Urban Edge Properties (UE) is a grocery-anchored shopping center REIT concentrated in the D.C. to Boston corridor. It has become interesting as its valuation has steadily become cheaper while shopping center performance continues to improve. The ongoing discussion of a Whitestone (WSR) buyout also adds a fresh angle to UE. We will begin with UE analysis and then explore the M&A.

UE has historically traded at a high valuation due to having superior catchment radius statistics regarding population density and household income. In the last 10 years, however, it has materially underperformed shopping center peers.

SA

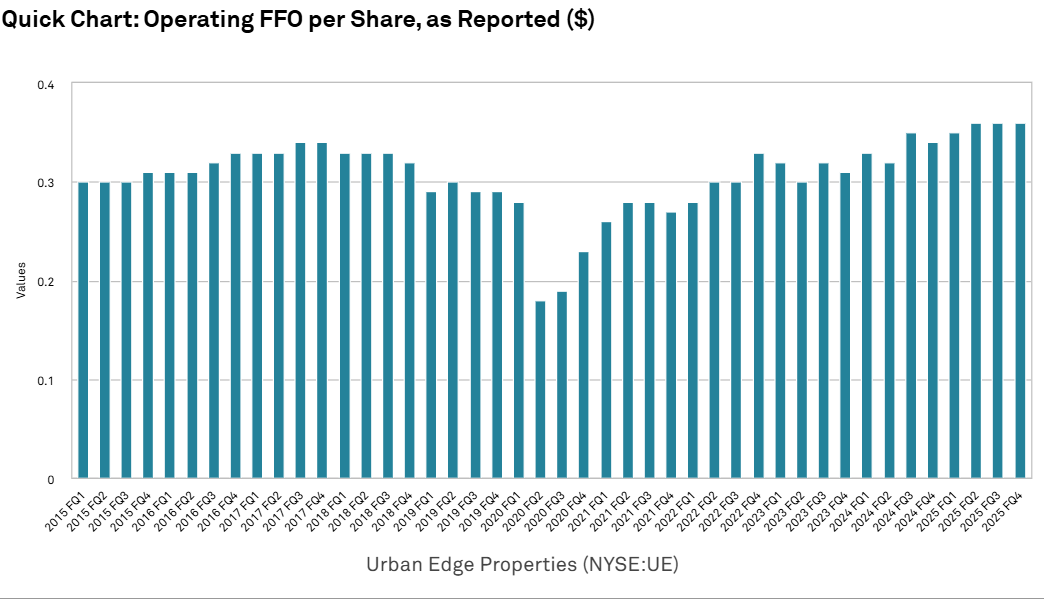

This stock price underperformance coincided with a period in which fundamentals generally improved, even inclusive of the Covid dip.

S&P Global Market Intelligence

With higher earnings and a lower stock price, UE has fallen into value territory. Specifically, it is trading at 17.6X AFFO and 79% of net asset value. This makes the stock interesting to us, so we dug into the fundamentals and outlook.

UE fundamentals: Advantages and disadvantages

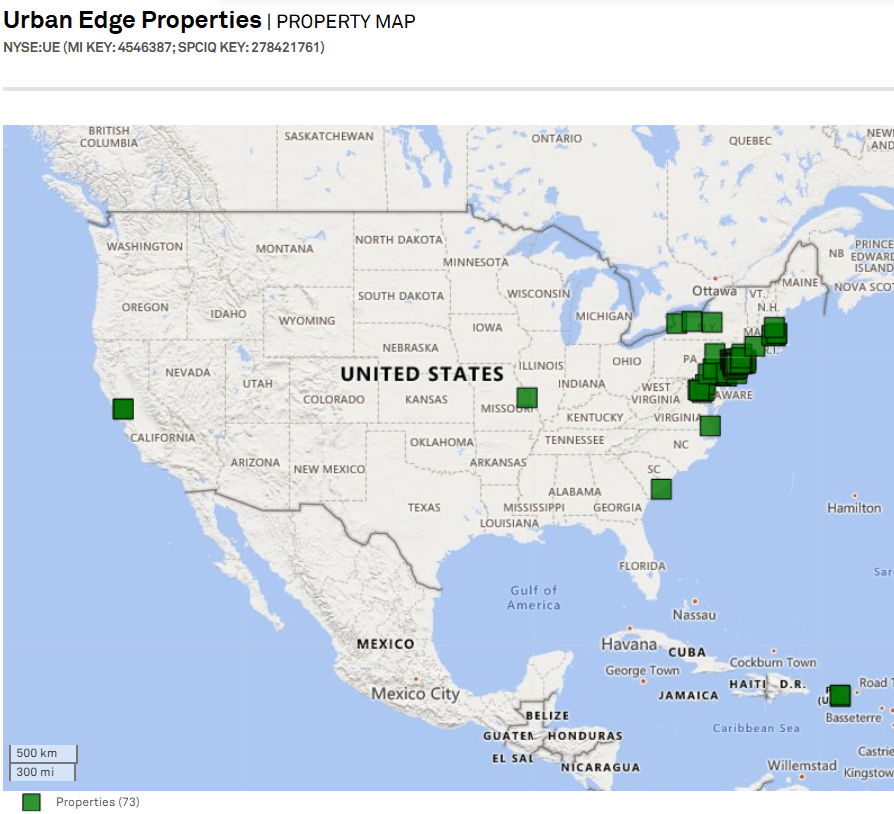

Aside from a few straggler properties, UE’s NOI is overwhelmingly driven by its Northeastern submarkets.

S&P Global Market Intelligence

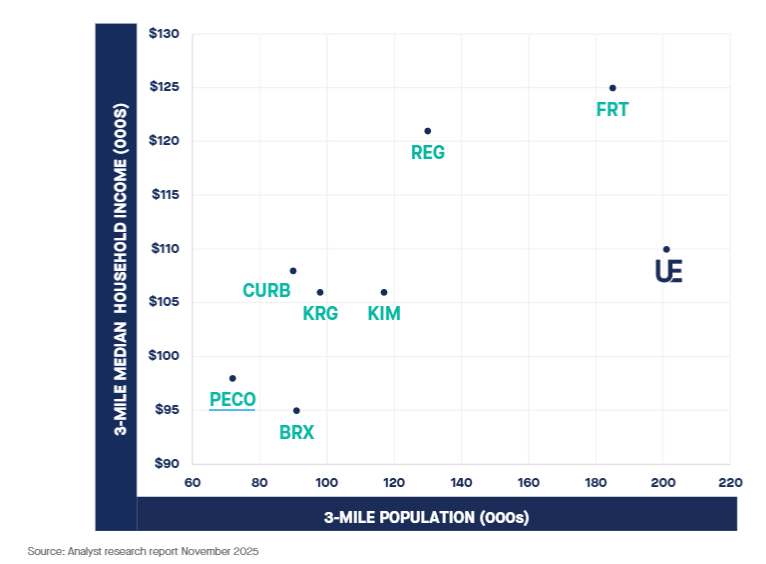

These markets significantly differentiate UE from peers, which tend to be more sunbelt and west coast. Population density in UE’s submarkets is very high, with over 200,000 people in a 3-mile catchment radius.

UE

Average household income is also well above average, with only Regency and Federal Realty higher.

Naturally, rent per square foot will be higher given these metrics. UE has rent per foot of $21.50 compared to a shopping center REIT average of $20.45.

The difference is actually much larger than those numbers make it look, as UE has a high percentage of anchor space, which pulls down rent per foot. Its small shops average $39.94 per foot.

These first ring submarkets are in high demand and somewhat limited in available land, which makes it difficult to build competing supply. This results in very high occupancy and property value. UE’s portfolio is 96.7% occupied, with 80% of centers grocery-anchored.

We consider this full occupancy, as frictional vacancy makes going above 97% unsustainable.

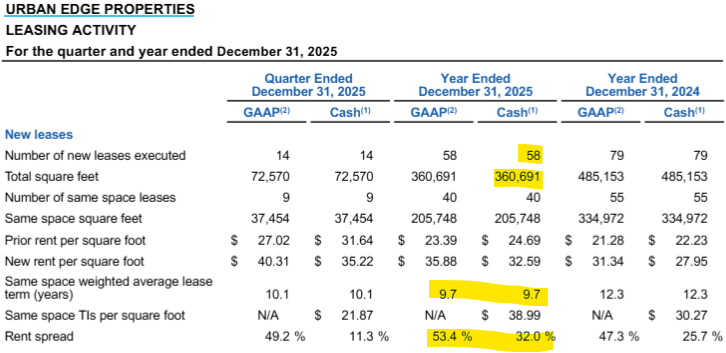

Full occupancy is a bit of a double-edged sword. On the positive side, it allows UE to instruct its leasing agents to push rental rates more aggressively. Over the past 4 years, UE has consistently been over +20% on new lease spreads. In 2025 they achieved new lease spreads of +53.4% GAAP and +32% cash.

Supplemental

Shopping centers have broadly experienced strong rental rate spreads, but UE is even higher than peers.

Some of the leasing strength is due to the high occupancy. Without having to worry about filling space, they can be quite aggressive in pricing negotiations.

The downside to already having full occupancy is that all the organic growth has to come from rate. Peers with lower occupancy, like Brixmor (BRX), are growing from both occupancy increases and rate growth.

Another factor that is limiting UE’s same-store NOI is that their tenants seem to have a higher than normal amount of renewal options. Out of 1.5 million square feet of leasing in 2025, more than 1.1 million of it was renewals and options. While the spreads on renewals are still positive at +19% GAAP, they are nowhere near as strong as the new leases.

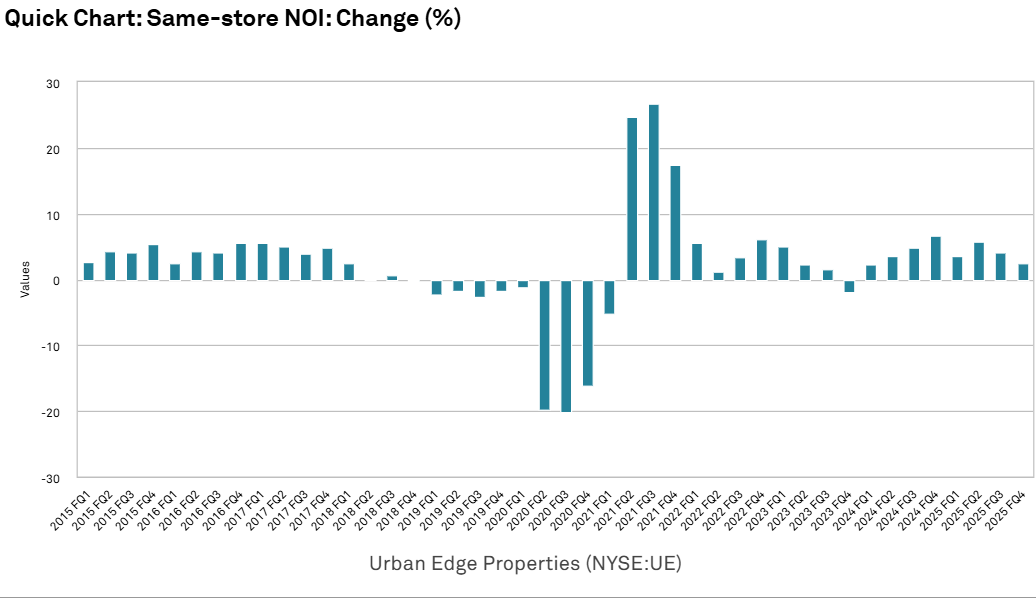

Thus, despite the incredibly high lease spreads and mark-to-market opportunity, Urban Edge’s same-store NOI has only been about average for the sector.

S&P Global Market Intelligence

Ignoring the Covid-driven crash and recovery that hit the whole sector, UE’s same-store NOI growth has generally been in the 3%-5% range. Strong, but largely in line with peers.

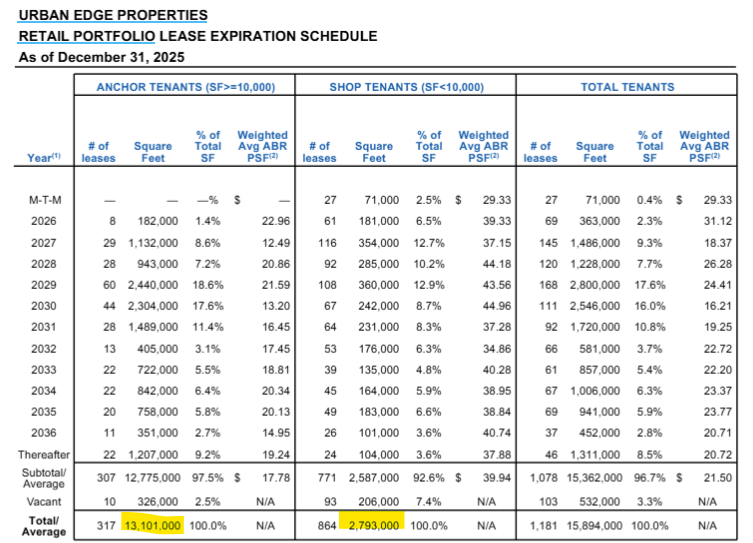

Another differentiating aspect of Urban Edge’s portfolio is that it is overwhelmingly big boxes.

UE

It has over 13 million square feet of anchor space (>10,000 sf) compared to just 2.8 million square feet of small shops.

I view this as a bit of a detractor, as small shops tend to have more favorable leasing economics. It does, however, give UE significant redevelopment potential. They have been averaging roughly 14% cap rates on redevelopment and could theoretically re-demise many of these big boxes into smaller shops to capture the much higher rent per square foot offered by that product.

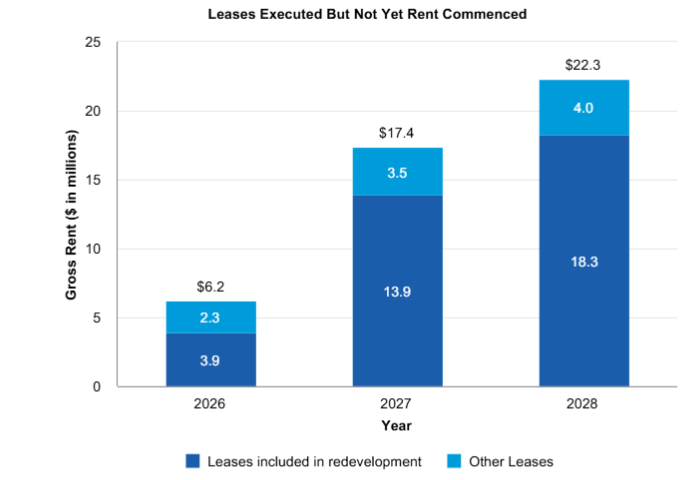

SNO leasing

Signed but not open leases, or SNO leases, are a key concept in shopping centers right now. Due to its redevelopment activity, UE has particularly long lead times on some leases.

UE

Inclusive of leases that commence through 2028, UE has SNO leases of $22.3 million, or just under $0.18 per share.

This provides strong visibility into future NOI growth.

Valuation and buyout potential in an M&A heavy market

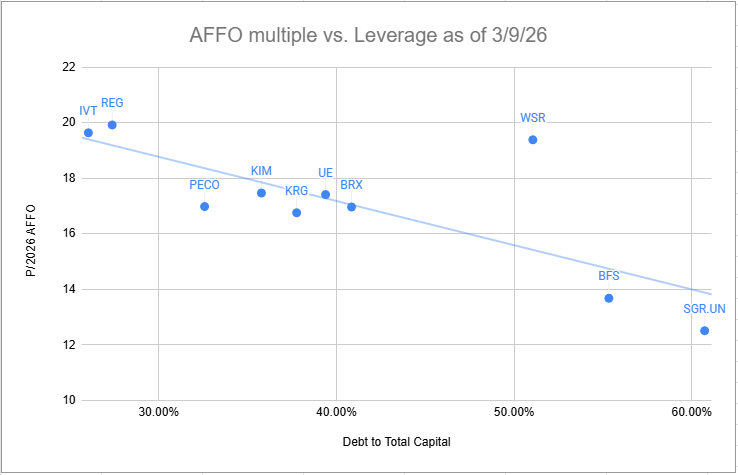

On AFFO multiple UE is trading precisely in line with peers given its current leverage.

Portfolio Income Solutions

You may note that Whitestone (WSR) is a significant outlier with an AFFO multiple far too high for its leverage.

There are two reasons for this:

- Whitestone has high NOI relative to its AFFO given its relatively small size, resulting in high overhead as a percentage of revenue.

- Whitestone is the subject of a potential buyout.

In addition to previous takeout bids from MCB, Whitestone is likely getting bid on by Blackstone (BX) and/or TPG.

Blackstone does not mess around. They already bought ROIC at a much lower cap rate (higher price) than where WSR is trading. I suspect they will bid a high enough offer that will make it difficult for WSR to refuse. My hunch would be in the $17 to $20 range.

We, along with our clients, have sold about half of our WSR in the run-up but still hold about 105,000 shares in anticipation of further upside should a merger manifest.

In addition to playing the potential Whitestone buyout, it behooves investors to consider what else might be on the table.

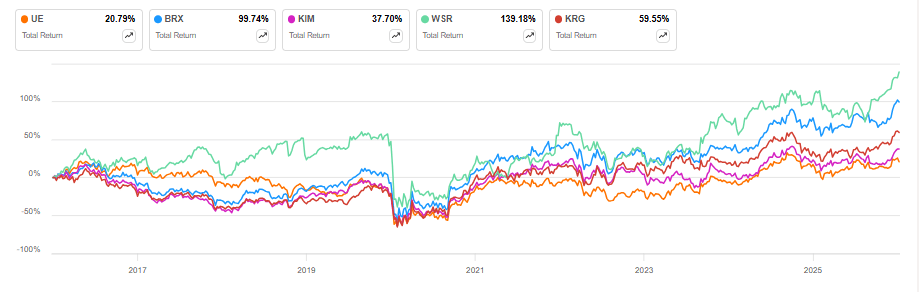

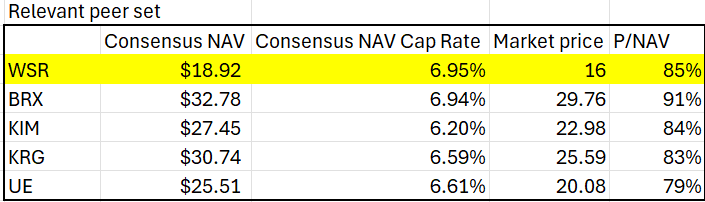

In my opinion, the 5 most in-play shopping centers are WSR, Brixmor (BRX), Kimco (KIM), Kite Realty (KRG), and UE.

2MC

Whitestone is, of course, top of the list because of previous buyout offers and the active discussions.

The factors that make WSR so attractive to buyers are:

- A high implied cap rate, currently trading in the 7s

- High overhead cost, which can be immediately removed by consolidating it with a buyer’s existing assets

- Desirable assets in high growth submarkets

Urban Edge is the top contender in valuation, trading at just 79% of NAV. The land-limited nature of UE’s markets could also stimulate a buyout, as it is difficult/expensive to develop assets there, making buying an existing portfolio one of the cleanest ways to gain exposure to these markets.

Brixmor was previously bought by Blackstone before being reintroduced to the public market. Since going public, BRX has redeveloped a large portion of its portfolio and greatly enhanced NOI per square foot. Blackstone often watches its former assets and goes in for a second helping opportunistically. With the discount at which BRX is trading and its very strong organic growth, it could be a takeover target.

Kite Realty (KRG) is later cycle in its growth. If the rest of the sector is in the 5th inning of same-store-NOI growth, KRG is in the 7th. They have marked a larger percentage of their portfolio to market, with a higher percentage of its portfolio reaching that stabilized full NOI. These stabilized assets often trade at lower cap rates in the private market, as many buyers want assets that will passively perform.

Kimco used to be more likely to be a potential buyer in an M&A scenario due to their size and reputation as a consolidator. However, in 2025 Kimco’s valuation fell dramatically, making them one of the clear value plays in the shopping center sector. They have bounced back nicely in 2026, almost keeping up with WSR even with WSR’s potential buyout surge.

S&P Global Market Intelligence

Yet KIM remains significantly discounted at 84% of NAV. KIM is likely too large to be bought by a fellow public REIT, but some of these private equity players have such deep pockets that KIM’s size could be seen as an efficient purchase rather than a deterrent.

Noting that Blackstone bought ROIC at a 6.2% implied cap rate and ALEX at a 6.4% cap rate, each of these REITs could be a highly accretive purchase given how cheaply they are trading.

Shopping center fundamentals have continued to improve since BX’s former purchase, so the fact that these REITs are trading at cap rates in the high 6s and low 7s today is, in my opinion, significant undervaluation.

The bottom line

Shopping centers as a sector have excellent fundamentals with steady demand growth and a paucity of new supply. They have a long runway of mid-single-digit organic growth driven by the large spread between existing rental rates and market rental rates.

We see much of the sector as undervalued and hold many of the REITs. Whitestone, Kimco, Brixmor, and CTO Realty (CTO) are key holdings for us.

Urban Edge is not a company we have been invested in, but due to its newly cheap valuation, we are adding it to our radar screen. I think the high percentage of anchor space makes it marginally less attractive than some of its peers, but it is clearly cheap on an asset value basis and is a valid investment.

We will watch UE and continuously monitor its relative opportunity.