photovs

Good Pedigree, However Spin-Offs Have A Doubtful Observe Report

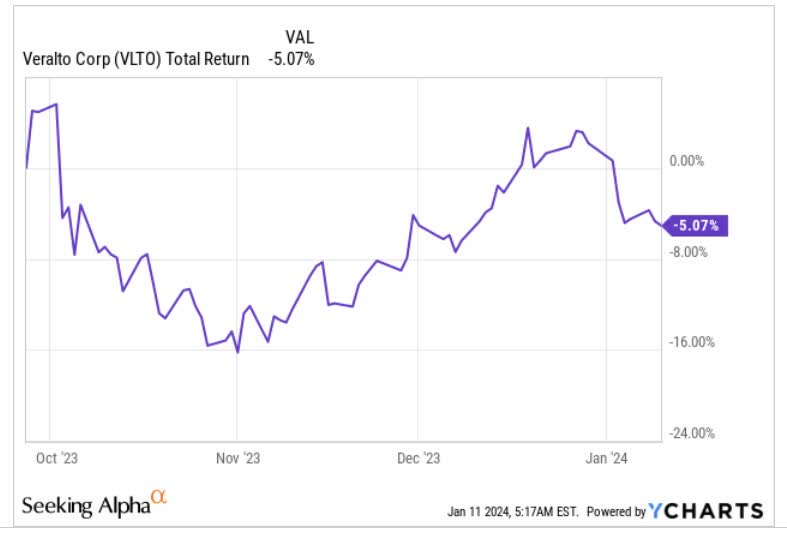

Veralto Company (NYSE:VLTO), which beforehand was part of the famed life sciences and diagnostics innovator – Danaher Company (DHR), got here into inception as a standalone entity in the beginning of This autumn final yr when it was spun-off. Notice that because it made its debut in the marketplace, VLTO hasn’t made any cash for its shareholders and is down by mid-single digits during the last three months.

YCharts

Granted, VLTO comes from a superb heritage, and the well-established system and practices of Danaher ought to maintain them in good stead as a standalone play, however research have proven that spin-offs sometimes do not add an excessive amount of worth to the events concerned.

For context, a study carried out by HBR entailing 350 massive spinoffs during the last twenty years confirmed that common returns post-separation, for the mixed market cap of the 2 entities was solely round mid-single-digits even after two years.

Spectacular Recurring Income Profile and Asset-Gentle Mannequin Interprets To Helpful FCF Era

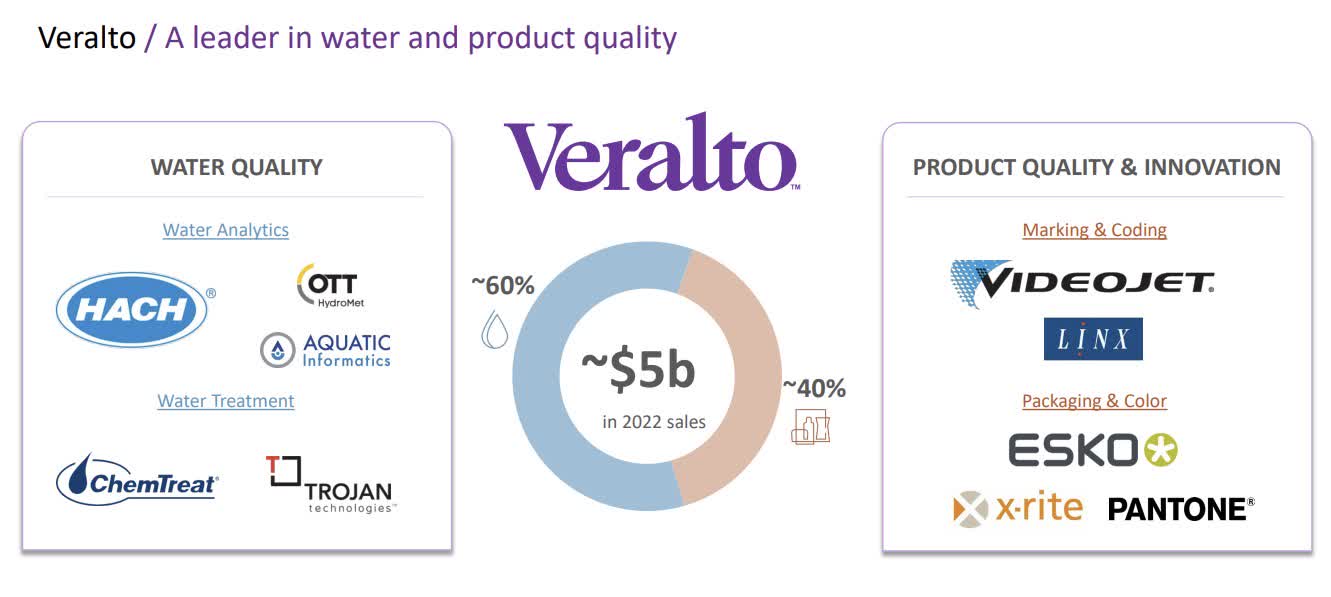

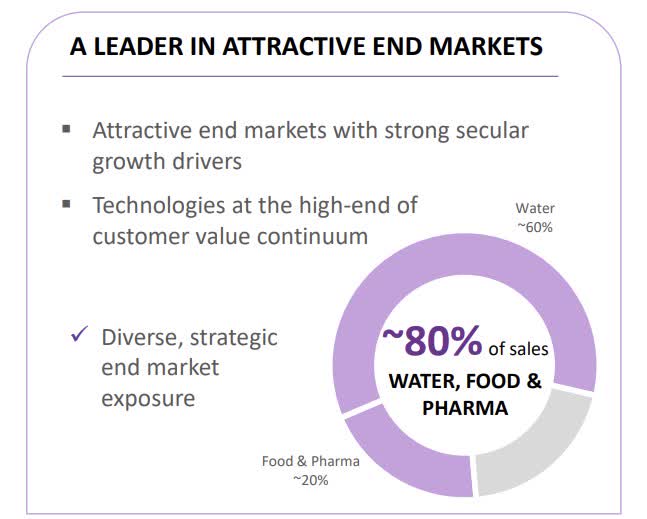

VLTO primarily includes Danaher’s previous environmental and utilized options (EAS) section. Merchandise listed here are primarily utilized to research, deal with, and handle water utilized in industrial, residential, and business purposes (60% of the enterprise). The remainder of the enterprise comes from the sale of varied devices, software program, providers, and consumables to the buyer, pharma, and industrial markets.

Analyst Day Presentation

One of many standout qualities of Veralto is that it has a wholesome stream of recurring income that accounts for 57% of its income base. This recurring income side is a mirrored image of how pivotal a few of VLTO’s choices are to its purchasers. As an apart, while that recurring income proportion is spectacular in its personal proper, do notice that the erstwhile Environmental & Utilized Options section of Danaher (which is what VLTO covers now) nonetheless had the bottom share of recurring income in comparison with Danaher’s different segments – Biotech (82%), Diagnostics (88%), and Lifesciences (62%).

Moreover the regular income stream, the relative reliability of the VLTO working mannequin additionally comes by by means of the markets it’s predominantly uncovered to. A large 80% of its topline comes from regular reliable finish markets reminiscent of water, meals, and prescription drugs.

Analyst Day Presentation

While the underlying texture of VLTO’s topline brings a level of reliability to this story, it additionally interprets to persistently positive working money move (OCF). That is additionally an asset-light enterprise, with CAPEX accounting for lower than 1% of gross sales, so inevitably the OCF protection of the CAPEX is kind of enormous (for the primary three quarters of 2023 the OCF coated the CAPEX by 22x) and interprets to glorious FCF. Between FY20 and FY22 the corporate transformed over 100% of its internet earnings to FCF, however final yr that improved even additional with the Q3 conversion coming in at 113%!

Do not Anticipate Beneficiant Distribution Development In Gentle of Vital Gearing

Regardless that VLTO has barely had any time as a public firm, we have already seen it take the initiative to distribute quarterly dividends of $0.09 per share, which will probably be paid on the finish of this month. That determine is definitely not Earth-shattering and solely interprets to a minuscule yield of 0.47%. Given the low base, some dividend-chasing buyers is likely to be hoping for some beneficiant distribution progress subsequent yr, however we might search to minimize these hopes in gentle of the elevated ranges of debt that exists on VLTO’s steadiness sheet

As per the most recent information Veralto had round $2.6bn value of debt, which as a perform of its working earnings interprets to a hefty gross leverage stage of two.27x. From one other lens, you are additionally looking at a remarkably excessive debt-to-equity ratio of 262%! For perspective, the typical debt to fairness for shares within the environmental providers universe is so much decrease at solely 88%.

Thus despite the fact that the VLTO working mannequin continues to generate wholesome doses of FCF (on a trailing twelve-month foundation, we’re taking a look at roughly $1bn of FCF), a big chunk of that will probably be required to handle the debt (which overshadows the FCF by 2.6x) and likewise gasoline VLTO’s inorganic ambitions. This can be a enterprise with ample urge for food for M&A (within the analyst day PPT they’ve spoken about their want for strategic acquisitions which will probably be pricier than your normal bolt-on M&A) and it’s mirrored within the goodwill on the books which already accounts for an enormous 48% of the entire asset base.

Monetary Outlook And Ahead Valuations

During the last couple of fiscals, VLTO has delivered wholesome core gross sales progress of 8%, however it seems that the tempo of progress is now on a declining pattern and will keep that method for some time.

In Q3, core gross sales solely grew by 1%, and administration implied that This autumn could possibly be worse with both a flattish efficiency or low-single-digit declines.

So long as the Chinese language market continues to be a drag (it was down by the high-teens in Q3), it could possibly be tough for VLTO to flourish. Moreover, the PQI section (significantly in North America) can be dealing with its personal set of challenges with subdued demand for packaging {hardware} and shade tools. Individually, weak spot within the client packaging items markets may additionally proceed to weigh closely on marking and coding-related income.

All in all, if one appears to be like at consensus income estimates for the present yr, it isn’t as if VLTO is about to dazzle with anticipated progress of solely 3%. The anticipated backside line progress for FY24 is fairly unremarkable at solely 5%. That quantity is a patch on the typical ahead EPS progress of 17.5% that different environmental-based shares are poised to ship.

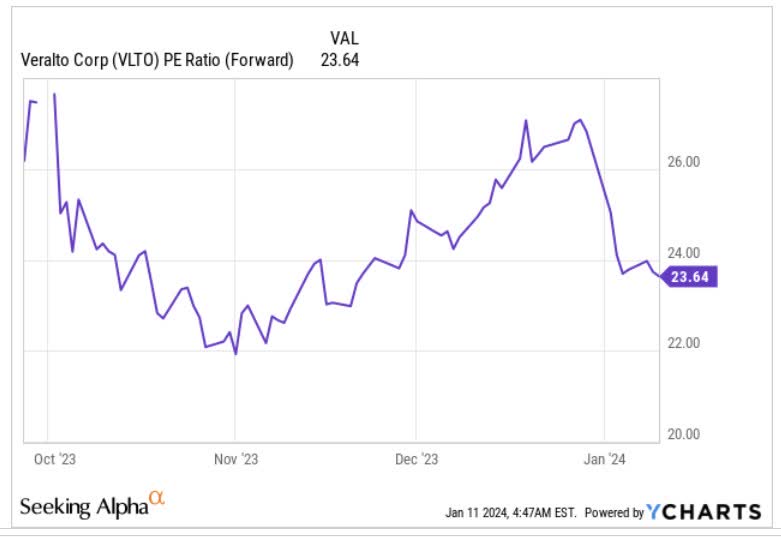

YCharts

In gentle of such a weak earnings trajectory, we do not suppose it makes an excessive amount of sense to purchase with a ahead P/E of 23.6, as that interprets to fairly a hefty PEG (Worth to earnings progress) ratio of 4.7x.

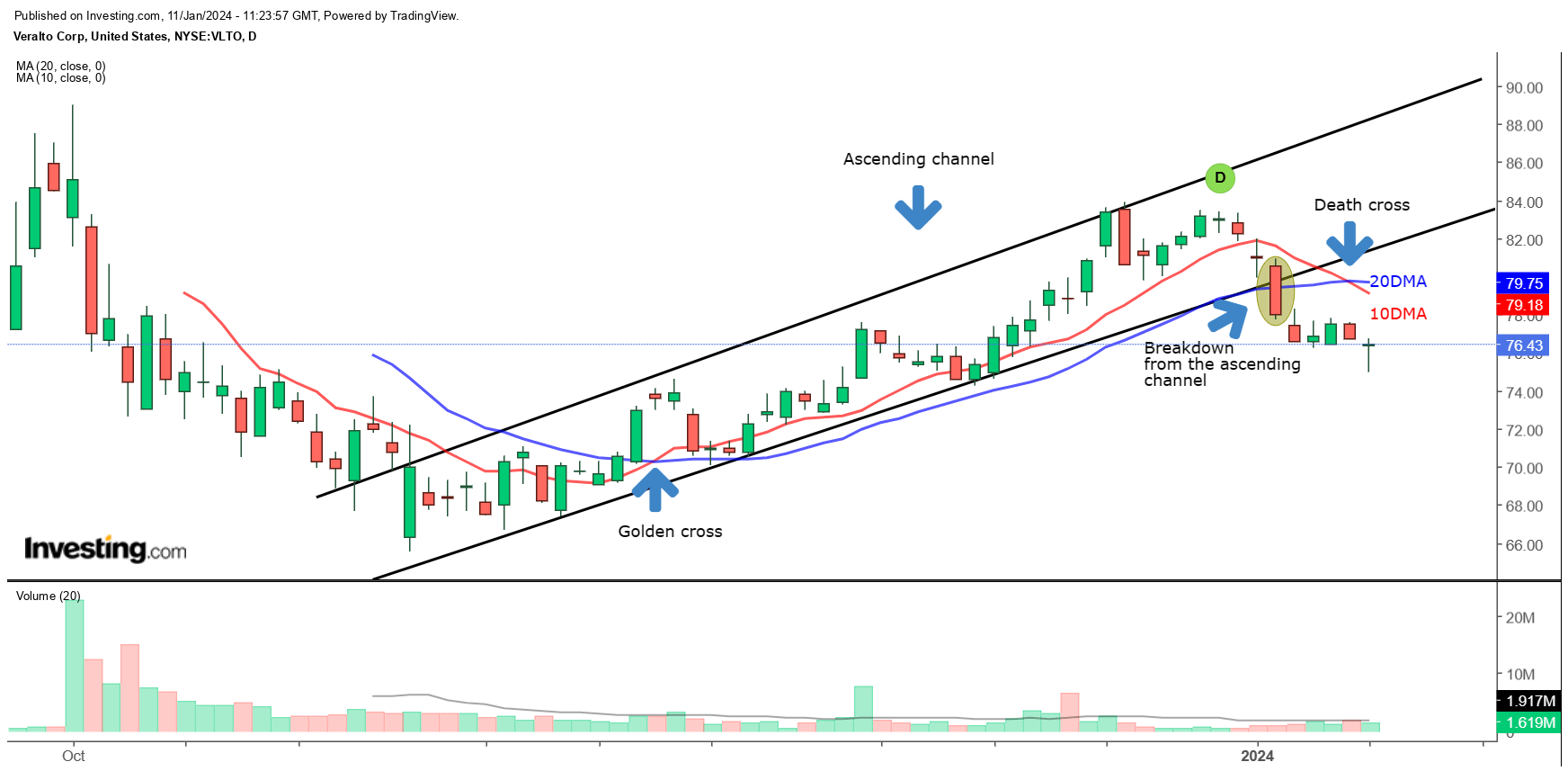

Closing Ideas – Technical Concerns

Current developments on the charts additionally counsel that VLTO wouldn’t make an incredible purchase at this stage.

The chart beneath measures how VLTO is positioned relative to its friends from the environmental providers universe. During the last three months, we have seen the ratio make a peak and a trough, setting the boundaries for a buying and selling vary. As issues stand, the ratio is now so much nearer to the mid-point of the buying and selling vary and is unlikely to learn from ample rotational curiosity (fairly not like the scenario in mid-November).

StockCharts

Individually, if we take a look at VLTO’s standalone worth imprints on the every day charts, notice that after forming a small base in late October/early November, we noticed the inventory pattern up within the form of an ascending channel. We additionally witnessed the Golden Cross set off by mid-November, which might have introduced just a few bulls to this counter.

From then till 2024 VLTO had trended properly throughout the ascending channel, till we noticed a large-bodied pink candle breakdown from the channel final week. Since then VLTO has did not recoup the channel, and we have additionally seen the death cross with the 10DMA dropping properly beneath the 20DMA which does not bode properly for somebody contemplating an extended place now.

Investing