Dragon Claws

Written by Nick Ackerman, co-produced by Stanford Chemist.

Reaves Utility Earnings Belief (NYSE:UTG) stays a preferred closed-end fund with earnings buyers. It is one among solely a number of CEFs which have an inception previous to the worldwide monetary disaster that has additionally by no means diminished its distribution. Which means it has gone by the GFC and Covid with out vital harm. Being a fund that emphasizes utility publicity is definitely one of many key causes for any such outcomes.

Nonetheless, with greater rates of interest, UTG confronted a brand new risk. One which pressures utilities extra acutely, and given the borrowings employed by UTG, its funding earnings was additionally pressured. Some funds hedged towards greater charges, UTG wasn’t one among them and that definitely is a unfavourable mark on the administration workforce right here.

That mentioned, charges have been receding, with the 10-Yr Treasury Price coming off of its newest highs when it was pushing ~5%. With the Fed trying about completed with additional charge hikes, what was a headwind may flip right into a tailwind for the fund if charges recede additional. Because of this, I imagine that UTG stays a ‘Purchase,’ as I did charge it earlier this year.

I believe that UTG is among the set-and-forget kinds of CEFs that does not essentially must be traded round. Nonetheless, it might seem all different buyers additionally view this fund favorably and making an attempt to get this fund at a screaming discount is hard. The fund has barely traded at any significant low cost for an prolonged time period for a number of years now.

The Fundamentals

- 1-Yr Z-score: 0.13

- Premium: 0.42

- Distribution Yield: 8.71%

- Expense Ratio: 0.93%

- Leverage: 21.07%

- Managed Property: $2.467 billion

- Construction: Perpetual

UTG’s investment objective is “to provide a high level of after-tax total return consisting primarily of tax-advantaged dividend income and capital appreciation.” To attain this, the fund “intends to invest at least 80% of its total assets in dividend-paying common and preferred stocks and debt instruments of companies within the utility industry.”

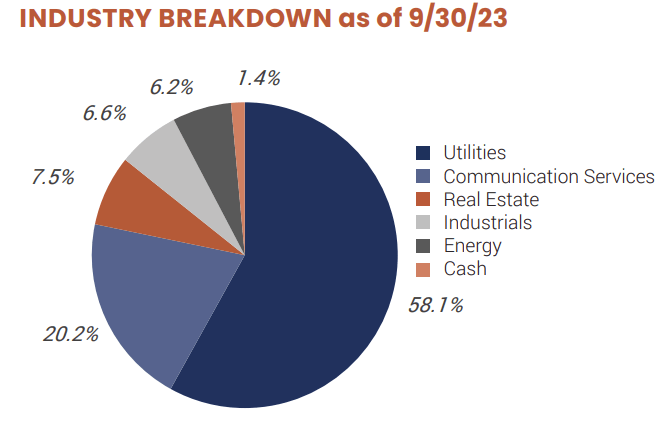

That leaves 20% exterior of the utility sector. Nonetheless, they’re pretty liberal with what they coin as “utility,” which may additionally embrace numerous holdings from the communication companies and actual property sectors as investments. Here is a take a look at the general sector breakdown as of their final fact sheet.

UTG Business Breakdown (Reaves)

In addition they depart it open for additional flexibility with investing throughout asset courses, however actually, they’re virtually fully invested in fairness securities.

The fund runs with leverage within the type of borrowings from a credit score facility. With greater rates of interest, that has seen their borrowing prices rise. Their expense ratio is pretty low for a CEF, however when together with the borrowing prices, the whole expense ratio comes as much as 2.17%. That was as of their last semi-annual report for the six months ended April 30, 2023. The Fed has bumped up charges greater since then, so we might anticipate that might have additionally elevated some since this final report.

Efficiency – Utilities Face Stress However Valuation Stays Tight

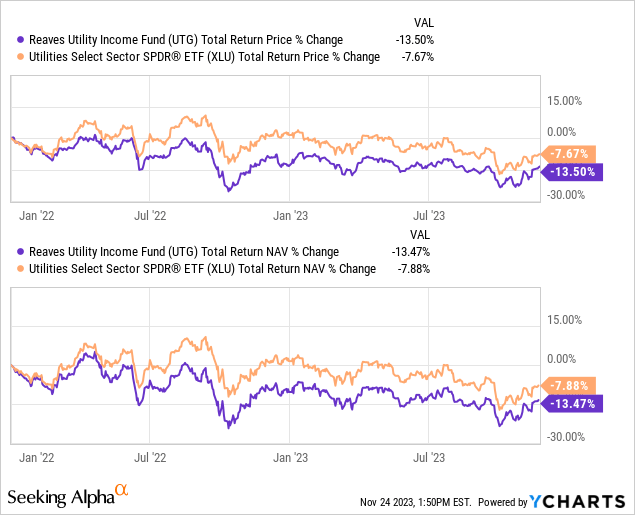

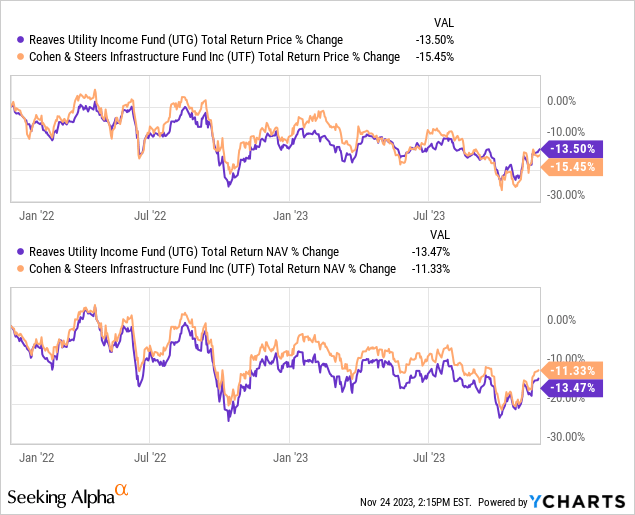

For the reason that Fed started growing rates of interest, utilities total have not carried out notably nicely. On this case, UTG has underperformed because the begin of 2022. As we are able to see under, although, it is not as if the Utilities Choose Sector SPDR (XLU) has had efficiency to boast about both throughout this time.

YCharts

UTG additionally carries some publicity to the communication companies sector, the extra conventional telecom corporations inside that area – not Meta Platforms (META) or Alphabet (GOOG) (GOOGL), which make up the biggest allocation of the Communication Companies Choose Sector SPDR (XLC). These two corporations make up virtually 49% of the ETF’s weighting, which has closely skewed the efficiency.

UTG has additionally had a sleeve of actual property publicity, which is one other space of the market that has been beneath stress as a consequence of greater charges. As quickly as we began to see these charges ease, we began to get a rebound in each the utility and REIT area. Given the outlook is for charges to come back down subsequent yr, there’s a good probability that Treasury Charges may face continued stress, and subsequently, UTG could possibly be trying to a discount at these costs.

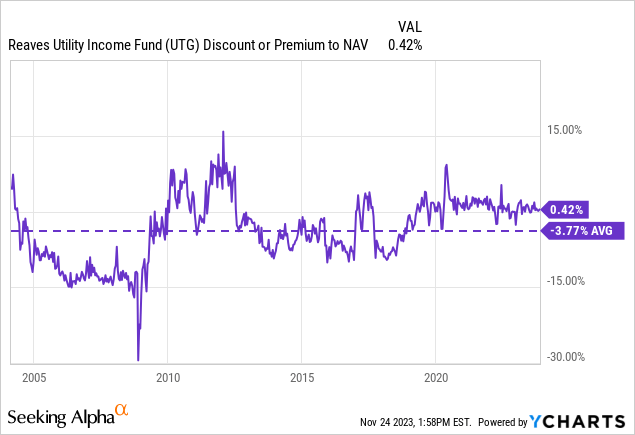

Alternatively, the unlucky half about UTG is that the fund’s premium has remained comparatively sticky. Even regardless of the pressures inside this area, buyers appear to proceed to be keen to drive the fund to commerce at parity with its NAV per share. That is fairly uncommon for a CEF, however actually, since going again to round Covid, buyers haven’t let UTG commerce too drastically far-off from its NAV per share.

YCharts

Nonetheless, as we are able to see above, that hasn’t at all times been the case. UTG was like most different CEFs in that it traded at reductions or premiums, and it generally diversified wildly. For that motive, whereas utilities seem like a discount and will have additional tailwinds driving them greater, UTG is not a screaming purchase till we see a wider low cost.

One fund that did hedge its leverage was its peer, Cohen & Steers Infrastructure Fund (UTF), which often will get talked about alongside UTG. That mentioned, whereas UTF did outperform UTG because the starting of 2022, it wasn’t by any landslide outperformance. UTF had been dealing with the identical kinds of pressures of upper charges impacting their underlying holdings, which additionally embrace some REIT investments and extra international publicity.

YCharts

UTF runs with greater leverage, and that was possible a contributing issue to seeing it carry out nearly as poorly as UTG throughout this time. They may be hedged, however when most of what you might be investing in is dealing with stress, and you might be investing in additional of it, losses will even be greater.

Distribution – Regular

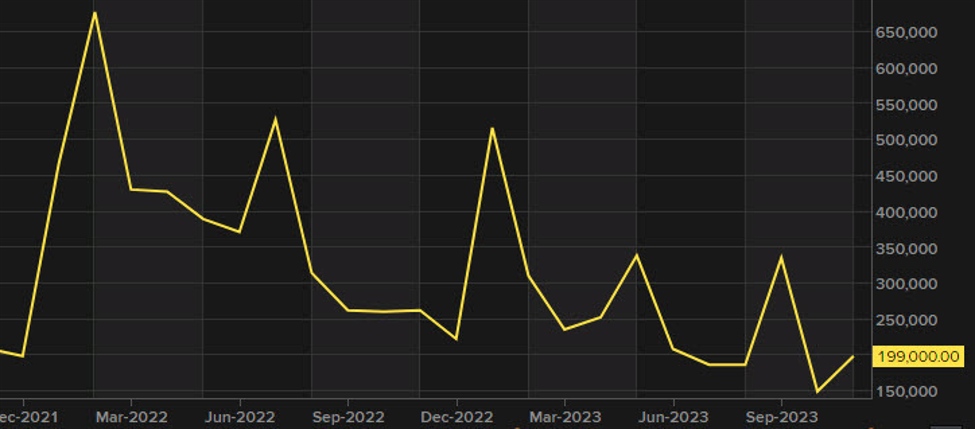

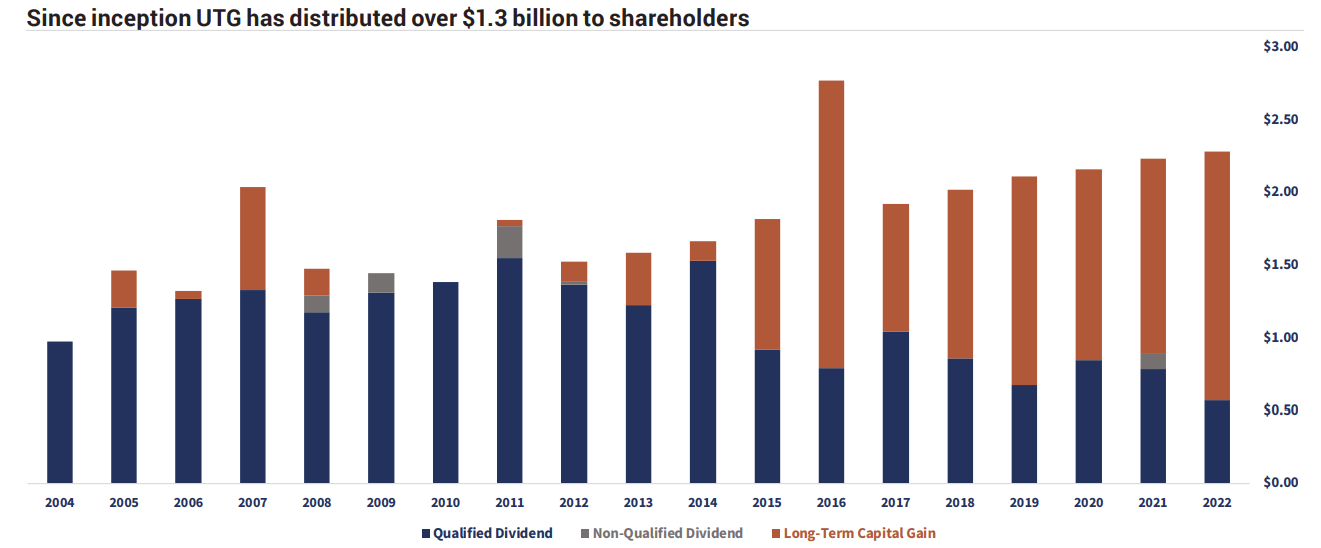

As famous on the open, UTG’s distribution has been extremely regular. Effectively, I suppose it might be much more acceptable to name it a gradual ascension, because the fund has elevated on various events since its launch.

UTG Annual Distribution Per Supply (Reaves)

The overwhelming majority of the distribution has been characterised as certified dividends or long-term capital beneficial properties. That may make it extremely tax-friendly if held in a taxable account.

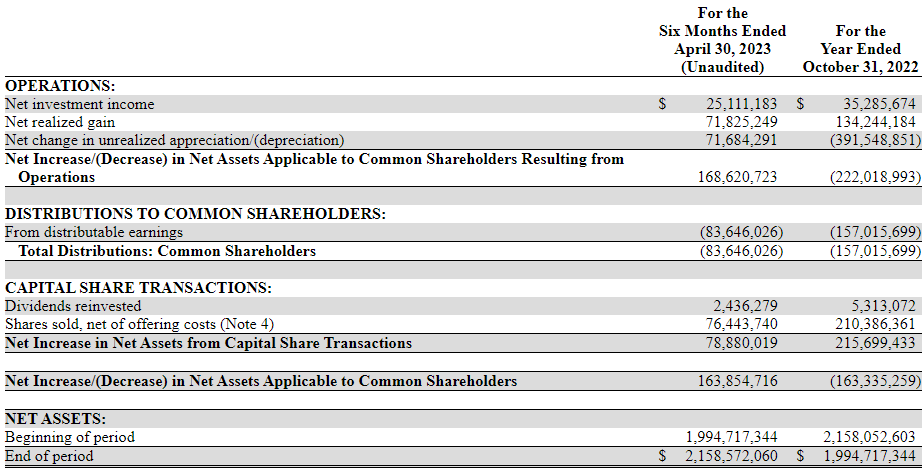

One factor that one would possibly level out is that they’ve been relying extra on capital beneficial properties over time, and that’s fairly true. Nonetheless, with the newest semi-annual report – regardless of the rising leverage prices – we have seen that NII is trying to rise. After all, these leverage prices meant that, comparatively talking the rise right here would have been lower than it in any other case can be, however seeing NII head greater remains to be encouraging.

UTG Semi-Annual Report (Reaves)

On a per-share foundation, NII for fiscal 2022 got here in at $0.51, and on this report, if it was annualized, it was on tempo for $0.68 NII per share. The fiscal year-end is definitely over, however CEFs have some actually large leeway for reporting up-to-date info. They have not traditionally launched their annual report till early January of the following calendar yr.

So we can’t get the precise quantity NII was for fiscal 2023 for a little bit of time but. Nonetheless, with the anticipation of potential beneficial properties returning with decrease charges and better NII, the distribution protection ought to be on the right track. Given the fund’s NAV charge of 8.75%, I do not suppose we’re at risk of seeing a distribution minimize both. I think that the administration workforce is aware of that that is the primary promoting level of UTG. Nothing is ever assured, however I might be keen to wager that they might be fairly hesitant to chop their payout. Not less than, I imagine it might take a considerably greater NAV charge with little probability of restoration. I do not imagine we’re in that scenario the place there is not some optimism going ahead, and at a sub-10% NAV charge, we aren’t at precarious ranges but.

UTG’s Portfolio

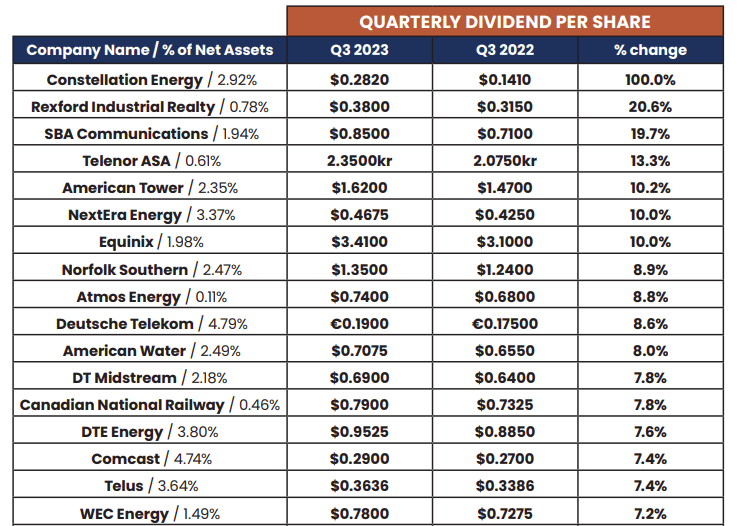

Moreover portfolio adjustments to extend NII for the fund, one factor they’ve additionally been specializing in extra lately this yr has been dividend will increase from their underlying holdings. They’ve now listed every holding for every quarter and what – if any – dividend enhance there was for every place. That they had a submit for Q2 2023, however the newest was for Q3 2023.

In that press launch, they famous 51 fairness positions, with 48 paying dividends through the quarter. In addition they famous that within the final 12-month interval, they noticed 43 elevated dividends and no reductions. Yr-over-year, the weighted common enhance was 7.9%.

Nonetheless, they did be aware that Constellation Vitality (CEG) noticed a very massive enhance of 100%. CEG was spun off from Exelon (EXC) in early 2022, leaving it with a comparatively quick historical past, however that may definitely present some confidence from the administration workforce going ahead. When factoring that out, the adjusted year-over-year enhance was 5.6%. Right here is the breakdown that they supplied of these corporations with the biggest will increase which are in UTG’s portfolio.

UTG Portfolio Dividend Will increase (Reaves)

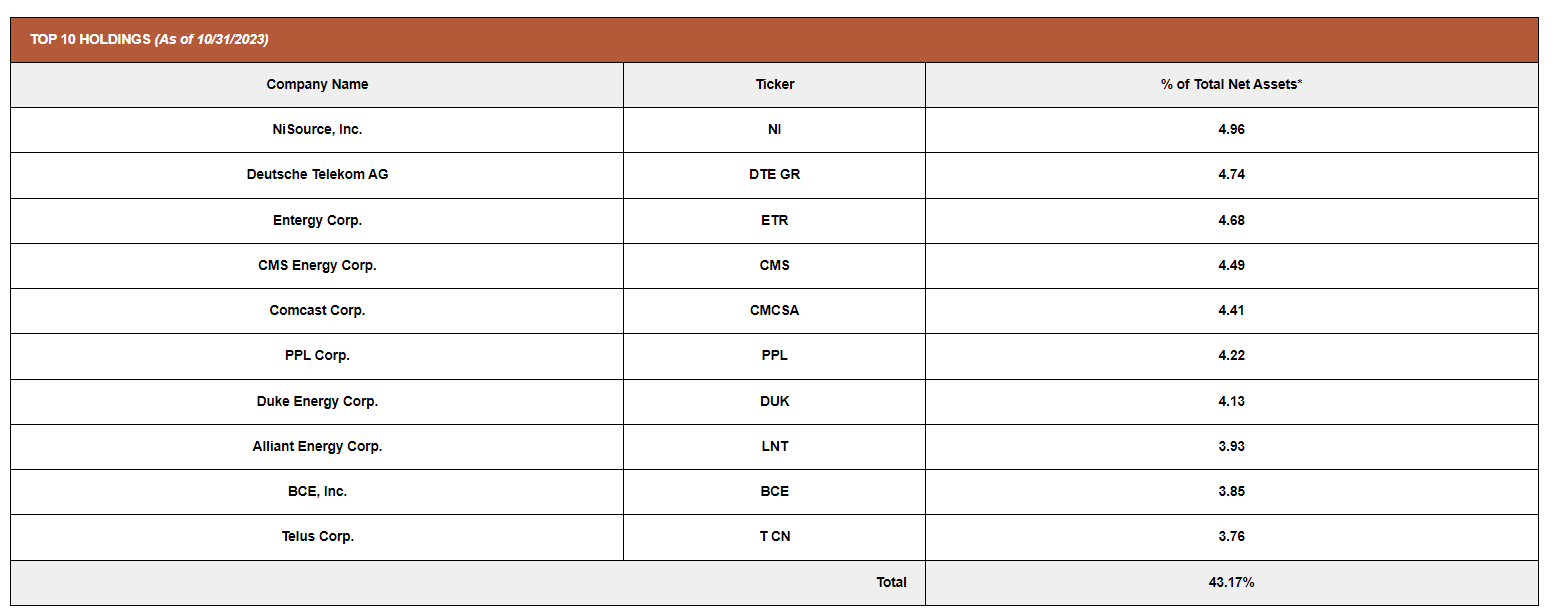

Total, UTG does not carry the biggest portfolio, as a substitute concentrating extra on fewer names. Their high ten holdings accounted for simply over 43% of the fund’s weighting. That positively places it on the extra concentrated aspect, and that was much like how the fund was positioned last year, with the highest ten at the moment making up 43.60%.

UTG Prime Ten Holdings (Reaves)

The portfolio turnover additionally is not that top right here, which tends to imply that the highest holdings usually keep high holdings for prolonged durations of time. That mentioned, the fund’s largest holding belongs to NiSource (NI), which wasn’t positioned within the high ten final yr. Moreover, Deutsche Telekom (OTCQX:DTEGY) is available in because the second largest place. That was additionally a brand new identify to the highest ten.

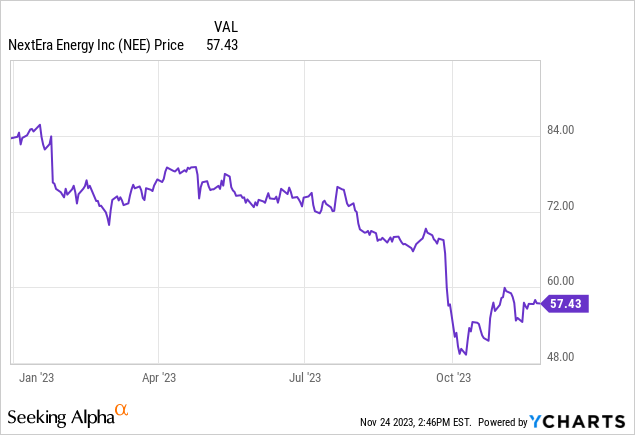

A noteworthy identify to fall off the highest ten record was NextEra Vitality (NEE). NEE is a extremely in style utility firm that has been within the high place in most utility and infrastructure funds. Nonetheless, after a tumble a few months in the past, that has seen its dominance begin to slide. NEE is also the biggest place in XLU, at a weighting of ~13%, that means that NEE remains to be a considerable a part of the general utility sector.

YCharts

On this case, UTG’s full holding list nonetheless reveals that NEE is a holding, but it surely has slipped slightly meaningfully. NEE went from 4.58% weight to three.37% weighting.

Conclusion

Utilities aren’t going away, and neither is UTG, at the same time as they face this new greater rate of interest surroundings. UTG is a stable utility fund that has been in a position to ship a steadily rising distribution to buyers. The final a number of years have been more durable for the fund. That mentioned, these greater rates of interest that had been a headwind may flip right into a tailwind. Whereas I imagine that UTG is price investing in, I am additionally cognizant of the truth that it is not a screaming purchase. The buying and selling close to parity with its NAV does not justify that degree of enthusiasm. Due to this fact, implementing a dollar-cost common method to build up a place on this one would in all probability be extra acceptable.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.