100pk

Tough instances usually separate the boys from the boys, and the best-run corporations from these with mediocre and poor administration groups. Since 2019 we’ve got seen COVID hit, value ranges rise exponentially, and conflicts overseas create added challenges as nicely.

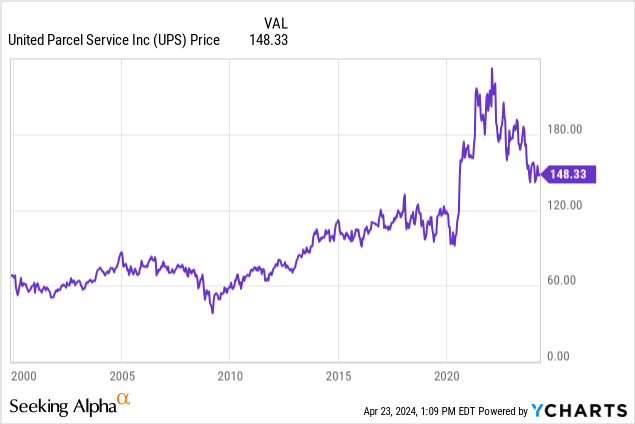

One firm that has struggled since inflation started to speed up in early 2021 is UPS (NYSE:UPS). The $124 billion greenback provider was one of many higher performing shares out there for a while, however this firm has constantly struggled over the past 3 years.

UPS is down 10.44% as measured by whole returns since Might of 2021, whereas the S&P 500 is up 25.75% as measured by whole returns throughout this similar time interval.

I final wrote about UPS in April of 2023, and I rated the corporate a promote primarily due to what I considered as a peaking revenue cycle and the specter of corporations corresponding to Amazon (AMZN). I’m downgrading the inventory to a robust promote at the moment. Administration has not confirmed they’ve an actual or substantive plan or technique to drive significant progress within the US or overseas within the present working surroundings, and the corporate is prone to proceed to see rising prices because the provider continues to spend closely within the US as nicely. The inventory additionally appears to be like overvalued utilizing a number of metrics given the deteriorating progress outlook for the corporate’s core enterprise.

UPS’s current earnings report highlighted the continued challenges administration has failed to regulate to since costs and prices started to rise considerably for the provider in early 2021. The corporate lately reported earnings of $1.43 GAAP precise and revenues of $21.71 billion, beating consensus estimates for EPS however lacking on revenues. Estimates have been for EPS of $128 a share, whereas anticipated income was $21.84 billion.

The earnings report appeared respectable on the face of issues, however there are a number of key underlying issues that ought to alarm traders within the current disclosures. First, administration’s steering was for almost no income progress this 12 months. Whereas UPS did see some slight margin enlargement and the corporate was capable of beat lowered earnings per share estimates, the corporate nonetheless expects revenues to be between $92-$94 billion this 12 months, versus revenues of almost $91 billion for the total 12 months in 2023. UPS additionally said that for the quarter that the typical every day quantity fell by 3.2% from the identical time final 12 months, and common income per piece fell by .3% on a year-to-year foundation. The leaders of this provider additionally confirmed that they plan to proceed to spend aggressively. The corporate’s present capital expenditure plans for this year are to spend $4.5 billion. UPS continues to spend aggressively whereas transport quantity and revenues per shipped merchandise are falling, and administration has not been profitable to find various revenues as e-commerce continues to gradual post-pandemic.

UPS has been damage considerably by the slowdown in e-commerce the corporate has seen since 2021, and administration’s plan to spend aggressively as part of the carrier’s technique to scale back reliance on guide labor and enhance productiveness. The corporate additionally hopes to drive revenues within the well being care logistics enterprise to offset the anticipated proceed decline in e-commerce. The issue with UPS’s plan is competitors within the well being care phase is fierce, and Amazon (AMZN) offering delivery in 50 states with Amazon clinic. UPS additionally expects labor prices to rise 9% this 12 months alone, and the corporate’s spending plan has not been impactful in decreasing overhead. UPS expects capital expenditures to be almost $17-18 billion over simply the subsequent 3 years between 2024-2026.

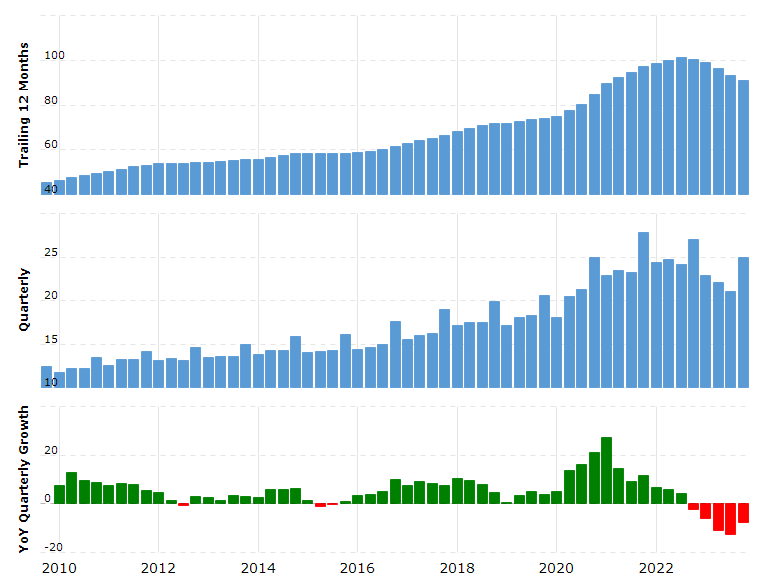

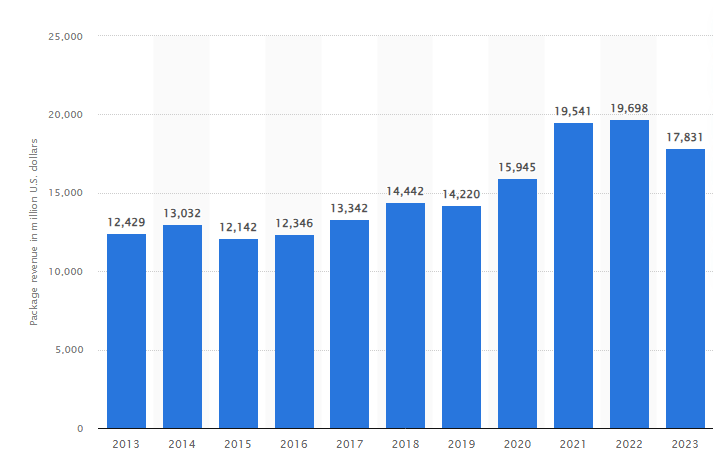

UPS’s quarterly income peaked in December 2021, and the corporate’s annual revenues have been in regular decline since September 2022. For my part, administration has not been capable of function efficiently within the present financial surroundings.

A Chart of UPS’s Revenues (Macrotrends)

UPS has additionally been spending aggressively for a number of years now on new cap-ex initiatives, and administration introduced plans to spend almost $5 billion this 12 months.

A Chart of UPS’s CapEx (Finbox)

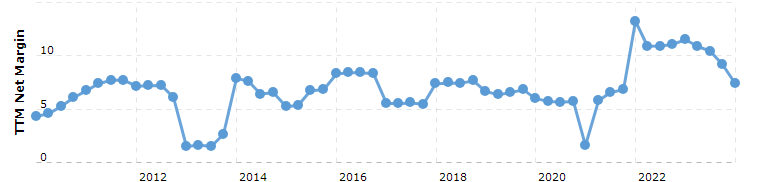

The corporate was spending lower than $3 billion a 12 months previous to 2017, however the provider’s spending has elevated dramatically over the past seven years. That is additionally why the margin compression UPS has seen lately ought to concern traders as nicely. Whereas the corporate reported working adjusted margins within the first quarter at 8%, the provider’s working adjusted margins have been 11% final 12 months.

A Chart of UPS’s Margins (Macrotrends)

UPS’s internet margins have been generally decline since late 2021, and the corporate can be expecting to see a 9% in labor prices alone as the brand new contracts with staff start to kick on this 12 months. This comes after the corporate noticed a 12% enhance in wages within the fourth quarter of final 12 months, forcing the company to cut nearly 12,000 jobs.

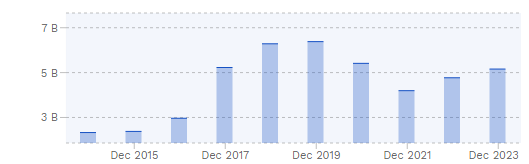

UPS’s worldwide income progress has additionally stagnated over the past three years.

A Chart of UPS’s Worldwide Revenues (Statista)

The main provider noticed worldwide revenues attain almost $20 billion in 2021, however administration hasn’t been capable of drive any significant progress abroad over the past 3 years, the place rising prices have been an issue as nicely.

This is also why the inventory nonetheless appears to be like overvalued utilizing a number of metrics. Costs stay excessive regardless that the speed of inflation has come down, and the affect of the labor scarcity and better power prices is prone to proceed. UPS raised costs by almost 6% up to now this 12 months after rising charges by almost 7% in 2023, and with elevated competitors from Amazon and volumes at present falling, the corporate will not possible have the ability to proceed to boost charges at this degree transferring ahead. Analysts are additionally predicting simply 4-5% income progress for UPS over the subsequent a number of years as nicely.

A chart of UPS’s anticipated Income Progress from 2024-2028 (In search of Alpha)

UPS at present trades at 17.93x anticipated ahead GAAP earnings and 15x predicted ahead EBIT regardless that the provider has seen revenues and earnings per share proceed to say no over the past a number of years. An organization rising revenues at simply 4-5% a 12 months shouldn’t be buying and selling with a progress a number of, and UPS additionally faces longer-term and shorter-term headwinds corresponding to elevated competitors from Amazon and prices. UPS has seen a notable slowdown in transport quantity, and the corporate has additionally been coping with falling income per package deal for the reason that provider over the past 12 months. Administration’s current conservative full-year steering for 2024 additionally exhibits that the present technique the corporate is pursuing is not prone to ship the expansion the market is pricing in at UPS’s present a number of of almost 18x predicted ahead GAAP earnings.

Amazon lately surpassed UPS as the biggest provider within the US, and the corporate has constructed an enormous fleet of vans that positions the web retailer nicely to compete with UPS. Amazon additionally has far additional cash to put money into the enterprise than UPS. UPS can be going through greater power and labor prices, the present plan by administration to rely extra on automation for package deal sorting does not materially change the corporate’s dependence on unionized labor. Given the headline danger UPS faces and the slowing income and EPS progress the corporate continues to see, this inventory shouldn’t be buying and selling at greater than a a number of of 12-14x anticipated ahead earnings, this isn’t a progress inventory.

UPS’s earnings per share have been declining over the past three years regardless of administration initiating a $5 billion greenback buyback final 12 months that has not added shareholder worth. Whereas administration has raised the dividend by 10% per 12 months over the past decade, the inventory has struggled since 2021. Whereas some analysts are projecting mid-double digit EPS progress for the corporate over the subsequent a number of years, these estimates are possible far too excessive with labor and power prices remaining very excessive and competitors from corporations corresponding to Amazon selecting up. The provider has not been capable of drive any significant income progress for years now, and UPS is counting on the share buyback to ship modest EPS progress. Administration’s heavy, aggressive current dividend raises additionally point out the corporate is having bother discovering methods to take a position capital within the enterprise or to seek out significant acquisition alternatives.

Recessions and inflationary durations usually power administration groups to make powerful decisions, and these difficult instances often present who the best-run corporations are. UPS’s administration group has didn’t drive any significant progress within the US or overseas over the past a number of years, and the present troublesome working surroundings is prone to endure for a while. Whereas the provider’s management group is dedicated to returning worth to shareholders, traders ought to have the ability to discover higher worth elsewhere.