Smith Assortment/Gado/Archive Pictures through Getty Photographs

Introduction

Expertise shares have been an awesome place to be. I believe we are able to all agree on that. It appears that evidently every thing tied to the present AI revolution is doing nicely, with shares like NVIDIA (NVDA) flying greater like there is not any tomorrow.

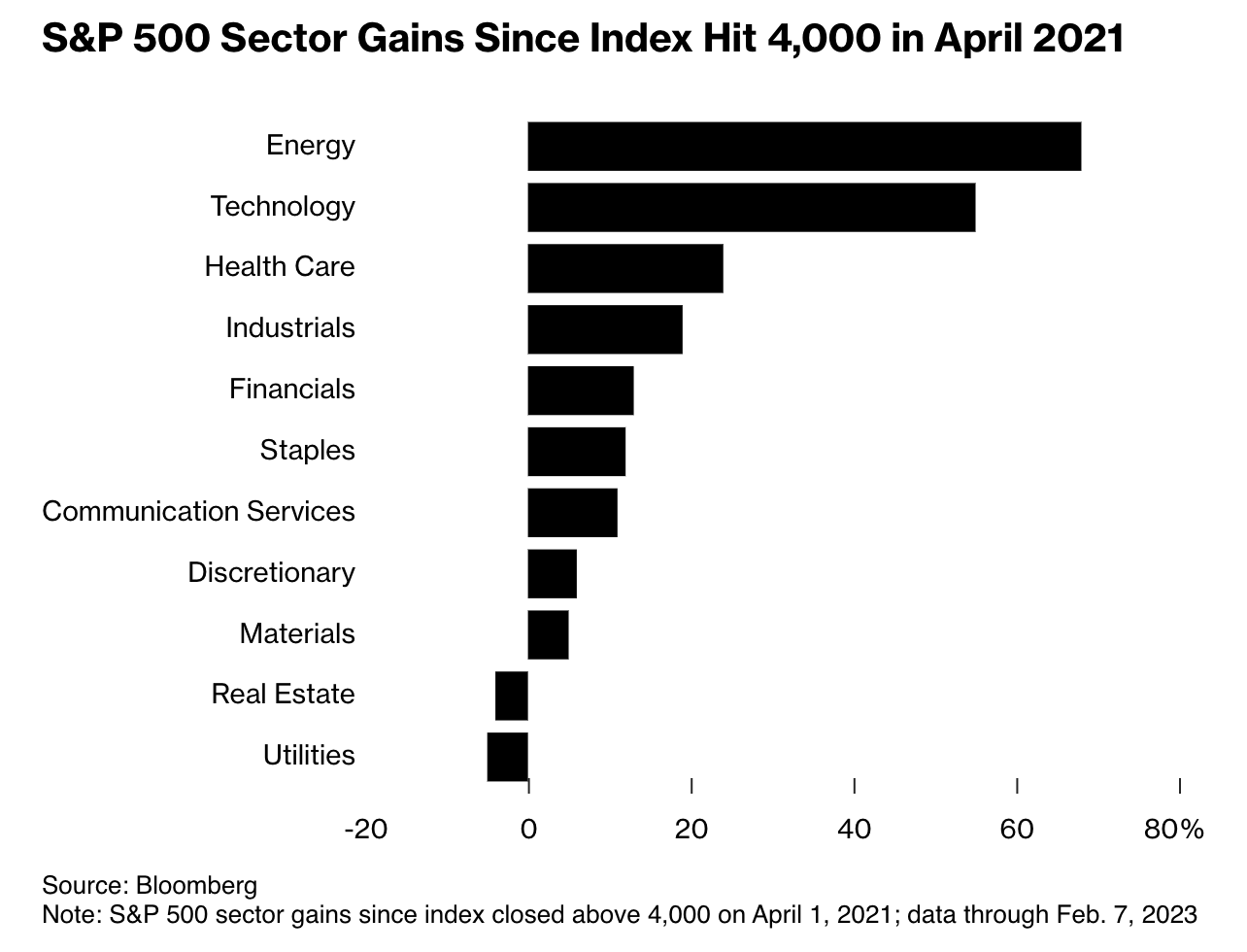

This has helped the S&P 500 so as to add 1,000 factors between April 2021 and February 2024.

Nonetheless, what’s fascinating is that know-how was NOT the best-performing sector throughout this era. Nope. Power did higher, gaining greater than 60%!

Bloomberg

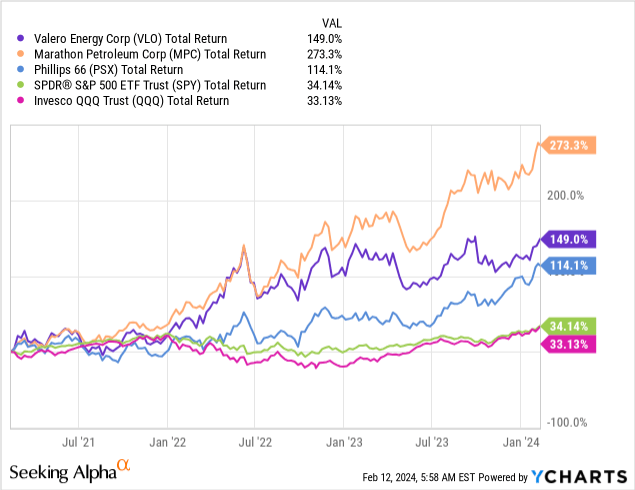

As we are able to see within the chart under, over the previous three years, the tech-heavy ETF (QQQ) has returned 33%, which is roughly in keeping with the efficiency of the S&P 500.

Throughout this era, the three main pure-play refinery shares in america, Valero Power (NYSE:VLO), Marathon Petroleum (MPC), and Phillips 66 (PSX), have all outperformed the market by an enormous margin.

Valero, the star of this text, has been a holding of mine for a really very long time till I made a decision to give attention to upstream oil manufacturing, which higher matches my private vitality thesis – a minimum of in the meanwhile.

Previously few years, we’ve got discussed Valero on a really frequent foundation, as it isn’t solely probably the most fascinating vitality shares within the downstream (refining) {industry} but in addition an organization susceptible to geopolitical turmoil just like the invasion of Ukraine and the tariffs that adopted.

The corporate additionally went by a powerful restoration, because it refused to chop its dividend through the pandemic, leading to an elevated debt load, which has been decreased quickly in recent times.

In consequence, the inventory went again to doing what it does greatest: outperforming the market.

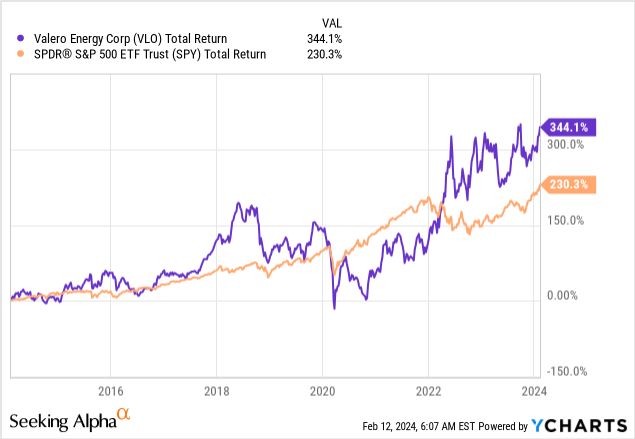

Over the previous ten years, VLO shares have returned 344%, beating the spectacular 230% return of the S&P 500 by a large margin – albeit with a ton of volatility!

My most up-to-date article on the inventory was written on January 3, once I went with the title “Valero’s A Dividend And Buyback Gem – If It Drops, I’m Buying.”

Since then, VLO shares have added 8%, together with dividends, outperforming the S&P 500 by roughly 200 foundation factors.

Now, it is time for an replace, as a LOT has occurred since then, together with the corporate’s 4Q23 earnings launch, new geopolitical developments, and excellent news for shareholder distributions.

So, as we’ve got loads to debate, let’s get proper to it!

The Refinery Area Continues To Be A Good Place To Be

Refinery operations are fascinating, as they contain so many variables.

For instance, refineries want to purchase oil to provide value-added merchandise like diesel and gasoline. This makes them depending on the value of crude oil and dependable feedstock.

As soon as this has been taken care of, refineries want to take care of their operations and ensure that they can produce effectively, permitting them to stay aggressive.

On prime of that, there are numerous components they can not affect, together with demand and (international) developments impacting provide, together with tariffs, provide chain disruptions, and investments in new refinery operations which will affect U.S. export demand.

With that stated, on February 12, it was reported that abroad circumstances stay extremely favorable as European diesel cracks rise to a 13-month excessive on tight provide.

Primarily, which means that margins for diesel manufacturing in Europe have improved. The crack unfold measures the distinction between enter prices and promoting costs of varied refined merchandise.

In line with the report (emphasis added):

[…] The upswing in margins was attributed to a mix of things, together with ongoing refinery upkeep and disruptions within the Pink Sea, resulting in tightened provides out there.

Through the afternoon buying and selling window, no diesel barges had been reported to have traded, regardless of a number of bids and affords being posted by merchants. The heightened refining margins mirrored the affect of decreased provide availability, with refinery upkeep season commencing in Europe and disruptions within the Pink Sea contributing to the tightening of diesel complicated provides.

Along with regional components, the worldwide distillate market skilled notable actions. U.S. distillate stockpiles, encompassing diesel and heating oil, demonstrated a big decline of three.2 million barrels within the previous week. The entire distillate stockpiles within the U.S. fell to 127.6 million barrels, surpassing market expectations for a extra modest 1 million-barrel drop. This surprising drawdown in distillate inventories within the U.S. contributed to the broader dynamics influencing diesel costs globally.

That is unbelievable information for U.S. refiners, as they profit from elevated costs abroad and subdued inventories at house – each of that are favorable for pricing and demand!

Reuters

Particularly in gentle of a possible demand rebound, costs may surge, providing fertile floor for earnings acceleration within the refinery {industry}.

Here is what Reuters wrote earlier this month in an article titled “Diesel prices primed to rise sharply in 2024.”

International shares of diesel and different center distillates are under regular and costs may begin to rise rapidly if the commercial economies of North America and Western Europe emerge from their lingering recession in 2024.

[…] However in Europe too there are indicators the worst of the downturn is now over and the sector will return to progress earlier than the tip of the 12 months.

Merchants anticipate each the U.S. Federal Reserve and the European Central Financial institution will minimize rates of interest this 12 months which might turbocharge the cyclical upswing.

In consequence, international distillate inventories are prone to stay under common and will simply tighten additional, intensifying the upward stress on costs

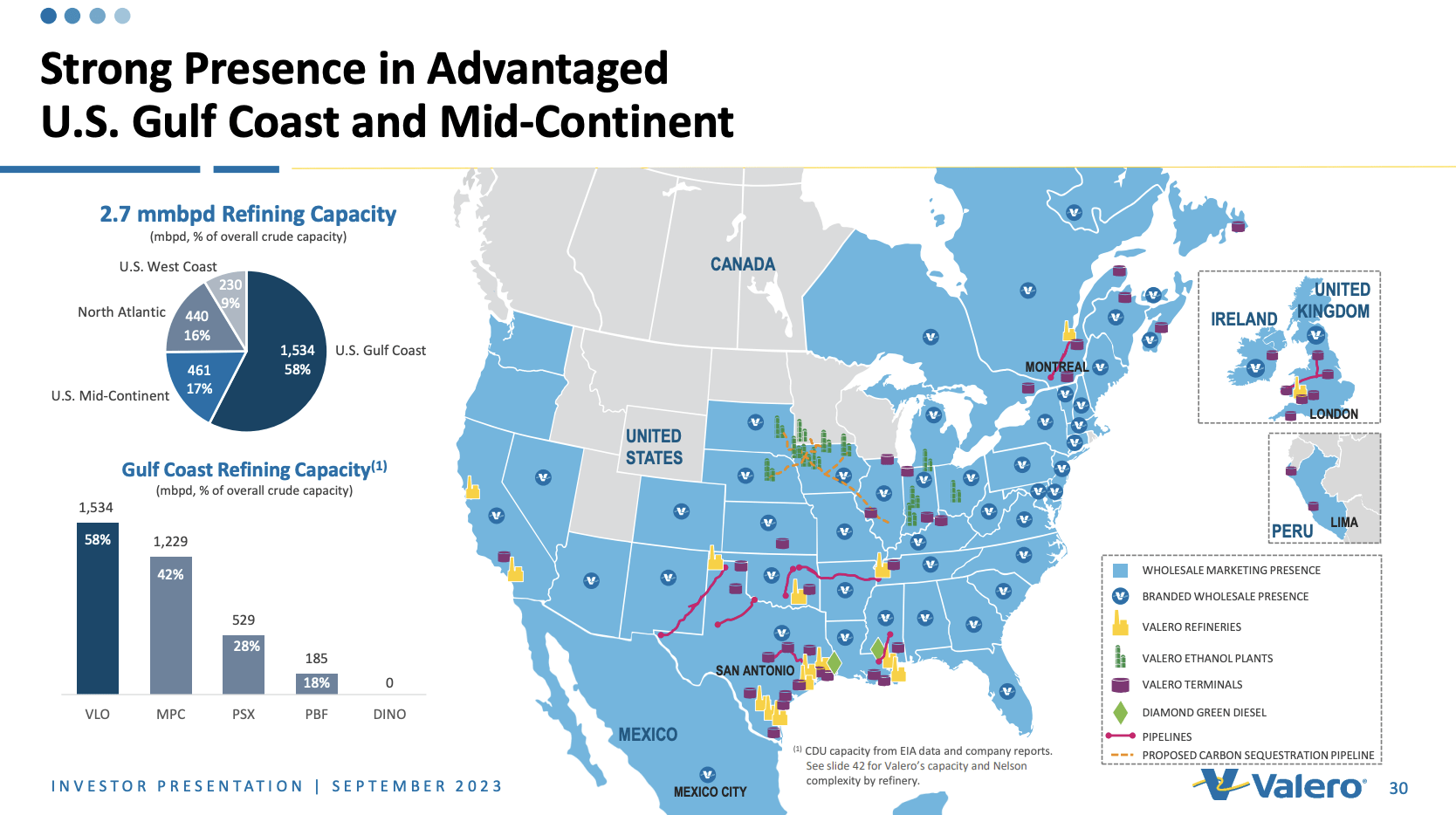

Additionally, keep in mind that Valero is in a unbelievable spot to fulfill excessive demand.

The corporate has shut to three million each day barrels of refining capability, most of it within the Gulf Coast. It additionally has operations in the UK and Eire and a unbelievable logistics community to facilitate exports.

Valero Power

We personal logistics property (crude oil pipelines, product pipelines, terminals, tanks, marine docks, truck rack bays, and different property) that assist our refining operations. Demand for transportation fuels in Latin America is anticipated to proceed to develop. To assist our wholesale rack operations in Latin America, we’ve got invested in or grown our entry to terminals and transloading amenities in Mexico and Peru. Our U.S. Gulf Coast refineries are nicely positioned to assist export progress to Latin America and different international locations world wide. – VLO 2022 10-K (emphasis added)

With that in thoughts, let’s take a better have a look at Valero.

Valero Continues To Impress And Ship Shareholder Worth

Based mostly on what we simply mentioned, enable me to throw some numbers at you as we dive into the corporate’s 4Q23 earnings.

Within the fourth quarter of 2023, Valero reported a web revenue attributable to stockholders of $1.2 billion, representing a lower from $3.1 billion in the identical interval of 2022.

This translated to earnings per share of $3.55 in comparison with $8.15 per share in 4Q22.

The excellent news is that adjusted earnings had been a lot stronger.

Aside from our 2022 outcomes, we delivered the very best fourth quarter and full 12 months adjusted earnings in firm’s historical past in 2023, demonstrating the earnings functionality of our portfolio. – VLO 4Q23 Earnings Call

On a full-year foundation, adjusted web revenue was $8.8 billion ($24.90 per share), in comparison with $11.6 billion, or $29.16 per share in 2022.

This decline was primarily on account of pricing headwinds, as 2022 was such a spectacular 12 months on account of unexpected components.

- The Refining phase reported $1.6 billion of working revenue through the quarter, a notable decline from $4.3 billion for the fourth quarter of 2022. Refining throughput volumes within the fourth quarter of 2023 averaged 3 million barrels per day with a utilization price of 94%. Nonetheless, refining money working bills exceeded steerage at $4.99 per barrel, primarily on account of an environmental regulatory reserve adjustment on the West Coast.

- The Renewable Diesel phase noticed a lower in working revenue to $84 million from $261 million within the fourth quarter of 2022, regardless of a rise in gross sales volumes to three.8 million gallons per day. This lower was attributed to decrease renewable diesel margins within the fourth quarter of 2023.

- The Ethanol phase reported a big improve in working revenue to $190 million from $7 million within the fourth quarter of 2022, pushed by greater manufacturing volumes and decrease corn costs.

What I discovered actually fascinating is that Valero’s operations proceed to shine.

Operationally, Valero’s refining system achieved a powerful mechanical availability price of 97.4% in 2023.

This achievement is especially noteworthy because it represents the corporate’s greatest efficiency thus far.

By way of gross sales volumes, Valero achieved a brand new annual file in 2023, with gross sales quantity reaching roughly 1 million barrels per day.

In line with the corporate, this milestone highlights the effectiveness of its branded and wholesale advertising and marketing community and underscores its means to capitalize on market alternatives to drive progress.

On prime of that, Valero continues to spend money on strategic tasks.

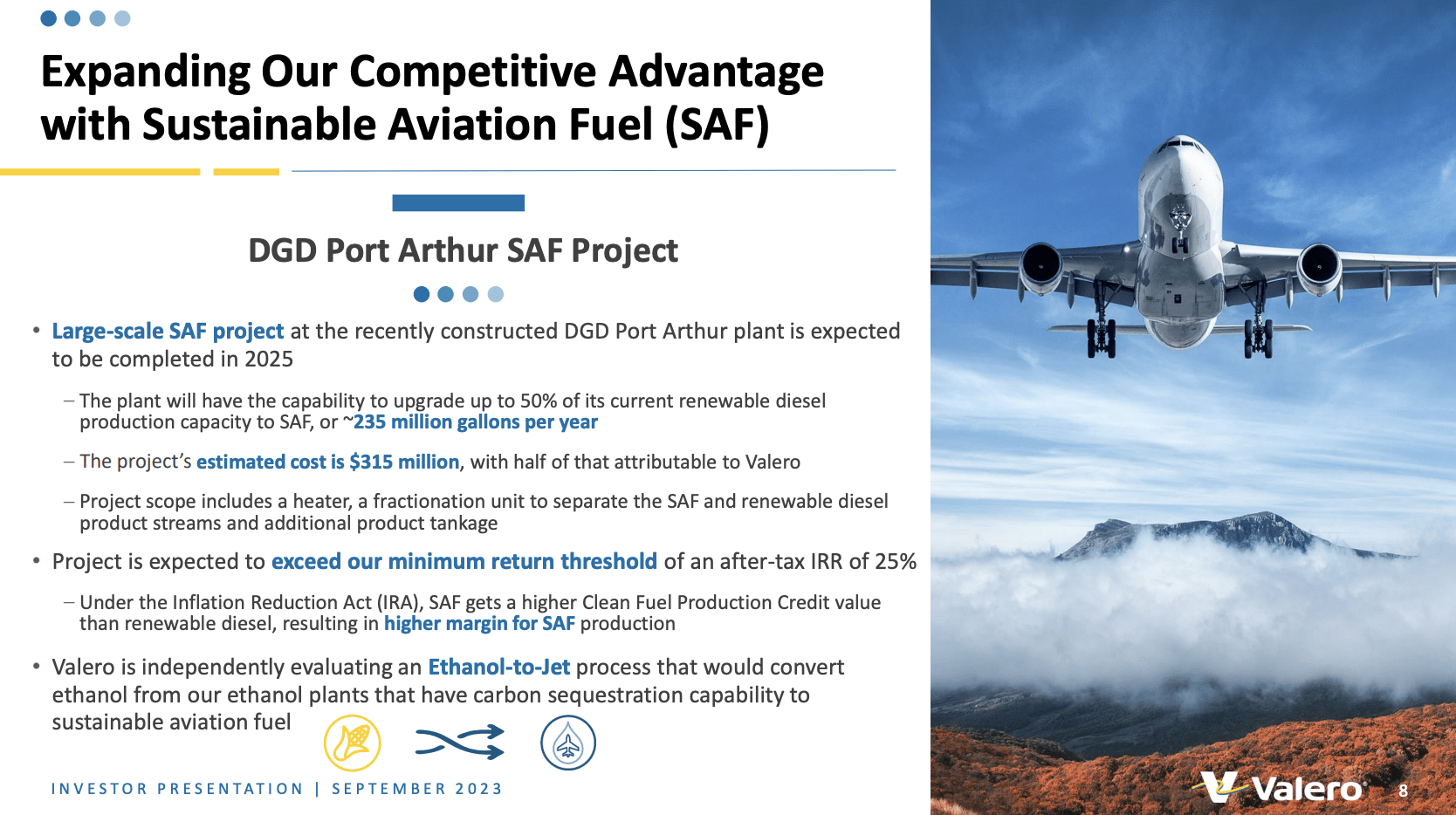

One notable mission is the DGD sustainable aviation gasoline (“SAF”) mission at Port Arthur, which is anticipated to be accomplished within the first quarter of 2025 at a complete price of $315 million.

As soon as operational, this mission is poised to place Valero as one of many largest SAF producers globally, additional diversifying its product portfolio and income streams.

Valero Power

This additionally bodes nicely for its buyers.

Financially, Valero stays dedicated to delivering worth to shareholders, which it has been doing for a really very long time. As I stated earlier than, through the pandemic, the corporate used its stability sheet to take care of its dividend.

Within the fourth quarter of 2023, the corporate returned 73% of adjusted web money offered by working actions to shareholders by dividends and share repurchases, leading to a 60% payout ratio for the total 12 months.

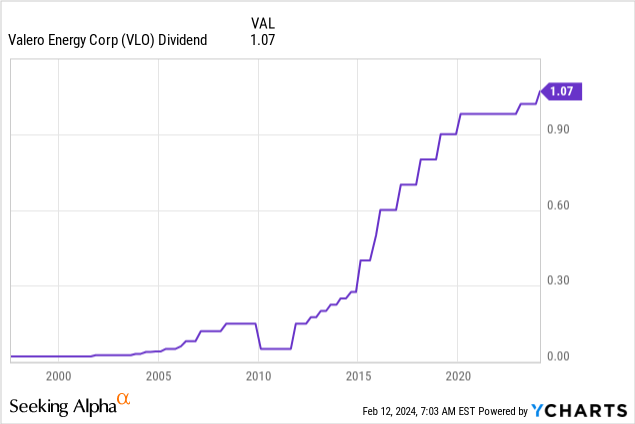

After climbing its dividend by 4.9% on January 19, the corporate at the moment pays $1.07 per share per quarter, which interprets to a yield of three.0%.

This dividend is protected by a 30% 2024E earnings payout ratio and the corporate’s BBB-rated stability sheet, which has a 2024E web leverage ratio of lower than 1x EBITDA.

In different phrases, though the corporate took an enormous threat through the use of its stability sheet for dividends through the pandemic, it was a wager that paid off, because it now has a top-tier stability sheet and a enterprise that helps aggressive dividend progress.

Furthermore, over the previous 5 years, the dividend has been hiked by 4.6% per 12 months, on common.

Whereas that quantity could also be a bit underwhelming, given huge EPS progress, there are two issues we’d like to bear in mind:

- It took some time for the corporate to restore its stability sheet after the pandemic. In 2019, the corporate had a 1.2x web leverage ratio. In 2020, that quantity rose to 11.3x EBITDA. It took till 2022 to decrease that ratio to lower than 1x EBITDA.

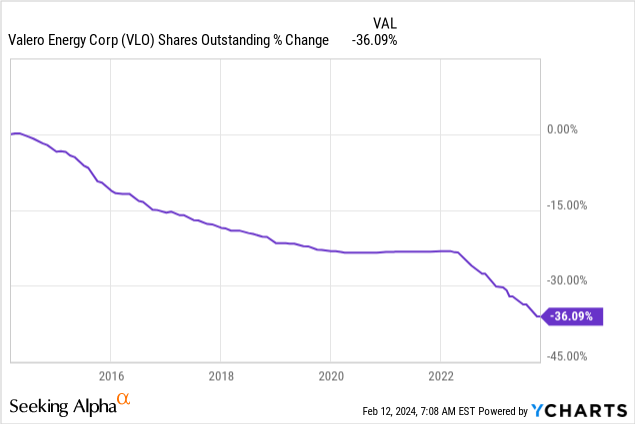

- The corporate has used money tailwinds after the pandemic to purchase again inventory, which is a way more versatile method to (not directly) distribute money to shareholders.

As we are able to see under, over the previous ten years, VLO has purchased again 36% of its shares, which has tremendously added to its favorable long-term inventory value efficiency.

The excellent news is that the corporate could be very proud of its payout ratio, particularly if 2024 is “more of a mid-cycle type year.”

That is what the corporate stated throughout its earnings call when it was requested about this (emphasis added):

John Royall [Analyst]

After which my second query is on return of capital. So your quantity for the quarter was very sturdy, and also you completed the 12 months at 60% of CFO. I do know you have talked about the way you have a tendency to come back in above the vary when cracks are sturdy. If ’24 finally ends up being sort of extra of a mid-cycle kind 12 months and even under, how ought to we take into consideration the place you would possibly fall in that 40% to 50% vary this 12 months?

Homer Bhullar [VP Investor Relations, Finance]

Sure, John, I imply our strategy to shareholder returns is pushed by our annual goal of 40% to 50% of adjusted web money from operations. And clearly, that features the dividend, which we take into account nondiscretionary and buybacks, that are thought-about the flywheel supplementing our dividend to hit our goal. And given the energy in our stability sheet within the fourth quarter, as we highlighted, we had a 73% payout which resulted in a 60% payout for the 12 months. And as you touched on, since 2014, we have recurrently paid above our goal. And in reality, the typical payout for the 5 years main into COVID was round 57%.

So I believe in brief and durations when the stability sheet is powerful as it’s now and sustaining CapEx, the dividend and strategic CapEx is roofed. You possibly can moderately consider our 40% to 50% goal as a flooring and anticipate any extra money to go in direction of buybacks.

In different phrases, we should always anticipate the dividend to stay a precedence, even when potential financial headwinds weaken working money circulation a bit – in any case, the corporate can simply dial again buybacks.

Talking of potential weak point, trying forward, the corporate appears to agree with the larger image we mentioned in the beginning of this text, because it expects refining margins to stay supported by tight product provide and demand dynamics.

Within the brief time period, product inventories are anticipated to be constrained on account of important industry-wide turnaround exercise, offering additional assist to refining margins.

Furthermore, Valero anticipates continued international demand progress outpacing product provide progress in the long run regardless of the emergence of recent refinery startups.

Valuation

That is the tough half for one main cause: analysts anticipate {industry} fundamentals to return again to “normal,” which means decrease margins and pricing headwinds.

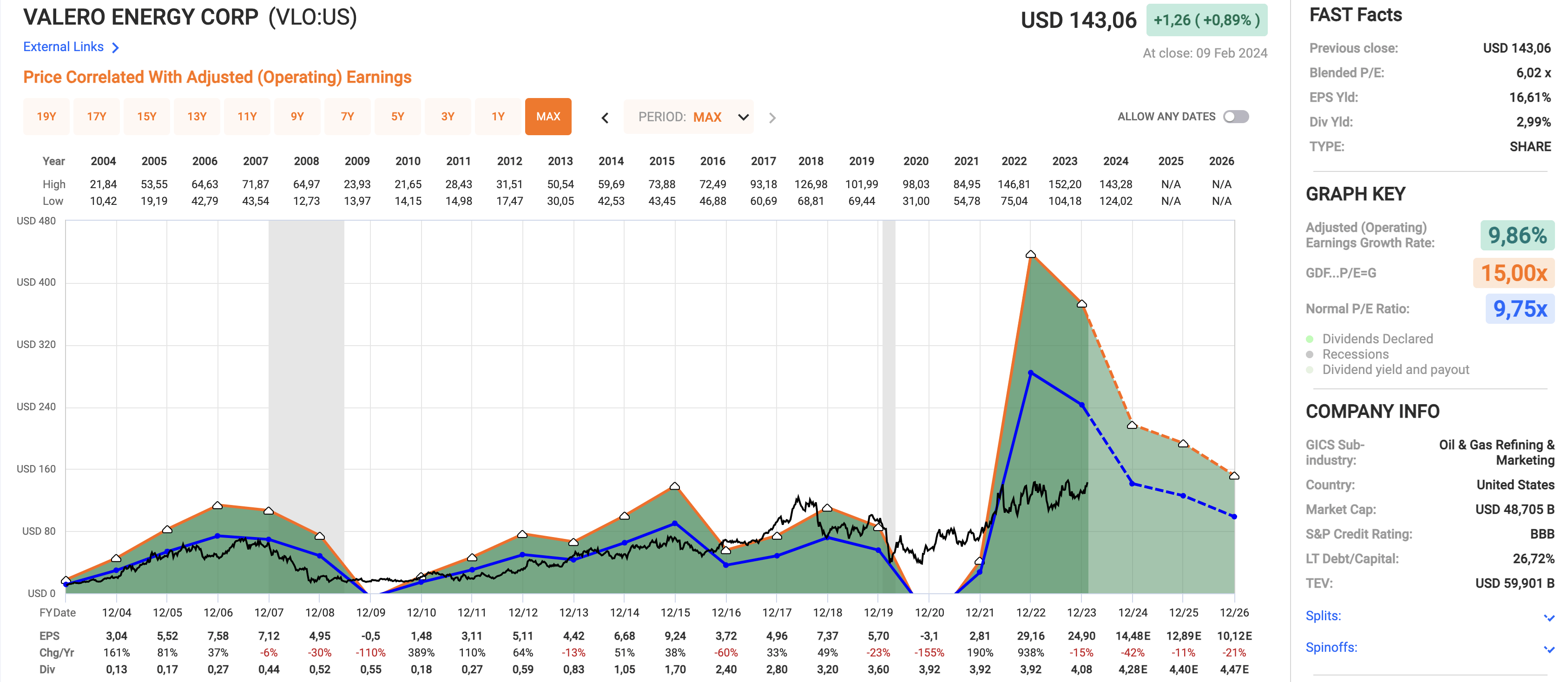

Utilizing the info within the chart under:

- Analysts anticipate 2024 EPS to say no by 42%, adopted by 11% contraction in 2025 and 21% contraction in 2026.

- VLO at the moment trades at a blended P/E ratio of simply 6.0x, which is method under its long-term normalized valuation a number of of 9.8x.

- If the corporate had been to return to a 9.8x a number of, it might have a good inventory value goal near its present value, primarily because of the steep anticipated EPS decline in 2024.

FAST Graphs

That is additionally mirrored in its goal value, which is at the moment $151, or 6% above its present value.

Personally, I don’t imagine that the corporate’s long-term outlook must be this bearish.

Certain, rising markets will construct extra refineries, and the conflict in Europe will not possible take without end.

Nonetheless, I imagine that analysts are method too bearish on Valero’s long-term earnings potential, which implies that any “unexpected” tailwinds may lead to steep goal value changes.

In consequence, I keep on with what I wrote in my prior article, which is that if the inventory corrects by 15-20% this 12 months, I am going to possible make it part of my dividend portfolio once more.

Takeaway

Whereas know-how shares have been within the highlight, the vitality sector, significantly refineries like Valero, has quietly outperformed.

Valero, with its strategic positioning and operational excellence, continues to impress buyers.

Regardless of short-term challenges and analysts’ conservative outlook, the corporate stays dedicated to delivering shareholder worth by dividends and buybacks.

As geopolitical components and market dynamics evolve, Valero’s resilience and potential for earnings progress make it an intriguing prospect for long-term buyers.

If the inventory experiences a big correction, it may current a compelling alternative for dividend-focused portfolios.

Therefore, in the meanwhile, I keep on with my Maintain score.

Professionals & Cons

Professionals:

- Resilience Amidst Volatility: Valero has demonstrated resilience, sustaining dividends even throughout difficult occasions just like the pandemic, reflecting its dedication to shareholder worth.

- Operational Excellence: With a mechanical availability price of 97.4% and file gross sales volumes, Valero’s refining operations proceed to shine.

- Strategic Investments: The corporate’s strategic tasks, just like the sustainable aviation gasoline mission, place it as a frontrunner in rising markets, diversifying its income streams.

- Shareholder-Targeted: Valero prioritizes shareholder returns, supported by constant dividend hikes and important share buybacks, backed by a powerful stability sheet.

Cons:

- Business Headwinds: Analysts anticipate {industry} fundamentals to normalize, probably resulting in decrease margins and pricing challenges, which may affect earnings within the brief time period.

- Geopolitical Dangers: Valero operates in a geopolitical panorama susceptible to disruptions, corresponding to conflicts in areas like Ukraine, which may have an effect on operations and profitability.

- Market Sentiment: Regardless of its long-term potential, market sentiment might fluctuate, resulting in volatility in Valero’s inventory value.