Thais Ceneviva/E+ by way of Getty Photos

Viking Therapeutics’ (NASDAQ:VKTX) most superior pipeline candidate is VK2809, a drug for non-alcoholic steatohepatitis (NASH). Lots of the joy surrounding VKTX proper now, nevertheless, pertains to its weight problems drug, VK2735 (the drug additionally has potential in varied metabolic problems together with diabetes and NASH).

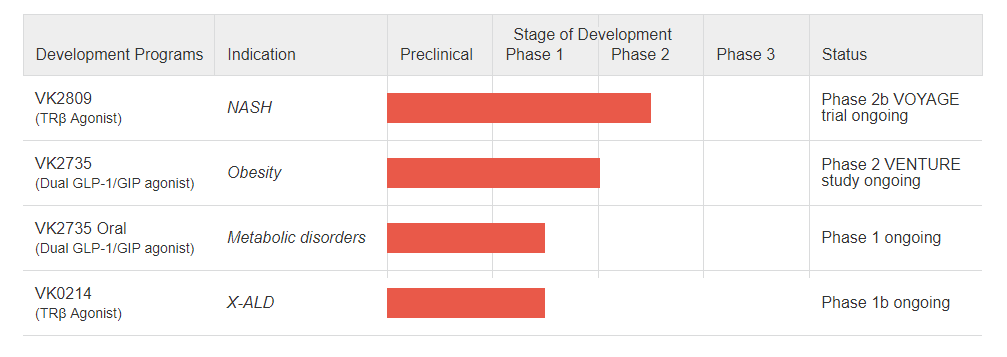

Determine 1: VKTX pipeline. (Firm web site.)

Incretin builders are rallying proper now

On December 4, Roche (OTCQX:RHHBY) introduced a merger settlement to acquire Carmot Therapeutics (which was about to IPO) for $2.7B in money, and as much as $400M in milestones. The deal sees RHHBY come up with Carmot’s pipeline of incretins, together with the part 2 prepared drug CT-388, which is an agonist of glucagon-like peptide 1 (GLP-1) and glucose-dependent insulinotropic polypeptide (GIP) receptors. Observe, Eli Lilly’s (LLY) Mounjaro (tirzepatide) can also be a twin GLP-1 receptor/GIP receptor agonist. Knowledge from a part 1/2 trial of CT-388, presented at the American Diabetes Affiliation Scientific Session in June 2023, famous 8% physique weight discount in simply 4 weeks in overweight and obese adults.

Outdoors of the acquisition, Pfizer’s middling results, introduced on December 1, with its oral GLP-1 receptor agonist, danuglipron, when dosed twice day by day, clears the trail for different incretin builders to have success.

What does it imply for VKTX?

For VKTX, the corporate’s VK2735 makes it a possible acquisition goal itself. Like Mounjaro and CT-388, VK2735 is a twin agonist of GLP-1 and GIP receptors.

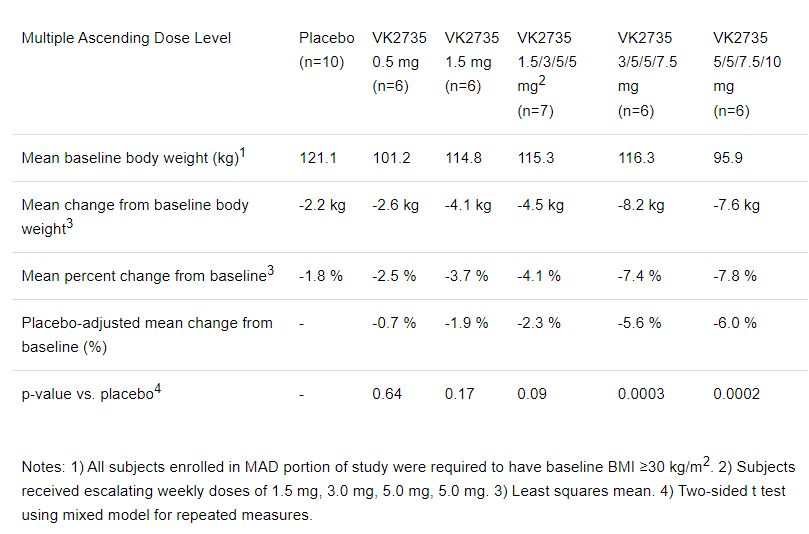

VKTX reported results in March 2023 from a randomized, placebo-controlled, double-blind part 1 research of VK2735 in overweight adults. That research confirmed 7.8% discount in body weight, from baseline to twenty-eight days, with the best dosing routine of VK2735 (vs simply 1.8% for placebo, P < 0.0002).

Determine 2: Screenshot of desk from VKTX press launch regarding outcomes from a part 1 research of VK2735. Observe the dose-response relationship. (March 28, 2023, press launch from VKTX.)

It is onerous to not discover the 7.8% discount in body weight, at 4 weeks with VK2735, is just like what Carmot Therapeutics produced with CT-388, and that firm simply acquired purchased out for $2.7B. Whereas that research used a subcutaneous formulation of VK2735, administered as soon as weekly, VKTX additionally has an oral formulation in growth. A part 1 trial trying on the oral formulation is anticipated to report ends in Q1’24.

Past the advantages of the drug on body weight in overweight adults, VK2735 additionally produced reductions in liver fats. The ends in the group of sufferers with non-alcoholic fatty liver illness (NAFLD) have been significantly spectacular the place a 58.5% placebo-adjusted discount in liver fats was proven.

VKTX2735’s subsequent act: Timing the readout

Whereas the part 1 knowledge with VK2735 was spectacular, I estimate we’re near a readout from VKTX2735’s subsequent act, outcomes from a part 2 trial known as VENTURE. The VENTURE research is a randomized, double-blind, placebo-controlled, 13-week research of VK2735 (subcutaneous, once-weekly) in overweight adults. Whereas the research had initially deliberate to enroll 125 adults, elevated demand has seen the corporate enroll 176 trial individuals. The first endpoint is the change in body weight from baseline to week 13 vs placebo.

I count on the VENTURE trial to hit the first endpoint, however that is not a lot of a prediction given the mechanism of the drug, we all know these brokers trigger weight reduction, and the part 1 knowledge. What might be extra in focus is simply how a lot weight reduction is seen and the charges of adversarial occasions. Given the mechanism of VK2735 is just like the extremely efficient Mounjaro, and the compelling weight reduction knowledge seen at 4 weeks, I believe we will count on some fairly spectacular weight reduction numbers from VENTURE. One thing additional to contemplate is that whereas the four-week research included within the part 1 work for VK2735 used a highest dose of 10 mg, the part 2 work features a dose group at 15 mg VK2735. As such, the potential to provide much more spectacular weight reduction numbers is in play.

On October 23, 2023, VKTX introduced that enrollment in VENTURE was full, and given the 13-week length of the trial, I calculate the research would full dosing on January 22, 2024. Whereas VKTX has guided to a H1’24 readout from the VENTURE research, that’s fairly conservative, given I doubt it’s going to even take till February 22 (a month later) to report topline outcomes. There’s a four-week follow-up interval constructed into the research, however VKTX would possibly current that knowledge later. If VKTX does anticipate that a part of the research to finish, I would transfer my prediction for outcomes one other 4 weeks ahead into March. Even then, I see outcomes as being due in Q1’24.

Monetary Overview

VKTX had money, money equivalents and marketable securities of $376M on the finish of Q3’23. R&D bills for Q3’23 have been $18.4M and G&A bills have been $8.9M in the identical quarter. Web loss in Q3’23 was $22.5M, and internet money utilized in working actions was $55.7M within the first 9 months of 2023. At that charge VKTX would have money for twenty quarters, or 5 years from the top of 2023. In actuality, if VKTX sees success with its pipeline members, it’s going to transfer them additional down the pipeline, into greater research and money burn will decide up. Proper now although, VKTX is definitely effectively funded.

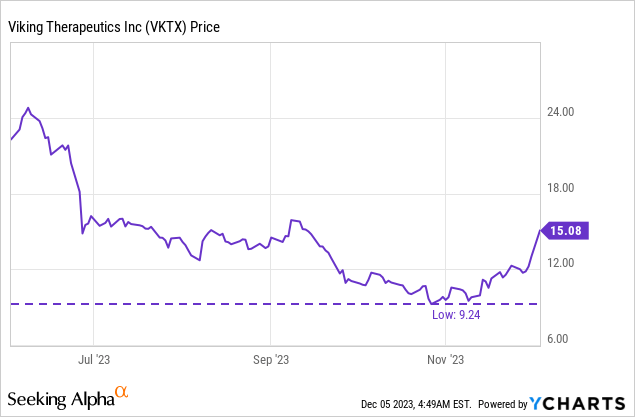

There have been 100,028,953 shares of VKTX’s frequent inventory excellent as of October 15, giving VKTX a market cap of $1.51B ($15.08 per share). There are additionally 5,243,807 inventory choices excellent (weighted common train worth of $6.78), though solely 2,380,983 have been exercisable as of September 30, 2023, and an extra 2,855,656 unvested restricted inventory items as of September 30, 2023.

Different catalysts on faucet

VK2809 is VKTX’s most superior drug, a thyroid hormone receptor-beta (THR-beta) agonist, which is in a part 2b research in NASH sufferers known as VOYAGE. VKTX has already reported knowledge from the research displaying considerably larger liver fats reductions at 12-weeks than placebo, which means the research hit the first endpoint. VKTX is planning to report longer-term knowledge nevertheless, with biopsy knowledge from 52 weeks of remedy being offered in H1’24. This knowledge might be vital, however the efficacy of VK2809 is already recognized, so beating placebo will not be sufficient, as a substitute there might be a comparability to different NASH medication like Madrigal’s (MDGL) resmetirom.

Outdoors of VK2809, the corporate has a second THR-beta agonist known as VK0214. A phase 1b research of VK0214 in sufferers with adrenomyeloneuropathy (AMN), the commonest type of X-linked adrenoleukodystrophy (x-ALD), is anticipated to finish enrolment in This autumn’23. There isn’t any efficacy knowledge with VK0214 to look at at present in AMN sufferers, so any prediction goes to be fairly the gamble.

The part 1b research is a randomized, double-blind, placebo-controlled research, so there may be potential to indicate a major beat of placebo on efficacy endpoints. For instance, VK0214 would possibly be capable of produce a major discount within the plasma stage of very lengthy chain fatty acids (VLCFA’s, which accumulate in X-ALD sufferers). The research has an anticipated enrollment of 36 sufferers.

Conclusions, scores and dangers

VKTX seems to have 4 catalyst on faucet in H1’24. Certainly, a key readout from the VENTURE research of VK2735 might come by mid-February, and be complemented by knowledge from the oral formulation of VK2735 in the identical quarter. The weight problems knowledge with VK2735 is especially related now because the market is aware of the potential for buyouts of weight reduction names. Certainly, VKTX is up over 60% because the lows in late October. Certain, some further analyses from VOYAGE, offered at a medical conference in mid-November, have helped the inventory rally too. The previous few buying and selling periods nevertheless, following information of PFE’s points with danuglipron and the RHHBY buyout of Carmot, have produced a very notable rally.

I fear then, on the time I am writing this text, that VKTX could be due for a small pullback, as those that purchased into the identify (day merchants, swing merchants) would possibly promote and transfer on. That does not imply the buyout potential is gone, neither is the potential for a runup, into VKTX’s medical readouts, to then begin once more following this hypothetical pullback.

Additional, VKTX trades with an enterprise worth of over $1.1B, regardless of having no authorized drug, so the pipeline has already taken on some worth. Even when we see incretins for weight reduction (and diabetes, amongst different metabolic situations) as being price billions, there may be room for VKTX to fall. For these causes I cease in need of ranking VKTX a powerful purchase, however I’ll charge it as a purchase, regardless of the very fact there could be a pullback this week, I believe the runup into Q1’24 outcomes will exceed that, and buyout hypothesis will stay in play.

The dangers of any lengthy in VKTX are a number of fold, just a few of which I am going to focus on. Firstly, the danger of a near-term pullback is definitely in play. Two key items of stories within the first few buying and selling periods of December (PFE points with danuglipron, RHHBY acquisition of Carmot) have led to an quantity of pleasure that might be onerous to maintain. We aren’t going to maintain getting information of an incretin struggling, or an organization being purchased out, each few days. Maybe each few weeks or months, however not each few days.

Past the short-term danger of a pullback as merchants take earnings and transfer elsewhere, long term, if VKTX’s pipeline would not carry out, the inventory might fall. If the oral formulation of VK2735 has too many unwanted side effects, or far much less efficacy, it will not create pleasure, for instance, and the inventory might truly fall.

Lastly, opponents could make advances with their very own incretins, displaying comparable or higher weight reduction numbers, or much less unwanted side effects, which might trigger VKTX to commerce down.