Lemon_tm

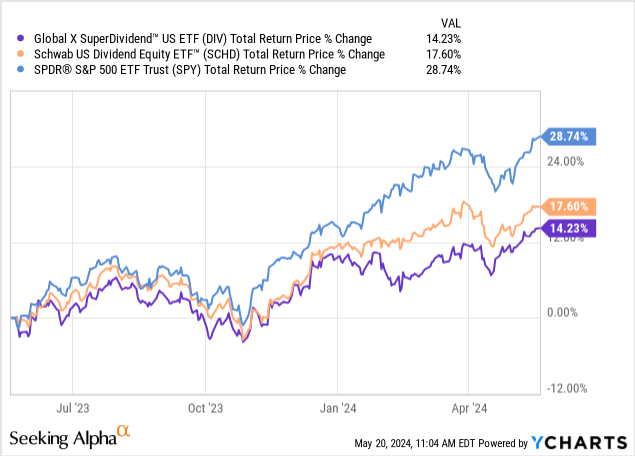

There’s been a lot of bad news lately for high-yield stocks (DIV, SCHD), which has fueled their general underperformance relative to the broader S&P 500 (SPY) over the past year:

In this article, we will discuss what these headwinds are, how we positioned our portfolio to outperform the high-yield sector and the S&P 500 despite these challenges recently, and how we plan to continue doing so moving forward.

Higher-For-Longer Inflation And Interest Rates

The first big headwind, which has had the biggest impact, is the fact that inflation, and therefore interest rates, appear poised to remain higher for longer. In addition to the headline readings showing this fact, the U.S.’s recent announcements of high tariffs on Chinese imports and growing divisions between these countries will likely be a factor that keeps inflation higher for longer. Moreover, consumer spending has remained much stronger than expected for quite some time, despite borrowing costs increasing and consumers rapidly spending down their pandemic savings. While this trend appears to be shifting somewhat, until it appears in the data, it’s difficult to get too optimistic about consumer spending no longer pushing inflation higher.

Another major reason why inflation has been high is due to runaway government deficit spending, including in areas like infrastructure, restructuring the global supply chain to decouple from China, significant increases in military expenditures due to rising geopolitical tensions, and support for Ukraine’s war against Russia. Additionally, the demographic shift in the United States is causing Social Security, Medicare, and Medicaid spending to soar. The massive influx of illegal immigrants in the United States is also driving up government and other societal costs. Another issue is that while the labor market has weakened somewhat recently, it remains fairly tight, resulting in wages going up and putting additional pressure on inflation.

An issue hurting inflation has been disruptions to global supply chains, including recent issues in the Suez Canal and the Persian Gulf due to the ongoing conflict between Israel and Palestine and the Iranian-backed Houthis, which has also pushed up shipping costs. Another inflationary headwind is that energy costs have been elevated due in part to Russia, a major oil exporter, being sanctioned over the war in Ukraine, along with strong demand and some issues with output meeting demand.

Additionally, while the AI boom is expected to be very deflationary over the long term, significant short-term investments are being made to build out the infrastructure for it, including data centers, and individual companies are investing aggressively in artificial intelligence research and development. The payoff from these investments is likely still several years away, so in the near term, it will have an inflationary impact before hopefully having a massive deflationary impact.

This higher inflation and higher interest rate environment are major headwinds for high-yield stocks relative to other types of stocks. High-yield stocks are often viewed as bond proxies, and therefore, when interest rates are higher, stock prices of high-yield companies like Realty Income (O), Enbridge (ENB), and AT&T (T) get beaten down accordingly to push up their dividend yields to have a sufficient premium to the risk-free rate to attract income investors. Additionally, many of these companies are also very capital-intensive, and therefore, higher for longer interest rates make it much more expensive for them to invest in sustaining and growing their businesses since they frequently need to tap the capital markets to raise additional capital for growth. In contrast, capital-light businesses in sectors like tech are less sensitive to interest rates when it comes to investing in their growth.

Specific Sector Headwinds

Additional bad news for high-yield stocks includes challenges facing specific sectors. For example, the BDC sector (BIZD) is facing a massive influx of investment capital, leading to growing competition and an increasingly unfavorable balance between supply and demand for lenders in the space. This is due to trillions of dollars pouring in from the world’s leading asset managers, such as Blackstone (BX, BXSL), BlackRock (BLK), Brookfield (BN, BAM, OCSL), Ares (ARES, ARCC), KKR (KKR, FSK), Carlyle (CG, CGBD), Apollo (APO), Blue Owl (OWL, OBDC), JPMorgan (JPM), Goldman Sachs (GS, GSBD), and others. As a result, there are concerns that underwriting standards may be declining, and at the very least, the terms that many of these lenders can command on their new investments are less attractive than previously, resulting in a declining risk-reward profile for investors.

In addition, the sector is dealing with weakening fundamentals as prolonged elevated levels of interest rates and inflation are beginning to squeeze many of their middle-market counterparties. As a result, their credit facilities are being drawn down, their leverage ratios are rising, and their interest coverage ratios are declining. Consequently, non-accruals are beginning to increase, and at some point, this is likely to turn into an increase in defaults, causing the sector as a whole to suffer.

Already, the number of credit card and auto loan delinquencies is rising across all age groups, as it did in the first quarter. Moreover, household debt grew by 1.1% in the first quarter to a staggering $17.69 trillion, with pandemic-era excess savings completely wiped out, going from a high of $2.1 trillion in August 2021 to -$72 billion as of the end of Q1. This likely means that middle-market companies are also going to feel the pain of weakened consumer buying power and the generally elevated debt levels of the U.S. economy.

Meanwhile, utilities and yield cos (XLU), while they have benefited from some recent regulatory changes and signs of growing demand for electricity from data centers—as highlighted by the recent $10 billion-plus deal between Microsoft (MSFT) and Brookfield Renewable Partners (BEP, BEPC) — are still grappling with higher capital costs, which are weighing on their ability to build out the necessary energy infrastructure at sufficiently attractive returns to meet demand. This weakened growth profile, combined with higher interest rates, is applying pressure to valuation multiples in this sector.

Moreover, the midstream sector (AMLP), while overall quite healthy due to strong balance sheets and free cash flow generation, is no longer the compelling deep-value bargain it was a few years ago and could face some issues if the global economy weakens and heads into recession. Additionally, opportunities for new growth are increasingly limited, though some businesses such as Enterprise Products Partners (EPD) and Energy Transfer (ET) continue to enjoy substantial growth profiles. In contrast, some of their peers like Western Midstream (WES) and Plains All American (PAA, PAGP) are slashing growth CapEx and instead aggressively growing their distributions and returning capital to shareholders. However, they are nearing their maximum ability to accelerate those returns, which means that their prices are likely near a peak.

Finally, the commercial property sector, represented by REITs (VNQ) and regional banks (KRE), which are both high-yield sectors, is also facing major challenges. These include high vacancy rates, especially in office buildings, leading to severe problems in the office REIT space that will likely continue for the foreseeable future. An increase in non-performing loans to landlords is weighing on regional banks, with the threat of this accelerating recently causing major distress and upheaval at prominent high-yield regional banks like New York Community Bancorp (NYCB). The higher interest rate for a longer environment, combined with a wall of upcoming commercial property debt maturities that were underwritten at much lower interest rates, could lead to a surge in defaults, additional property vacancies, and ultimately substantial distress in both the commercial real estate and regional bank sectors, which have substantial exposure to commercial real estate. Regional banks are also suffering from increased regulatory scrutiny, as NYCB can attest, which could lead to further dividend cuts and turmoil in this sector.

Investor Takeaway

Given all these challenges facing the high-yield space, it’s not surprising at all that it has underperformed recently, and it would not shock us if it continued to underperform in the near future. That being said, we have been able to generate meaningful outperformance for the last three and a half years thanks to our focus on financially strong companies and sectors like midstream as the core of our portfolio, which have provided a powerful combination of current yield, distribution growth, and increasingly strong balance sheets. Meanwhile, we have also opportunistically picked our spots in the alternative asset management, BDC, utility, and infrastructure spaces.

While we do not have a 100% success rate in these sectors, overall, we have been able to identify several high-yielding, high-quality businesses that have been unfairly beaten down by Mr. Market, thereby offsetting at least some of the headwinds in these sectors. We have also invested on the fringes of the high-yield space with some opportunistic picks in places like market makers and consumer and industrial goods and have doubled down on our bets on the bullish outlook for precious metals and copper for the foreseeable future, generating significant profits there as well.

Moving forward, we continue to see some niche opportunities in each of these spaces, placing some of our heaviest bets on stocks that are off the beaten path and largely immune to these aforementioned headwinds (e.g., Patria Investments (PAX)). As a result, we remain confident in our ability to continue generating a lucrative combination of current yield and attractive long-term total returns, regardless of how these current headwinds to the high-yield space evolve moving forward.