power lost by 90%.

- Being significantly smaller in size.

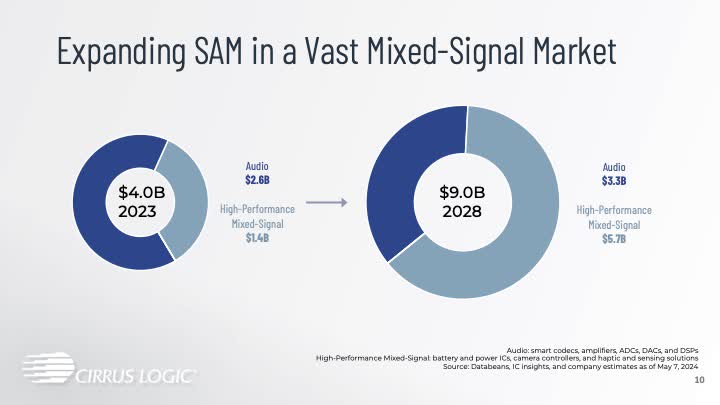

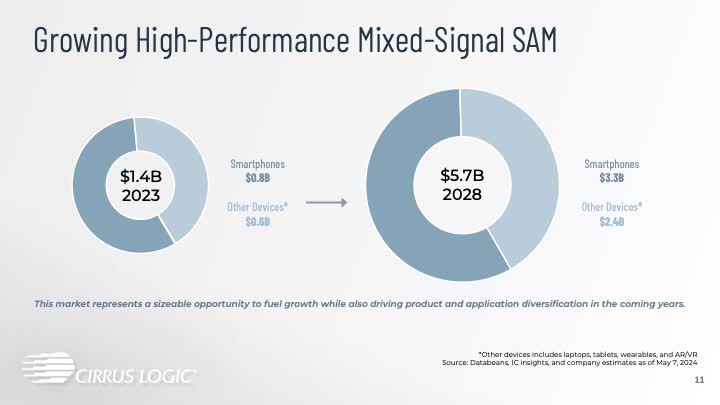

Cell phones or PCs with batteries require several step changes in power, generally two or three or more in each device. Again, in the past, management discussed $0.75 – $1.25 per device or approximately $2 per cell phone. Our long-term belief is that this technology likely penetrates into more than Apple products, maybe into the 50% – 60% portion of the smartphone market, Cirrus’ once targeted percentage. This equals north of 600 million units. The SAM is much higher. The next two slides from the latest presentation show this point quite nicely.

Cirrus Logic

And the next slide showing HPMS’ SAM.

Cirrus Logic

A careful look reveals the major change is within smartphone SAM. The company estimates the delta at almost $3 billion.

This statement made in a previous Shareholder Letter continues to haunt us. Under HPMS in Smartphones, the March 2024 Shareholder letter contained,

“The company made solid progress executing on our strategy to drive diversification through our HPMS product line. Our engineering teams are developing new intellectual property that we believe is key to delivering innovative HPMS products in our newest applications, including battery and power and camera control.”

Later during that conference, Forsyth noted that the power and battery technology is still too early to discuss. A smartphone OEM is interested, which translates to Apple, in our view.

A General Note

Before continuing, let’s review a note directly taken from our last article.

- Cirrus ships 60 million units of iPhone parts in September with an ASP average of $5 before the coming 2024 change.

- Cirrus’ new closed loop controller (“CLC”) ASP increased a modest amount toward $1.5 from $1.0 or so within older phones.

“Also, for this year, Cirrus’ CLC solution increased in half the phones, Pro Models, by $0.40-$0.50 ASP or $15 – $20 million. This increase in iPhone share increases to approximate 80% going forward.”

September Quarter Update from the Windshield

Now we offer for quarter estimates new updates beginning with September. The updates include direct quotes from that article with changes bracketed.

“Concerning the iPhone ASP increases, analysts tried several approaches for more detail. A question was asked about the new Apple iPhone parts. In part, “assume that obviously means some higher content.” Management did not deny ASP increases but did answer with “that we see reasons for efficiency to increase for prices to come down somewhat in the coming years.” For investors, Cirrus has long-term plans for holding the ASP solid.”

“When asked about back half of the year gains vs. last year, John Forsyth, CEO, answered, “And we do also, as you said, we feel good about the content that we have coming this fall. But beyond that, we’re not giving guidance right now.””

“Now, in the September quarter, we expect ASP growth from:

- Further penetration into 90% of the phones using Cirrus’s premium CLC.

- [$1.5] ASP growth with the new codec amplifier pair.

- Ramping of new PCs with Cirrus inside to the tune of 2 million a quarter at $5 ASP.”

“A table follows with an increase estimated for a year-over-year change.”

| Revenue Adders (Millions) * | PCs | CLC | New Codec @ [$1.5] |

| September | $10 | $10 ** | $40 [***] |

| Additional Parts at $3.5 + **** | $15 |

* 60 million units delivered.

** 40% of 60M million units times $0.40 – $0.50.

[*** 60 million time 0.4 times $1.5.]

**** Apple will likely add extra, over normal, codecs and amplifiers guessed at 5%.

“Cirrus reported $480 million in revenue in September 2023. When adding the increment shown above, this year’s September might range between [$550 – $560 million.]”

December Quarter

“Our December quarter estimate assumes 75 million iPhones sold and delivered.”

| Revenue Adders (Millions) | PCs | CLC | New Codec @ [$1.5] |

| December | $10 | $12 | $50 |

“The total for December might equal $620 million plus [$75 million] totaling near $700M.”

March Quarter

“Our March quarter estimate assumes [50 million] iPhones sold and delivered.”

| Revenue Adders (Millions) | PCs | CLC | New Codec @ [$1.5] |

| [March] | $20 | $10 | [$30] |

“The total for March might equal $375 million plus $60 million, totaling near [$435] million.”

Summary of the Totals for the Next Three Quarters

A table summarizes the estimated earnings.

| Earnings Estimate | Revenue (Millions) | Non-GAAP Exp. (Millions) | Tax Rate | Share Count (Millions) | Earnings (Rounded) * |

| September | $555 | $125 | 22% | 55 | $2.2 |

| December | $700 | $130 | 22% | 54 | $3.2 |

| March | $440 | $120 | 22% | 53 | $1.5 |

* Margin steady at 50%.

Cirrus seems positioned to grow earnings significantly on a year-over-year basis, with our estimate of slightly less than $8. Of importance, we believe that tablet unit sales will increase year over year with its refresh and targets at AI. The above chart from Statista shows how low the bar for improvement is. With tablet revenue in mind, we believe that our estimate might be low. It also excludes iPhone unit volume increases.

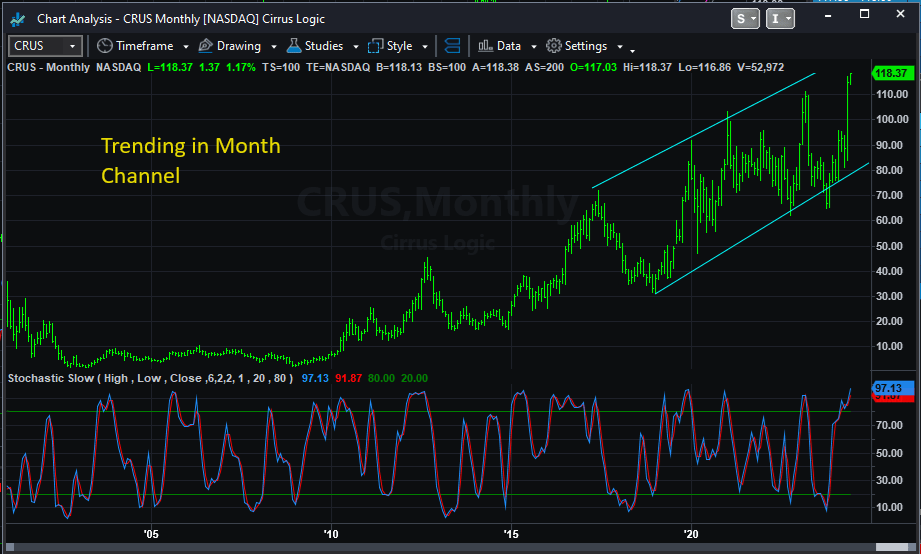

Month Chart

Next a month chart from TradeStation helps illustrate possible future stock prices.

TradeStation Securities

The current pricing resides at the top of the trading channel. In time, that channel will increase in value. With significant earnings growth likely to continue, the channel will be pushed north.

Risk & Summary

Before discussing risks, it seems important to discuss coming years. From the new codec/amplifier, we expect additional revenue from deeper penetration going from 40% to 90% next year. That 50% increase might add $200 million. Noted above, expected revenue increases from the camera controller are likely to continue at $50 – $80 million a year. And PC revenue begins steep growth into the future $200 million a year, next year. This represents more than $2 a share gain in FS-2026. A very valued poster on Investor Village, AZWarrior observed that during growth periods, Cirrus’ stock price tends to follow near a 20 P/E placing $150+ very possible.

The potential might be significantly higher if our belief of power conversion coming to the phone world is correct. That alone adds between $5 and $10 per share in earnings. And we haven’t included much for the PC markets, $200 million vs. the $1.3 billion SAM. The earnings story for Cirrus continues to grow.

Yet, Cirrus carries risk. A China invasion of Taiwan can’t be viewed as positive. Deep recessions become headwinds. But, during the next year, Cirrus’ trajectory with new design wins is set. The value of new revenue isn’t small. We continue our buy rating with a watch for lower prices. At some point, the market must correct. A nice road trip today wasn’t it.