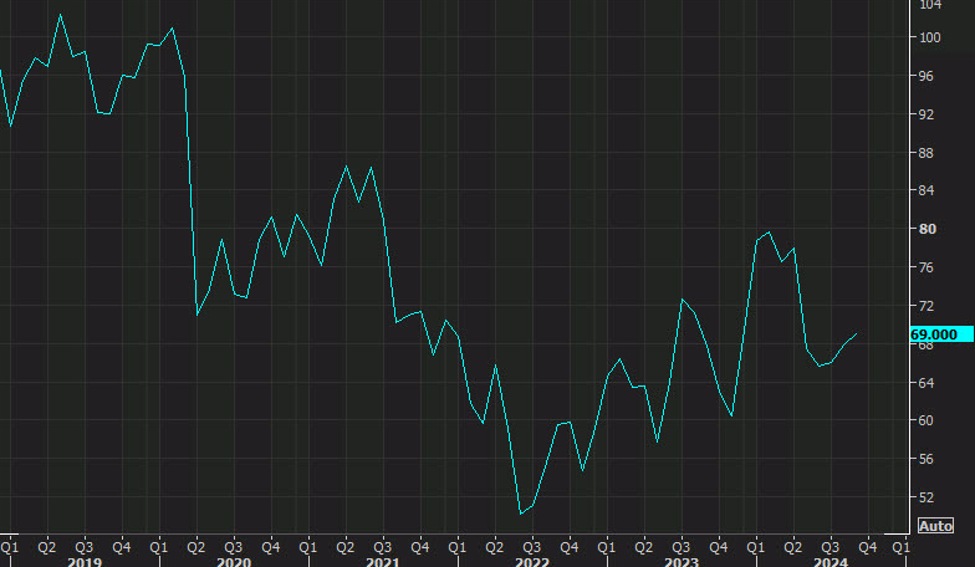

- Sept final reading was 70.1

- Current conditions 62.7 vs 64.3 expected (63.3 prior)

- Expectations 72.9 vs 75.0 expected (74.4 prior)

- 1-year inflation 2.9% vs 2.7% prior

- 5-year inflation 3.0% vs 3.1% prior

I don’t put much stock in this report as it’s highly politicized and we’re at the peak of the political cycle.

Here is the commentary in the survey:

Consumer sentiment inched down a meagre 1.2 index points in October,

well within the margin of error, following two straight months of gains.

Sentiment is currently 8% stronger than a year ago and almost 40% above

the trough reached in June 2022. While inflation expectations have

eased substantially since then, consumers continue to express

frustration over high prices. Still, long run business conditions lifted

to its highest reading in six months, while current and expected

personal finances both softened slightly. Despite widespread news

coverage about the Middle East and Ukraine, few consumers connected

these developments to the economy. Concerns over these conflicts climbed

this month but were relatively rare, mentioned spontaneously by less

than 5% of consumers. With the upcoming election on the horizon, some

consumers appear to be withholding judgment about the longer term

trajectory of the economy.

This chart speaks to those comments:

This article was written by Adam Button at www.forexlive.com.