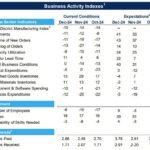

- Prelim was 69.0

- Prior was 67.9

- Current conditions 63.3 vs 62.9 prelim (61.3 prior)

- Expectations 74.4 vs 73.0 prelim (72.1 prior)

- 1-year inflation 2.7% vs 2.7% prelim

- 5-year inflation 3.1% vs 3.1% prelim

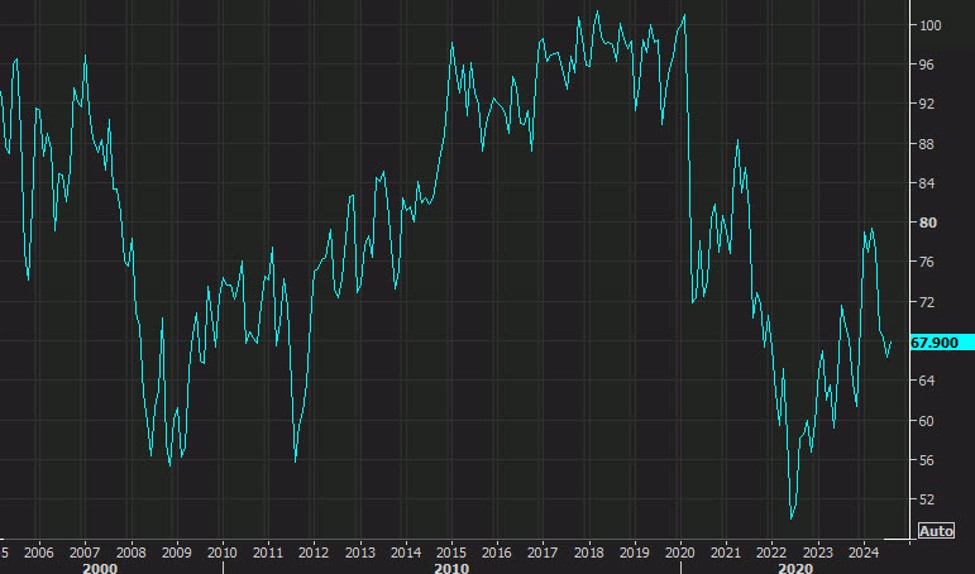

The final revisions are rarely a market mover but the chart illustrates how this is a different picture than consumer confidence, which is nearing a breakdown.

A big part of the divergence is that the UMich survey is influenced by a massive amount of partisanship.

The comments in the survey also highlight politics:

Consumer sentiment extended its early-month climb, ultimately rising

more than 3% above August. This increase was seen across all education

groups and political affiliations. Furthermore, all five index

components gained, led by a 6% surge in one-year business expectations.

The expectations index is now 13% above a year ago and reflects greater

optimism across a broad swath of the population. While sentiment remains

below its historical average in part due to frustration over high

prices, consumers are fully aware that inflation has continued to slow.

Sentiment appears to be building some momentum as consumers’

expectations for the economy brighten. At the same time, many consumers

continue to report that their expectations hinge on the results of the

upcoming election. Relative to August, consumers across political

parties are increasingly expecting a Harris presidency, though about

two-thirds of Republicans still expect Trump to win.

Someone will be disappointed after November.