Matteo Colombo

Introduction

I like biotech companies, as many come with wide-moat business models that allow for consistent dividend growth, buybacks, and capital gains.

These wide-moat characteristics often rely on the patents owned by these biotech giants.

- The average patent duration is 20 years, which often provides companies with the ability to exploit a certain market niche with very limited competition.

- Developing new drugs is very expensive. According to the NIH, the mean costs of developing a new drug are somewhere between the low-$300 million and high-$2 billion range. This makes it very hard for entrants to compete without having the financial resources and expertise.

Drug companies tend to benefit from intangible assets, a source of economic moat, in the form of intellectual property, but may also reap the rewards from investment in innovation. Not only do many of these companies benefit from long-term patents on existing drugs, their research and development efforts to release new drugs can help offset margin pressures on existing drugs when patents expire and generic versions enter the market. – VanEck

The problem is that once these patents expire, moat advantages quickly disappear. Hence, once you lose exclusivity, your niche is fair game for everyone.

Earlier this year, The Healthcare Technology Report wrote that the top 20 biopharma companies collectively face a $180 billion revenue patent cliff through 2028!

One example mentioned in the article is Humira, the blockbuster drug from AbbVie Inc. (ABBV), which is a company I own. After losing its patent, sales dropped by 35%, which was partially offset by strategic pricing and rebates.

Luckily, but not unexpectedly, AbbVie quickly recovered from this shock, as it has a strong existing product base and a promising pipeline.

That’s where Vertex Pharmaceuticals Incorporated (NASDAQ:VRTX) comes in, a $122 billion market cap giant I started covering last year.

My most recent article was written on February 28, when I went with the title “Vertex: One Of My All-Time Favorite Biotech Stocks Has More Room To Run.”

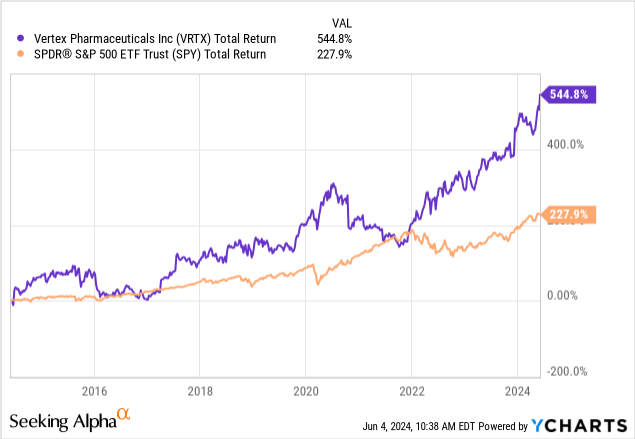

Since then, shares have added another 10%, beating the S&P 500 by roughly six points.

This brings the ten-year performance to 545%, more than 300 points above the S&P 500’s impressive return.

In this article, I’ll revisit my thesis and explain what to make of the risk/reward after this non-dividend-paying stock added another $20 billion to its market cap.

So, let’s get to it!

Innovation-Driven Growth

Vertex is a complicated company, as it is working on a number of impressive drugs with the potential to fuel elevated growth for many years to come.

For starters, the company has established itself as a leader in treatments for cystic fibrosis (“CF”), pain management, and other areas.

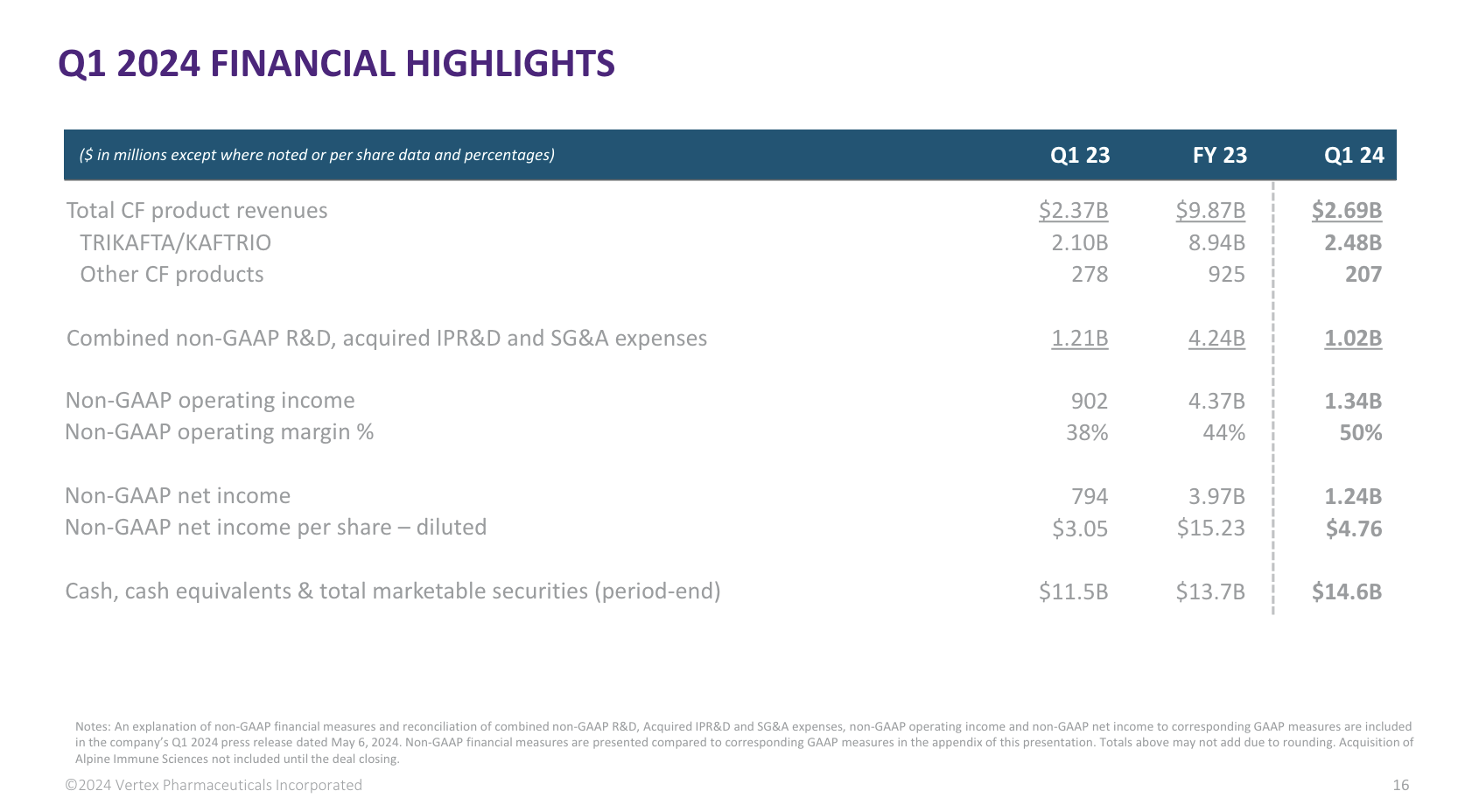

In the first quarter, the company delivered $2.69 billion in revenues, which represents roughly 14% growth compared to last year’s $2.37 billion in Q1 revenues.

Vertex Pharmaceuticals

Furthermore, the company’s late-stage pipeline is full of promising drugs that could make a big difference in many people’s lives.

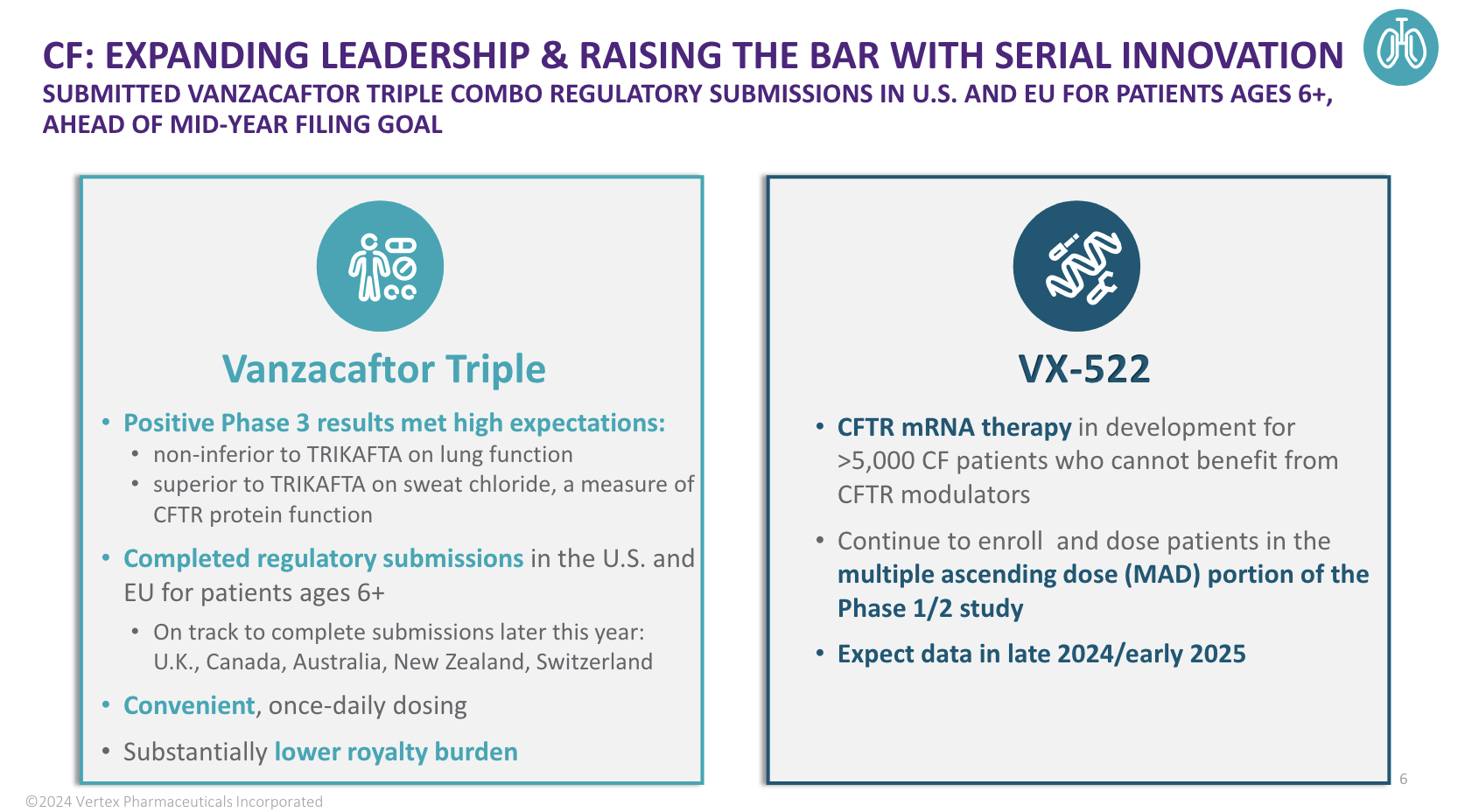

For example, according to the company, Vanzacaftor is an expected game-changer for cystic fibrosis patients.

So far, early data indicates the drug’s ability to significantly improve lung function and sweat chloride levels, potentially setting a new standard in CF treatment.

This was confirmed in a February press release from the company (emphasis added):

Head-to-head against TRIKAFTA, on the first key secondary endpoint, the vanza triple was superior in reducing SwCl levels in SKYLINE 102 and SKYLINE 103. In the second and third key secondary endpoints, which were pooled across SKYLINE 102 and SKYLINE 103, the vanza triple achieved superiority in the proportion of patients below 60 mmol/L (the diagnostic threshold for CF) and below 30 mmol/L (carrier level) compared to TRIKAFTA. – Vertex

Vertex Pharmaceuticals

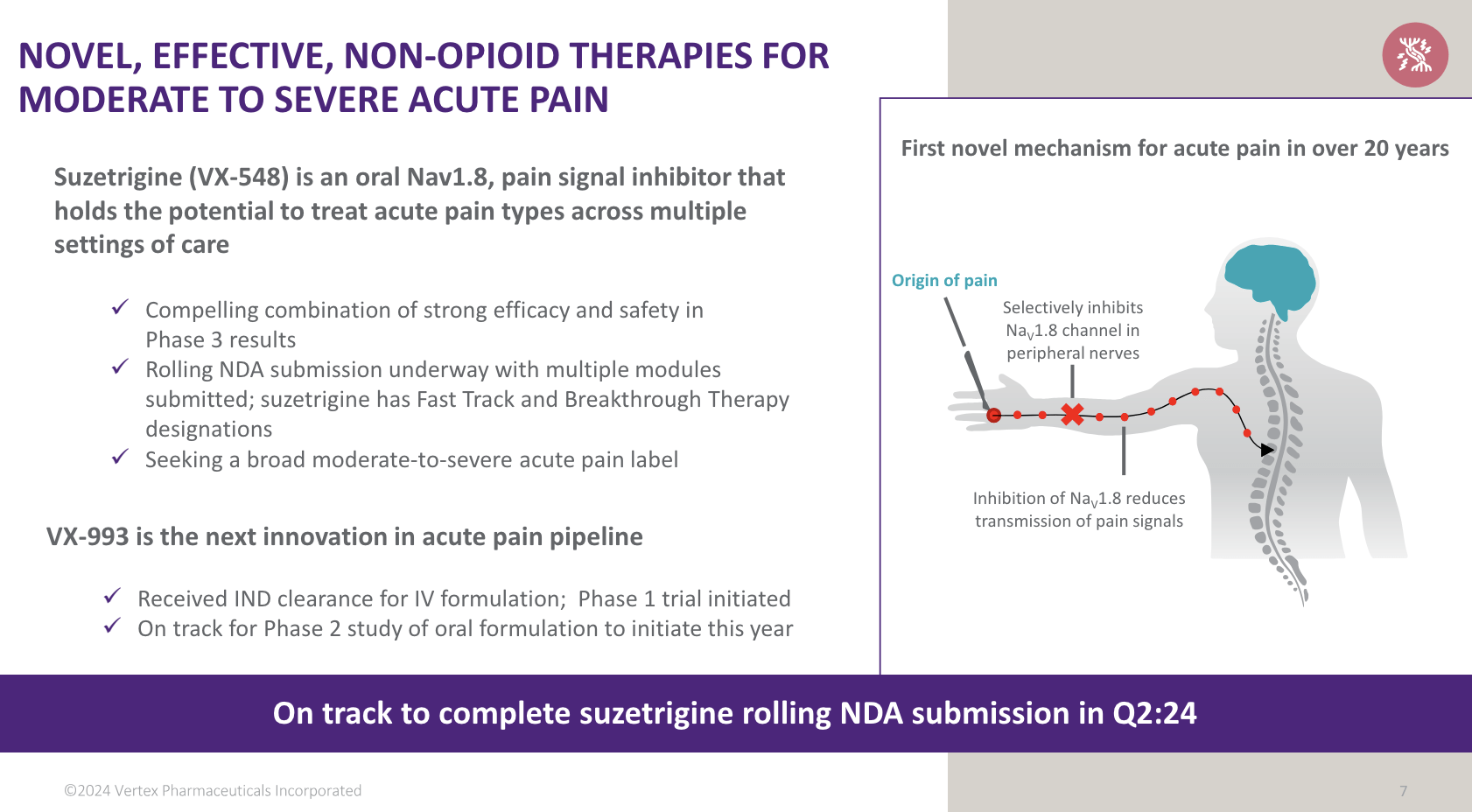

Moreover, Suzetrigine, which is a pain management drug, and Inaxaplin, a kidney disease drug, are in late-stage development, with the potential to significantly influence what are still unmet medical needs.

To me, Suzetrigine is fascinating, as it is a non-opioid painkiller.

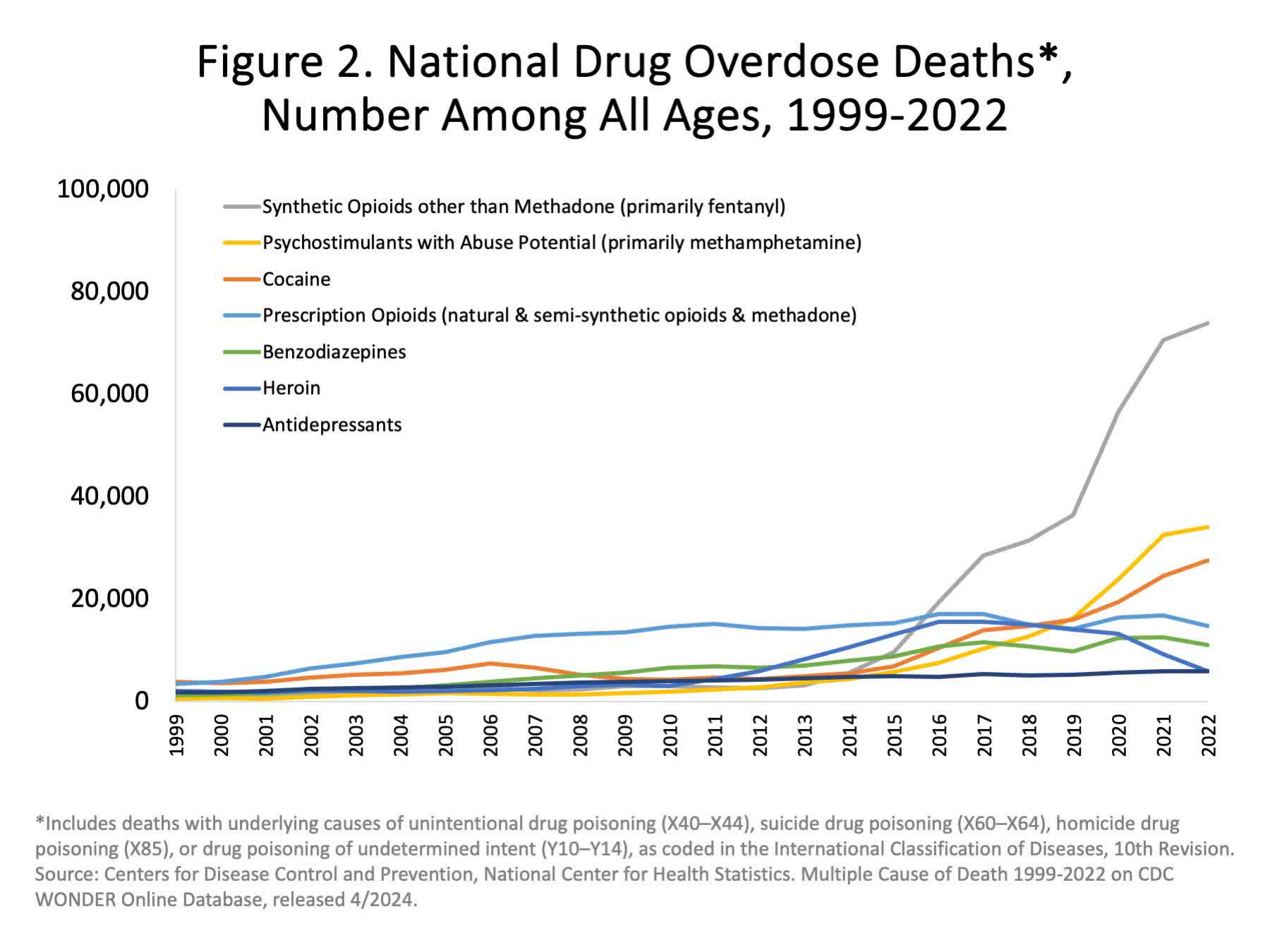

As some will know, prescription opioids have become a silent killer, costing more lives than heroin in recent years (data through 2022 – released in April 2024).

NIDA

According to Vertex, this drug offers a combination of efficacy and safety, which puts it in a great spot to be used across a wide range of conditions, from moderate to severe pain.

So far, data is extremely promising:

Both trials met the primary endpoints, and suzetrigine demonstrated a favourable safety profile with no serious adverse events reported. Vertex has started the rolling submission process and aims to finish by Q2 2024.

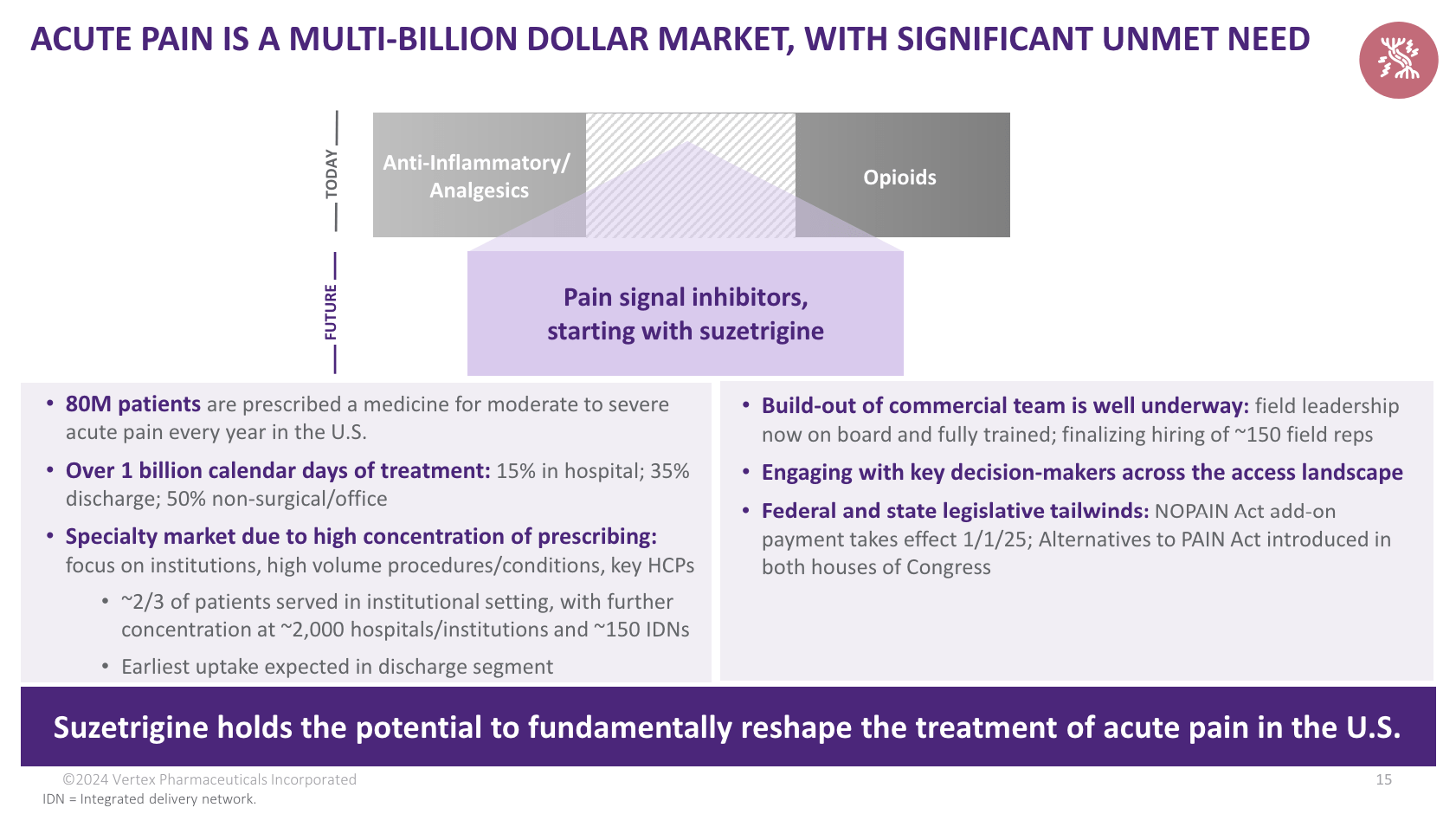

Once released, Vertex aims for a launch focused on institutions, as these account for roughly 50% of acute pain prescriptions.

I believe this drug could significantly limit opioid addiction in the United States.

Recall this discharge segment represents roughly 35% of the approximately 1.1 billion calendar days of acute pain treatment in the U.S. each year. The average prescription length in this setting is approximately 2 weeks. Treatment in this setting commonly includes opioids, where prescription length is shorter, 4 to 5 days, due to side effect profile, addiction concerns and prescribing limits at the state and IDN and hospital level. – VRTX 1Q24 Earnings Call

Vertex Pharmaceuticals

Even better, given the qualities of this drug and the massive market, it has the potential to become a blockbuster drug with a massive positive impact on the quality of many lives, as 80 million patients are prescribed medicine for pain in the United States – every single year.

This includes one billion calendar days of treatment – 85% of these outside of a hospital setting.

Vertex Pharmaceuticals

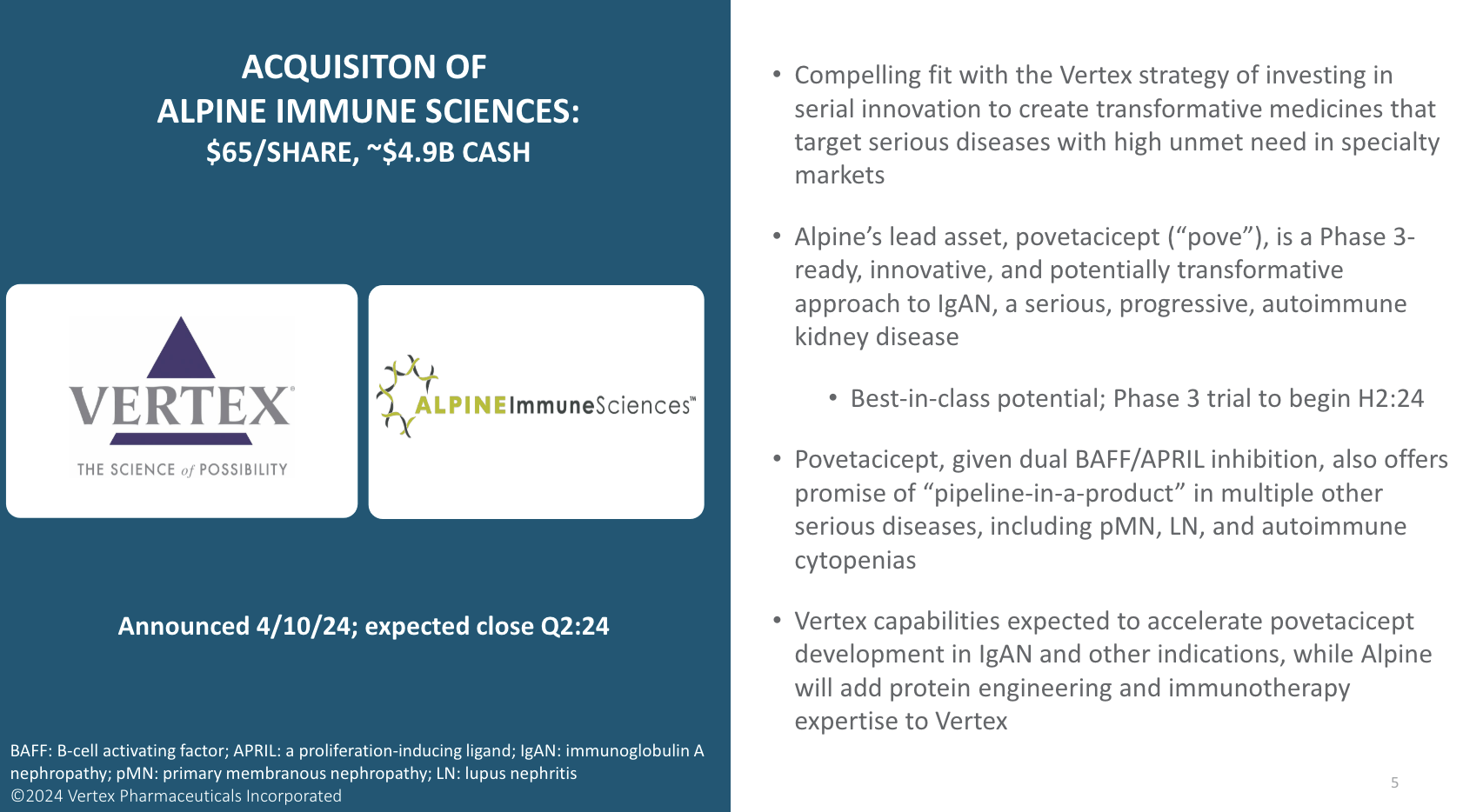

Beyond CF and pain, the company is also expanding into kidney health.

On April 10, the company announced the acquisition of Alpine Immune Sciences for $4.9 billion in cash.

The deal gives Vertex the rights to Povetacicept, which is a mid-stage development drug that treats IgA Nephropathy.

Povetacicept works by targeting types of proteins called BAFF and APRIL, which together contribute to the development of multiple autoimmune and antibody diseases.

IgAN, which occurs when clumps of antibodies are deposited in the kidneys, affects about 130,000 people in the United States, according to the companies. – Reuters

Vertex Pharmaceuticals

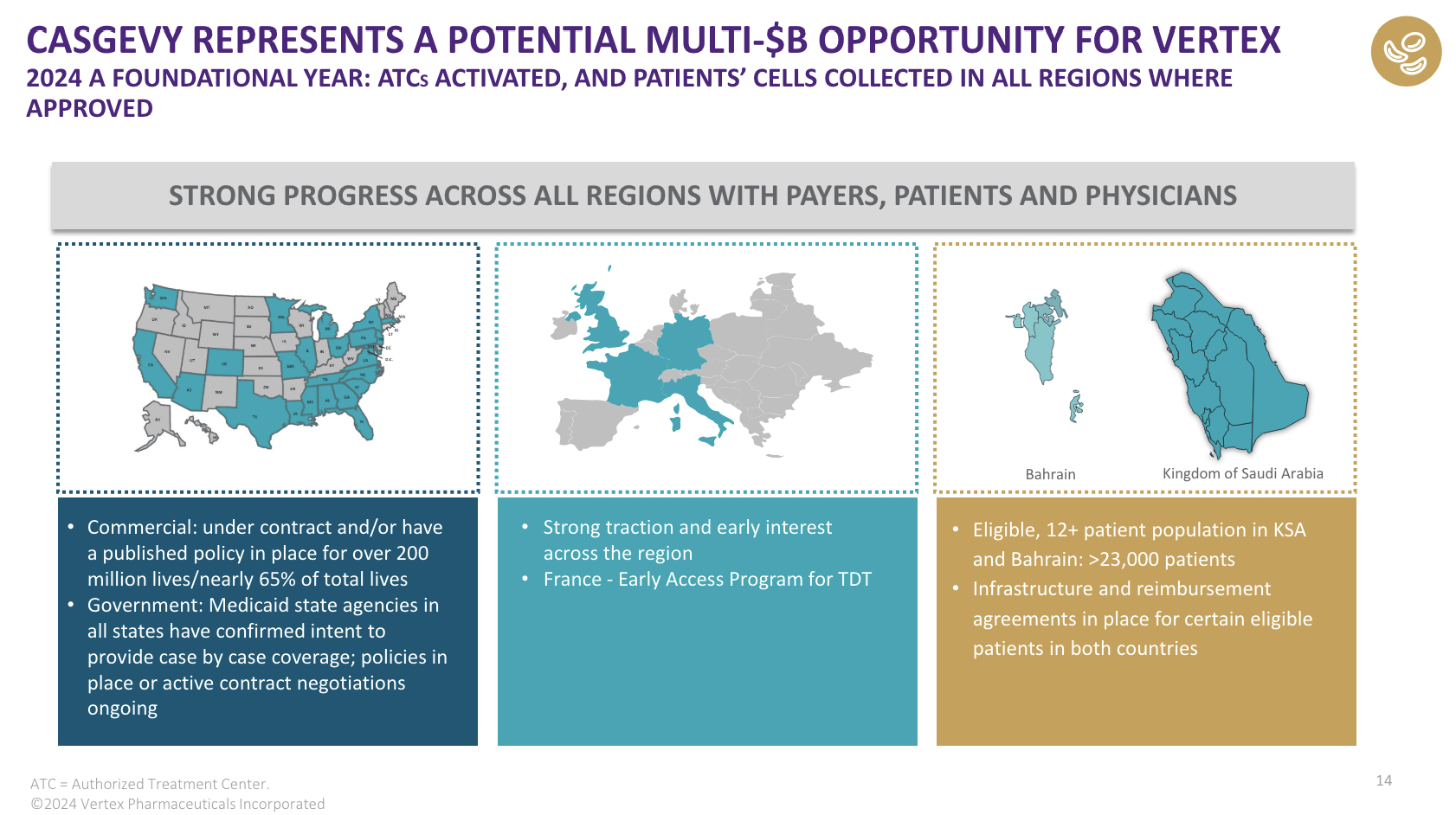

Moreover, the company launched CASGEVY, which is a new gene therapy for sickle cell disease and beta-thalassemia.

According to the company, it has made significant progress in securing reimbursement agreements with payers and started to enroll patients for treatment.

Using the data in the chart below, we see this drug is expected to be a potential multi-billion dollar opportunity for the company.

Vertex Pharmaceuticals

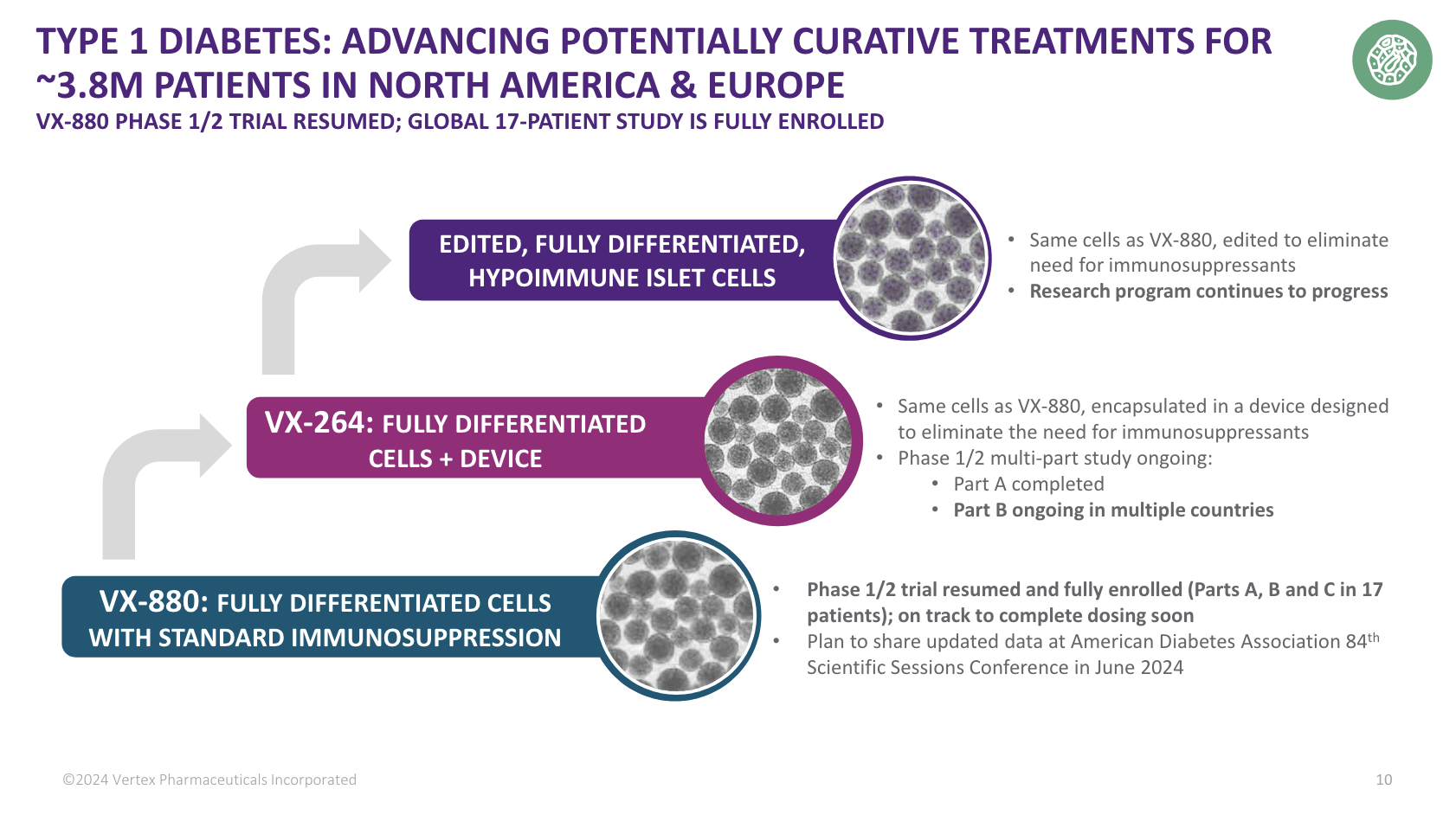

Last but not least, the company is focusing on type 1 diabetes with VX-880, which is a smell cell-derived, fully-differentiated islet cell therapy.

Essentially, this therapy targets patients with type 1 diabetes and impaired hypoglycemic awareness.

According to the company, following a positive data review, the VX-880 study has resumed, and all parts of the global 17-patient study are fully enrolled.

Vertex Pharmaceuticals

This summer, the company will present new results.

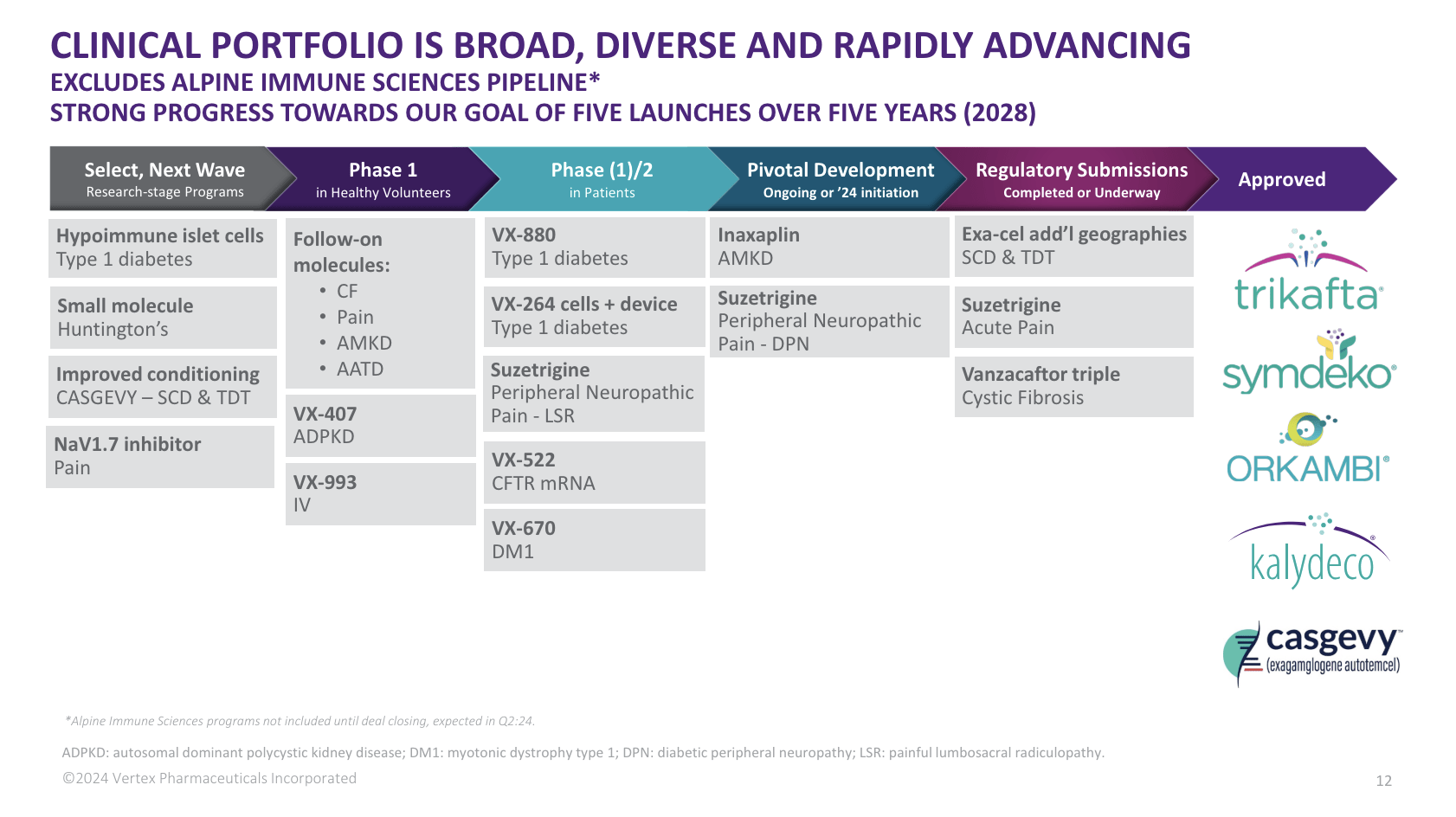

With all of this being said, here’s a full overview of the company’s pipeline and approved products:

Vertex Pharmaceuticals

So, what does this mean for shareholders?

Risk/Reward (Valuation)

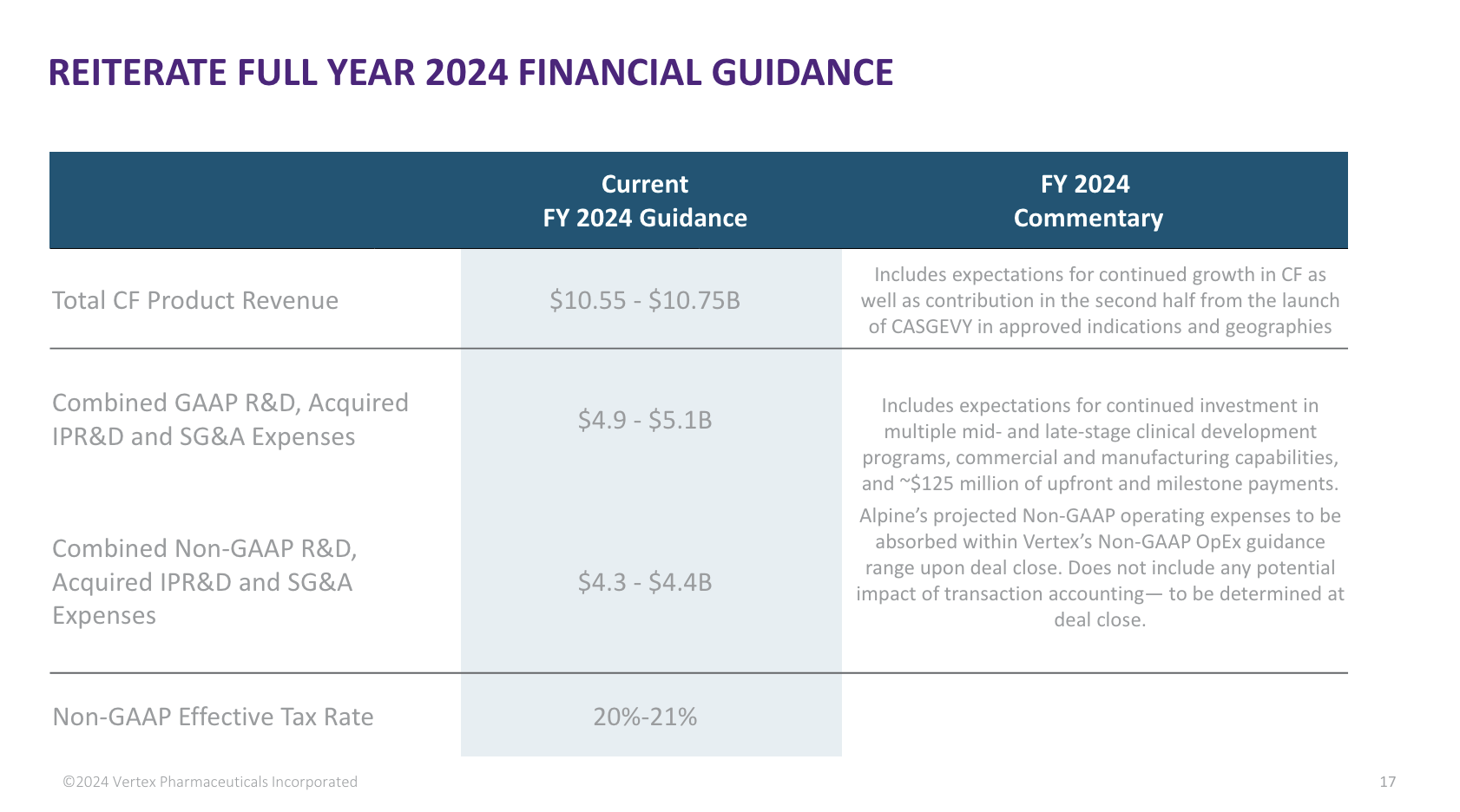

Thanks to a solid performance in existing products, the company stuck to its guidance, which sees annual revenue of $10.55 to $10.75 billion. The midpoint of that range is 8% above the 2023 result.

Vertex Pharmaceuticals

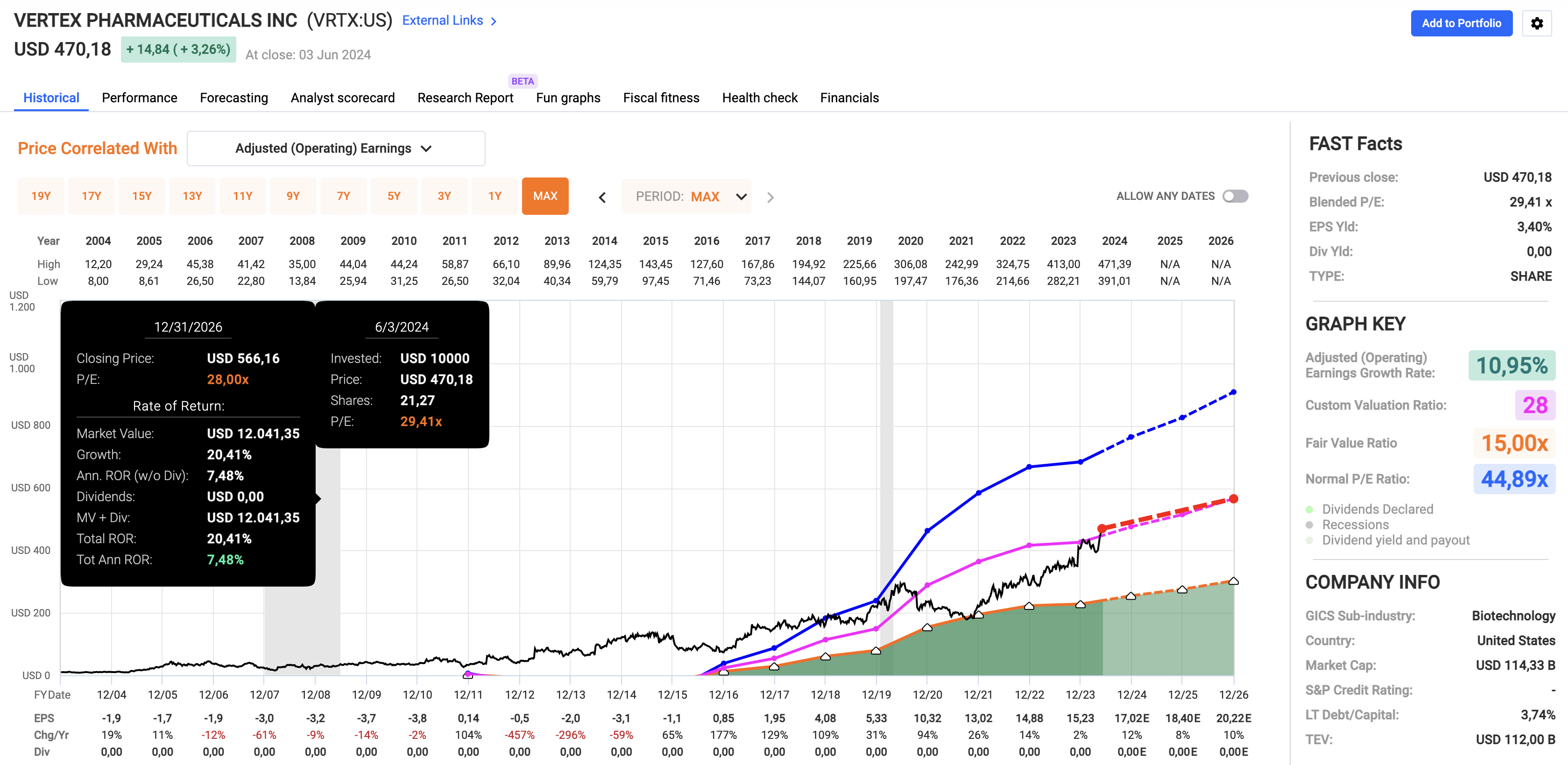

Using the FactSet data in the chart below, analysts expect this year’s EPS growth to be 12%, up from last year’s 2% growth. In 2025 and 2026, EPS growth is expected to be 8% and 12%, respectively.

FAST Graphs

This bodes well for shareholders.

Using its five-year normalized P/E ratio of 28x, we get a fair stock price target of $566, 20% above the current price.

It also is expected to end this year with close to $14 billion in net cash (more cash than gross debt), thanks to $4.3 billion in free cash flow (roughly 3.5% of its market cap).

While the absence of a dividend may keep some investors from buying the stock, I think we’re dealing with a healthcare giant that still has a lot of room to run.

Takeaway

I have little doubt that Vertex’s robust pipeline and strategic focus on innovation position it for substantial long-term gains.

Thanks to promising drugs for cystic fibrosis, pain management, kidney health, and type 1 diabetes, Vertex is well-positioned to maintain long-term elevated growth rates.

Essentially, the company’s solid portfolio and promising pipeline make it a compelling investment, as reflected in its strong revenue and EPS growth projections.

With a fair stock price target of $566, I believe Vertex still has significant room to grow, making it a biotech giant worth watching.

Pros & Cons

Pros:

- Strong Pipeline: Vertex has a very promising pipeline with major drugs for cystic fibrosis, (chronic) pain, kidney health, and type 1 diabetes.

- Market Leadership: The company is an established leader in cystic fibrosis treatments, which funds innovation/diversification.

- Revenue Growth: Vertex’s current portfolio is capable of elevated revenue and earnings growth.

- Valuation: With a fair stock price target of $566, there’s significant upside potential from current levels.

Cons:

- No Dividends: Although this is no dealbreaker, the fact that VRTX does not pay a dividend may keep some people from investing.

- Patent Cliff Risk: Like other biopharma companies, Vertex faces the risk of patent expirations. However, the company’s patents are young, which protects investors for more than a decade (assuming no new product launches).

- Market Volatility: Like most stocks, VRTX is subject to general market volatility, which could hurt its stock price in the mid-term.