Thai Liang Lim/E+ by way of Getty Photographs

As a basic rule of thumb, it’s silly to count on a inventory to double or greater than double in a brief window of time. Though fundamentals could also be in your facet and main selections might be made by administration, timing is commonly a bigger function to play in case you can seize that sort of return in a yr or much less. And often, after an organization does expertise such meteoric upside, the pure transfer is to promote your inventory and transfer on. However one agency that has skilled this sort of transfer increased that seemingly does warrant slightly further upside is premium egg producer Very important Farms (NASDAQ:VITL).

Again in October of 2023, I ended up upgrading the company from a ‘maintain’ to a ‘purchase’. As much as that time, I had been moderately impartial on the enterprise. Nonetheless, I discovered myself impressed with its continued progress. This included not solely income, but additionally earnings. Once I dug in deeper, I additionally seen that the corporate remained assured in its plan to develop income to over $1 billion by 2027. And once I checked out what this is able to imply for shareholders in the long term, I couldn’t assist however to take a extra bullish stance on the enterprise than I beforehand had. Thus far, that decision has confirmed to be successful. Whereas the S&P 500 is up 26.1% since then, shares of Very important Farms have seen upside of 113.5%. Clearly, the simple cash has been made. However I’d argue that some further upside in all probability exists from right here. So due to that, I’ve determined to maintain the corporate rated a delicate ‘purchase’ presently.

The image retains enhancing

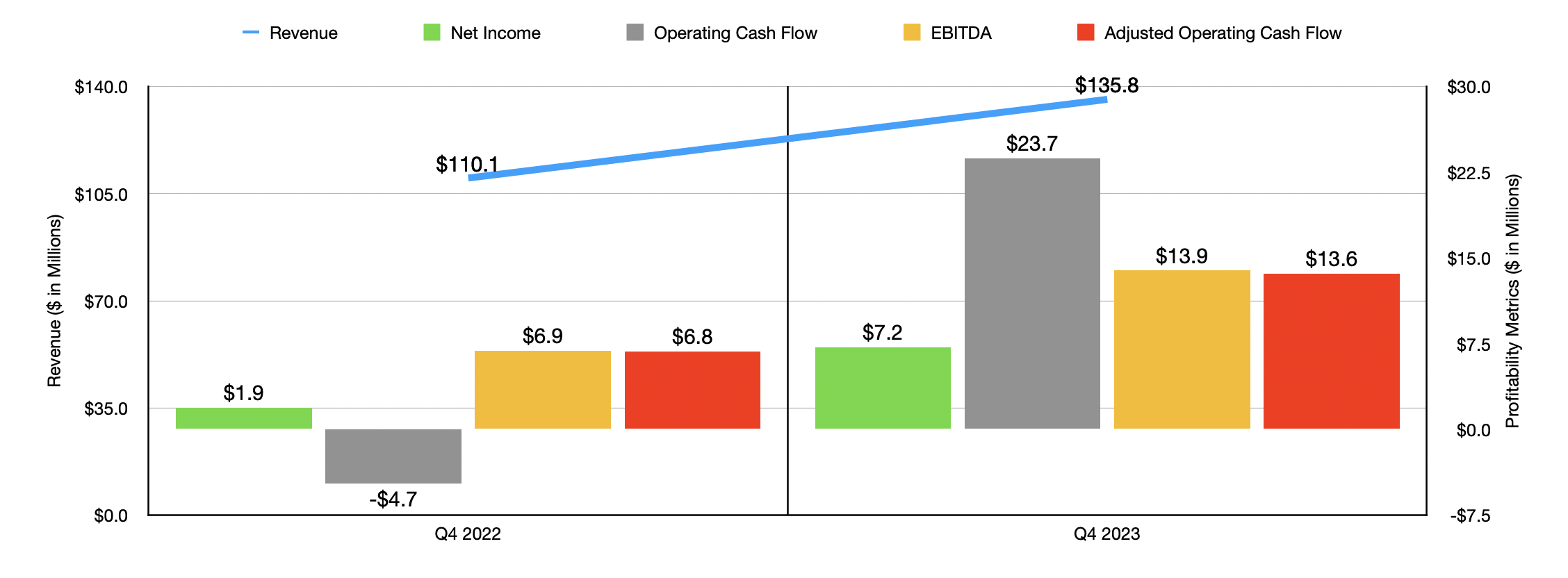

Essentially talking, issues are going fairly properly for Very important Farms and its traders. Take the final quarter of the 2023 fiscal yr for instance. Throughout that point, income for the enterprise got here in at $135.8 million. That is 23.3% increased than the $110.1 million reported one yr earlier. To be clear, a few of this upside was pushed by an additional working week that the corporate had. If we strip this from the equation, income nonetheless would have risen by 15.7%. Increased costs performed a job on this improve. However the greater contributor was a rise in quantity as the corporate constructed up its capability additional. That helped to the tune of 11.6% and mirrored elevated enterprise from not solely new corporations, but additionally current retail prospects.

Writer – SEC EDGAR Knowledge

On the underside line, Very important Farms carried out rather well. Web revenue spiked from $1.9 million to $7.2 million. And working money circulate improved from unfavorable $4.7 million to constructive $23.7 million. If we regulate for adjustments in working capital, we get precisely a doubling within the metric from $6.8 million to $13.6 million. And lastly, EBITDA for the corporate managed to develop from $6.9 million to $13.9 million. Despite the fact that the agency suffered from increased advertising prices geared toward supporting model improvement, in addition to a rise in worker associated bills due to increased headcount, the agency benefited not solely from the rise in income, but additionally from higher revenue margins when it got here to value of products offered.

Writer – SEC EDGAR Knowledge

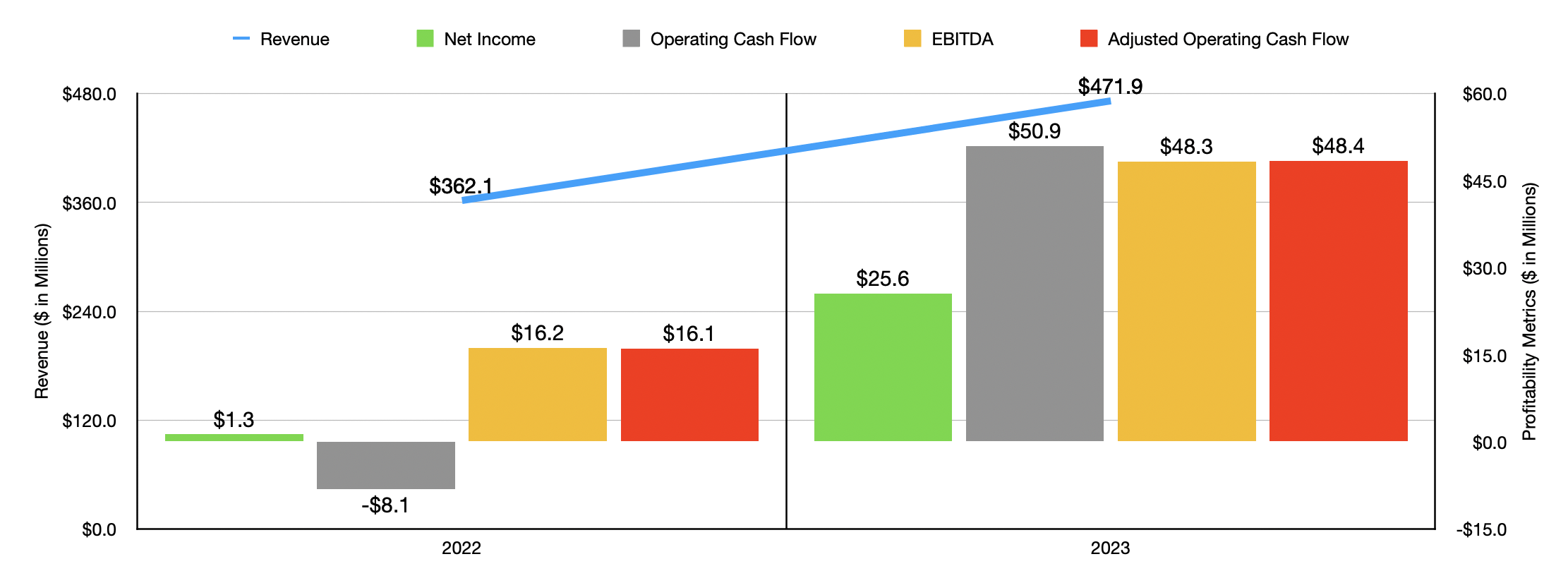

In relation to the 2023 fiscal yr and its entirety, the image for the enterprise was fairly constructive. Income of $471.9 million dwarfed the $362.1 million reported in 2022. Increased costs and a quantity achieve of 13.9% have been largely answerable for this enchancment. Naturally, the corporate’s backside line expanded as properly. As you’ll be able to see within the chart above, internet earnings skyrocketed from $1.3 million to $25.6 million. Working money circulate and adjusted working money circulate each improved markedly. And EBITDA for the corporate expanded from $16.2 million to $48.3 million.

Very important Farms

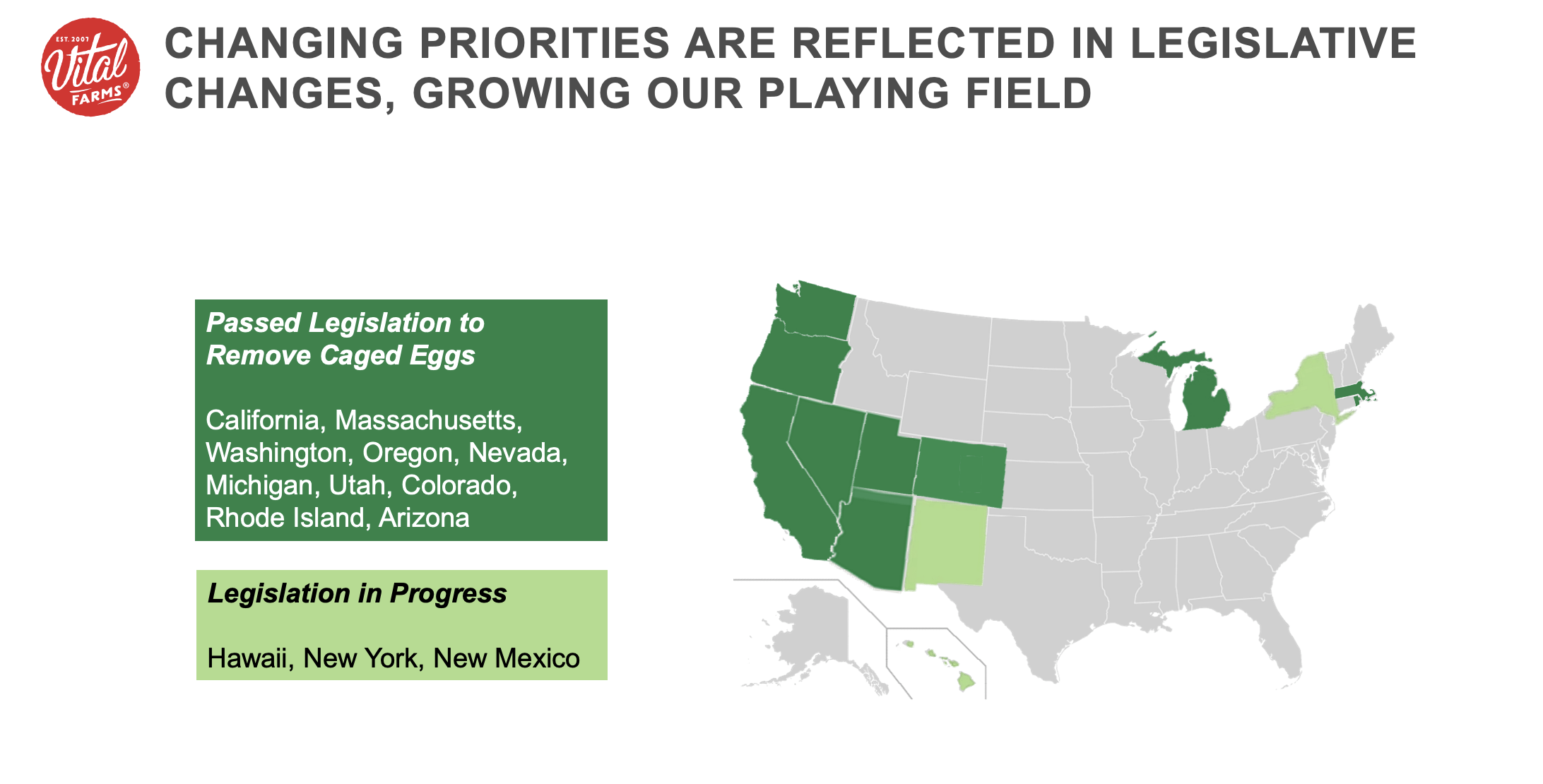

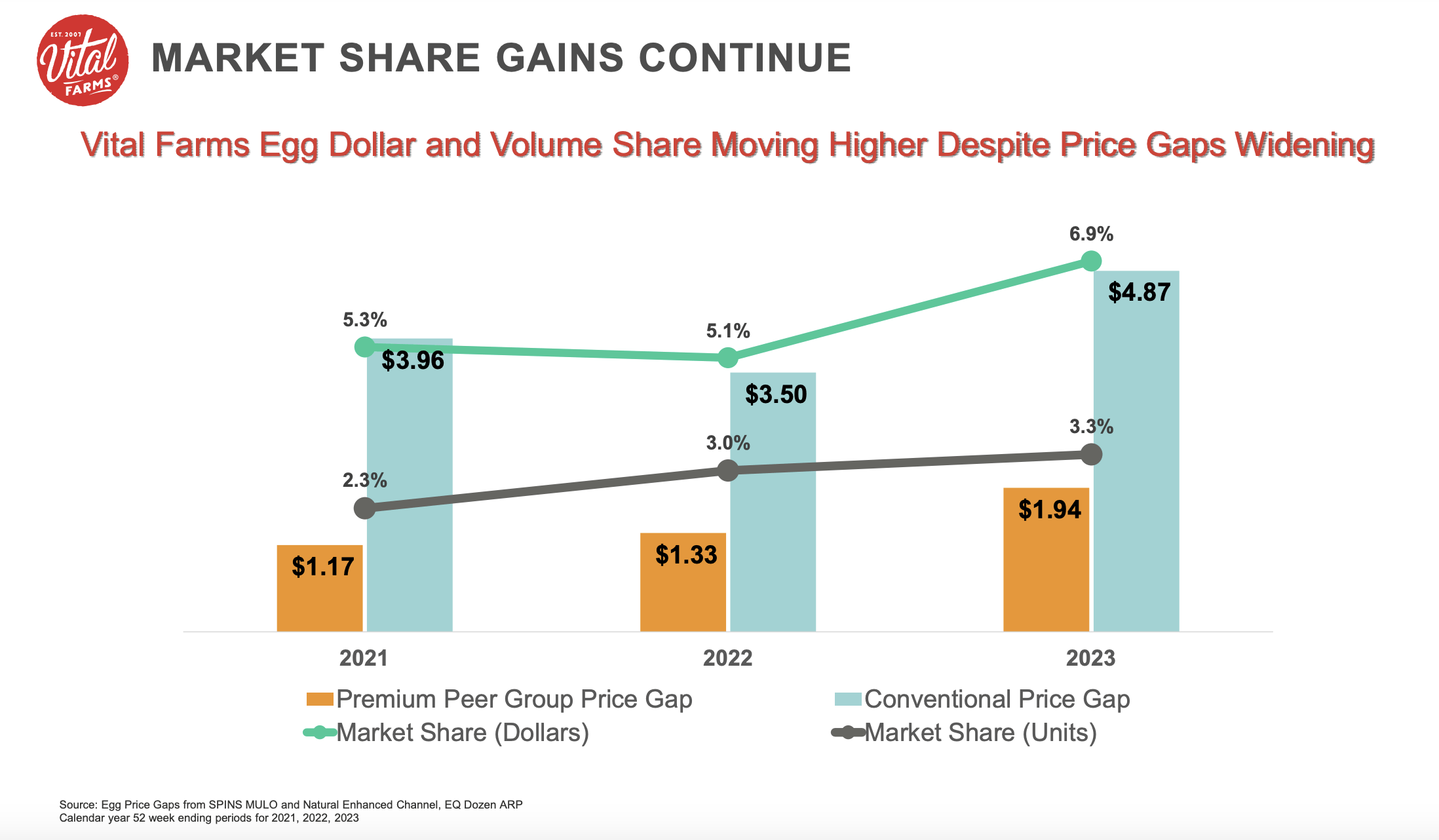

The actually thrilling factor for shareholders is that administration expects progress for the enterprise to proceed. For starters, in response to administration, several states, together with California, Massachusetts, Oregon, and others, have all handed laws to take away caged eggs from their markets. Different states like Hawaii, New York, and New Mexico, are contemplating doing the identical. This can improve the demand for the cage free eggs promoted by Very important Farms. Actually, the corporate boasts that the typical hen has an open air, 108 sq. foot area. Along with rising in popularity due to regulatory adjustments, customers are snatching up its eggs. In relation to shell eggs, the corporate boasted a 23.7% share of pockets spend in 2023. That is up from 18.6% again in 2020. And as you’ll be able to see within the chart under, the corporate’s greenback and quantity share within the egg area continues to enhance.

Very important Farms

Administration believes that continued funding, together with between $35 million and $45 million on capital expenditures this yr, that may assist it develop capability to the purpose the place income needs to be $1 billion or increased by 2027. After all, the corporate has to get there one step at a time. For 2024, income is anticipated to be in extra of $552 million. And EBITDA it is forecasted to be above $57 million. If the corporate can hit its targets for 2027, then EBITDA would climb to round $130 million. That brings with it practically 300 foundation factors in margin enlargement that can be pushed by value will increase and, for essentially the most half, elevated quantity.

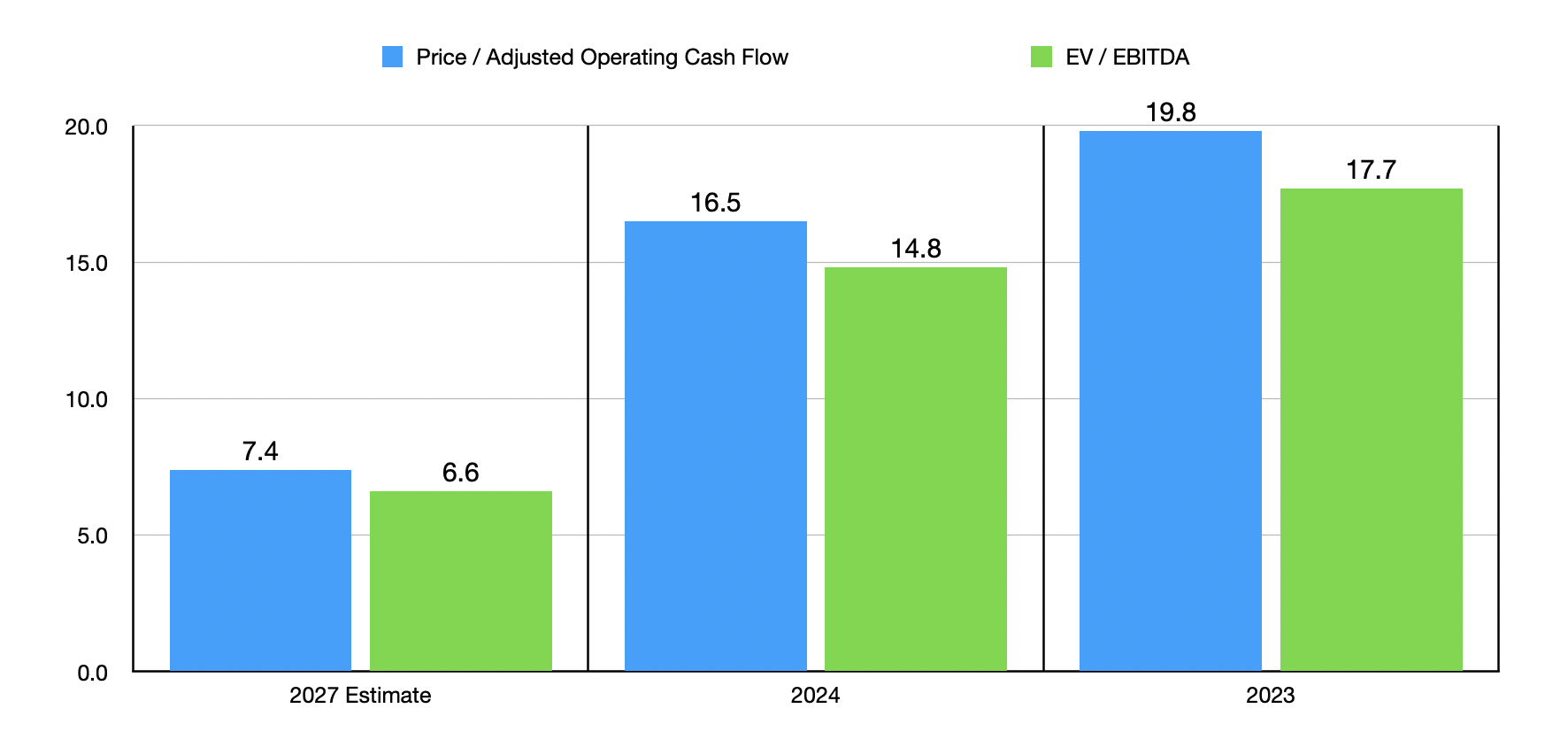

Writer – SEC EDGAR Knowledge

Usually, I’m skeptical about steerage, notably after we are speaking a number of years into the long run. However administration has remained assured on this goal for a while. Moreover, the corporate’s progress has been fairly spectacular as of late. Utilizing the estimates supplied by administration, I used to be capable of worth the corporate as proven within the chart above. It reveals historic outcomes for 2023, in addition to projected outcomes for each 2024 and 2027. Utilizing even the 2024 estimates, I’d say that the inventory is kind of pretty valued. It won’t even be that far off from being overvalued. However once you mission out to 2027, shares appear to have some moderately significant upside. As an illustration, if we use the worth to adjusted working money circulate a number of for the enterprise and assume that, as soon as it hits its goal in 2027, an applicable worth for the enterprise could be a a number of of 12, that may indicate upside of round 13% each year between every now and then. That is a bit higher than the roughly 11% or in order that the S&P 500 averages over time. I then in contrast the corporate to 5 comparable corporations as proven within the desk under. On a value to working money circulate foundation, even utilizing the 2023 figures, three of the 5 corporations ended up being cheaper than it. This quantity does rise to 4 of the 5 when utilizing the EV to EBITDA method.

| Firm | Worth / Working Money Circulation | EV / EBITDA |

| Very important Farms | 19.8 | 17.7 |

| SunOpta (STKL) | 51.6 | 25.3 |

| The Hain Celestial Group (HAIN) | 6.9 | 16.1 |

| B&G Meals (BGS) | 3.4 | 16.7 |

| Mission Produce (AVO) | 20.8 | 15.1 |

| Adecoagro (AGRO) | 2.4 | 3.0 |

Takeaway

Essentially talking, Very important Farms is doing rather well for itself. The corporate continues to display engaging progress, and I’d say that it’ll in all probability obtain its goal by 2027. After all, something can change. However to date, you’ll be able to rely me as a type of which can be impressed. The simple cash has been made and, relative to comparable corporations, shares are trying moderately dear. However after we think about future progress, upside appears to be interesting sufficient to warrant a bit extra optimism. If shares rise one other 10% to twenty%, I’d in all probability contemplate it an excellent candidate for a modest downgrade. However as issues stand, a delicate ‘purchase’ score continues to be logical.