SergeyZavalnyuk

Funding thesis: Betting on Vale S.A. (NYSE:VALE) won’t make a lot sense if one is anticipating a kind of stagnated world economic system or worse in 2024. There’s a distinct chance that at occasions its inventory value will see a major decline from present ranges. I see such a attainable decline in its value as a chance to purchase and maintain for a longer-term wager. If there’s a decline in world iron demand, it is not going to final, as a result of a worldwide financial slowdown might be counteracted by fiscal stimulus measures, together with infrastructure initiatives that are usually a classical go-to authorities coverage for such events. Infrastructure initiatives want metal as an enter, which can in all probability imply that a rise in world iron ore demand will precede an total world financial restoration. My present technique is to keep up my present place in Vale inventory, whereas I intend to deal with any retreat in its value larger than 20% from present ranges as a window of alternative so as to add to my present place.

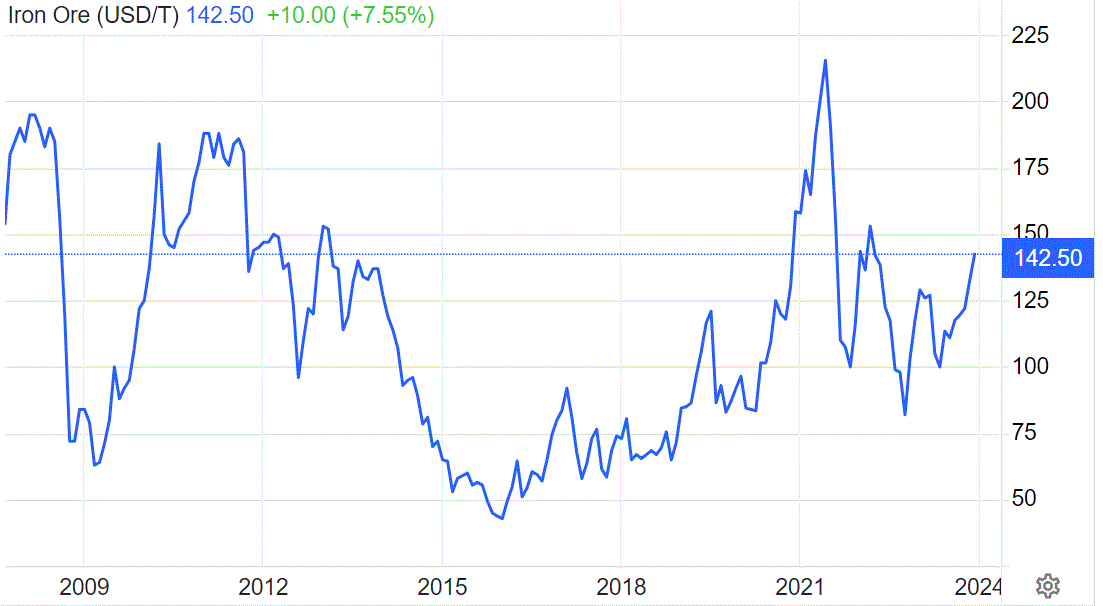

Q3 outcomes had been respectable, whereas This autumn may doubtlessly be even higher on larger iron ore costs.

For the third quarter of the 12 months, Vale noticed a rise in revenues from just below $10 billion in Q2, 2022, to $10.62 billion. Greater revenues didn’t translate into larger internet earnings, as they declined from $4.46 billion in Q2, 2022, to $2.84 billion for the newest quarter. Sure bills had been larger, with some which can be of observe from my viewpoint, together with larger gross curiosity bills of $192 million for the quarter, which quantities to 1.8% of revenues. This is a vital information level from my perspective as a result of I comply with the curiosity expense to revenues ratio as crucial measure of an organization’s monetary well being. I have a tendency to fret when curiosity prices cross above 5%, whereas something within the 10% vary I see as being outright harmful to an organization’s survival prospects.

It must be famous that once we are speaking of measurements comparable to curiosity prices/income ratios, it comes inside the context of an organization that relies upon an ideal deal on risky uncooked materials market costs in relation to revenues, earnings, and so forth, thus this measure can fluctuate an ideal deal.

Buying and selling Economics

Iron ore costs had been considerably decrease in Q3 of this 12 months in contrast with This autumn, subsequently we are able to assume that the curiosity/income ratio, in addition to different measures, will see an enchancment within the newest out there quarterly outcomes when This autumn outcomes are available.

Fears of attainable iron demand weak spot on account of a possible world financial slowdown make sense till we remind ourselves that financial slowdowns are often countered by stimulative authorities spending, typically centered on infrastructure initiatives.

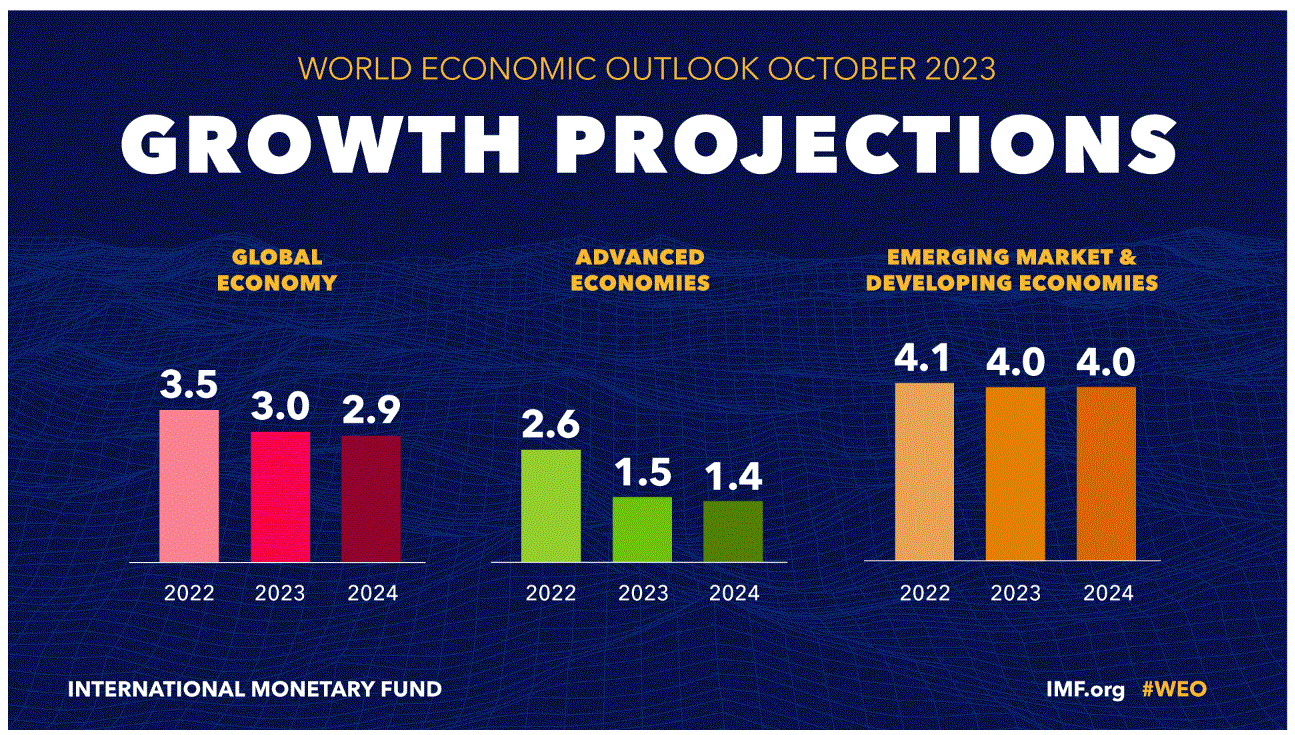

Main establishments such because the IMF are sounding the alarm on a worldwide economic system that already noticed lower than splendid development in 2023 slowing down even additional.

IMF

The IMF at the moment initiatives solely a slight slowdown in world financial development for 2024 in contrast with 2023. In my opinion, there may be much more draw back danger to its present forecast than there may be potential for upside surprises.

The prospect of a worldwide financial slowdown might seem to be a foul time to spend money on iron ore mining firms at first look. An financial slowdown may counterintuitively spark a spike in demand, as governments are inclined to react to financial slowdowns with stimulus measures, which regularly embody infrastructure initiatives. In different phrases, much less metal could also be wanted within the manufacturing of shopper items, however it might be greater than compensated by an increase in infrastructure wants.

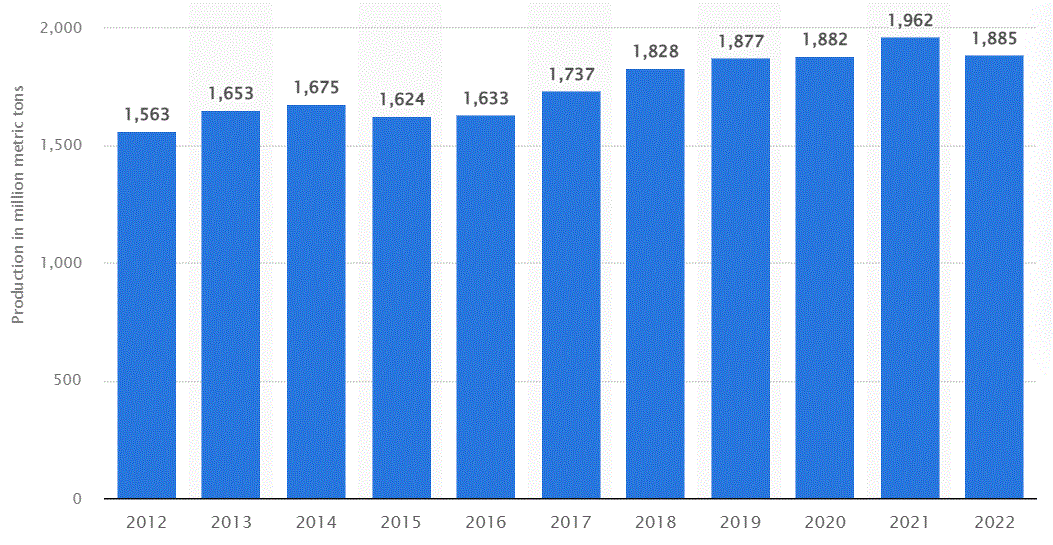

International metal manufacturing (Statista)

As we are able to see from the chart, world metal manufacturing didn’t decline in 2020 from 2019 ranges, regardless of the deep financial slowdown, after which it elevated considerably in 2021, which for my part is a mirrored image of worldwide efforts to maintain the economic system going, together with by infrastructure initiatives, which are inclined to require vital volumes of metal.

I ought to observe that one attainable obstacle to a replay of the previous world responses to financial slowdowns could also be an absence of fiscal room for a rising variety of main economies. The US debt/GDP ratio is at over 120% at the moment, and deficits are approaching $2 Trillion. China appears to even have its troubles, together with some overbuilding within the residential sector which might make it much less prone to see a increase in metal demand. On the general public infrastructure aspect, nonetheless, it appears decided to maintain constructing, at the least for now. The EU, Japan, and the UK are all shrinking when it comes to global economic relevance and are unlikely to interact in large-scale infrastructure initiatives. The one vivid spot could be a group of growing nations, led by India, the place infrastructure is sorely wanted and at the least some governments have sufficient fiscal room to interact in infrastructure initiatives to stimulate their economies.

Funding implications:

Iron ore costs might expertise a number of months of weak spot in 2024, as an preliminary response to what can doubtlessly be a weaker world economic system than present institutional forecasts might recommend. Vale’s inventory value may even see an outsized decline, as traders will probably promote your entire mining sector in response to an financial slowdown. I at the moment have a comparatively modest place in Vale inventory, of about 1.5% of my inventory portfolio and I intend to carry on to it, though I imagine that there’s a respectable likelihood of a short-term decline in its inventory value this 12 months. If there is no such thing as a decline, I’ll probably proceed to trip out my present place and I might be content material to proceed gathering on the beneficiant dividend of 5%, whereas I await a good inventory value to begin lowering my place. If the inventory value sees a decline of 20% or extra from present ranges, I intend to begin shopping for.

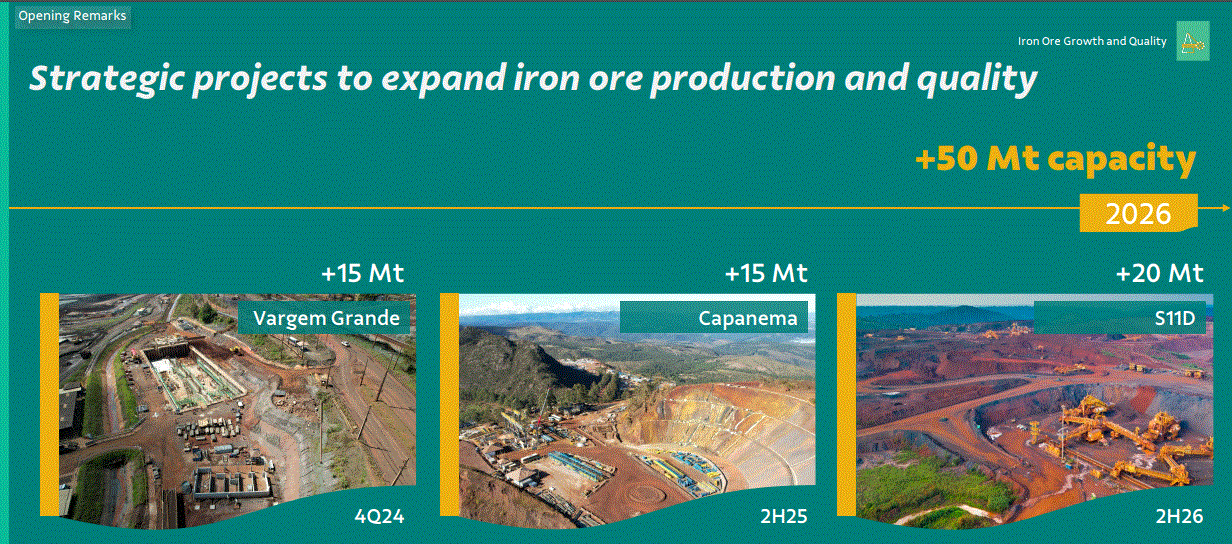

The argument in favor of shopping for Vale inventory rests on the potential exterior elements I specified by the article, in addition to inside elements that might doubtlessly play properly inside the context of an assumed improve in world iron ore demand within the shorter time period, in addition to for the long term. As an illustration, Vale is ready to extend manufacturing by an estimated 50 Mt/12 months between now and 2026.

Vale

The rise in manufacturing represents about 19% in contrast with Vale’s present iron ore manufacturing ranges.

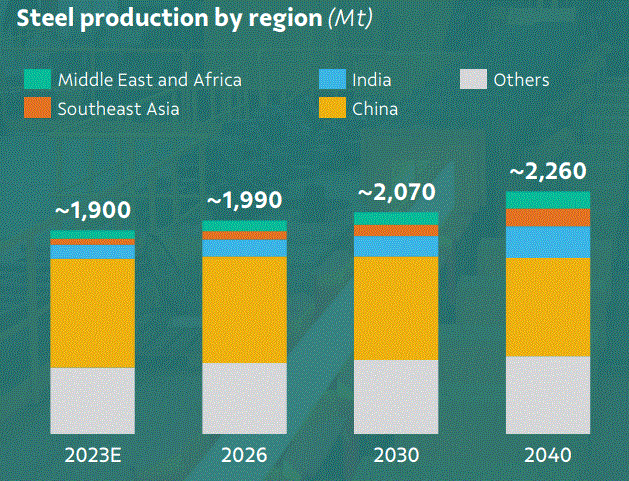

Vale’s deliberate improve in manufacturing is kind of in keeping with estimated provide and potential demand development for a similar interval, on condition that recent forecasts put world provide development at 2.7% per 12 months for this era.

It stays to be seen whether or not or not the business is gearing as much as ramp up manufacturing by greater than what the world wants, as demand development will not be essentially going to materialize at the same tempo, wherein case, it may set off a collapse in iron ore costs within the subsequent few years. It must be famous that Vale has a extra subdued forecast for world metal manufacturing development of nearly 5% by 2026 from the estimated 2023 ranges.

Vale

There’s a doubtlessly extra bearish end result for Vale and all different iron ore miners, and that will be a possible sustained upward shift in world vitality costs. Greater vitality costs would probably result in an extra decline in world financial actions, which might create downward strain on iron ore costs and on the identical time, it could push manufacturing prices up. Greater inflation in most main economies would additionally make it much less seemingly that governments could have fiscal room to interact in infrastructure spending as a solution to restart financial development as a result of larger inflation tends to maintain borrowing prices excessive.

Whereas Vale’s inside fundamentals are strong, with a low debt servicing burden, and an honest revenue margin, which means that its present dividend is protected, the potential exterior dangers are vital sufficient to warrant warning when investing on this inventory. Threat administration is why I intend to think about including to my already current place, provided that a extra favorable shopping for alternative arises within the coming months.

I’m in search of a pullback of about 20% earlier than I determine so as to add extra Vale inventory, which could or won’t occur within the brief time period. In case Vale’s inventory value goes in the wrong way, I’m trying to begin promoting as soon as it approaches $20/share, from the present value stage of below $16/share. For the reason that begin of this decade, I modified my method to managing my portfolio, to replicate my total view that as we speak’s market carries much more danger than what the market is at the moment pricing in. If these had been bizarre occasions, a mining firm with a 5% dividend, a ahead P/E ratio of seven.5, and a strong monetary efficiency when it comes to sustaining a low debt-servicing burden as a proportion of its revenues would appear like a protected long-term wager. Sadly, we’re not residing by bizarre occasions and I’m adjusting my method to investing accordingly.