Olivier Le Moal

Simply over three months in the past, I wrote on Victoria Gold (OTCPK:VITFF), noting that whereas the H2 outlook had seen a downgrade due to wildfire associated stoppages, this was getting priced into the inventory. And whereas the inventory drifted decrease heading into its Q3 report, I began a place at US$4.30 on condition that it was changing into far too low cost to disregard, even for a quickly higher-cost producer (LOM AISC estimates: $1,114/ozper 2022 TR). This place has contributed to continued outperformance in my portfolio vs. the Gold Miners Index (GDX), and the justification for lastly beginning a place within the inventory was three-fold:

1. The sell-off seemed overdone with the inventory down 78% from its all-time highs even with the gold worth simply ~10% from all-time highs.

2. The valuation was essentially the most engaging it had been in years at ~0.40x P/NAV and ~3.0x FY2025 free money move estimate.

3. Its pipeline was bettering, with Raven persevering with to seem like a ~2.0 million ounce deposit at increased grades (1.8+ grams per tonne of gold), and the latest acquisition paving the best way to probably changing into a dual-asset producer down the road.

Portfolio Returns – July 1st 2020 to November 2023 – Creator’s Photograph

I’ve purposely used the worst attainable benchmark for GDX in Q3 2020 when the index peaked vs. solely exhibiting returns in intervals when the benchmark has been constructive.

Since its October lows, Victoria has outperformed the GDX with a ~30% rally, launched new drill outcomes from Raven, and launched its Q3 outcomes, which confirmed a ~93% margin enchancment (albeit helped by decrease than deliberate capitalized stripping). And with the gold worth marching to new all-time highs in This autumn, the corporate can have an excellent higher This autumn-23 and a a lot better FY2024 if the gold worth can maintain on to most of its beneficial properties. On this replace, we’ll dig into the Q3 outcomes, why Victoria appears poised for additional upside, and the place the inventory’s up to date low-risk purchase zone lies.

Eagle Gold Mine Operations – Firm Web site

All figures are in United States {Dollars} until in any other case famous with a C$ in entrance of the greenback determine.

Q3 Manufacturing & Gross sales

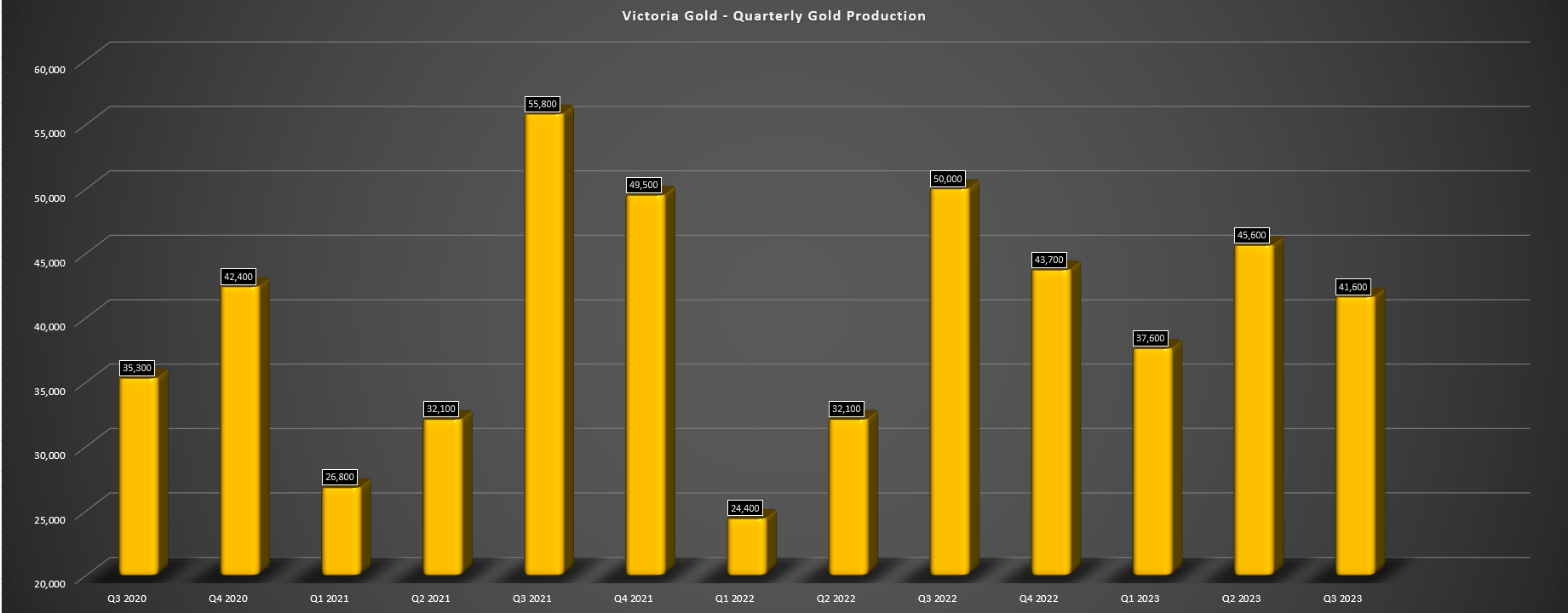

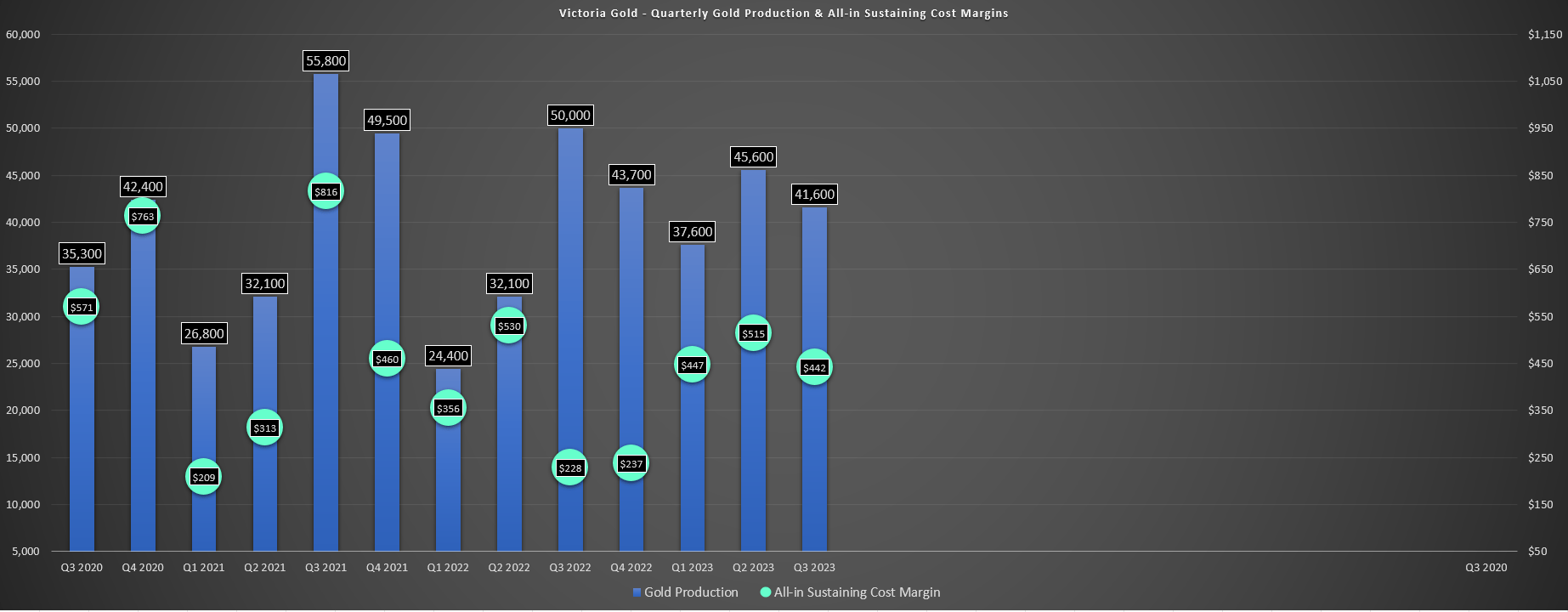

Victoria Gold launched its Q3 outcomes final month, reporting quarterly manufacturing of ~41,600 ounces of gold, a 17% decline from the year-ago interval. Nevertheless, this sharp decline was associated to decrease grades (mine sequencing) and the influence of two temporary stoppages associated to wildfire evacuations that affected stacking operations. This definitely put a dent in its Q3 efficiency and has left it monitoring in the direction of the low finish of annual steering vs. being on observe for a beat on its mid-point beforehand. And whereas it is clearly disappointing to see the Eagle Mine monitoring in the direction of one other steering miss this 12 months after a number of consecutive misses since mine start-up, however the present miss is totally out of the corporate’s management and operations look to be operating smoother total exterior of the Q3 headwinds with much less seasonality (year-round stacking). Plus, whereas Q3 manufacturing was decrease, year-to-date manufacturing is sitting at a report ~124,800 ounces regardless of the influence of decrease grades, suggesting this mine is able to producing ~200,000 ounces if it will probably function with out shock interruptions.

Victoria Gold Quarterly Gold Manufacturing – Firm Filings, Creator’s Chart

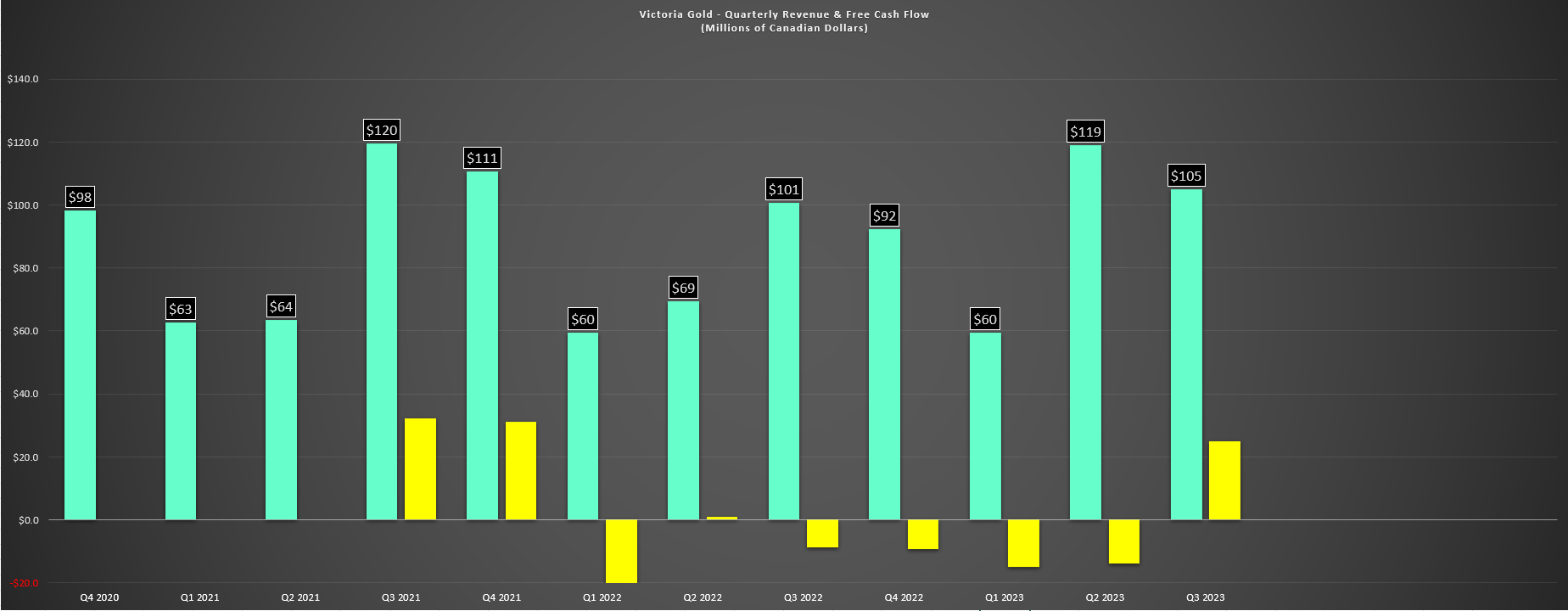

As for Victoria’s monetary outcomes, income got here in at C$105.1 million (+5% year-over-year) regardless of fewer ounces bought than produced, with Victoria getting some assist from the upper gold worth. In the meantime, web earnings elevated to C$5.6 million, and the corporate reported constructive free money move of C$18.2 million earlier than working capital. As for its stability sheet, Victoria ended the quarter with ~$14 million in money and ~$170 million in web debt and it prolonged the maturity of its RCF from year-end 2024 to year-end 2025. General, that is definitely a fabric enchancment from the year-ago interval helped by increased gold costs, with Victoria producing over C$31 million in free money move year-to-date, elevated capital expenditures relative to lifetime of mine averages (Q3 2023: C$21.1 million) and regardless of the influence of wildfire evacuations.

Victoria Gold – Quarterly Income & Free Money Circulation – Firm Filings, Creator’s Chart

Prices & Margins

Transferring over to prices and margins, all-in sustaining prices [AISC] got here in beneath my expectations in Q3 at $1,484/ozwhich was partially associated to decrease than guided capitalized stripping as a result of timing of waste mining. This represented a marginal decline over the year-ago interval (Q3 2022: $1,489/oz), however a 93% improve in AISC margins ($442/ozvs. $228/oz) with Victoria benefiting from a better common realized gold worth. And whereas that is partially associated to lapping simple year-over-year comparisons (low gold worth and unplanned downtime), precise unit prices would have been nearer to $1,400/ozif not for the setback in Q3. Plus, whereas value steering is now monitoring in the direction of the excessive of the $1,350/ozto $1,550/ozguidance vary, we should always see one other step up in margins in This autumn with the gold worth averaging $1,960/ozquarter-to-date and more likely to common a minimum of $1,975/ozfor This autumn.

Victoria Gold Manufacturing & AISC Margins – Firm Filings, Creator’s Chart

The one adverse price noting is that Victoria definitely hasn’t been immune from inflationary pressures, however on condition that it is a high-volume operation it has seen some advantages from the pullback in vitality costs. This was mentioned on the Q3 Convention Name (as proven beneath).

“Our #1 cost input is labor and the persistent upward pressure on wages is causing increased cost, and this also affects contractors and consultant costs. We have seen a fairly wide range of commentary from our industry peers regarding inflation with some peers noting that inflation is subsiding and others noted that it’s still an issue. This might be influenced by jurisdiction or a host of other factors. But for Western Canada and Yukon, where we do business, inflation continues, and we are seeing wage pressures as well as cost pressures across the board.”

– Q3 2023 Convention Name, Victoria Gold

Nevertheless, from a much bigger image standpoint, there’s purpose to be optimistic. For starters, Victoria Gold ought to produce nearer to 190,000 ounces in 2024 and over 200,000 ounces in 2025 which is able to positively influence unit prices (increased denominator), and the mine may even profit from a decrease strip ratio (2024-2026) and barely decrease capital expenditures vs. 2022 and 2023 which have been increased capex years. Concurrently, Victoria appears more likely to profit from a better gold worth, and I do not assume it is unreasonable to consider that the gold worth might common $2,000/oznext 12 months. So, even assuming AISC of $1,450/ozin 2024 and $1,200/ozin 2025, we should always see AISC margins enhance from ~$450/ozin 2023 to $550/ozin FY2024 and $800/ozin FY2025 which I might count on to lead to a big enchancment in sentiment for the inventory. And for my part, that is shift to constructive sentiment is nowhere close to priced in presently, with Victoria nonetheless buying and selling at a depressed a number of as we’ll dig into beneath:

Latest Developments

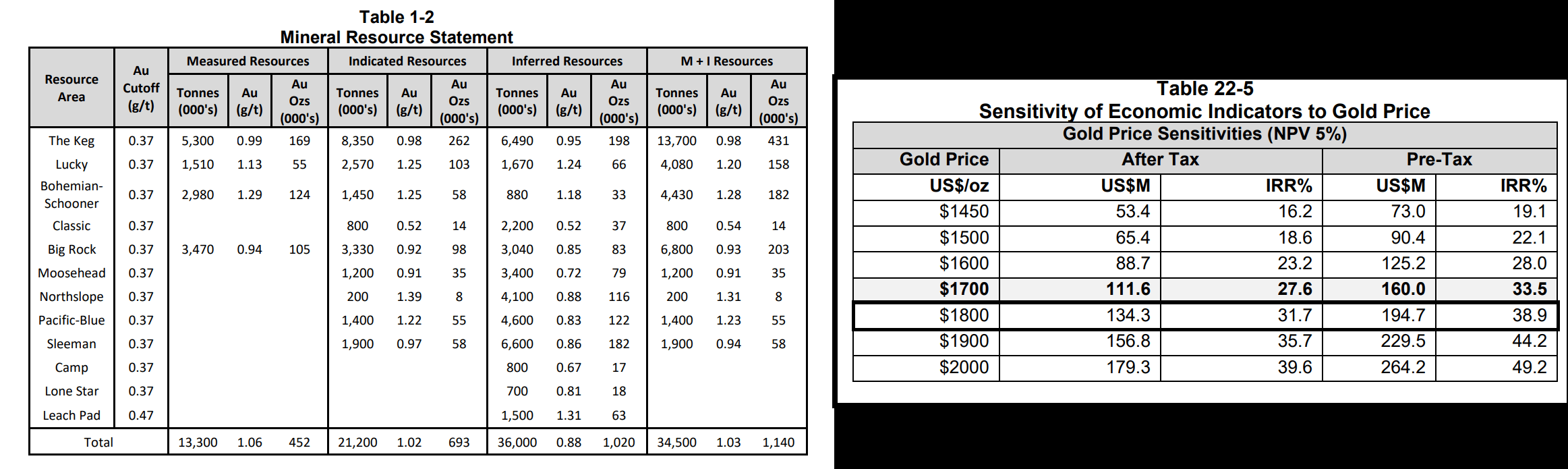

In mid-September, Victoria Gold introduced that it had bought Sabre Gold Mines’ Yukon belongings for $10 million (some would possibly acknowledge these belongings in the event that they adopted Golden Predator), which included a 100% curiosity in Brewery Creek (advanced-stage heap-leach mission), Gold Dome and Grew Creek. This deal comes after they missed their alternative to purchase ATAC Assets with Hecla (HL) outbidding them. Grew Creek and Gold Dome cowl 230 sq. kilometers, considerably increasing Victoria’s land place within the Yukon Territories. In the meantime, Brewery Creek (historic producer of ~280,000 ounces of gold) is a 180 sq. kilometer mission that lies 120 kilometers west of Victoria’s Eagle Mine and it is a good match with it being an above common grade heap leach mission with ~1.14 million ounces of measured & indicated sources at 1.03 grams per tonne of gold and one other ~1.02 million ounces of gold at 0.88 grams per tonne of gold.

Brewery Creek Useful resource & After-Tax NPV (5%) – 2022 TR

As for mission economics, A PEA was accomplished in early 2022 that envisioned $117 million in upfront capex (doubtless nearer to $145 million when baking in 22%-25% inflation to be conservative by the point it is constructed) with common unit prices of ~$21.50/tonne with a 9,000 tonne per day processing charge, and ~$970/ozall-in sustaining prices (~$1,300/ozlooks extra life like when adjusting for inflation and the truth that scoping research typically understate precise prices). Nonetheless, the mine has an estimated mine lifetime of eight years and anticipated gold manufacturing of ~480,000 ounces, and the estimated After-Tax NPV (5%) was $134 million at $1,800/oz. So, even adjusting for increased capital prices and working prices to be extra conservative, it appears like Victoria acquired this asset for simply ~$10/ozand fewer than 0.15x P/NPV, which is a really affordable worth.

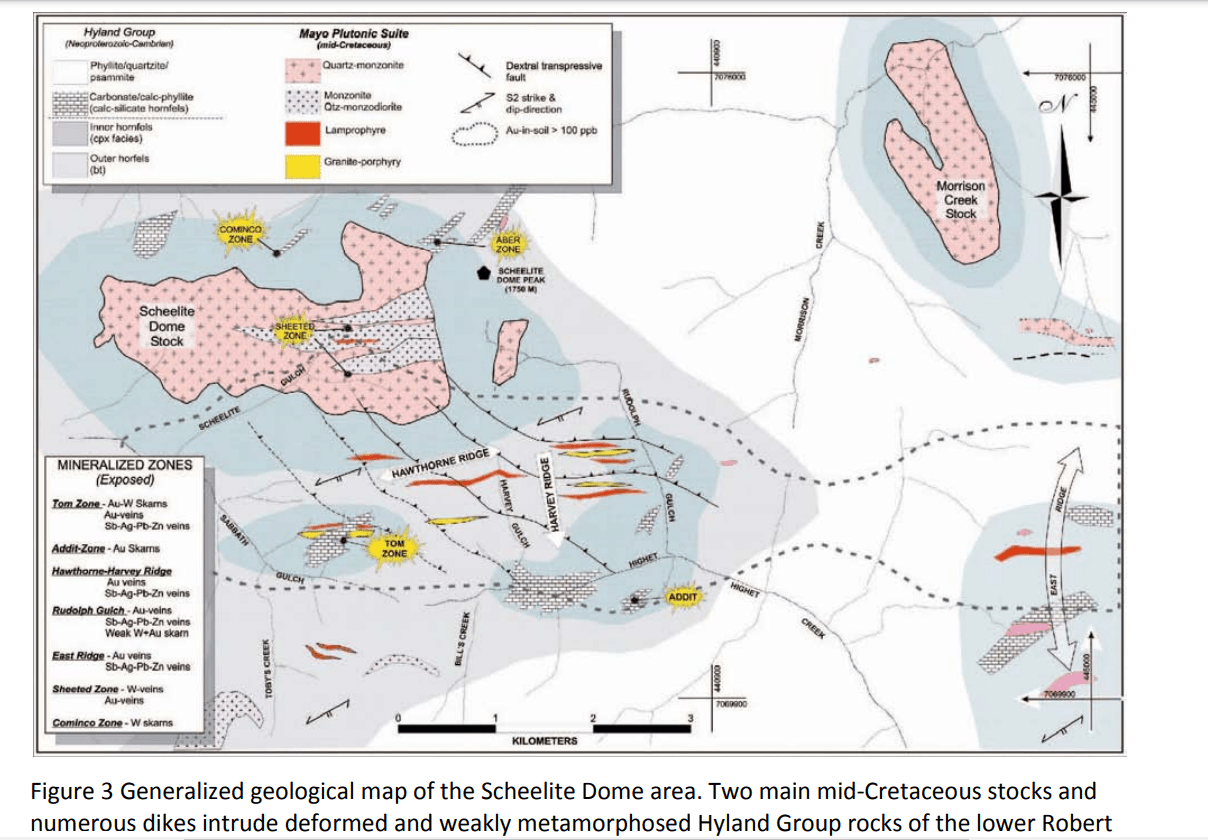

Nevertheless, the opposite profit is that Golden Predator (Sabre’s wholly owned subsidiary) had $33 million in non-reported capital losses, probably offering synergies from this angle as nicely. Lastly, the corporate seems fairly excited in regards to the Gold Dome Venture, which is south of Eagle and far nearer relative to Brewery Creek. In keeping with Victoria, Gold Dome is a 9,500 hectare property and an “intrusion related gold target with the potential for bulk tonnage sheeted vein style deposits and high-grade skarn, replacement, and vein style deposits, and one of the largest gold-arsenic-bismuth soil anomalies in the Yukon.” Small placer mining occurred on the property after the invention of placer in Johnson Creek and Highet Creek, and historic outcomes by Golden Predator embody:

- 21.95 meters of 1.00 grams per tonne of gold (Hawthorne Ridge)

- 25.4 meters of 11.12 grams per tonne of gold (Tom Zone)

- 9.8 meters of 1.68 grams per tonne of gold (Tom Zone)

- 13.3 meters of 1.29 grams per tonne of gold (Tom Zone)

- 12.19 meters of 1.49 grams per tonne of gold (Swede Zone)

Gold Dome Mineralized Zones – Golden Predator Evaluation Report

General, I like this deal. It is because it is a comparable mission in the identical jurisdiction, suggesting that it is in Victoria’s wheelhouse when it comes to technical complexity, and it is a logical match, much like when Orla (ORLA) additionally acquired an above common grade heap leach asset (Railroad South) to enhance its Camino Rojo Oxides Mine. Plus, the danger is low on a deal at this worth and the corporate will get further exploration upside, making this one of many higher offers accomplished previously few years from a threat standpoint (low worth paid, potential tax swimming pools and good optionality). And assuming the corporate goes forward with beginning a brand new operation at Brewery Creek, it is a comparatively low capex strategy to shed its single-asset producer standing and add one other 50,000+ ounces of annual manufacturing every year.

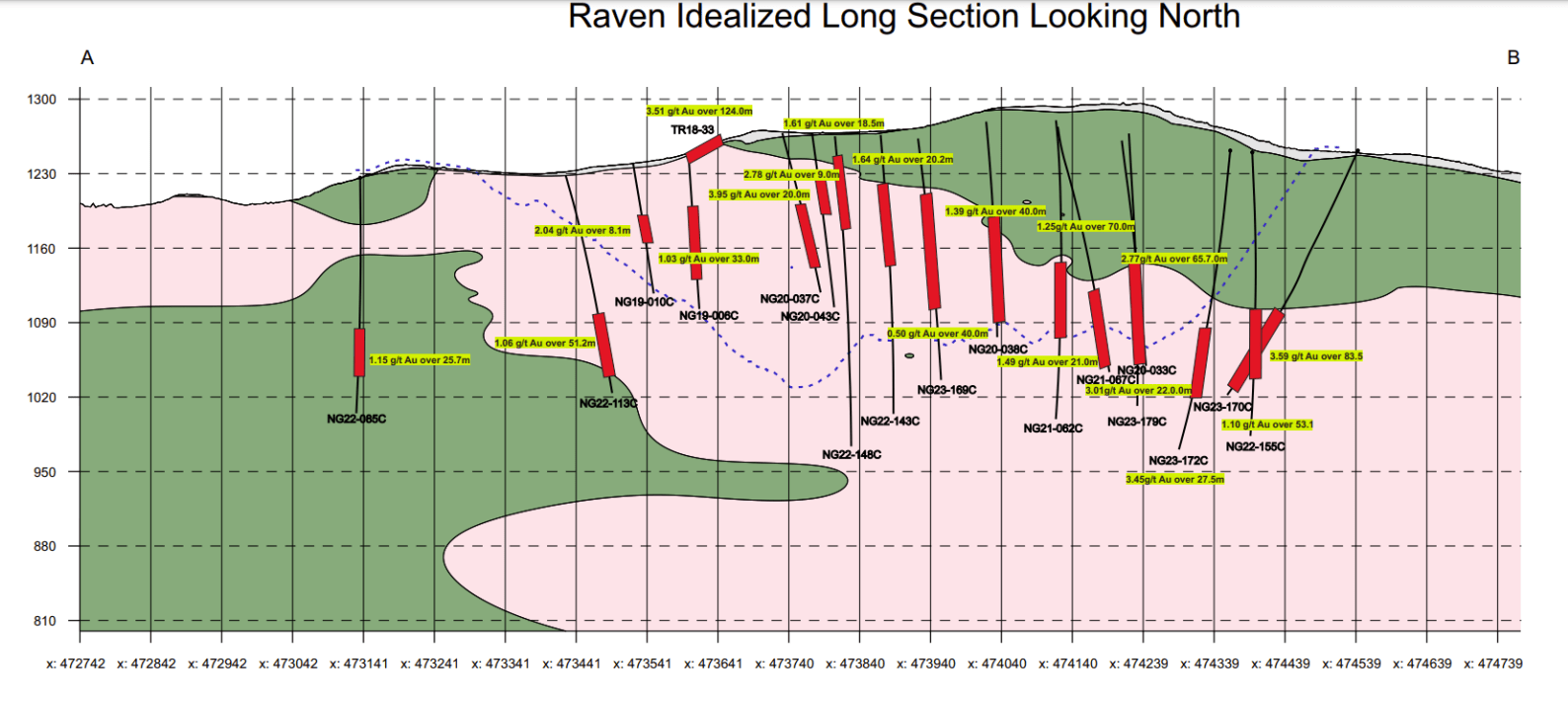

Lastly, I might be remiss to not focus on Raven briefly, a deposit that’s presently house to ~20 million tonnes of fabric (inferred) at 1.67 grams per tonne of gold and a ~1.07 million ounce useful resource foundation. As Victoria famous, a brand new useful resource is due out at Raven in Q1 2024 and we have seen a 20% plus improve within the strike since Victoria launched a maiden useful resource in 2022. As well as, latest exploration outcomes have been distinctive, with strong grades over thick intercepts, together with highlights like 83.5 meters at 3.59 grams per tonne of gold, 25.7 meters at 1.15 grams per tonne of gold, plus 31.4 meters at 5.83 grams per tonne of gold, and 27.5 meters of three.45 grams per tonne of gold extra just lately. Simply as noteworthy, the corporate has hit some very vital base steel intercepts with extraordinarily excessive silver, lead, and zinc values, together with 2.7 meters at 311 grams per tonne of silver and 57.1% lead/zinc, and 14.7 meters of three.9 grams per tonne of gold, 74 grams per tonne of silver and 6.5% lead/zinc.

Raven Step Out Drilling – Firm Filings

Victoria shared that “it was not until late 2022 that their potential (high-grade sulphosalt bearing base metal veins) as consistent veins distinct from the gold-bearing massive sulphide was recognized and analytical over-limit procedures were established on all core samples.” The corporate shared that the put up discipline season work will embody reviewing these veins and unbiased modeling, and it will probably conduct over-limit assays on intervals of notice if required on condition that it has maintained the coarse rejects and pulps from all 2018-2023 drilling. General, this definitely provides one other dimension to Raven, and Raven already appears prefer it might finally develop to ~2.0 million ounces at 1.8+ grams per tonne of gold. And whereas this may require a special processing technique from current infrastructure at Eagle, it is definitely encouraging to see a possible second mine on the identical property east of Eagle.

Victoria Gold Properties & Different Deposits/Mines – Firm Presentation

Valuation

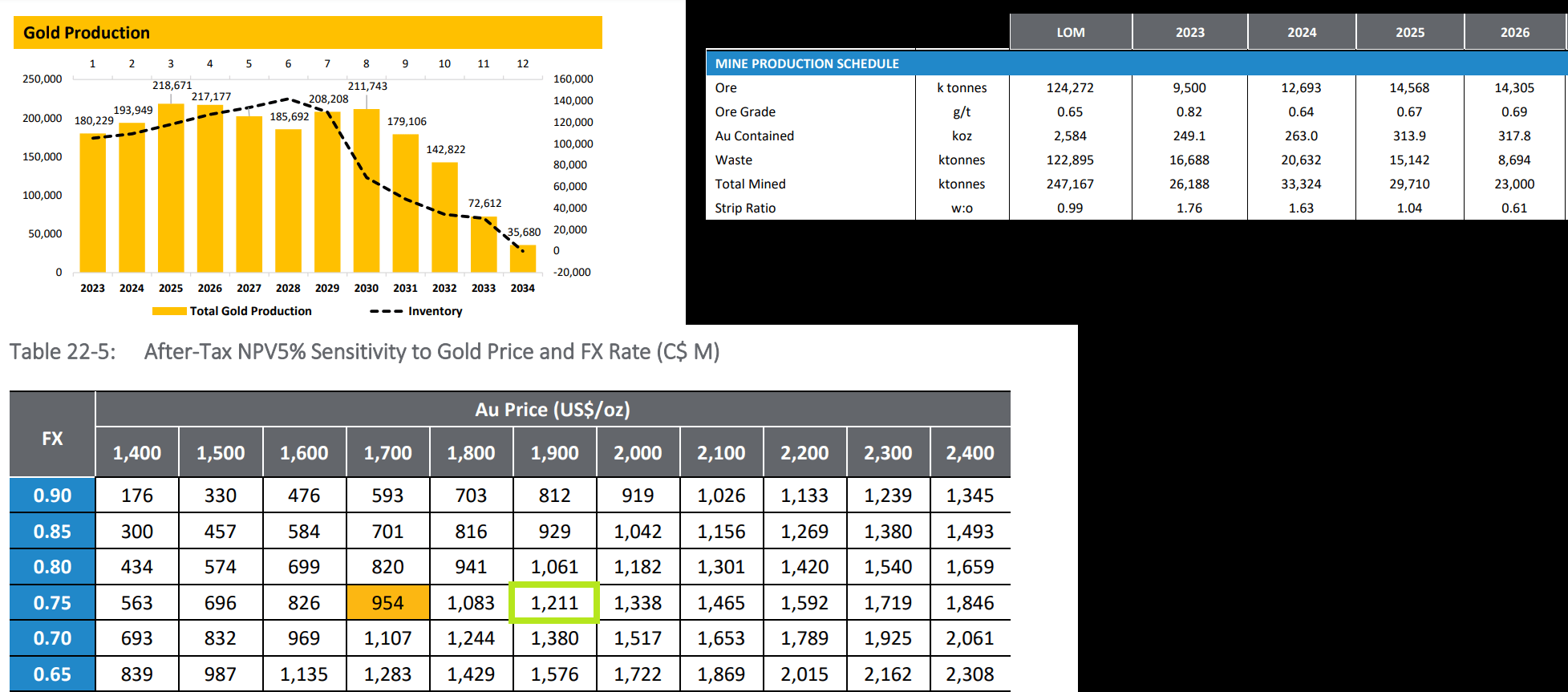

Based mostly on ~68 million absolutely diluted shares and a share worth of US$5.20, Victoria trades at a market cap of ~$350 million and an enterprise worth of ~$520 million. This represents a big low cost to its estimated web asset worth of ~$720 million ($1,875/ozgold worth, with $100 million in exploration upside for non-operating belongings), leaving the inventory buying and selling at simply ~0.50x P/NAV, and one of many decrease P/NAV multiples in its peer group. Plus, it is necessary to notice that Eagle continues to have upside at depth (mineralization continues to ~800 meters) and to the west of the reserve pit, with drilling extending Eagle mineralization 500 meters alongside strike. Lastly, if the gold worth can maintain above the $1,950/ozlevel and common $2,000/ozover the remainder of the mine life, there’s materials upside to the mine’s estimated after-tax NPV (5%), as proven beneath.

Because the desk beneath highlights, Eagle’s After-Tax NPV (5%) is C$1.34 billion [US$1.0 billion] at $2,000/ozgold, and even factoring in inflationary pressures, this nonetheless factors to an After-Tax NPV (5%) nicely above the ~US$715 million NPV (5%) on the base case $1,700/ozgold worth.

Victoria Gold After-Tax NPV Sensitivity & Mine Schedule – Firm Filings, 2022 TR

As free of charge money move era, the corporate lastly seems to have ironed out the kinks at Eagle and whereas Venture 250 made much less sense from a return standpoint given the influence of inflationary pressures, a brand new Common Supervisor and fewer seasonality suggests a extra constant a number of years forward at Eagle. This transition to extra constant operations is handy timing when mixed with a gold worth that’s repeatedly making increased lows and hanging out close to all-time highs, and manufacturing ought to common ~200,000 ounces over the subsequent six years with a decrease strip and decrease capital expenditures. Therefore, Eagle needs to be a free money move machine going ahead, with the potential to generate ~$105 million in FY2025 free money move at a $2,000/ozgold worth. And if we examine this determine to its present market cap of ~$350 million, leaving it buying and selling at ~3.3x FY2025 free money move.

On an EV/FCF foundation and assuming whole web debt of ~$70 million, Victoria’s FY2025 EV/FCF a number of sits at ~4.0x.

Subsequently, irrespective of the way you slice it, Victoria is dirt-cheap even after its latest rally, and even at a comparatively conservative a number of of 7x free money move, the inventory might commerce at US$9.80 (2-year worth goal).

Abstract

Victoria Gold had a mediocre Q3 resulting from occasions exterior of its management however operations are operating higher total, it is obtained a tailwind from the gold worth at its again, and we’re heading into increased manufacturing and decrease strip years over the subsequent few years. This could morph Victoria Gold from a high-cost producer right into a extra common value producer and from a mine producing some free money move to 1 producing over $100 million in free money move post-2024. And with the inventory buying and selling at one of many lowest free money move multiples sector-wide, I believe there’s appreciable upside left within the inventory. In abstract, I might view any sharp pullbacks as shopping for alternatives.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.